The Week Ahead - 6/21/26

A look at the upcoming week for the US economy and equities — covering key drivers including earnings, positioning, breadth, valuations, sentiment, seasonality, and the Fed.

The Week Ahead

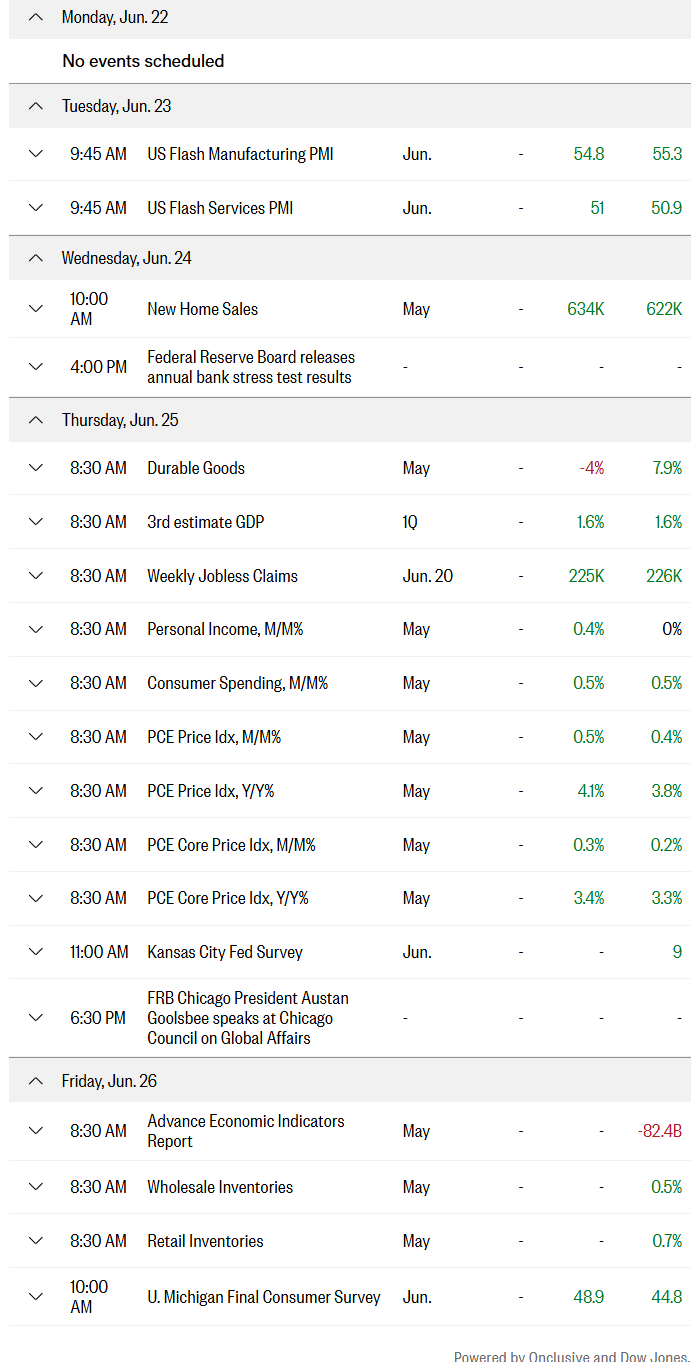

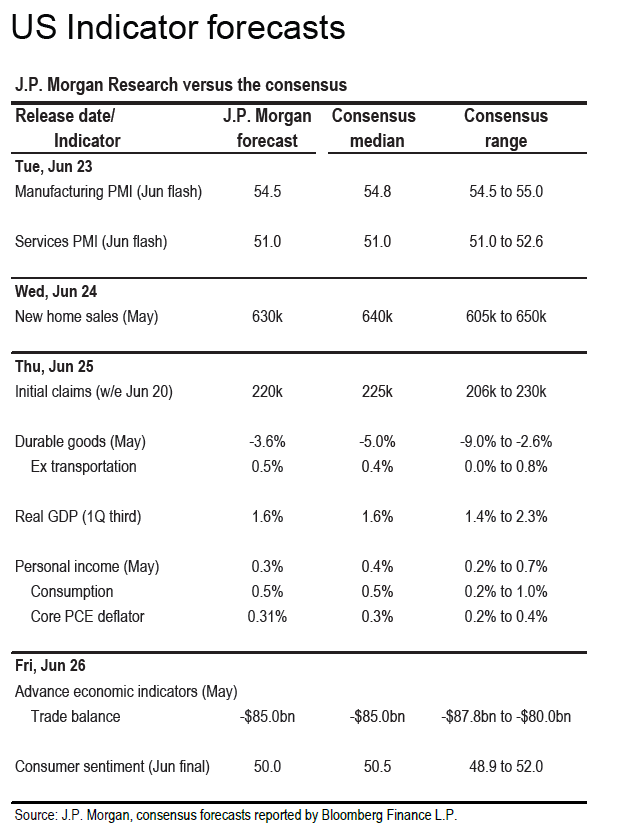

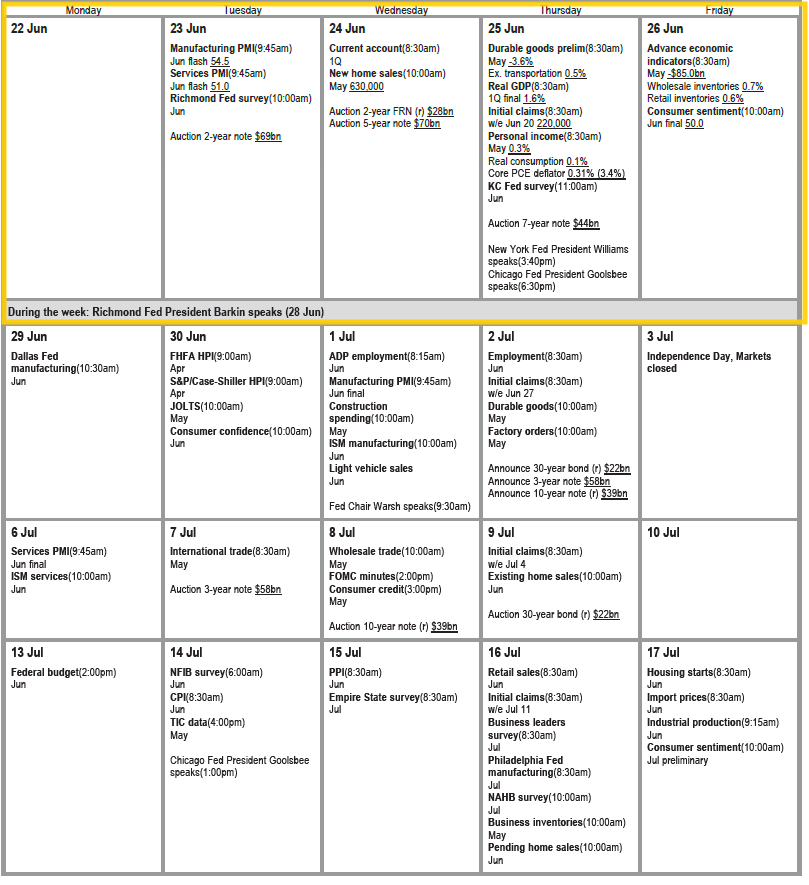

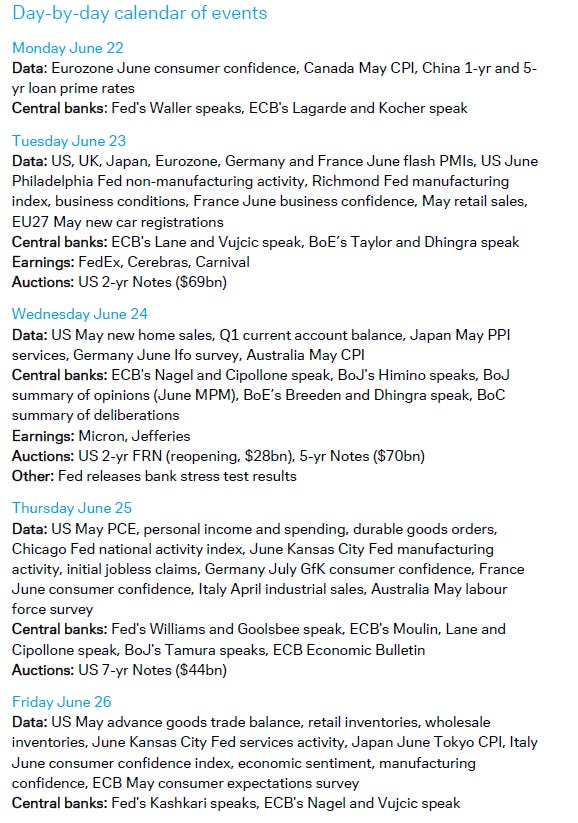

As mentioned last Wednesday, US economic data is fairly light until we get to the upcoming Thursday when we get quite a bit in the May personal income and spending report, our most complete look at incomes, spending, and prices (containing what has traditionally been the Fed’s preferred inflation metric in PCE prices (we’ll see if that survives the “task force”)). We’ll also that day get the final look at Q1 GDP, May durable goods, and weekly jobless claims. The rest of the week, we’ll get June flash PMIs and final UMich consumer sentiment and May new home sales and advance goods trade balance and inventories. We’ll also get the weekly ADP report along with mortgage applications and EIA petroleum inventories.

Fed blackout is over, and we have a few speakers on the docket, and I’m sure there will be more. From what I can piece together we seem to have Governor Waller along with Fed presidents Williams, Goolsbee, Barkin, and Kashkari. It will be interesting though to see if we get fewer appearances under the new Fed chair who is not a fan of Fedspeak.

US Treasury auctions also pick up this week with auctions of 2, 5, and 7-year notes Tues, Wed, Thurs respectively.

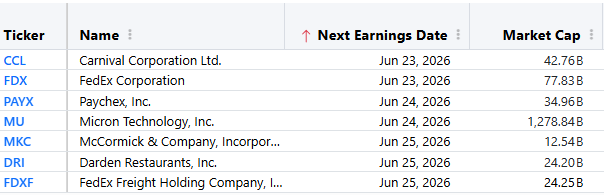

Earnings do accelerate a touch with seven SPX components reporting, but one will garner outsized focus in memory maker Micron Wednesday. We’ll also get FedEx which is often seen as a global economic barometer, and the bank stress test results from the Fed.

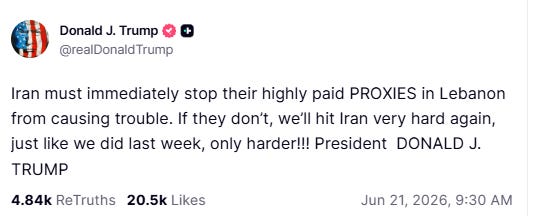

In terms of Iran, as noted last week, talks did finally germinate into a Memorandum of Understanding, an initial reopening of the Strait of Hormuz, and the start of four-party talks in Switzerland. That said, in keeping with how things have been since the start of the conflict, confusion abounds with Iran at various points over the weekend declaring the Strait closed and talks off, upset over continued Israeli attacks in Lebanon and comments from Donald Trump on social media that “Iran must immediately stop their highly paid PROXIES in Lebanon from causing trouble. If they don’t, we’ll hit Iran very hard again, just like we did last week, only harder!!” while also telling Fox News, he said he told Iranian leaders directly that if they close Hormuz, “You won’t even make it back” to Iran, using an expletive. Meanwhile Israeli Defense Minister Israel Katz said on Sunday that “[t]here has been, and there is, no restriction on IDF soldiers in Lebanon acting to remove threats.”

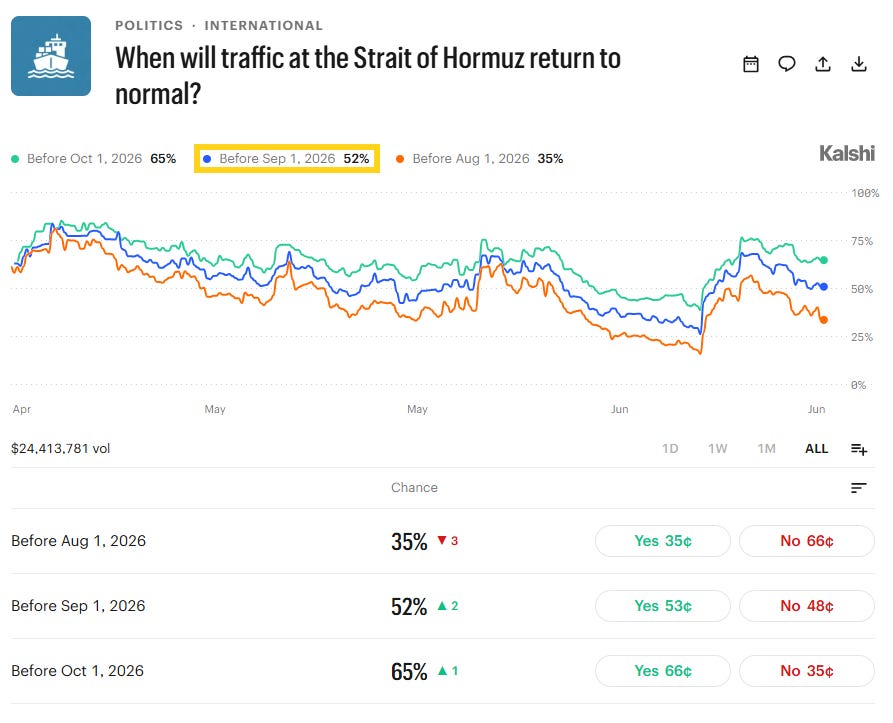

So we’ll just have to see how things progress. Reports are the two sides are currently still in negotiations and traffic is making its way through the Strait, although Kalshi gives it just 50/50 odds that traffic through the Strait normalizes by Sept 1st. The sides have already made “great progress” over the last few hours, Vice President Vance told reporters on Sunday in Switzerland.

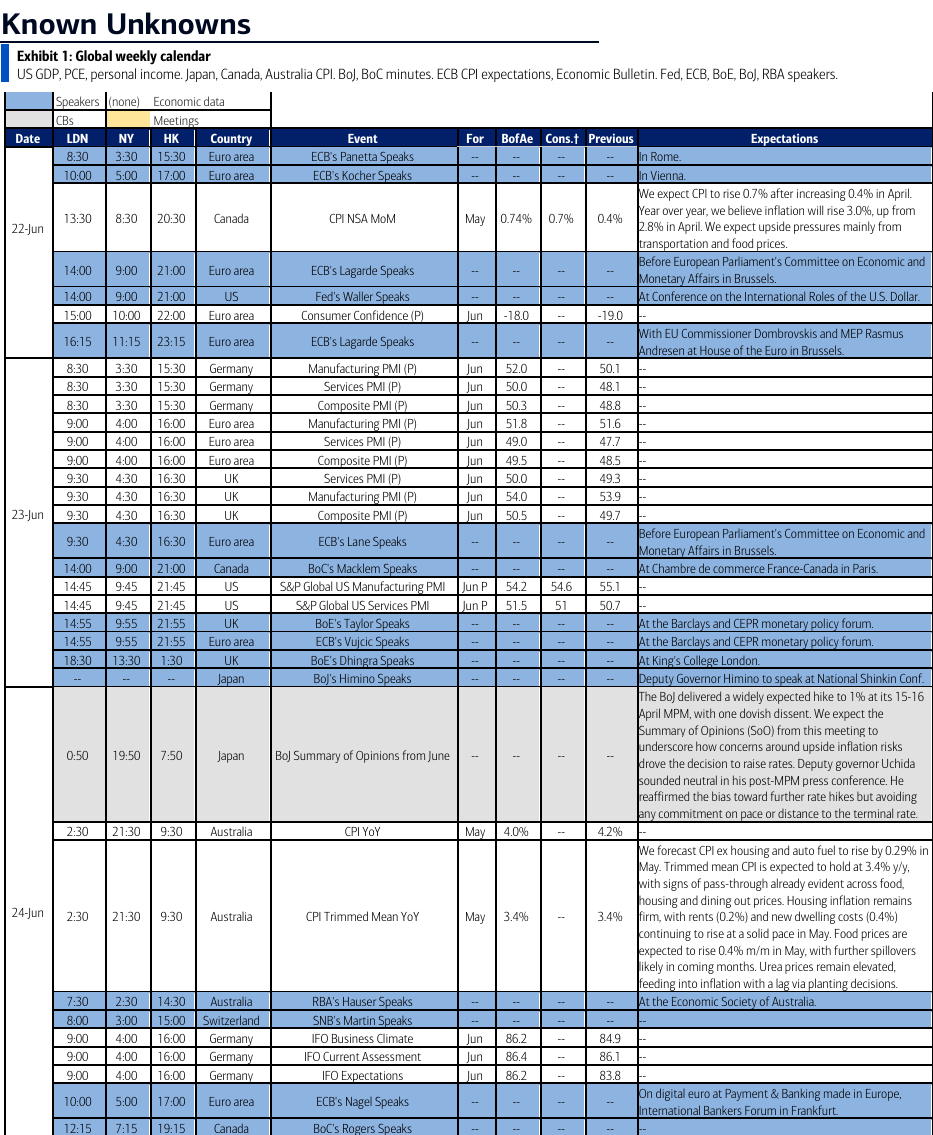

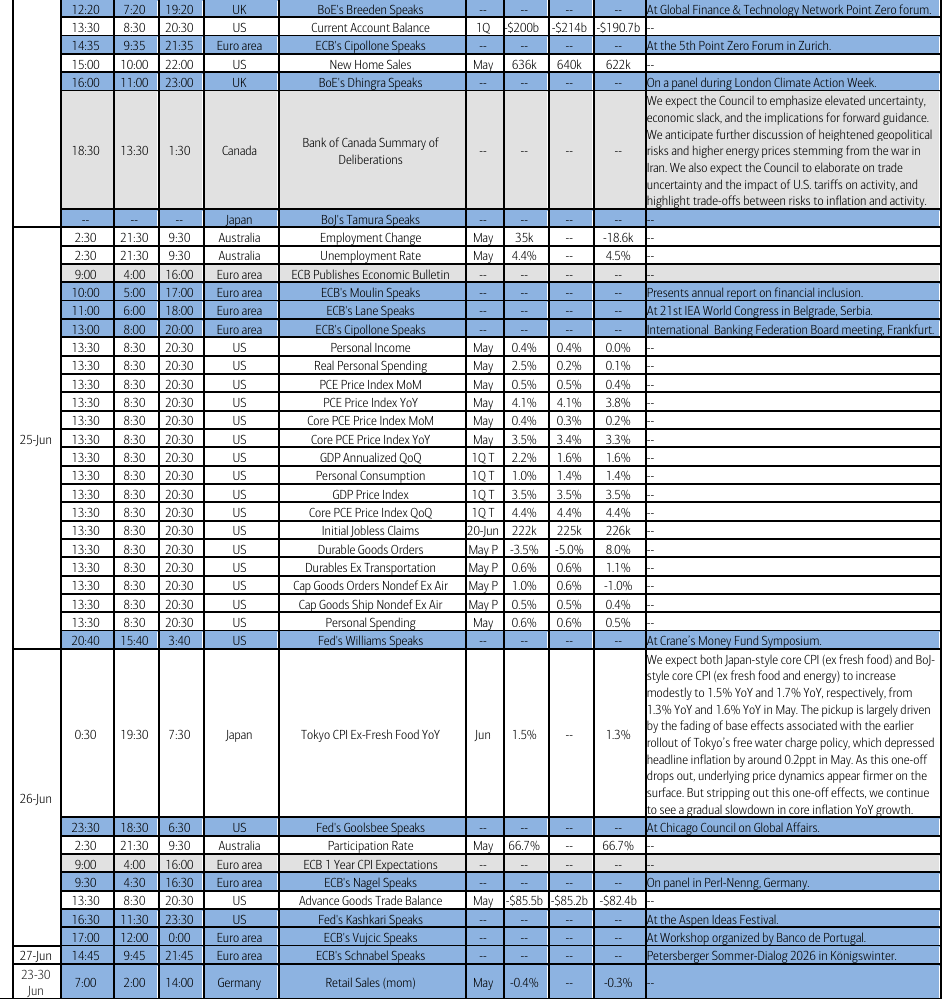

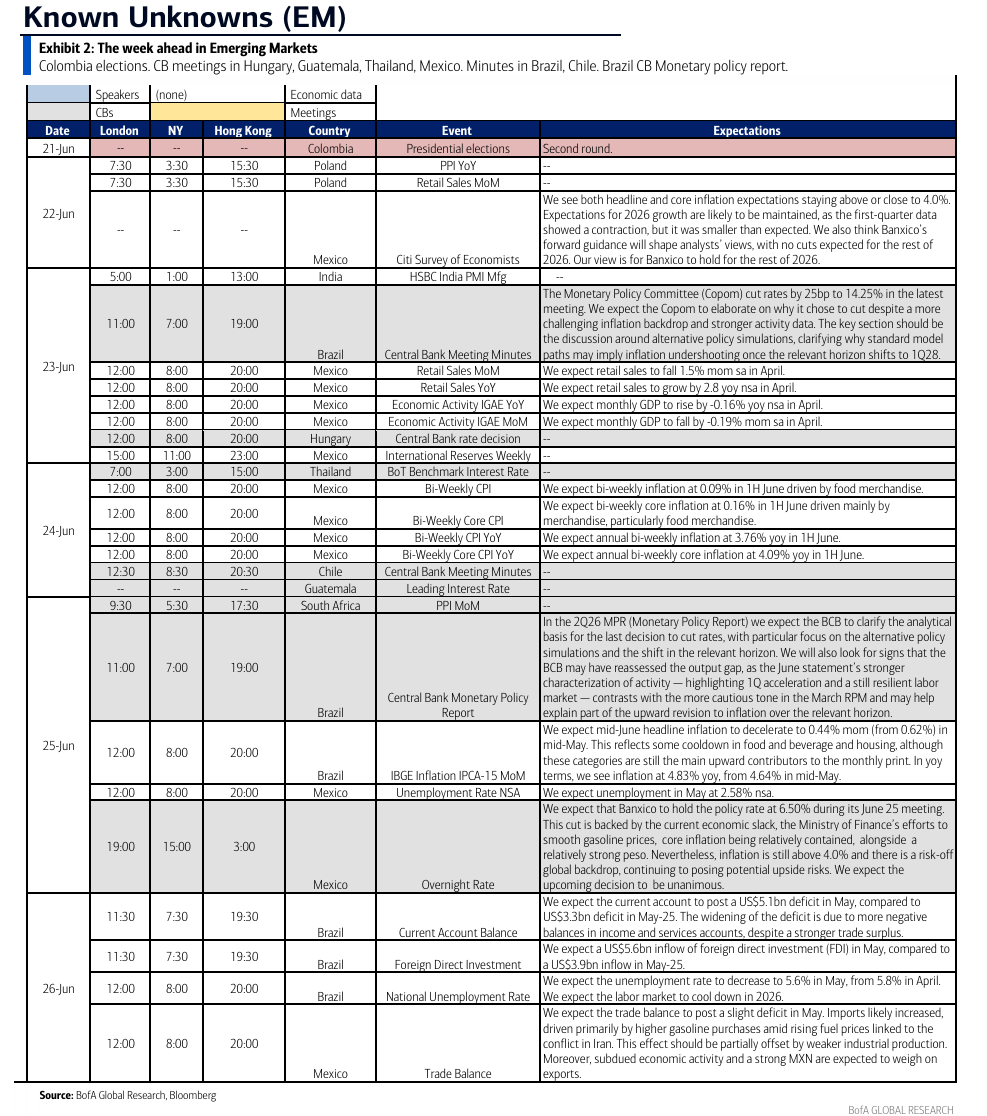

Ex-US highlights from DB:

The global flash PMIs will be amongst the main data highlights next week.

In Europe, UK politics will also be in focus after reports that Prime Minister Starmer will step down likely clearing the way for Andy Burnham to become the next PM following his resounding victory in the Makerfield by-election. Also, in addition to the PMIs, sentiment indicators in Germany will include the Ifo survey (Wednesday) and the July GfK consumer confidence print (Thursday). In France, there will be business confidence on Tuesday and consumer confidence on Thursday. Finally, the ECB will release its May consumer expectations survey on Friday, with inflation expectations in focus. ECB speakers will include President Lagarde amongst others.

In Asia, inflation prints due include the Tokyo CPI for June on Friday in Japan and Australia’s May CPI due Wednesday. Other notable data features BoJ’s Summary of Opinions from its June meeting (Wednesday), Australia’s labour force survey (Thursday) and the 1-year and 5-year loan prime rates in China (Monday).

Here’s their one-pager:

And BoA’s cheat sheets:

In this week’s Week Ahead:

How the economy continues to exceed expectations but also keeps pressure on inflation, including last week’s stronger retail sales report, the latest GDP trackers, the Dallas Fed Weekly Economic Index, Goldman’s Current Activity Indicator, BoA card spending, Redbook sales, trucking demand, and the key labor-market caveats from Goldman and JPM, and a look ahead to data for this week.

How earnings expectations keep powering higher, with Q2, 2026, and 2027 estimates continuing to move up, earnings revisions the strongest since 2022, bottom-up S&P 500 targets continuing to rise, all keeping valuations in check.

Why the earnings story is powerful but also increasingly demanding, including the high bar heading into Q2 earnings season, the surge in long-term Tech earnings expectations, and concerns that some AI-related earnings momentum may be getting ahead of itself.

What breadth is and is not confirming, with mixed signals from the McClellan Summation Index, stocks above key moving averages, equal-weight vs cap-weight performance, small caps vs large caps, and growth/value.

A detailed look at positioning and flows after the largest options expiration on record, including positioning metrics from BofA, Deutsche Bank, Tier1Alpha, and more that cover composite positioning, discretionary vs systematic exposure, CTAs, vol-control sensitivity, leveraged ETFs, retail activity, put/call ratios, buybacks, pensions, liquidity, correlations, and gamma.

Why retail demand remains one of the strongest supports for the market, even as some seasonal flow headwinds may emerge in July.

Why near-term technical conditions may be choppier after OpEx, with less gamma support, possible quarter-end pension rebalancing, fading buybacks, and tighter liquidity all creating more room for market noise.

A full sentiment check, including AAII, NAAIM, Goldman’s sentiment indicator (off this week), CNN Fear & Greed, BoA’s Bull & Bear Indicator, and Helene Meisler’s weekend poll.

A look at seasonality, including the weak late-June midterm-year pattern, the post-new-Fed-chair setup, and broader second-half market statistics.

A lot on the Fed and rates after Chair Warsh’s first meeting, including the front-end repricing, the flattening yield curve, inflation expectations, Fed funds pricing, and the latest views from Goldman, BoA, Morgan Stanley, Deutsche Bank, JPM, Yardeni, and others.

Note: While I cannot post BoA charts on X, I include many in the Week Ahead.