The Week Ahead - 5/10/26

A look at the upcoming week for the US economy and equities — covering key drivers including earnings, valuations, positioning, breadth sentiment, seasonality, and the Fed.

The Week Ahead

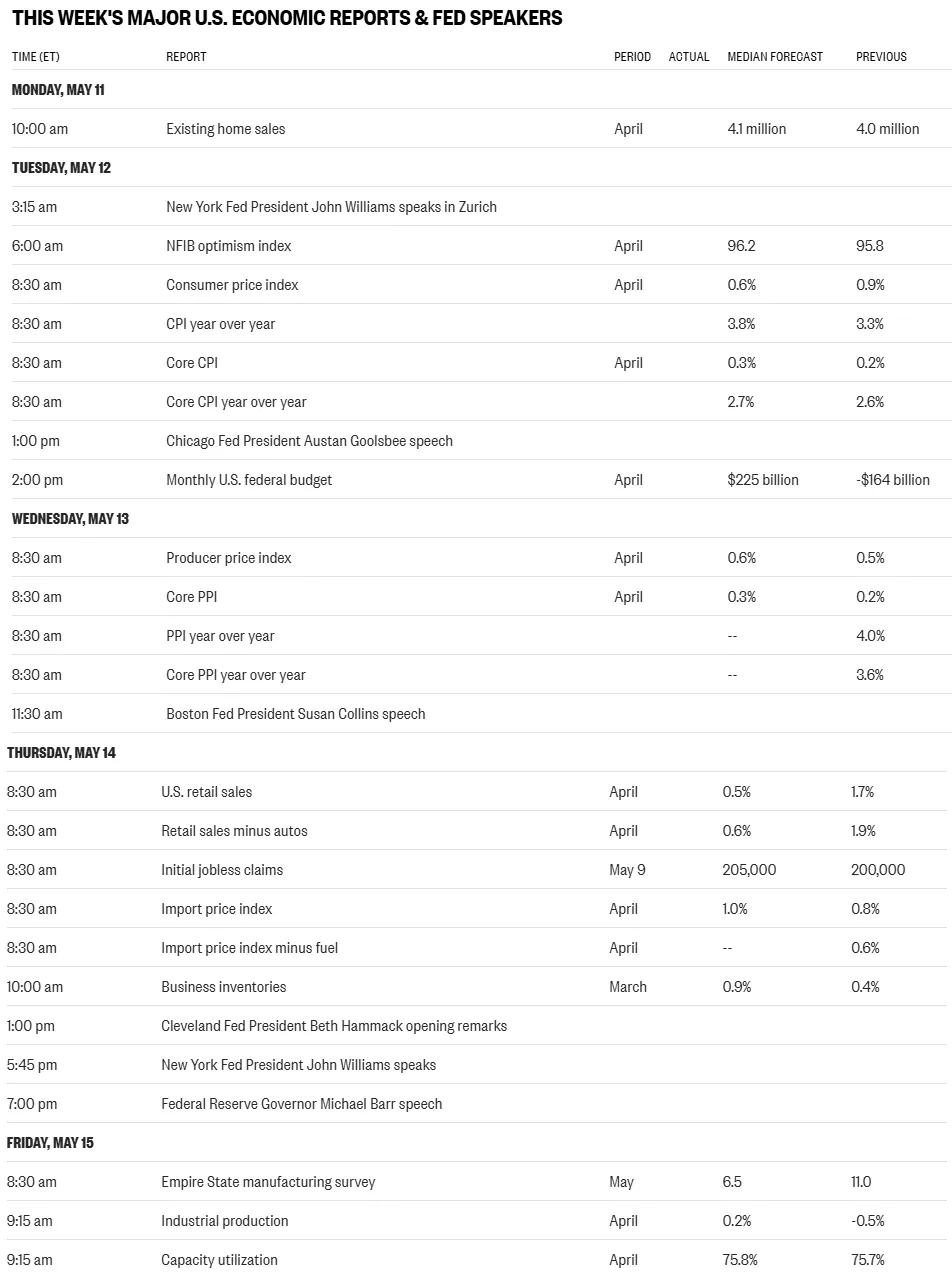

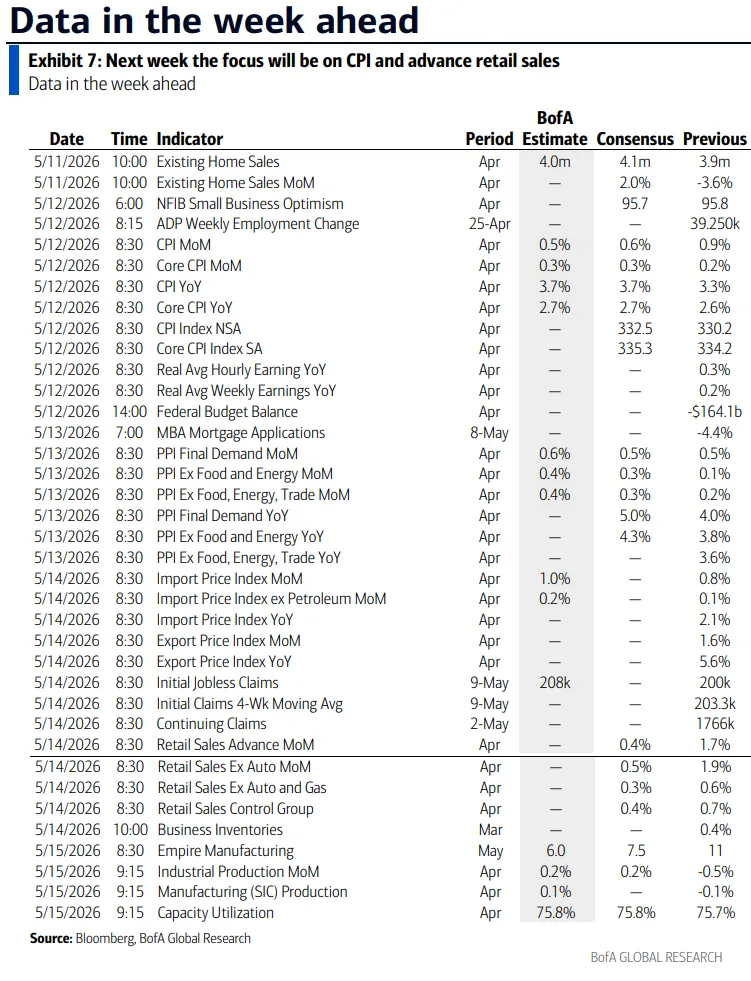

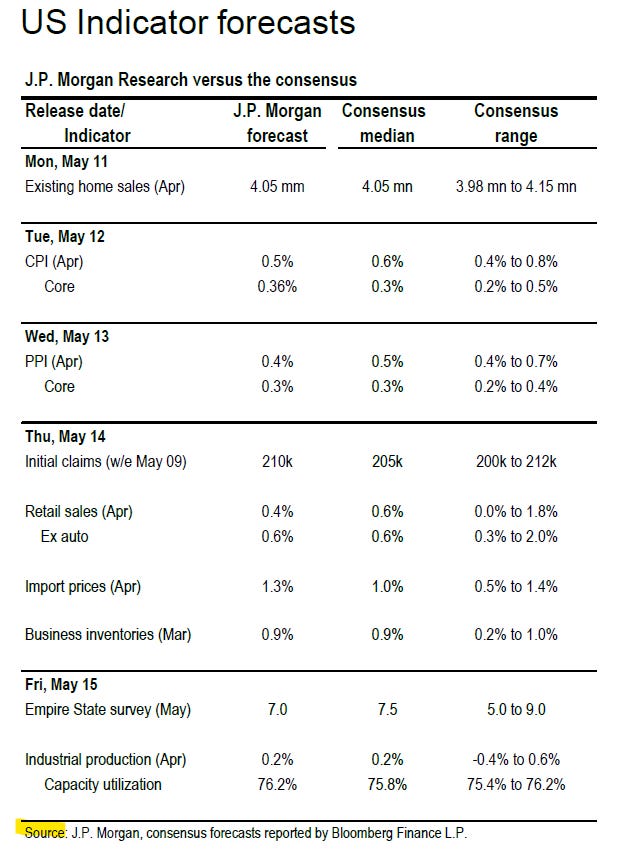

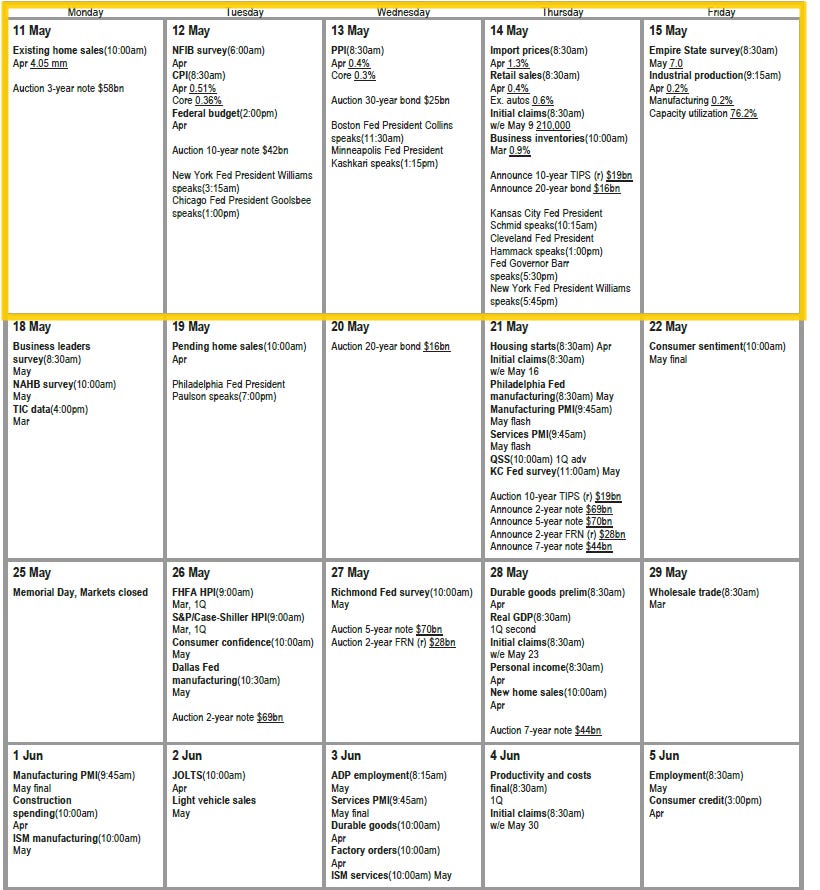

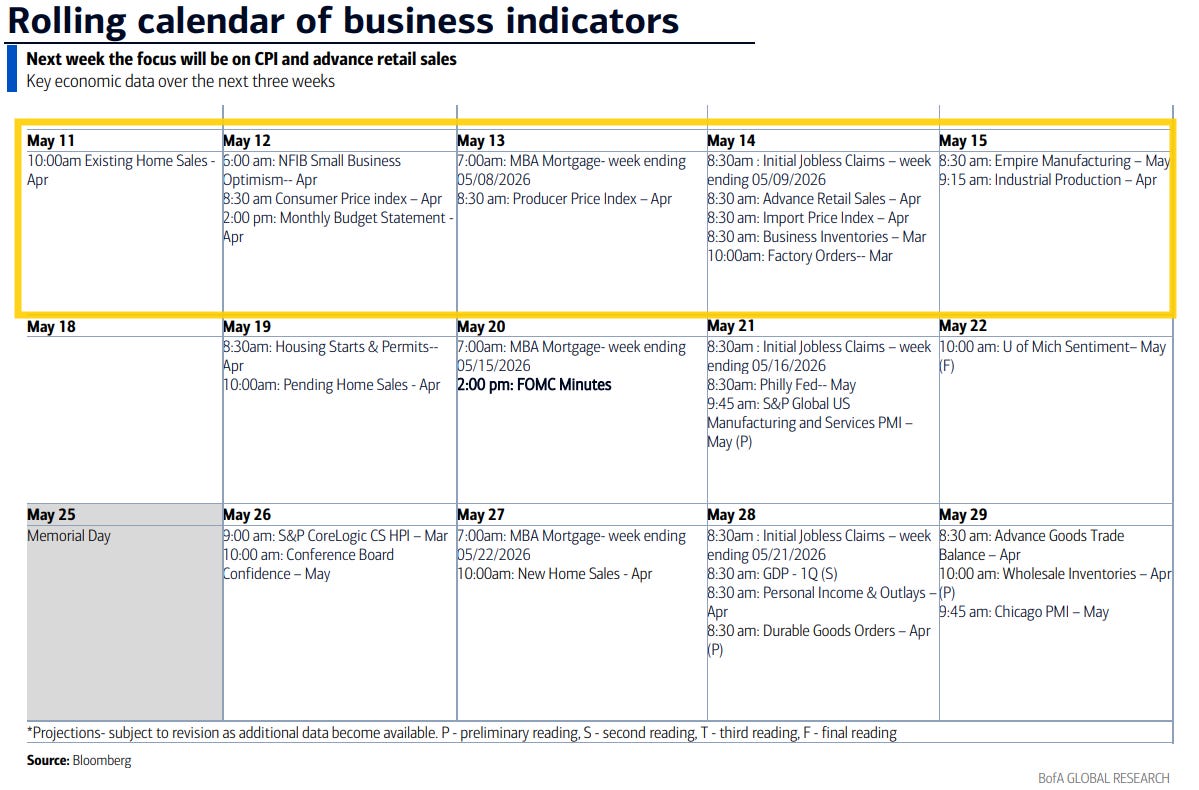

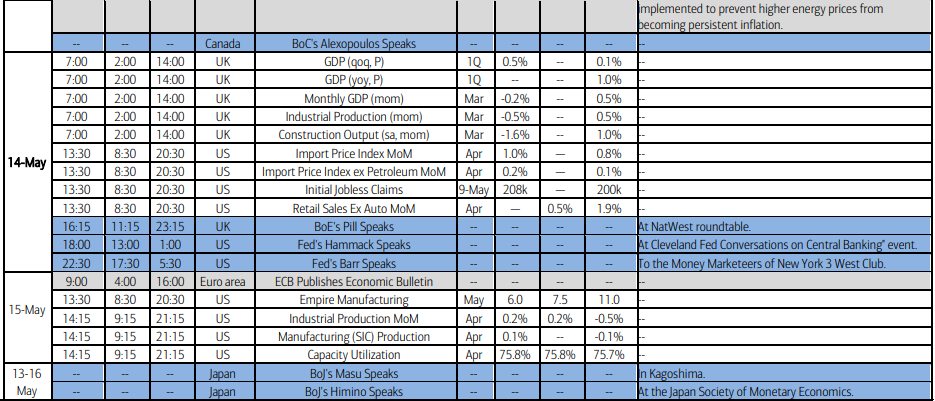

US economic data remains heavy in the week ahead although at least not quite the firehose of the last two weeks. We’ll get two top-tier reports in April CPI and retail sales. Other reports include April PPI, import prices, industrial production, existing home sales, and NFIB small business sentiment as well as the Q1 household debt/credit report and the standard weekly reports (ADP, jobless claims, etc.).

In terms of Fed speakers we’ll get Gov Barr and regional Fed presidents Williams, Goolsbee, Collins, Kashkari, and Hammack, but we know where all of them stand at this point. Also the Senate votes on Monday to confirm Kevin Warsh as the new Fed chair (approval is expected). Jerome Powell’s current term ends Friday. Warsh though still does need to be “elected” by the Board of Governors as head of the FOMC (also expected) once Powell steps down (his term technically runs through the end of the year).

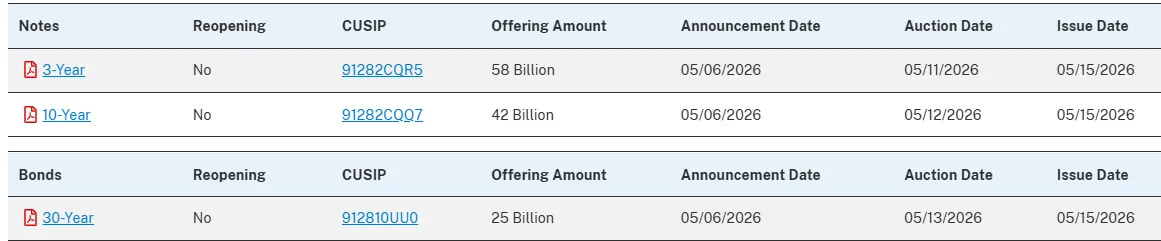

US Treasury auctions pick back up for non-Bills (>1yr in duration) with 3, 10, and 30-yr auctions Mon, Tues, Wed, respectively (a day earlier than normal due to Friday’s settlement).

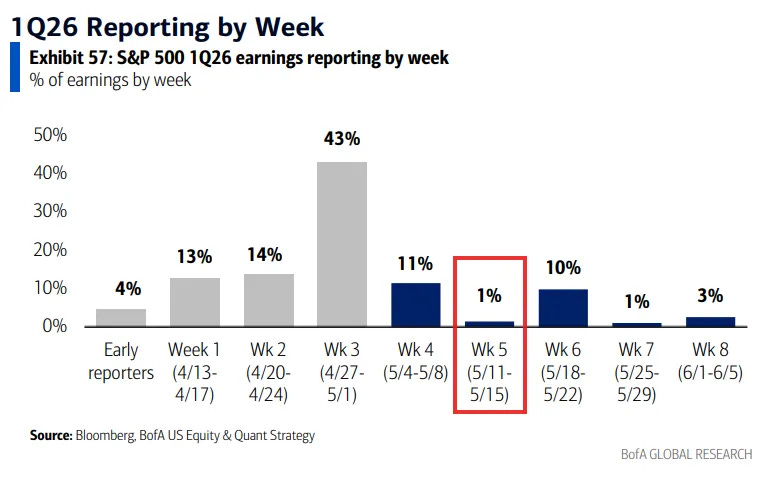

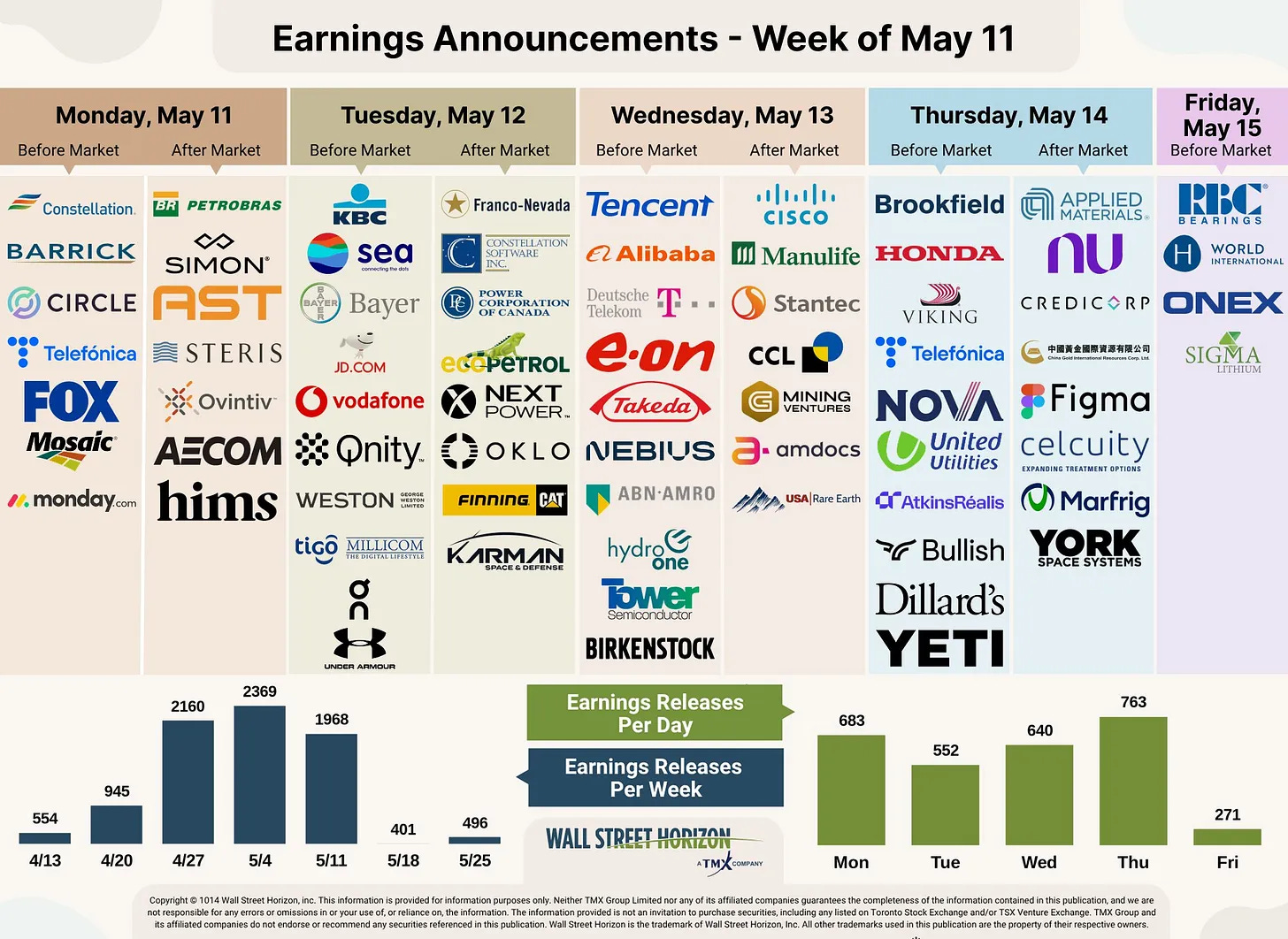

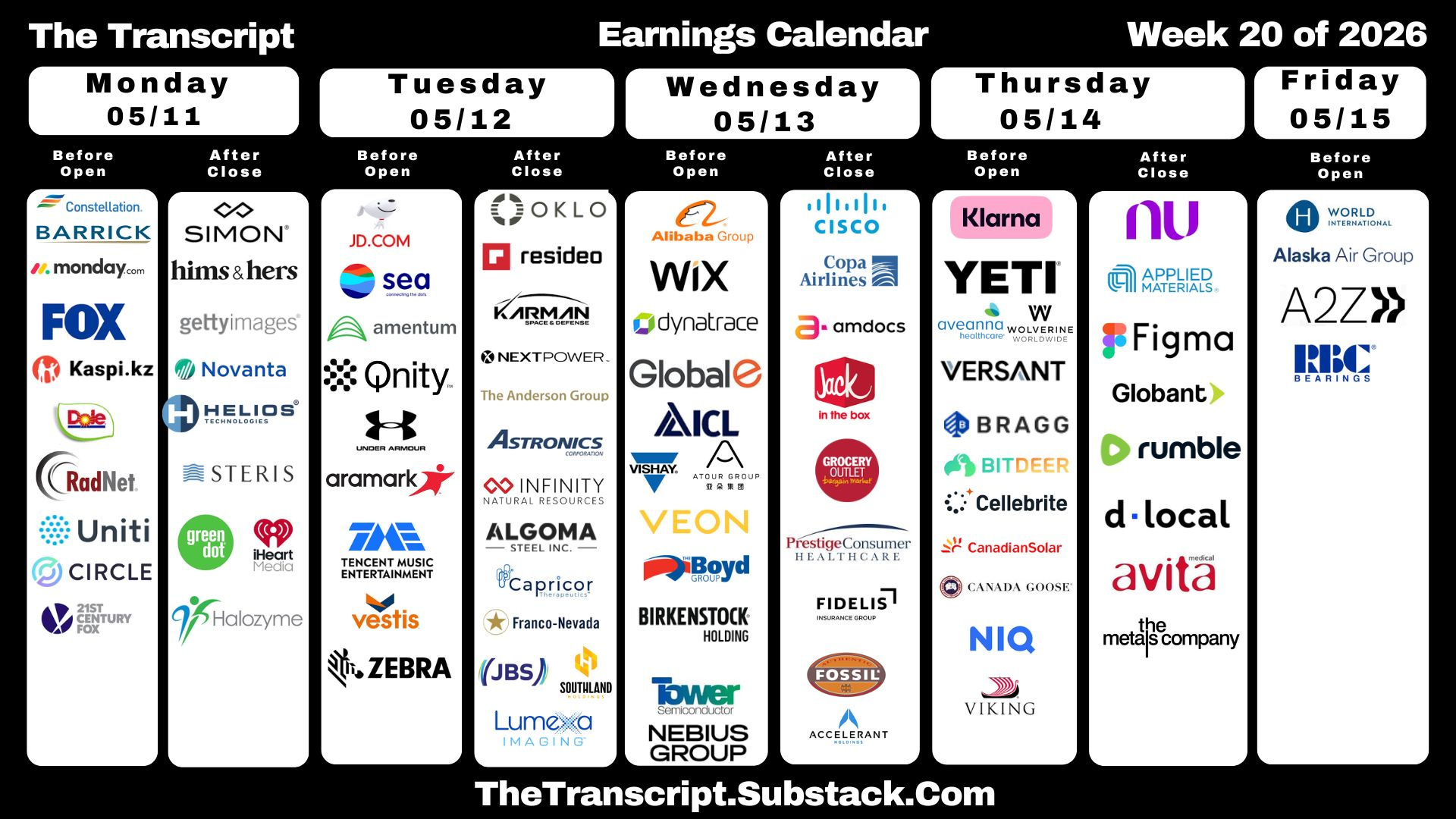

In terms of SPX Q1 earnings we’re very much in the windup phase now with just a few heavyweights left including NVDIA and WMT the week after next (AVGO is the week after that). In the upcoming week, just 1% of the SPX reports by earnings weight consisting of 10 components with three >$100bn in market cap in CSCO, AMAT, CEG (in descending order by market cap). There are though nearly 2,000 total companies reporting next week according to WallStHorizon including several non-US heavyweights such as BABA, TCEHY, etc.

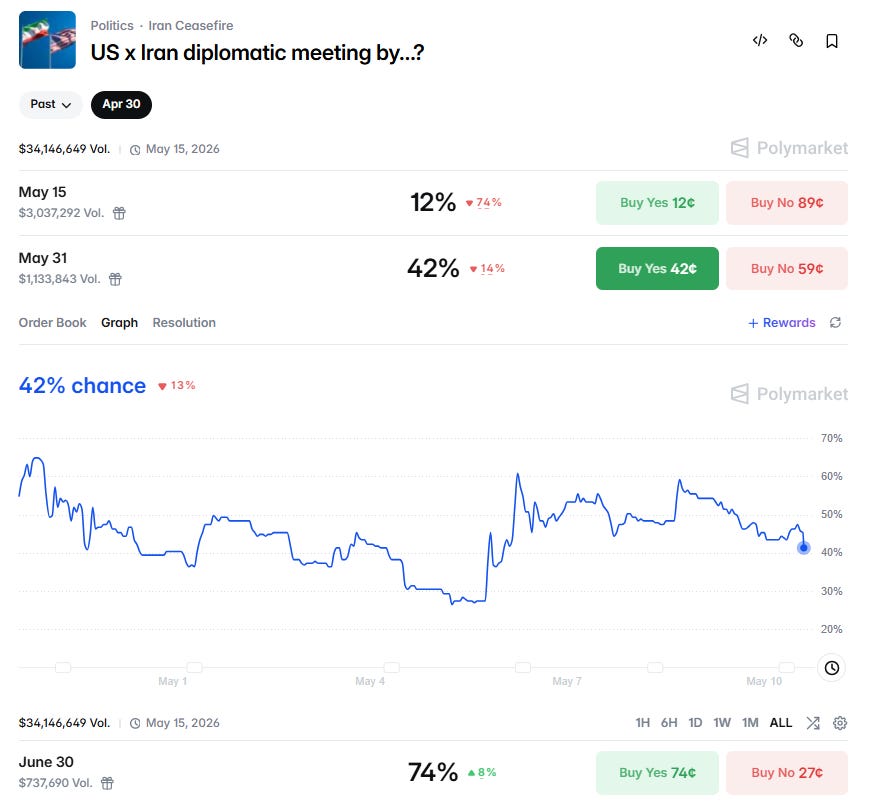

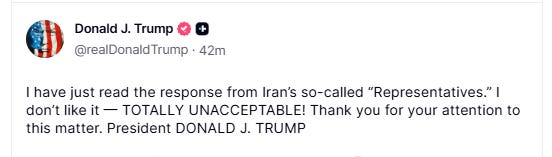

In terms of the Iran war, that continues to drag on with no end in sight (Iran delivered their response to the US proposal (see post below) which continues to see large gaps between the parties on the significant nuclear issue as well as likely others such as control over the Strait of Hormuz). President Trump’s initial response was to the point: “I have just read the response from Iran’s so-called ‘Representatives.’ I don’t like it — TOTALLY UNACCEPTABLE!”

It seems that both sides feel they have the upper hand, and both need a conclusion which allows them to claim “victory”. Not a setup conducive to a quick conclusion. FWIW Polymarket sees just a 42% chance the two sides meet by the end of the month. Betters are more optimistic about by the end of June (74%).

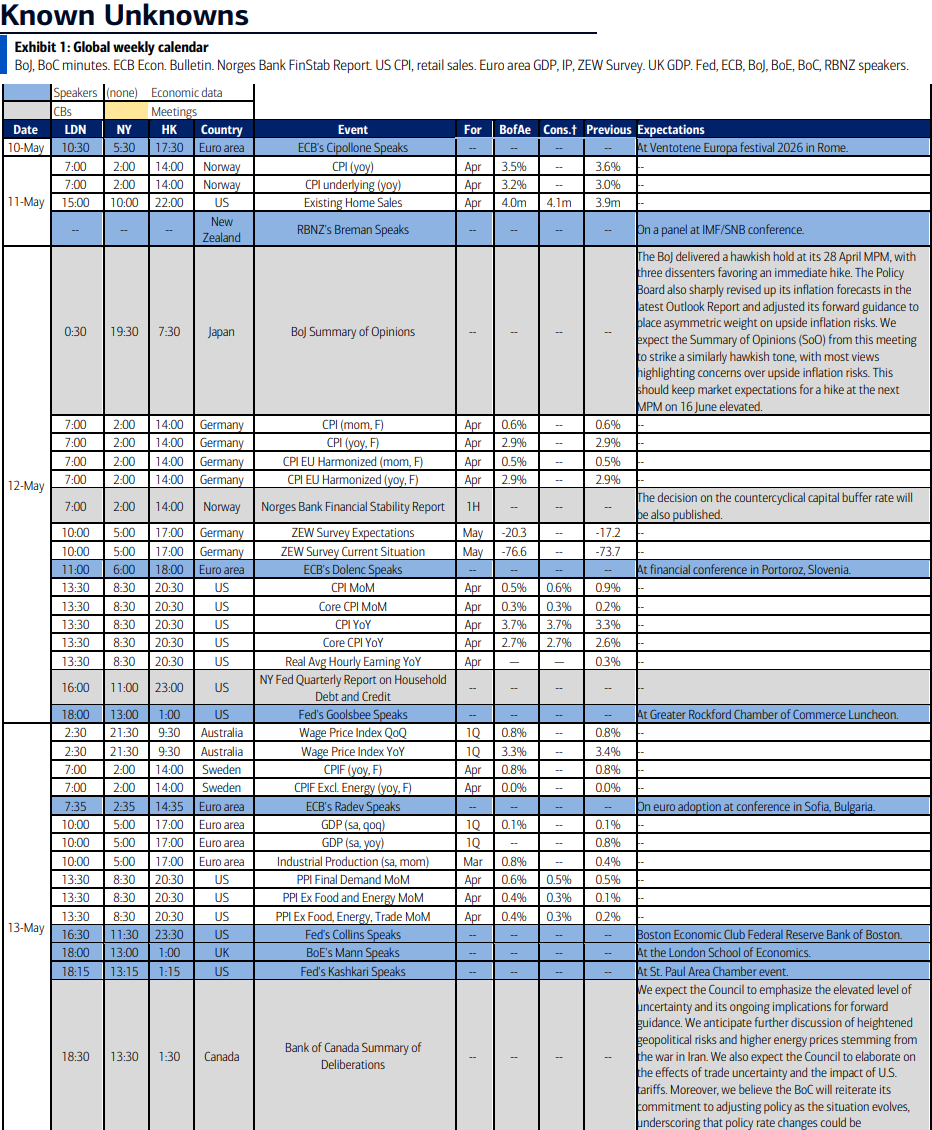

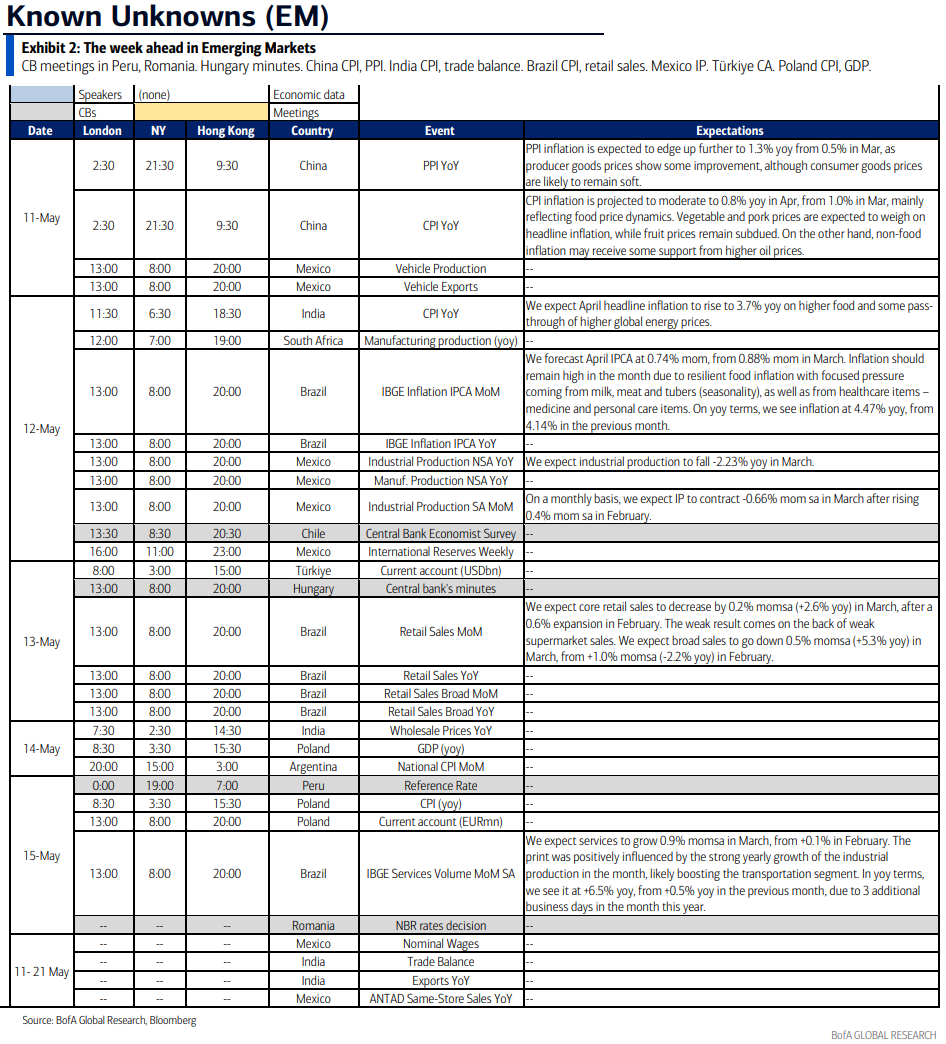

Ex-US highlights from DB:

In geopolitics, the focus will be on the meeting between US President Trump and Chinese President Xi scheduled for May 14–15.

Moving on to Europe, notable data releases will include the April inflation reports from Denmark and Norway on Monday and the ZEW survey in Germany on Tuesday. In the UK, the spotlight will be on the State Opening of Parliament on Wednesday, when the King’s Speech will announce the government’s legislative programme for the year ahead. In economic indicators, there will be Q1 GDP on Thursday.

Over in Asia, starting with China, key data reports include inflation on Monday and trade this Saturday, both covering April. Our economists forecast PPI to further rise to 1.8% YoY in April, up from 0.5% in March, and see CPI inflation slightly decreasing to 0.9% YoY from 1.0%. For trade, their expectations are a 10% YoY growth in exports and an even higher increase for imports (18%). In Japan, notable data releases feature household spending on Tuesday, the Economy Watchers survey and bank lending on Wednesday, and from the BoJ, the summary of opinions from the April meeting (Tuesday).

Here’s their one-pager:

And BoA’s cheat sheets:

Executive Summary

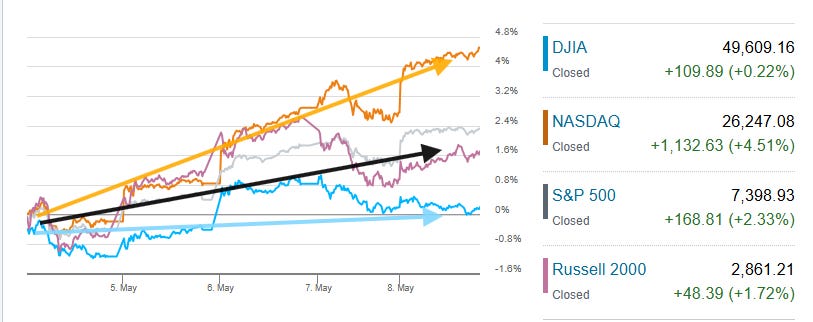

Markets last week were a snapshot of the rally since the March 30 bottom despite a continuation of the stalemate between the US and Iran (including at least one exchange of fire between the sides), seeing the Nasdaq powering to a +4.5% advance, the S&P 500 (SPX) and small cap Russell 2000 (RUT) up around +2% (all three with their 6th straight weekly gain (for the SPX the longest since 2024)), while the Dow Jones Industrials (DJIA) lagged although at least finished positive +0.2%.

It was another big week of economic data (detailed in the subscriber section) which continued to support my long-time thesis of a stable (if not now accelerating) US economy.

While economic data has been an overall boost to equities, a much larger lift has come from corporate earnings, the strength of which has been relatively unprecedented, especially for a quarter not coming out of an earnings trough. That has kept valuations stable at moderate levels even as equities have lifted to new highs.

Positioning and sentiment continue to rebound but are still mostly not yet to the peaks from earlier this year, although pockets are looking frothy. Seasonality and the Fed continue to be less supportive as does the ongoing Iran situation, while breadth continues to deteriorate, all as detailed in the subscriber section.

Now let’s take a closer look at the economy, earnings, positioning, breadth, sentiment, seasonality, Fed, and other factors that will play out in the week ahead.