The Week Ahead - 5/24/26

A look at the upcoming week for the US economy and equities — covering key drivers including earnings, valuations, positioning, breadth sentiment, seasonality, and the Fed.

The Week Ahead

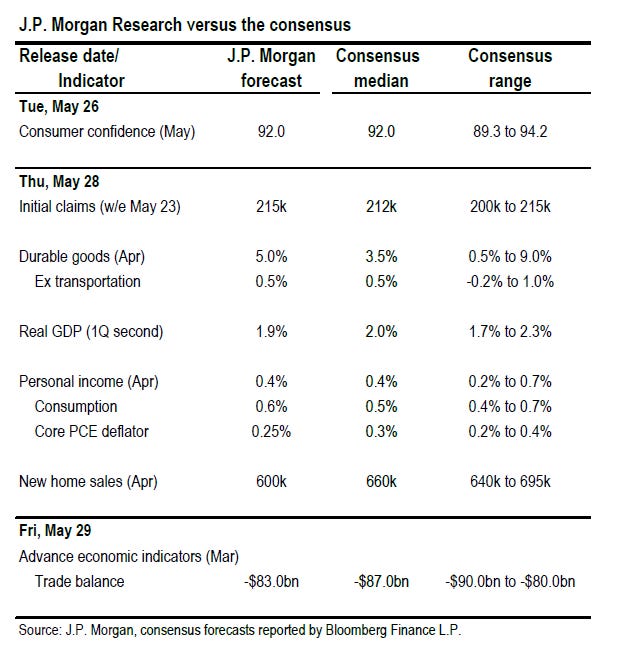

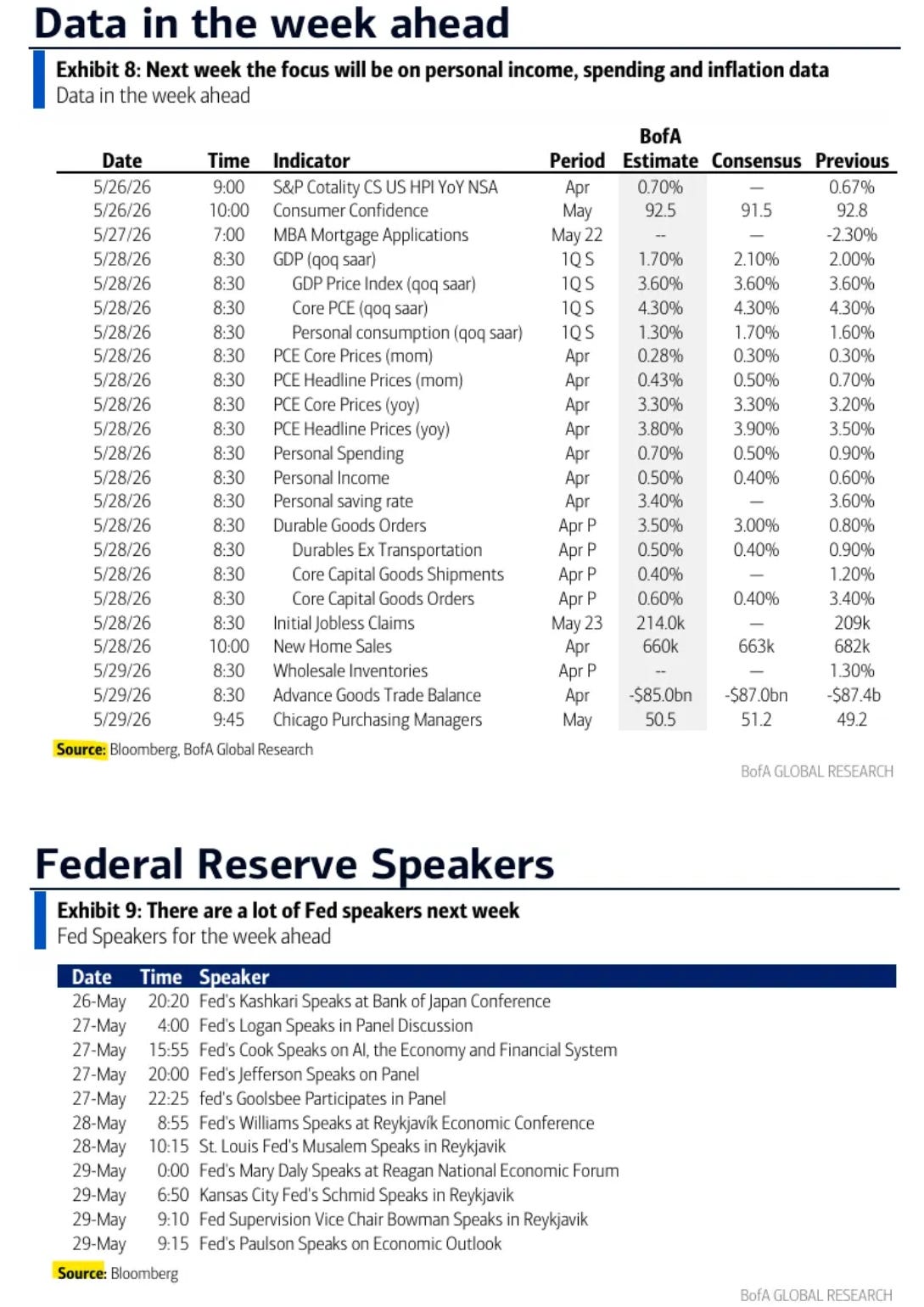

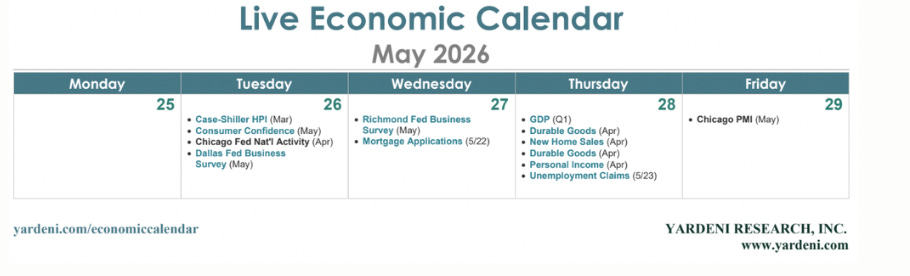

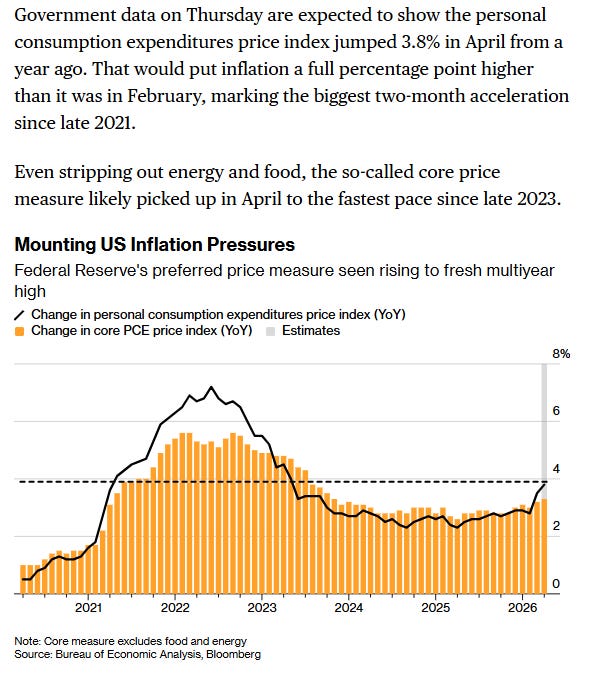

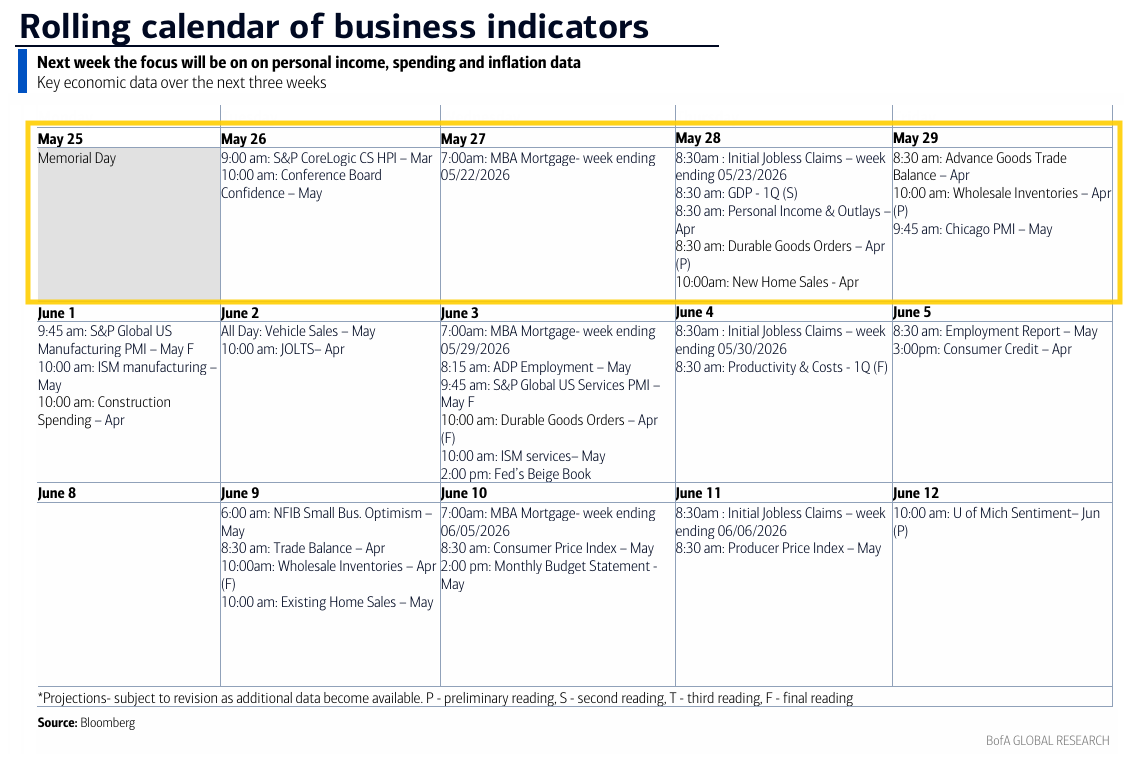

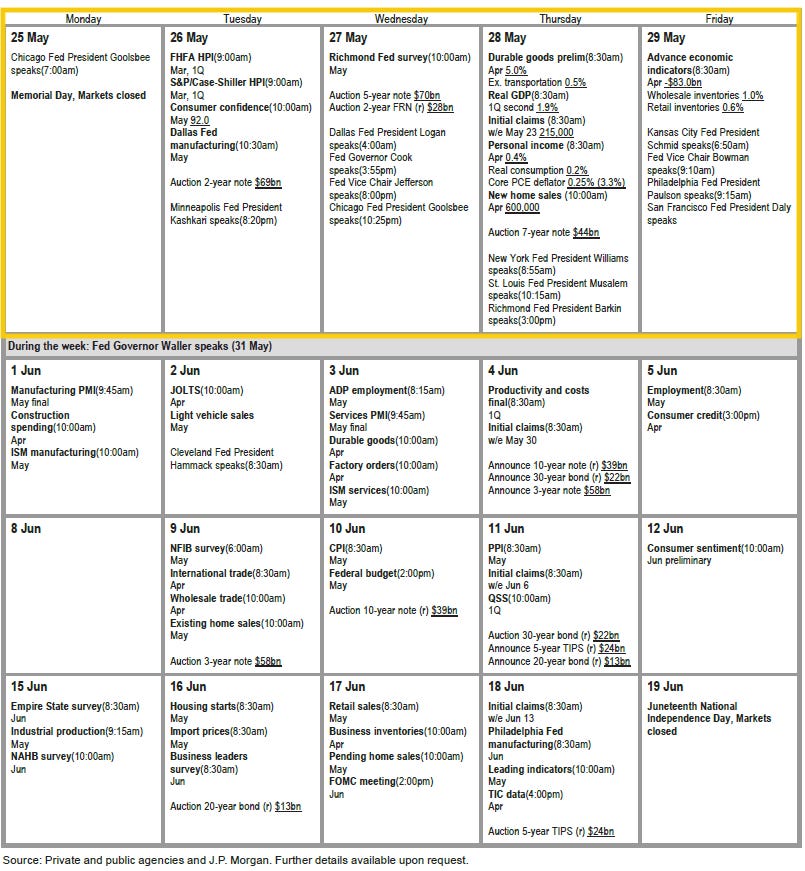

US economic data in the upcoming week is not especially heavy, but we’ll get one of our top tier reports in the April personal income and spending report, which contains PCE prices (the Fed’s preferred inflation metric). In addition, we’ll get April durable goods, new home sales, inventories, Chicago Fed National Activity Index, and goods trade balance, May consumer confidence from the Conference Board, March repeat home price indices, the second estimate of 1Q GDP, and the normal weekly reports (ADP, unemployment claims, etc.).

In terms of Fed speakers more than half the Fed will have appearances (perhaps trying to jam them in before new Chair Warsh puts the kibosh on all the Fedspeak), with Governors Cook, Jefferson, and Bowman, and regional Fed Presidents Logan, Goolsbee, Williams, Musalem, Daly, Schmid, and Paulson. With the Waller hawkish pivot on Friday, you may very well be seeing more following (in addition to the many that were already there) in looking to drop the easing bias, and saying a hike is the next step if inflation does not fall back towards 2%.

In terms of non-Bill (>1yr in duration) US Treasury auctions we’ll get 2, 5, and 7-yr auctions Tues, Wed, and Thurs respectively.

Q1 earnings season will continue to wind down with 12 SPX components reporting of which three are >$100bn in market cap in COST, DELL, CRM.

In terms of the Iran war, as I have been saying for a while, “it continues to drag on with no end in sight.” As I have also said “It seems that both sides feel they have the upper hand, and both need a conclusion which allows them to claim ‘victory’. Not a setup conducive to a quick conclusion.” But as I also said last week “it is clear that President Trump’s patience is starting to wear thin.”

Recent events appear to indicate Trump is very much between a rock and a hard place. While it seems he wants to come to an agreement with Iran, Iran knows that and also that with each passing day pressure builds from the coming mid-term elections. And Trump is now getting counter-pressure to “finish the job” from hard-line Republicans who came out with some blistering criticism Saturday after Trump said that a deal was imminent.

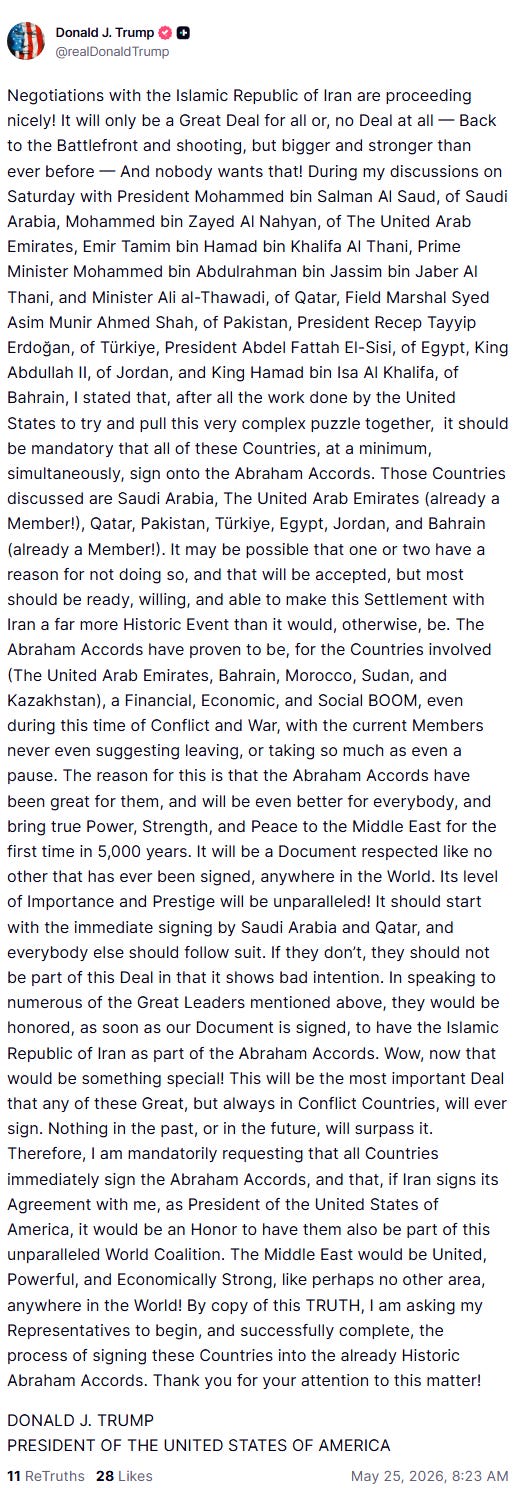

While reports are that the sides are “inching towards a deal,” and Iran’s semi-official Tasnim news agency reported there are “one or two provisions” that need to be ironed out, Iran’s Foreign Ministry Spokesman said “no one can claim that the signing of an agreement is imminent,” while Trump posted this morning that “Negotiations with the Islamic Republic of Iran are proceeding nicely! It will only be a Great Deal for all or, no Deal at all — Back to the Battlefront and shooting, but bigger and stronger than ever before — And nobody wants that!”

As a side note, Trump also injected a new item onto the agenda mandating that a long list of regional countries “sign onto the Abraham Accords” (US‑brokered agreements that normalized diplomatic relations between Israel and several Arab/Muslim‑majority countries starting in 2020) in order to benefit from any deal, which the President says would create “a Document respected like no other that has ever been signed,” and “if Iran signs its Agreement with me, as President of the United States of America, it would be an Honor to have them also be part of this unparalleled World Coalition. The Middle East would be United, Powerful, and Economically Strong, like perhaps no other area, anywhere in the World!”

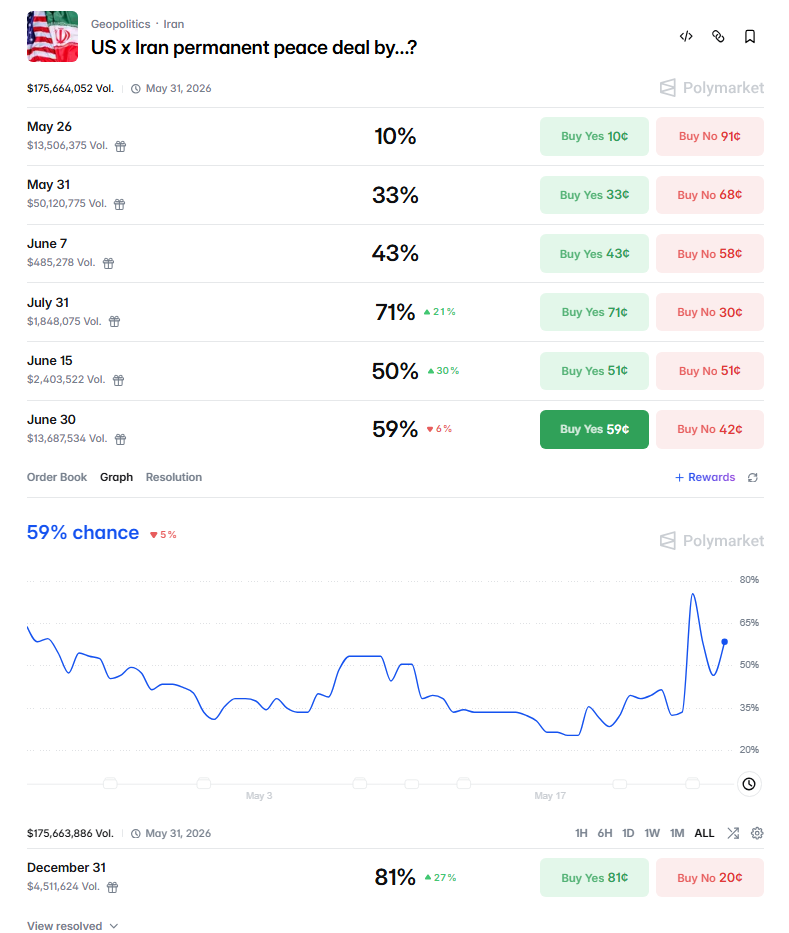

FWIW Polymarket currently sees a 60% chance of a permanent US-Iran peace deal by June 30th, down from nearly 80% Saturday night, but up from around 35% a week ago.

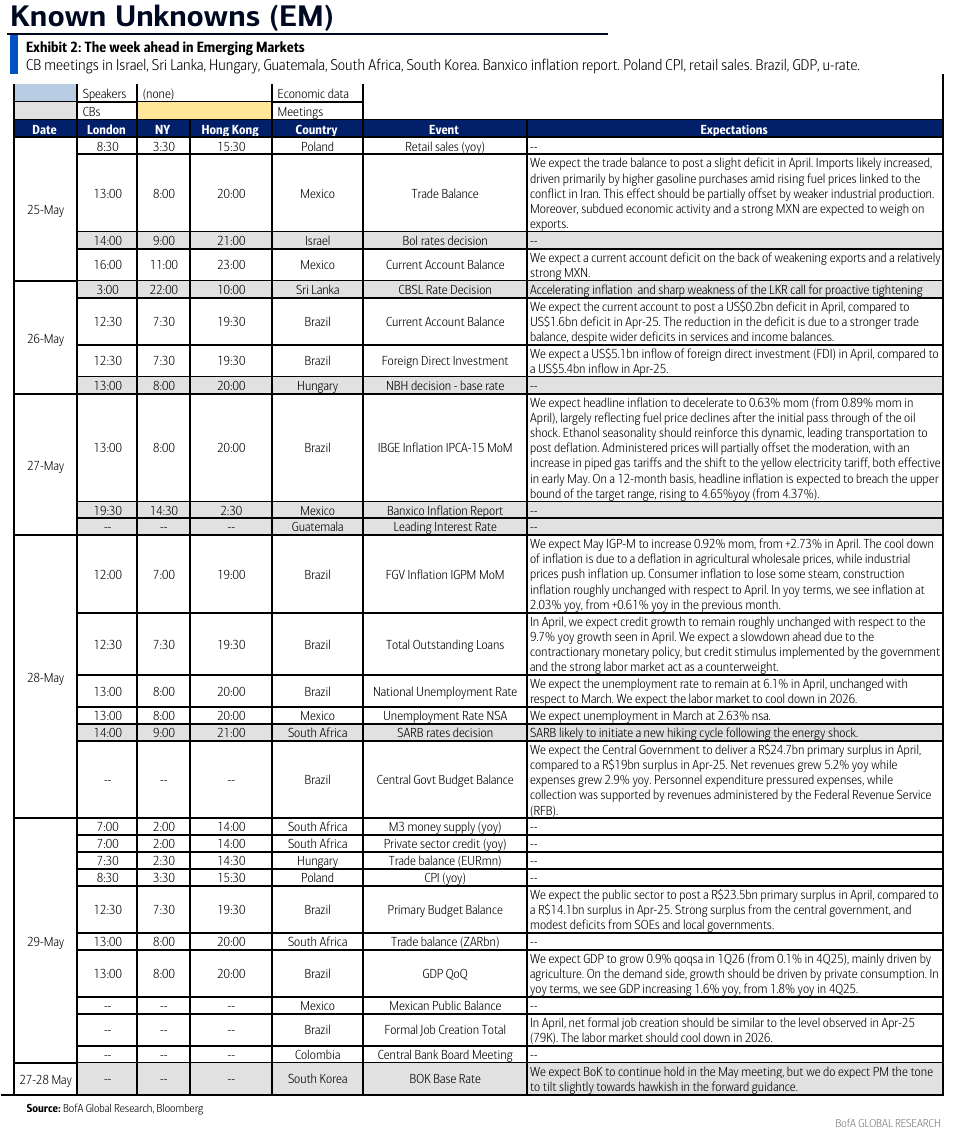

Ex-US highlights from DB:

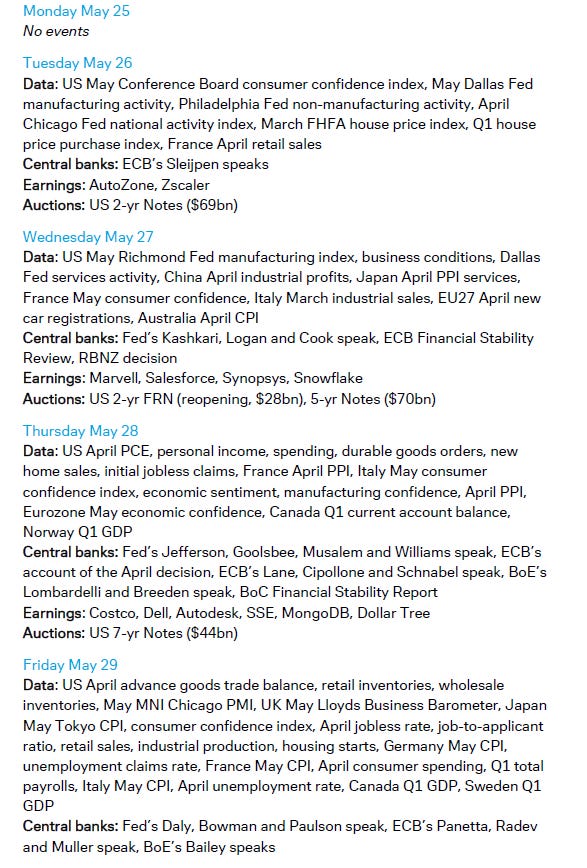

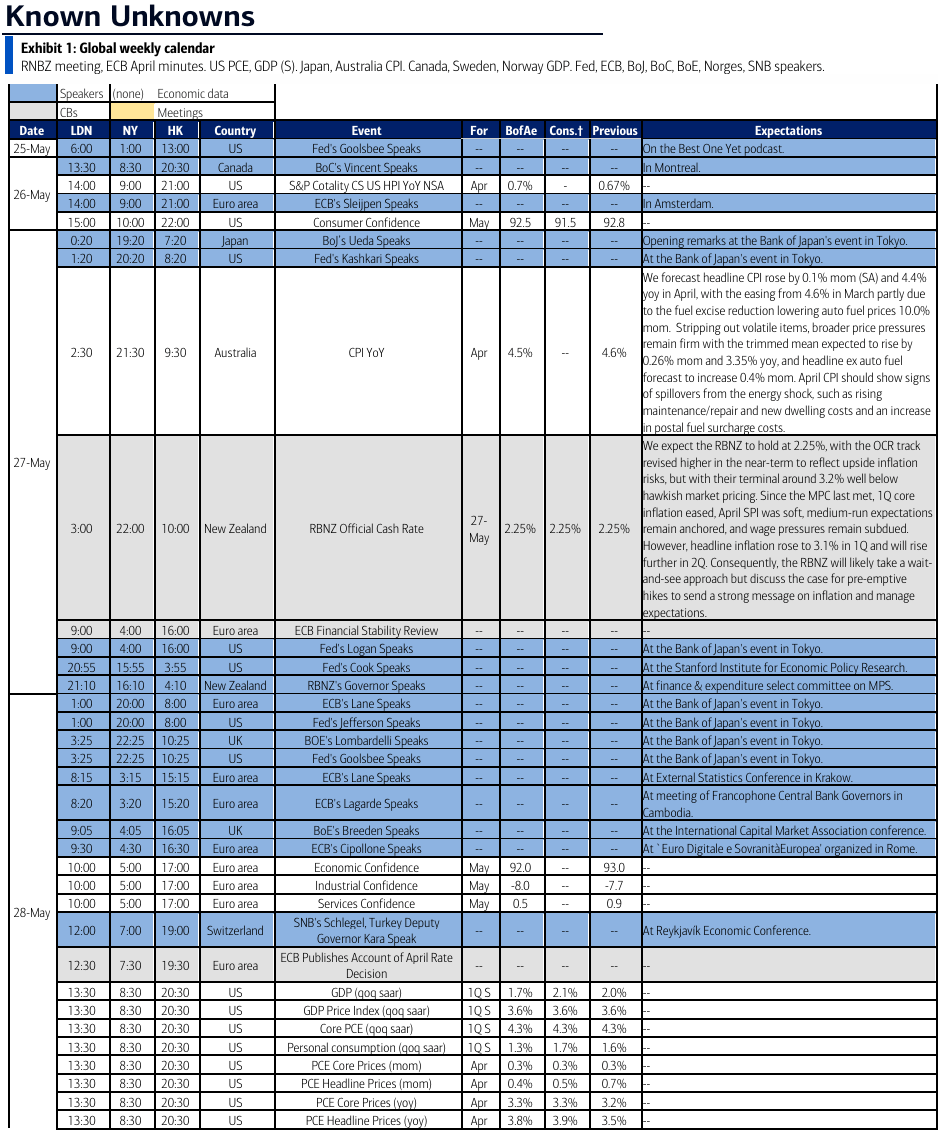

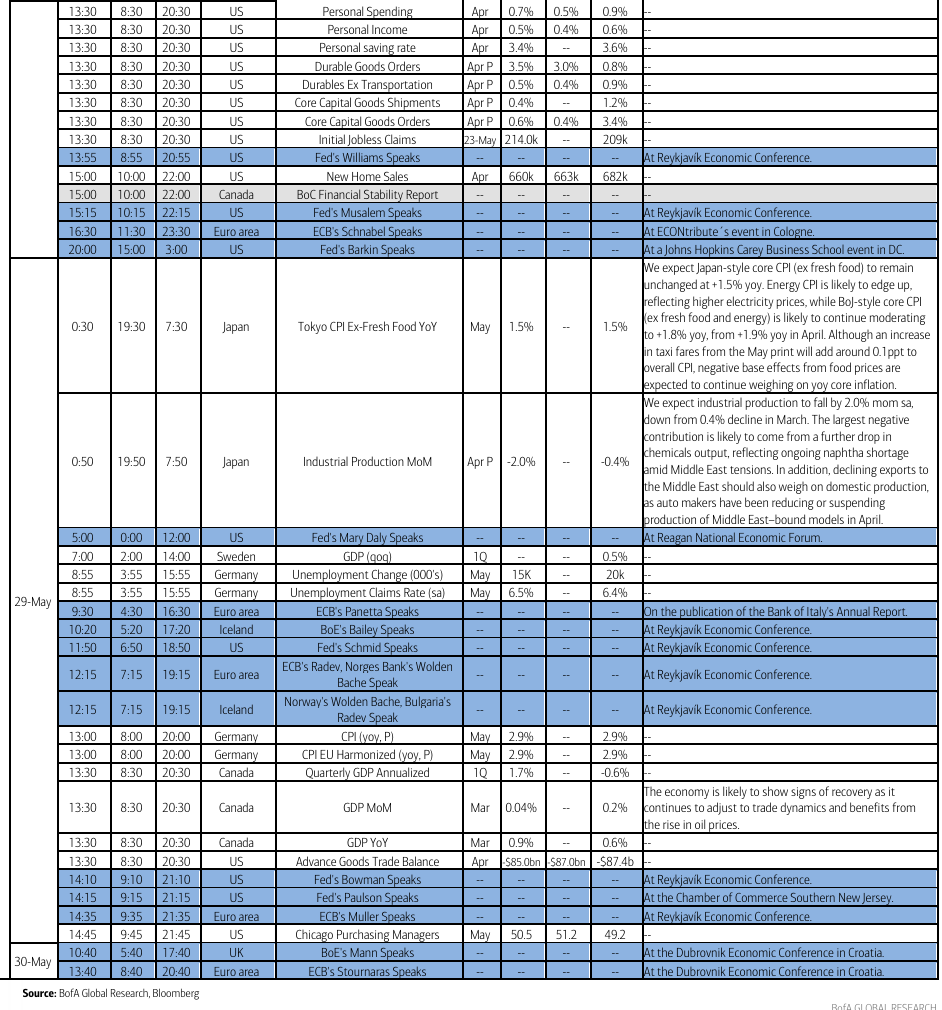

In Europe, the focus will be on the May flash inflation prints across the Eurozone, with Germany, France, Italy and Spain amongst those reporting on Friday and the Eurozone-wide measure due the following Tuesday. Our European economists expect inflation at 2.82% YoY in Germany, 2.83% in France and 3.42% in Italy and 3.59% YoY in Spain. Another highlight in Europe will be the ECB’s account of their April meeting due Thursday, and the central bank will also release its Financial Stability Review on Wednesday.

Over in Asia, the focus will be on Japan, where the Tokyo CPI on Friday will provide an early read on national inflation trends. Economic activity data is also due Friday, featuring the April industrial production and retail sales indicators. In terms of forecasts, our Chief Japan economist sees core CPI ex. fresh food speeding up to 1.6% YoY (1.5% in April) and core-core ex. fresh food and energy to 2.0% (+1.9%). For industrial production, he expects a +0.2% MoM increase. Finally, he mentions that the Ministry of Finance will announce the results of its forex market interventions conducted from 28 April to 27 May on Friday.

Elsewhere in the region, notable releases include industrial profits in China, Australia’s April CPI and the RBNZ policy decision all due Wednesday. Our economists look for a 0.3% MoM headline print for Australia inflation report and expect RBNZ to keep the cash rate unchanged at 2.25%.

Here’s their one-pager:

And BoA’s cheat sheets:

Executive Summary

US equity indices last week would hit their lows on Tuesday morning under pressure from rising oil prices and bond yields, but those would start to ease off mid-day Tuesday and continue through the end of the week, allowing equities to move higher on hopes for a US-Iran deal despite a tepid reaction to Nvidia earnings.

Economic reports were light. In reports covered this week contract signings for existing homes rose for a third straight month in April, while housing starts and permits came in solidly above expectations, May preliminary purchasing manager indices (PMIs) came in unchanged in May at the headline level which, though, masked a continued widening between a resurgent manufacturing sector and “sluggish” services sector while prices rose the most since 2022, and consumer sentiment index from the University of Michigan would come in at a record low (as did both index components) with long-run inflation expectations jumping to a 7-month high.

Companies continued to put the finishing touches on a Q1 earnings season which as noted in previous weeks has been exceptionally strong, especially for a quarter not coming out of an earnings trough. That has kept valuations stable at moderate levels even as equities lifted higher.

Positioning and sentiment were mixed, mostly easing back last week after getting to levels where even the more bullish have been indicating limited near-term upside. While downside risks have grown, few are expecting more than a modest consolidation, if that. Corporates have also exited their buyback blackouts providing their support to markets, and breadth saw a modest expansion last week, all as detailed in the subscriber section.

The Fed would turn less supportive though with the minutes from the April FOMC meeting which confirmed a committee becoming increasingly hawkish with a majority in favor of rate hikes if inflation “continues to run persistently above 2 percent.”