The Week Ahead - 3/22/26

A comprehensive look at the upcoming week for US economics, equities and fixed income (including earnings, the Fed, valuations, positioning, breadth, sentiment, and seasonality)

If you're a new reader or maybe one who doesn’t make it to the end feel free to take a second to subscribe now.

Or take a moment to invite others who might be interested to check it out (it’s appreciated!).

Please note that I do sometimes add to or tweak items after first publishing, so it’s usually safest to read it from the website where it will have any updates.

As a reminder, some things I leave in from prior weeks for reference purposes, because it’s in-between updates, it provides background information, etc.. Anything not updated this week is in italics. As always apologize for typos, errors, etc., as there’s a lot here, and I don’t really have time to do a thorough double-check.

For new subscribers, this is a relatively long post. The intent is to cover the same areas each week. Sometimes the various areas are more interesting, sometimes less, but it’s easier just to go through them all, so you can expect this format (with things in the same places) each week.

The main sections are intended to cover 1) what’s upcoming next week, 2) what the Fed and rates markets are up to, 3) what’s going on with earnings (the most important determinate to stock prices over the long term (along with valuations (the price paid for those earnings))), 4) what’s going on with the economy (both because of its impact on our daily lives but also because it impacts earnings), 5) valuations (for the reason noted), 6) breadth (which gets into sector/style performance), 7) positioning/flows (this is the largest determinant to equity price changes in the short term), 8) sentiment (really only matters at extremes but interesting to track), 9) seasonality (gives you an idea of what normally happens), 10) “Final Thoughts” and 11) my portfolio (to be transparent about where my money is in the market (but note first it is most definitely not intended as financial advice, and second my portfolio is invested with the intention of wealth building not daily income, etc., so my portfolio is built with that in mind (plus see note about MLP’s in that section)).

A continued thank you to the many who have contributed to the charity fund. I appreciate very much each paid membership, and I have tried to respond to all messages from paid members. If you have sent me a message, and I have not responded, please don’t hesitate to send a new message, as it likely was just buried in my email inbox.

Also, a few readers mentioned that the volume of material can feel like a lot to get through. That’s understandable, especially as different readers find value from different parts of the subscription. But everything I publish is meant to stand on its own (often even each section), so please feel free to read whatever is most useful and skip the rest.

I have also continued to remove some things to try to clean up the flow. If I remove something that you would like in, just let me know, and I’ll see what I can do. As always, feedback is welcome.

Note: Next week’s Week Ahead will be abbreviated as I am competing at the IBJJF Pan-American Championships in Orlando next weekend.

The Week Ahead

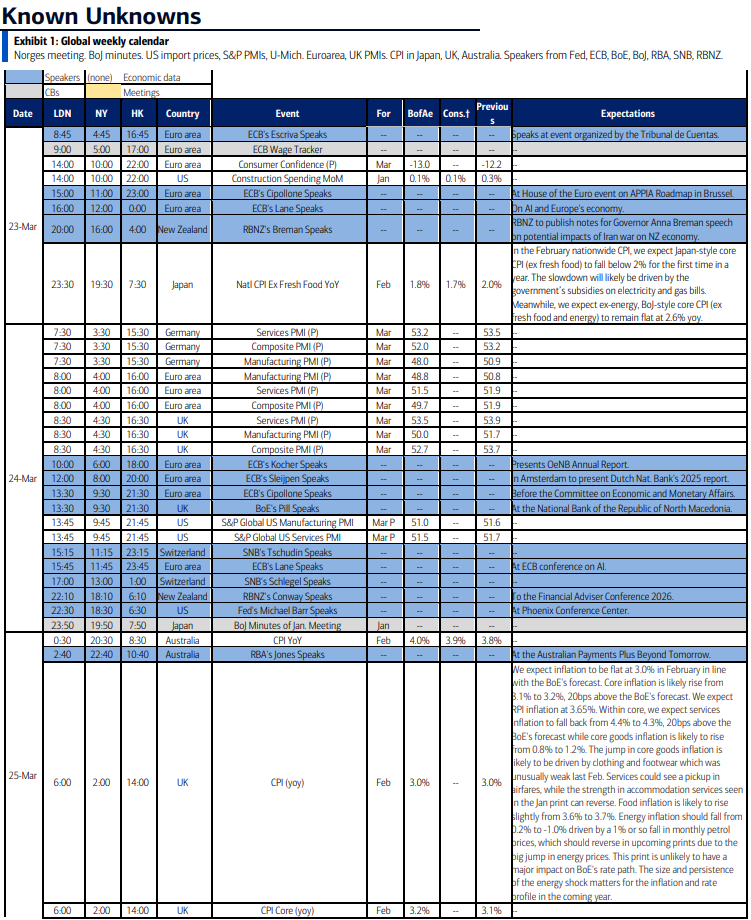

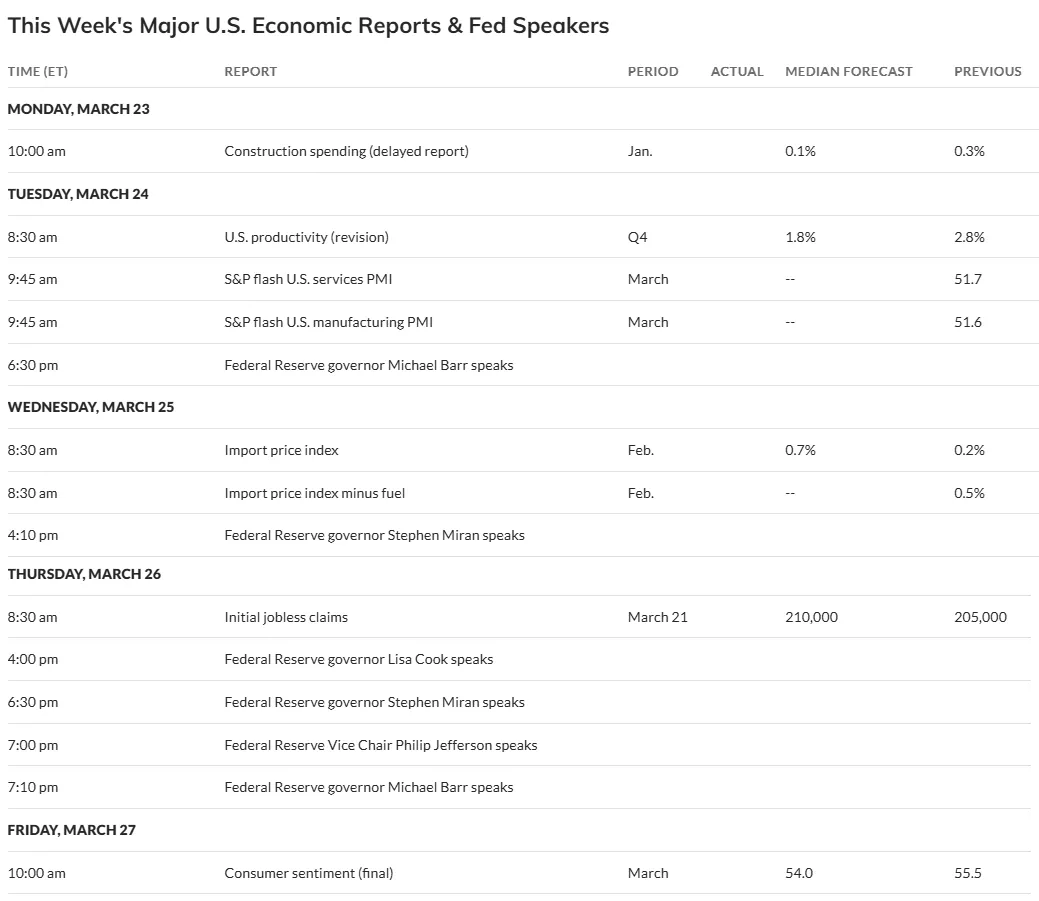

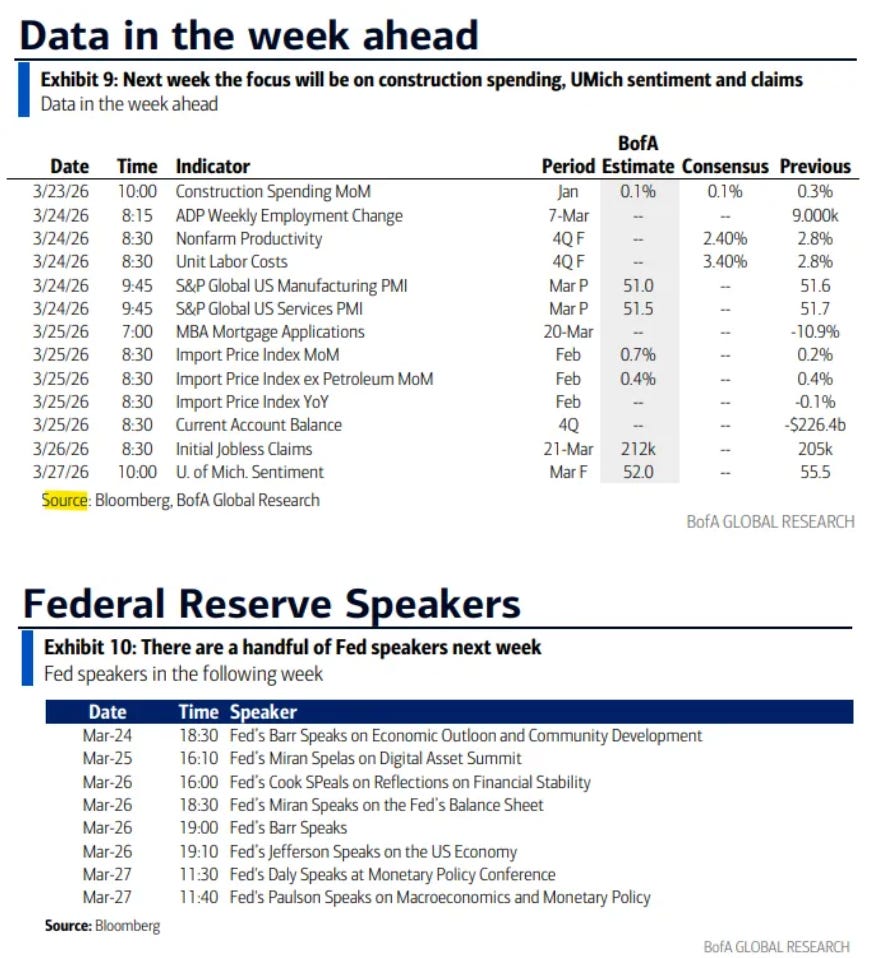

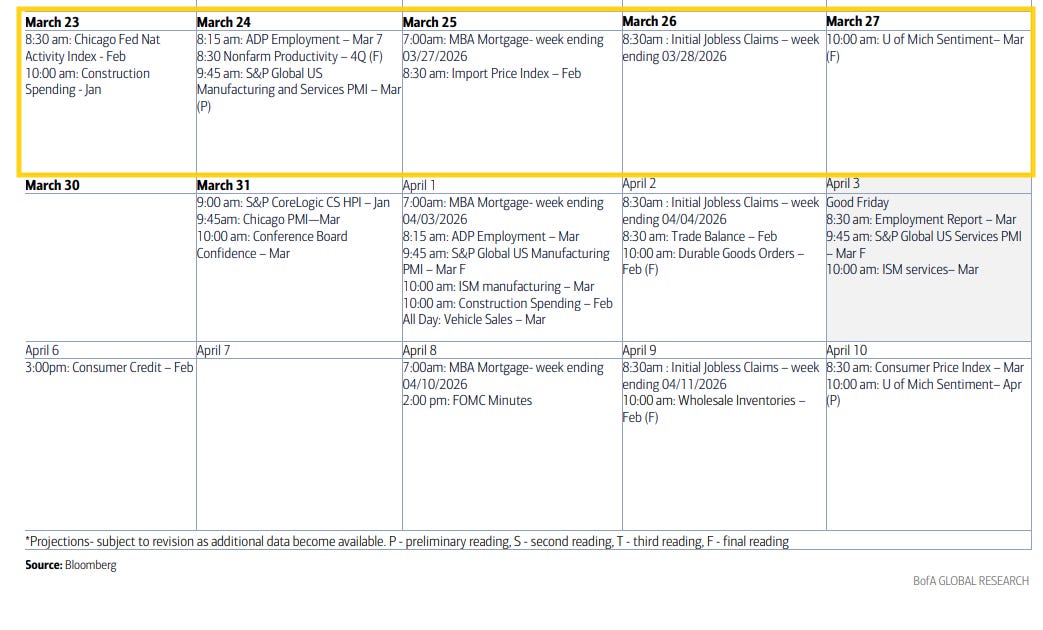

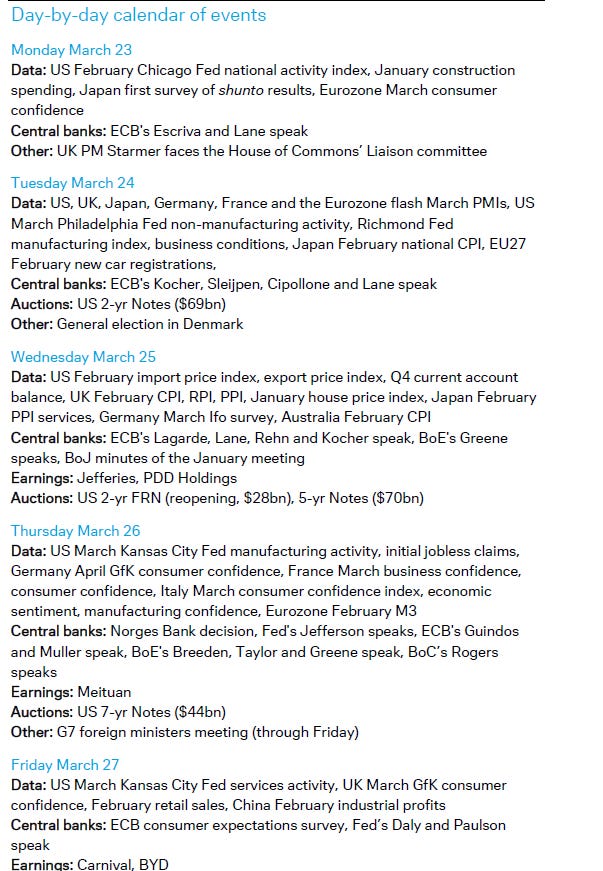

The upcoming week is the lightest in a while for US economic data with again no top-tier releases (normally we’d get the February personal income and spending report on Friday, but that’s not coming until April 9th), but we will get Feb Chicago Fed National Activity Index (correlates well with GDP), import prices, March flash PMIs (which seem to have fallen to third-tier data status) and final UMich sentiment, a delayed Jan construction spending report and final Q4 productivity plus the standard weekly reports (ADP, jobless claims, etc.).

The Fed speaking blackout is over (we had Waller and Bowman already Friday), so you can expect plenty of appearances. As of now, there’s Gov’s Barr, Cook, Miran, Jefferson and regional bank presidents Daly and Paulson, and there will be plenty more most likely.

Non-bill Treasury auctions (>1yr in duration) give us 2, 5, and 7-years on Tues, Wed, Thurs respectively.

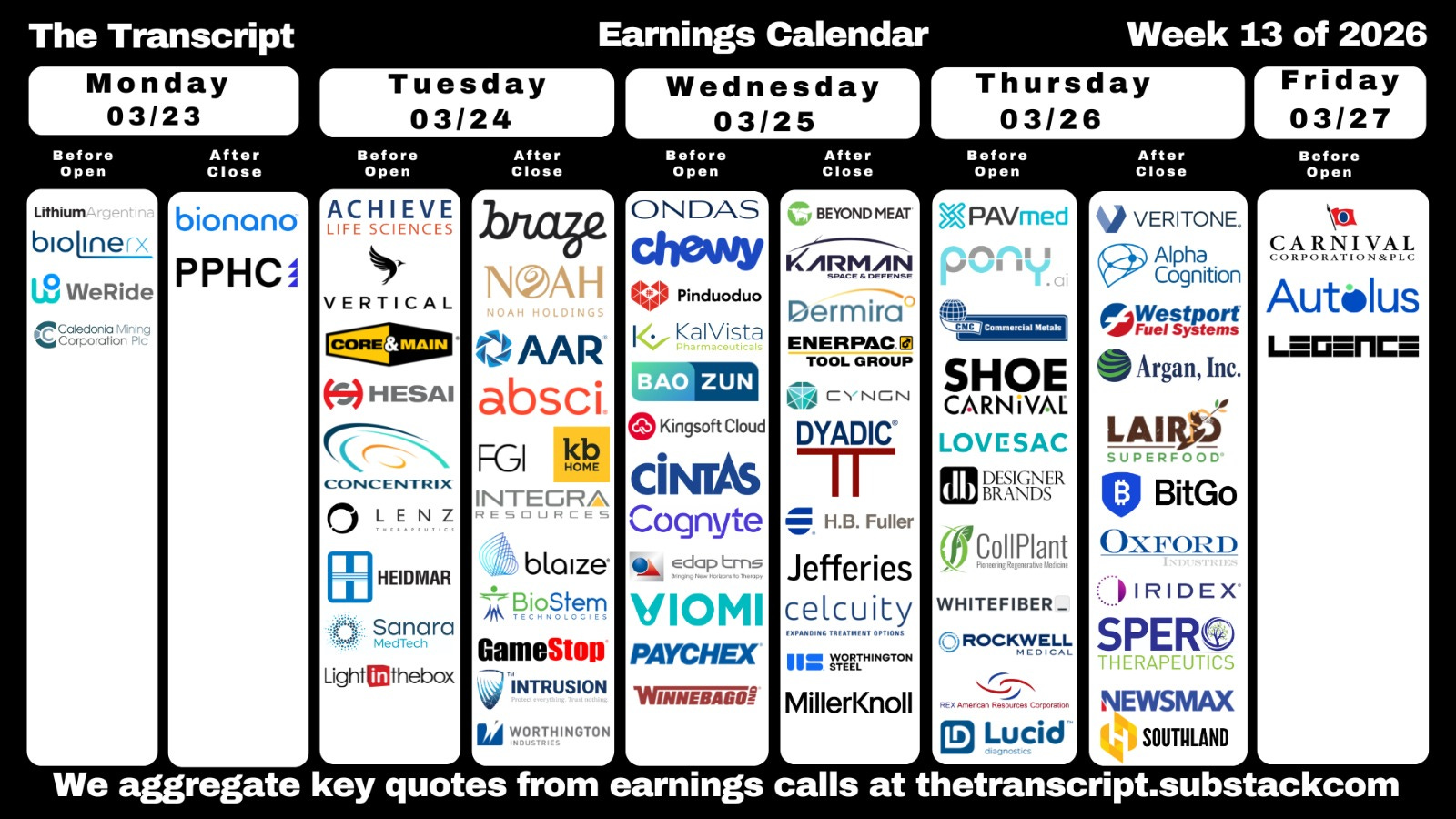

Q4 earnings season continues to wind down but just three SPX reporters next week CTAS, PAYX, CCL.

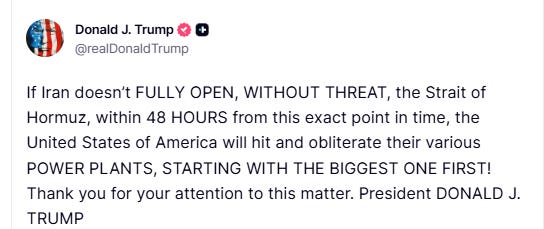

Of course overshadowing most all of that will continue to be what’s going on with Iran. As of now I continue to believe, as I have since it began, the duration of this conflict will end up being measured in weeks not months (if only to get energy and other prices (it’s feeding into food prices, etc.) back down and otherwise assuage his base, which is not thrilled about foreign entanglements, ahead of the mid-terms), but as I noted last week “I have to respect that consensus (if Polymarket can be considered consensus)” is that this will stretch out past April with just a 40% chance of it ending by then (down from 50% a week ago).”

So while on the one hand I do think it will be “weeks,” as I noted last week “it does seem the conflict will likely extend into April. I still have a hard time believing this goes past April, but quite honestly the whole thing has surprised me thus far.” It does seem over the weekend that Pres Trump is looking to escalate things to perhaps force a resolution by declaring that Iran has until “exactly” 7.44pm ET Monday to “fully reopen, without threat” the Strait of Hormuz or he will “obliterate their various power plants”.

And while we did get the IEEPA decision from the Supreme Court we’re still waiting on the Lisa Cook opinion which we’ll get at some point. And that IEEPA decision has unleashed an entire new round of tariff uncertainty, which will continue, if in the background. While my base case has been that things will end up not far off from where they were prior to the decision, you never know with these things although it does seem that markets have settled into this “new normal”.

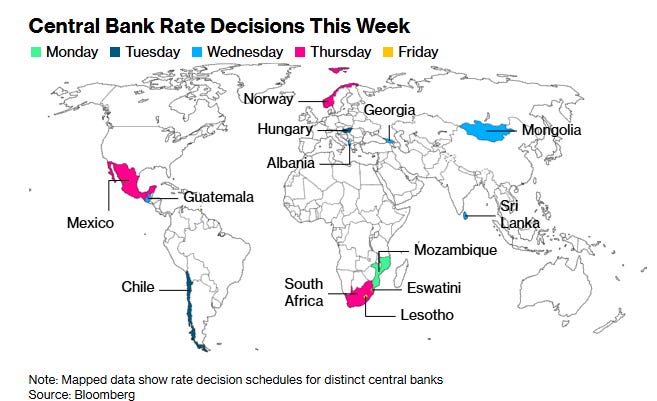

Ex-US highlights are also the flash PMIs, inflation readings from UK, Spain, Japan, and Australia, Germany’s Ifo survey, early Japan shunto wage results, and policy decisions from Norway and Mexico among others.

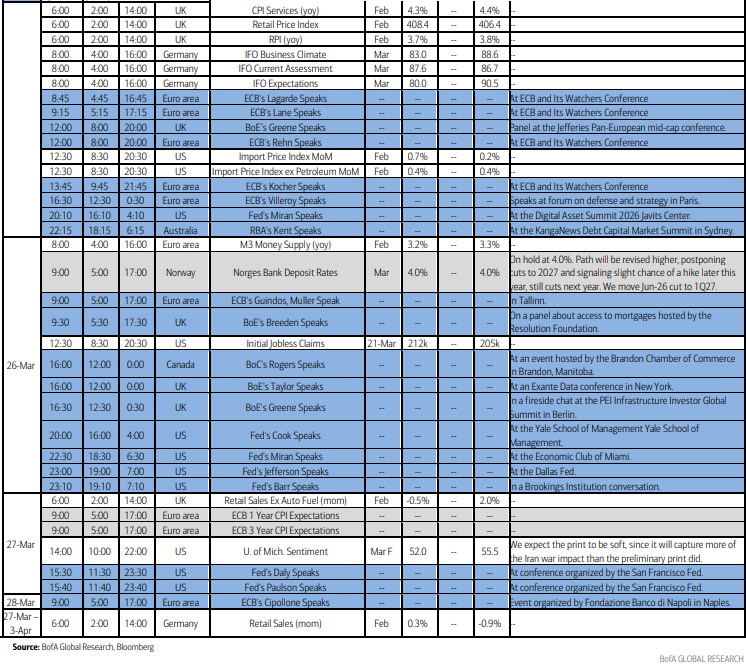

Canada

Bank of Canada Senior Deputy Governor Carolyn Rogers will speak in Brandon, Manitoba, on the forces shaping Canada’s economic outlook and financial system, including this year’s renewal of the monetary policy framework. Meanwhile, flash wholesale and manufacturing data will offer an early read on how two tariff-hit sectors are performing in the first quarter.

Asia

Inflation data will be a focus in Asia. Japan’s consumer price growth moderated in February after utility subsidies reduced energy costs and food price gains eased compared with a year earlier, data on Tuesday are expected to show. The key gauge that excludes fresh food likely slowed below the Bank of Japan’s 2% inflation target for the first time in almost four years. It will probably be a short-lived phenomenon given the surge in oil prices after the March escalation of the Iran war.

The following day, Australia’s CPI will likely show the trimmed mean gauge remained elevated in February, data that will justify the back-to-back hikes undertaken by the Reserve Bank and may underpin bets on another increase to borrowing costs in May. Singapore also releases February CPI in the coming week. Nations releasing PMI figures for March include Australia, Japan and India, with all three expected to report manufacturing gauges stayed in expansionary territory.

China reports year-to-date industrial profits through February on Friday after annual profits eked out a 0.6% gain last year, the first such increase since 2021. Trade figures are due from the Philippines, Thailand, South Korea and Hong Kong, and New Zealand closes out the week with its March consumer confidence report. China’s own trade surplus has caused unease in the past, an issue addressed by Premier Li Qiang at the China Development Forum in Beijing on Sunday. “We take our trading partners’ concerns seriously and we are ready to work with all parties to promote the sound and balanced development of trade,” he said. Speaking at the same event exports continued to boom to start 2026, People’s Bank of China Governor Pan Gongsheng defended his nation’s surplus.

In policy action, Sri Lanka’s central bank is expected to keep its rate steady at 7.75% on Wednesday, extending the streak of holds to five meetings and reinforcing views that the easing cycle may have run its course as authorities eye an expected acceleration in inflation. Meanwhile, South Korea’s president on Sunday nominated Shin Hyun Song, head of the monetary and economic department at the Bank for International Settlements, as the new Bank of Korea governor. Elsewhere, Reserve Bank of New Zealand Governor Anna Breman will outline her thinking on inflation implications from the Middle East conflict in a speech on Tuesday, with economists expecting price growth to breach the top of its 1% to 3% target band for much of the year. Pricing in the overnight swaps market indicates traders are predicting a roughly 42% chance of a hike by July.

Europe, Middle East, Africa

The aftermath of a big week for monetary decisions will reverberate around Europe, with remarks by several policymakers on the schedule as well as some key data. UK inflation numbers on Wednesday are predicted by economists to show the slowdown in annual price growth halted at 3% in February, in a report that will draw particular attention after Britain’s 10-year gilt yield touched the highest since 2008. That market shift followed the Bank of England’s pivot away from rate cuts to declare itself “ready to act.” Deputy Governor Sarah Breeden, chief economist Huw Pill, and rate-setters Megan Greene and Alan Taylor are all scheduled to speak.

From the European Central Bank, which could raise rates if needed as soon as its next decision on April 30, speakers on the calendar include chief economist Philip Lane on Monday. President Christine Lagarde will address the annual ECB and Its Watchers conference in Frankfurt on Wednesday. Swiss National Bank President Martin Schlegel will speak in Zurich on Tuesday following the central bank’s move to restate that its willingness to intervene against war-driven haven flows into the franc has increased. The next day, Sweden’s Riksbank publishes minutes of its own decision, where policymakers kept borrowing costs steady.

Some more monetary meetings are planned for the coming days: On Tuesday, Hungary’s central bank will set rates for the final time before the nation’s make-or-break election, with the energy crisis likely to curb appetite for further cuts. Norwegian officials are poised to keep borrowing costs on hold on Thursday after data showed no significant relief in underlying price pressure and an outlook for a resilient economy. Governor Ida Wolden Bache is expected to signal even less easing than the current view of one quarter-point cut per year. The same day, South Africa’s central bank is expected to hold its rate steady at 6.75% as it assesses inflation fallout from the war that’s weakened the rand and sent oil prices surging.

Latin America

In a busy week for policymaking in Latin America, Brazil’s central bank on Tuesday publishes the minutes of its March 18 decision to deliver a cautious quarter-point cut from a near two-decade high 15%. With the war in the Middle East introducing so much uncertainty, BCB chief Gabriel Galipolo and colleagues offered minimal forward guidance in their post-decision statement and are unlikely to break new ground here. Latin America’s No. 1 economy will also post the BCB’s monetary policy report, mid-month inflation readings, and February unemployment figures.

The war in Iran will also be a factor during central bank meetings in Chile and Mexico. For Banco Central de Chile, the conflict has quite likely turned a possible quarter-point rate cut, from 4.5%, to a definite hold, given that the Andean nation imports nearly all its fuel. For Banxico, the higher oil prices and a weaker peso stemming from the Middle East conflict have likely tipped the balance in LatAm’s No. 2 economy from good odds for a quarter-point cut to a fairly certain hold. Mid-month inflation data posted before Banxico’s board gathers may well cement a decision to keep the key rate at 7% for a second meeting.

Argentina’s January GDP-proxy data are likely to dovetail with the overall cooling seen in South America’s No. 2 economy since the first quarter of 2025. Many analysts see December’s strong output readings as more of a headfake than a trend, and have been marking down their 2026 growth estimates accordingly.

DB one pager:

BoA’s cheat sheets: