The Week Ahead - 5/31/26

A look at the upcoming week for the US economy and equities — covering key drivers including earnings, positioning, breadth, valuations, sentiment, seasonality, and the Fed.

Note: I will be traveling to London June 2nd through the 9th. I will post as I am able, but there will be no morning or nightly updates until the 10th.

The Week Ahead

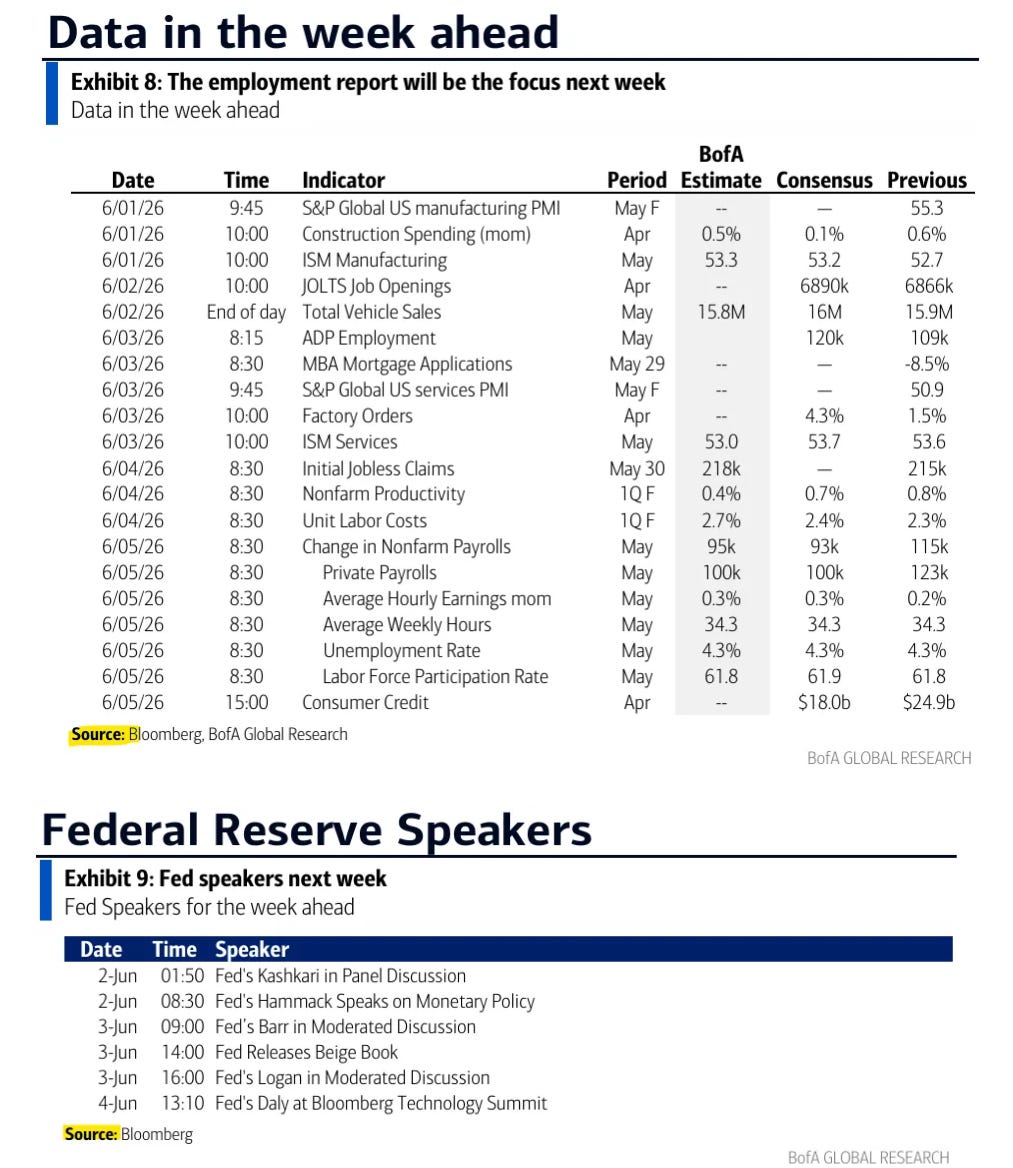

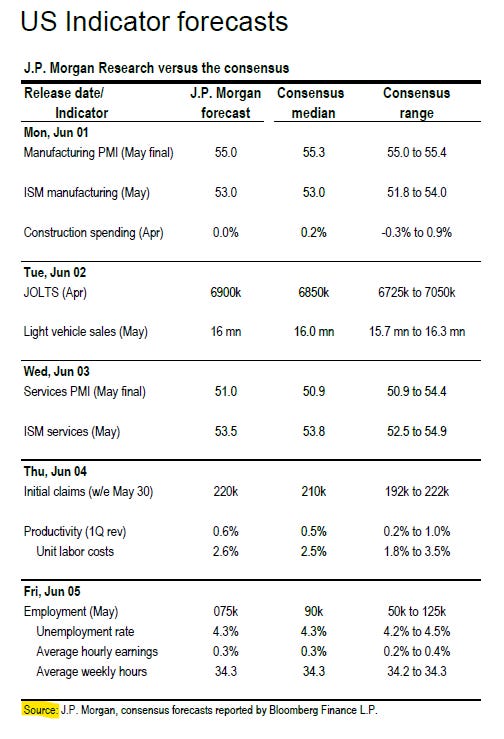

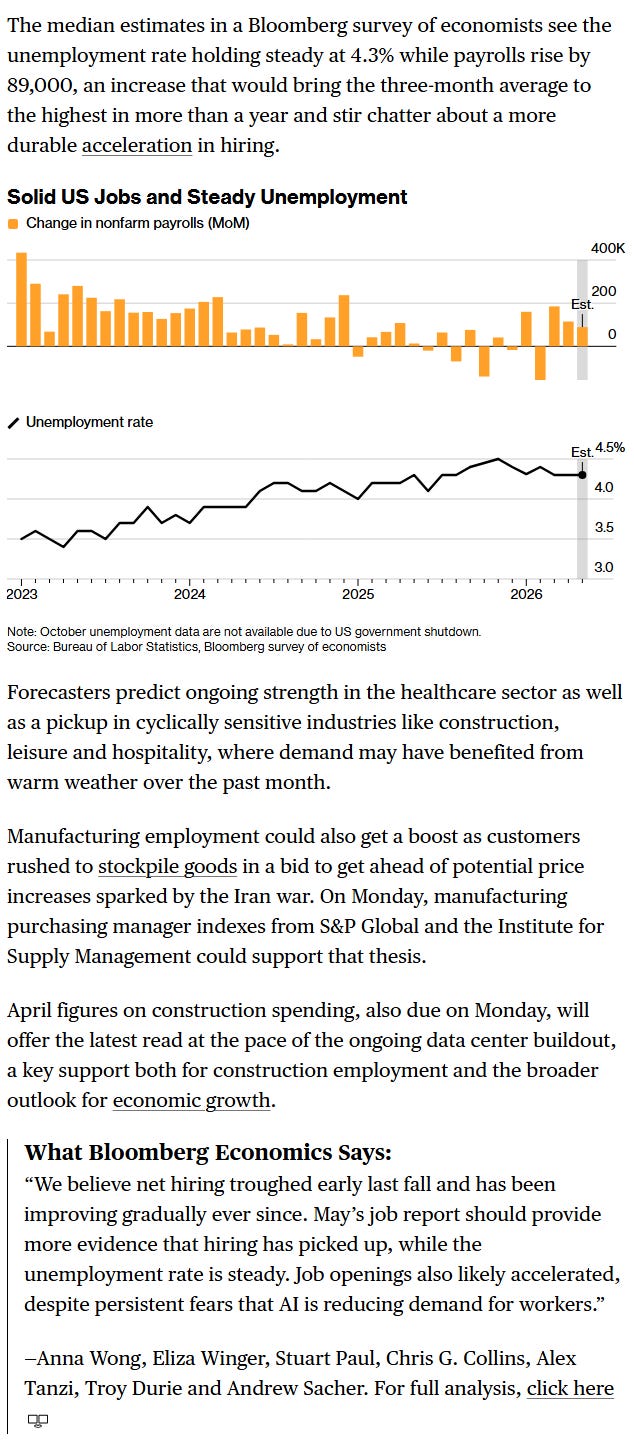

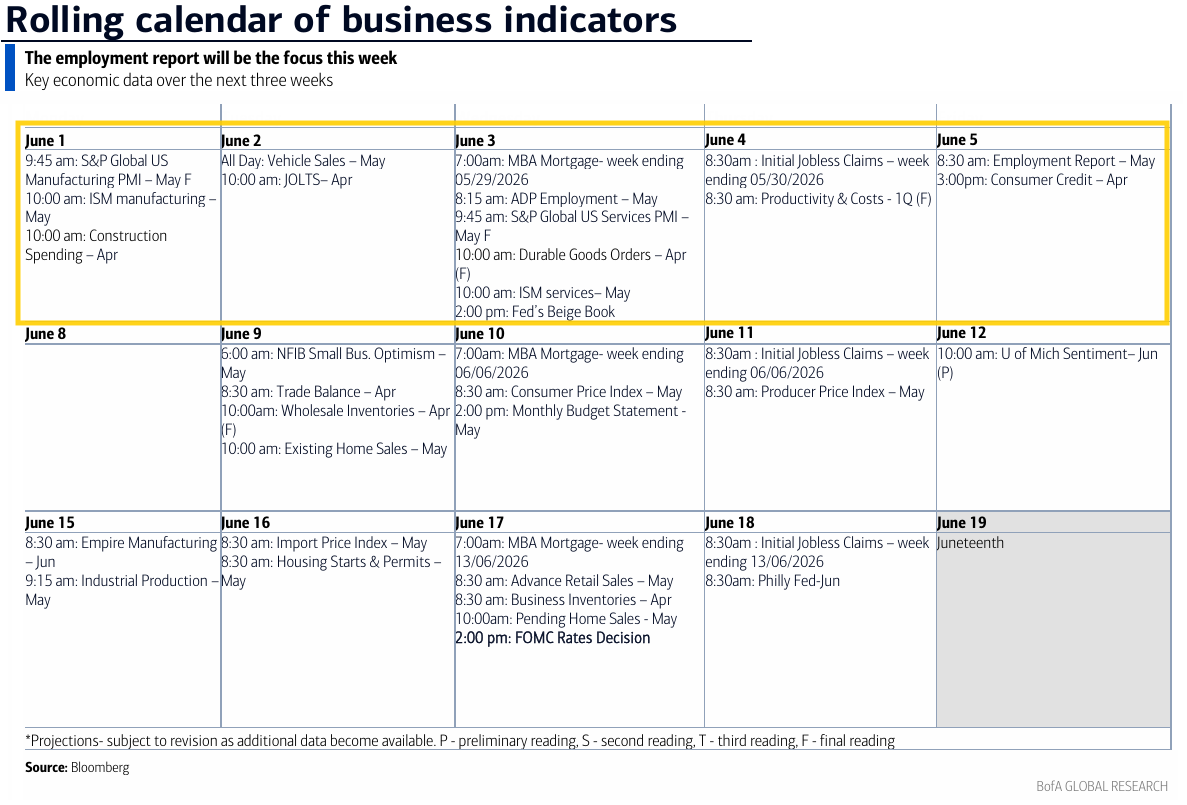

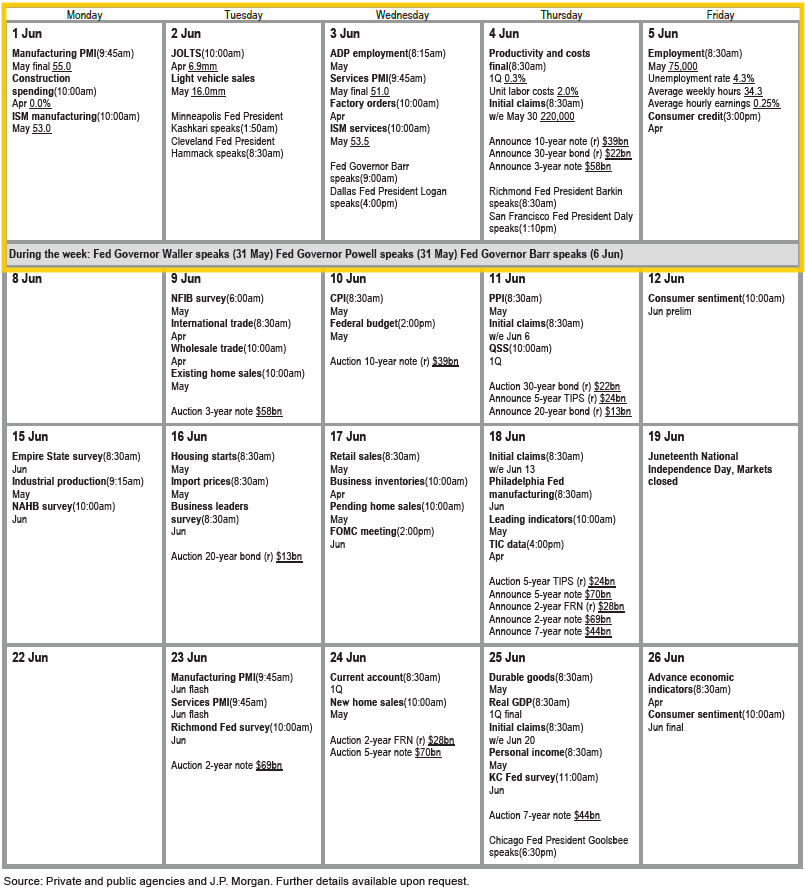

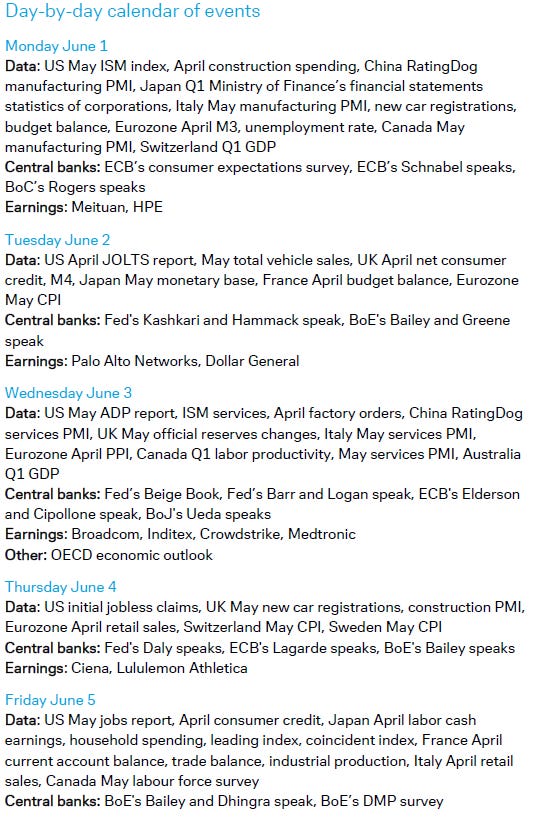

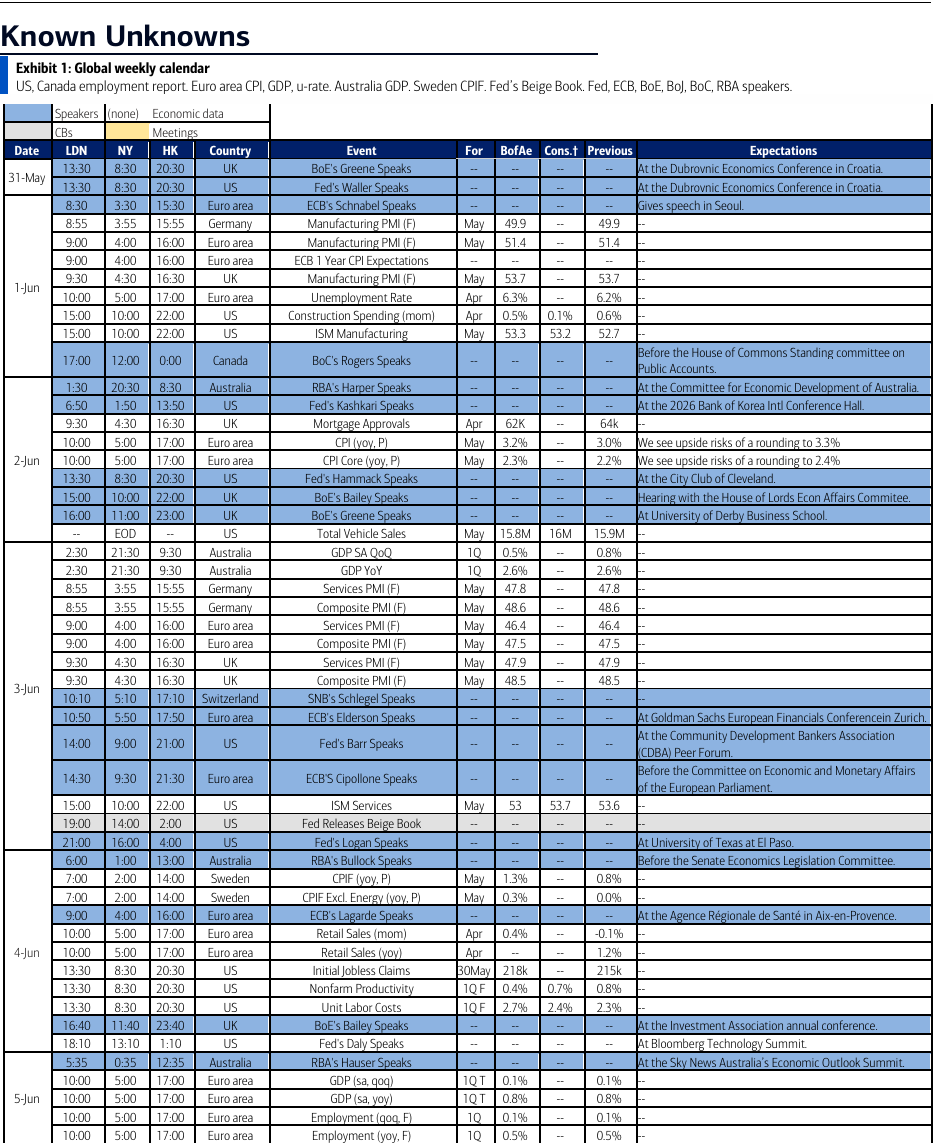

Next week is the first week of the month which also means it’s jobs week in the US, and with no shutdown to mess things up, we’ll get for the first time since then the normal first week of the month cadence of reports culminating in May’s Nonfarm Payrolls Friday (technically the Employment Situation report).

As usual before we get there we’ll get the May ADP monthly employment, Challenger job cuts, PMIs, and auto sales, April JOLTS, construction spending, factory orders, trade balance, and consumer credit, as well as the standard weekly reports (jobless claims, mortgage applications, and US petroleum inventories (not ADP though with the monthly report this week)). We’ll also get the final revision for Q1 productivity.

Fed speakers are lighter (at least scheduled) even though this is the last week before the start of the blackout with just Governor Barr and regional bank presidents Kashkari, Hammack, Logan, and Daly. We’ll also get the Fed’s Beige Book for the June meeting on Wednesday.

In terms of non-Bill (>1yr in duration) US Treasury auctions, we’re off next week.

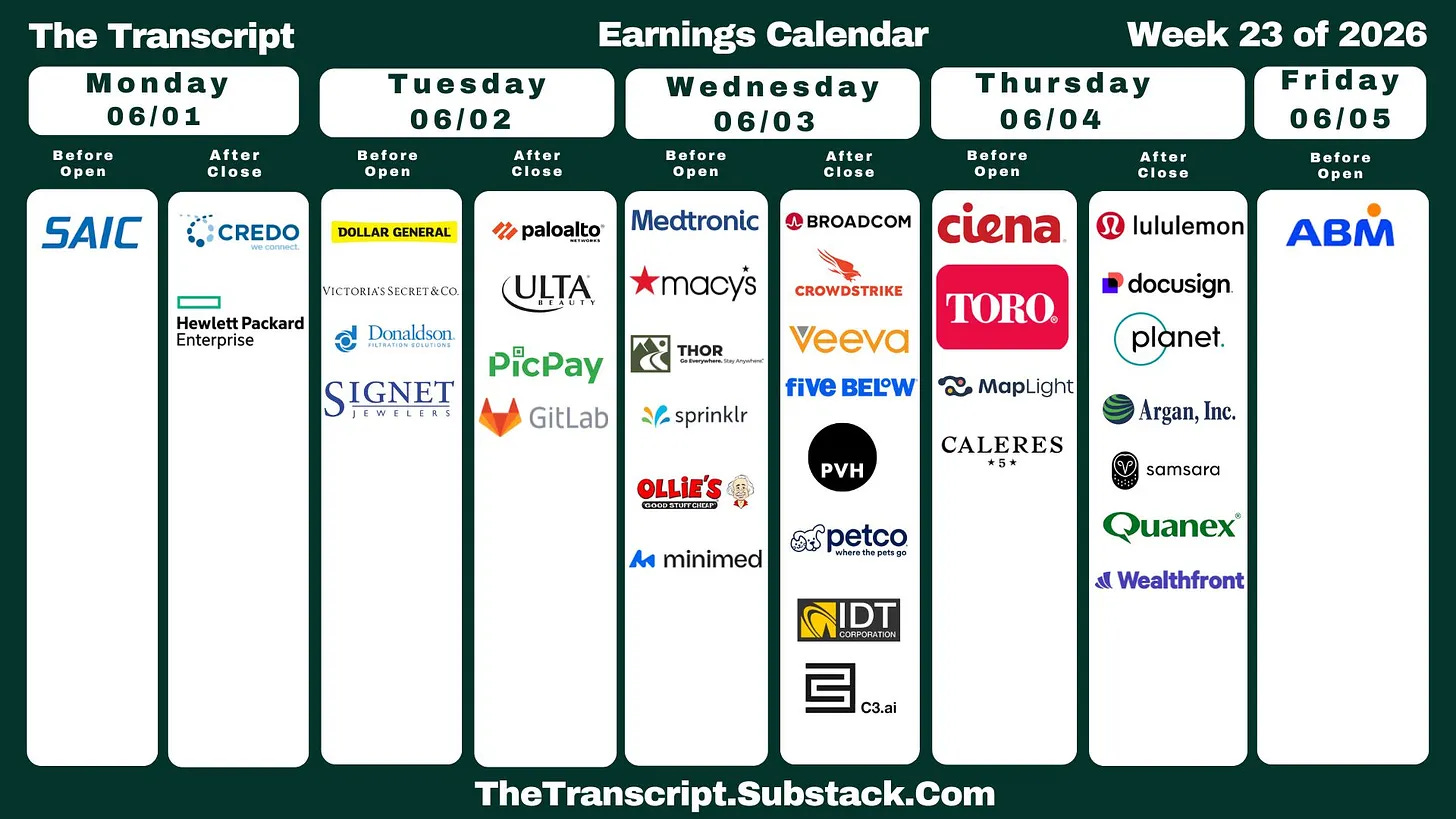

Q1 earnings season will continue to wind down with 12 SPX components reporting, but we will get one top 10 SPX market cap name in chip supplier Broadcom (AVGO) on Wednesday. Two other >$100bn market cap reporters are cybersecurity providers PANW and CRWD.

Also, AI industry leaders will present at Computex Taipei, while Microsoft (MSFT) hosts its annual Build developer conference. Both events are expected to feature major announcements around AI, datacenters, software, and robotics. Honeywell-backed quantum computing company Quantinuum (QNT) is expected to debut, making it one of the largest technology offerings of the year, while FedEx (FDX) will complete the spinoff of FedEx Freight (seeking alpha).

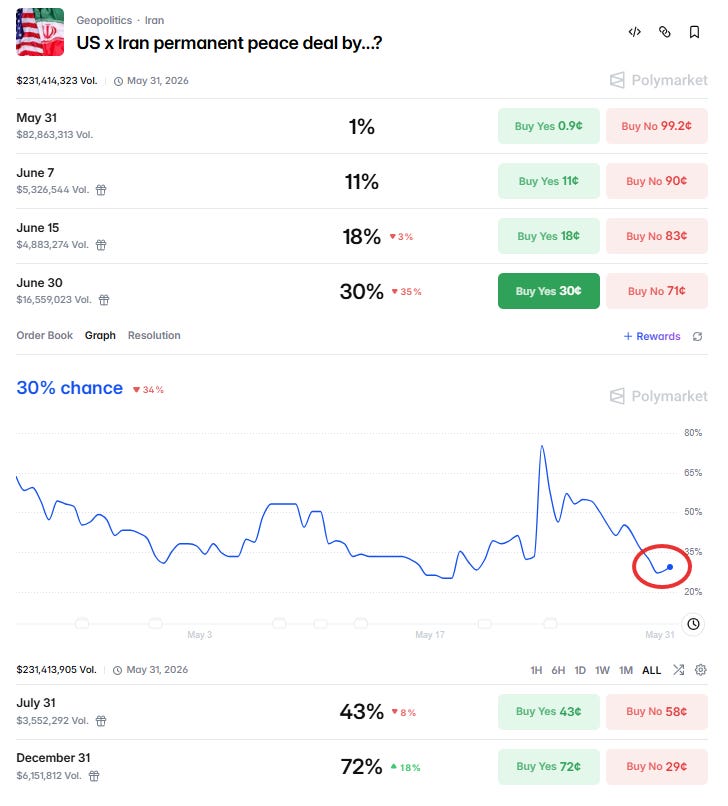

In terms of the Iran war, as I have been saying for a while, “it continues to drag on with no end in sight.” As I have also noted “It seems that both sides feel they have the upper hand, and both need a conclusion which allows them to claim ‘victory’. Not a setup conducive to a quick conclusion,” but “it is also clear that President Trump’s patience is starting to wear thin.”

As I mentioned last week “recent events appear to indicate Trump is very much between a rock and a hard place. While it seems he wants to come to an agreement with Iran, Iran knows that and also that with each passing day pressure builds from the coming mid-term elections. And Trump is now getting counter-pressure to ‘finish the job’ from hard-line Republicans who came out with some blistering criticism after Trump said that a deal was imminent Memorial Day weekend.” So while Trump wants a deal, it also has to look like “a good deal,” again all of which Iran knows. It’s no wonder it continues to drag on.

FWIW Polymarket now just sees a 30% chance of a permanent US-Iran peace deal by June 30th, half of where it sat a week ago, and down from nearly 80% last Saturday night.

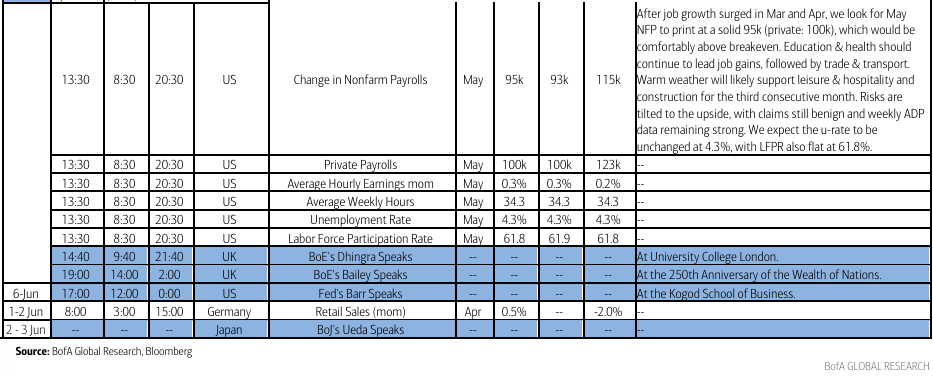

Ex-US highlights from DB:

In Europe, the highlights include the flash CPI print for May for the Eurozone on Tuesday. In addition, a read on inflation expectations will come from the ECB’s consumer expectations survey out on Monday. Briefly turning to central banks, speakers will include ECB President Lagarde on Thursday, BoE Governor Bailey (Tuesday, Thursday and Friday) and BoJ Governor Ueda on Wednesday.

Over in Asia, the focus will be on China’s PMIs, with the official gauges due this Sunday and private manufacturing and services PMIs following on Monday and Wednesday. In Japan, labour cash earnings are due Friday and there will be the financial statements statistics of corporations from the Ministry of Finance on Monday. Our Chief Japan economist expects wages growth to slow to around 2.5% YoY (2.8% in March). Elsewhere in the region, Australia’s Q1 GDP is due Wednesday.

Here’s their one-pager:

And BoA’s cheat sheets:

Executive Summary

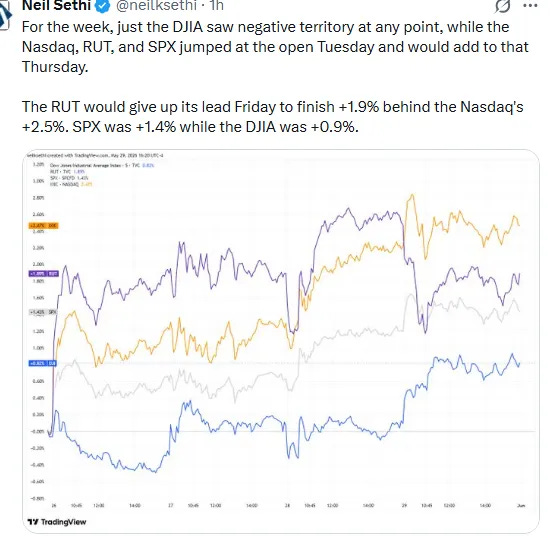

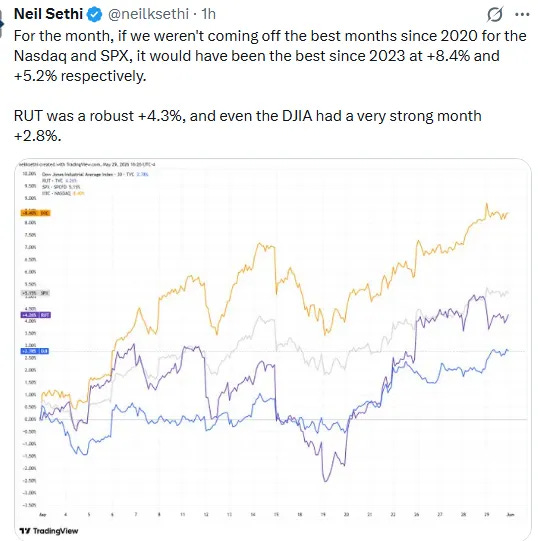

US equity indices saw solid gains last week continuing to be led by the Tech heavy Nasdaq which finished +2.5%. With interest rates falling back, the small cap Russell 2000 would come in at +1.9%, the S&P 500 (SPX) +1.4%, its 9th straight weekly gain, the longest streak since 2023, and the Dow Jones Industrial Average (DJIA) +0.9%.

It would cap what would have been the best month since 2023 if it wasn’t for the even stronger performance in April.

Economic reports were highlighted by April’s personal income and spending report which showed negative income growth when adjusted for inflation, personal spending as expected with modest growth when adjusted for price rises (seeing the savings rate fall to the least since June 2022), and PCE prices (the Fed’s preferred inflation index) slightly below expectations but compared to a year earlier core inflation was the highest since November 2023. More coverage on economic reports and indicators in the subscriber section.

With Q1 earnings season mostly wrapped up, attention has turned to Q2 and beyond with estimates continuing to ratcheted higher.

Positioning rebounded after softening a touch the prior week pushing up to levels where many (most?) analysts think falling volatility or another catalyst are needed to see them ratchet higher. Buybacks remain very solid with corporates in their open windows.

Sentiment remained mixed with some indicators hitting frothier levels while others remained subdued.

The Fedspeak continued to turn more hawkish but rates nevertheless softened last week, adding some fuel to equities.