The Week Ahead - 6/28/26

A look at the upcoming week for the US economy and equities — covering key drivers including earnings, positioning, breadth, valuations, sentiment, seasonality, and the Fed.

The Week Ahead

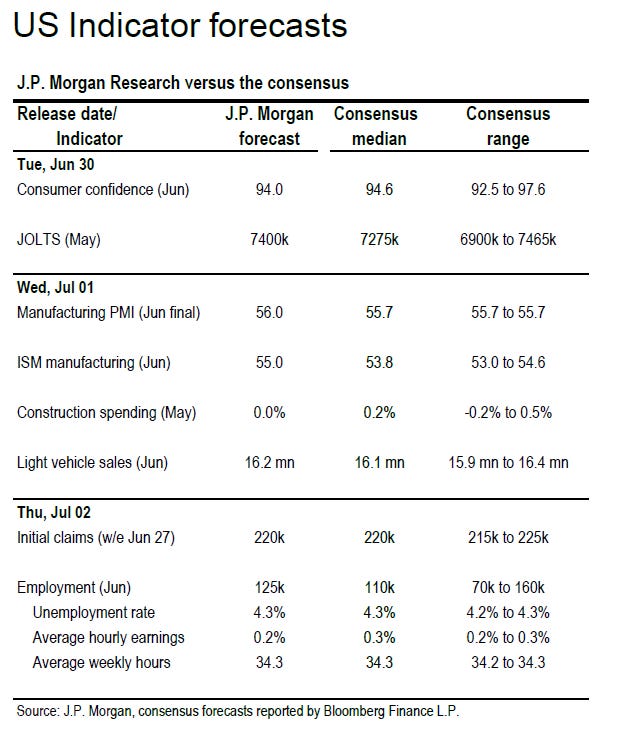

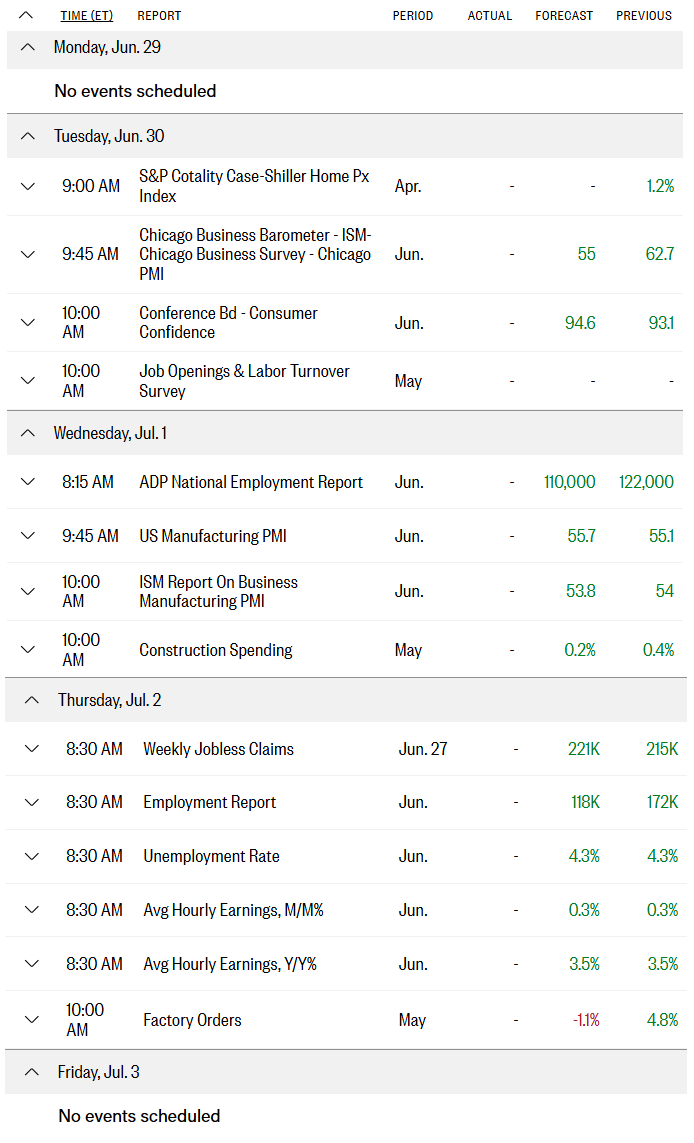

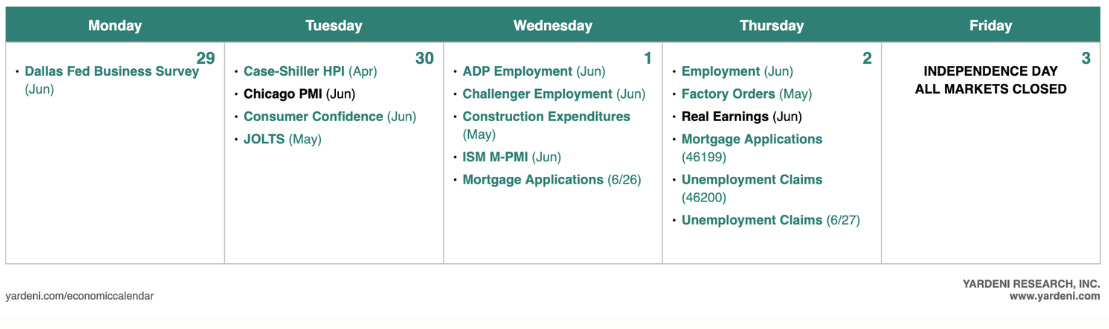

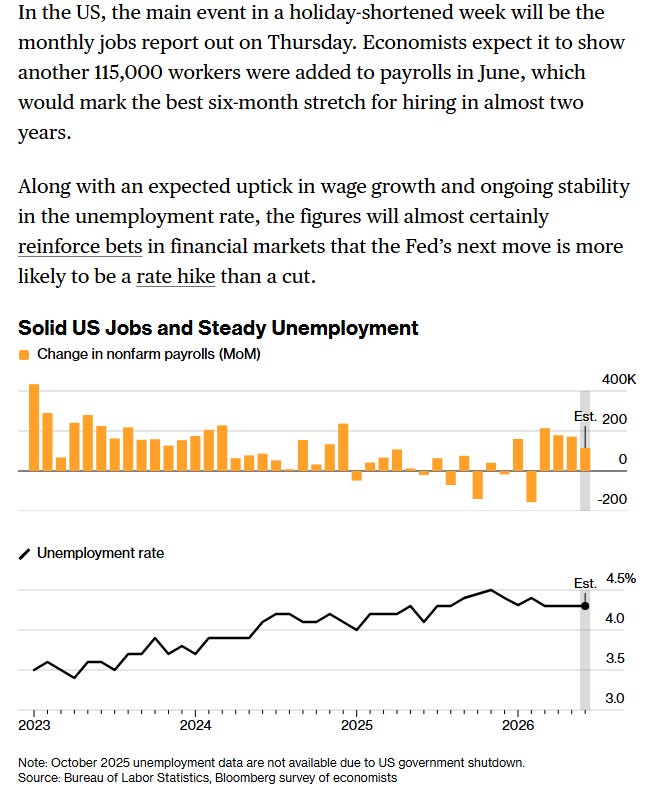

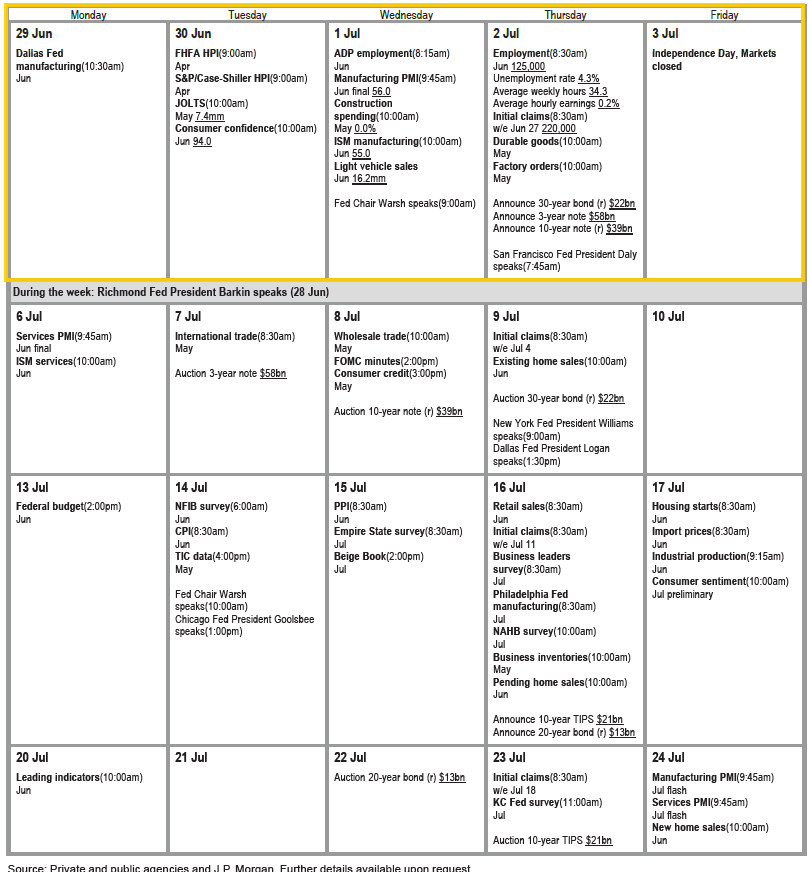

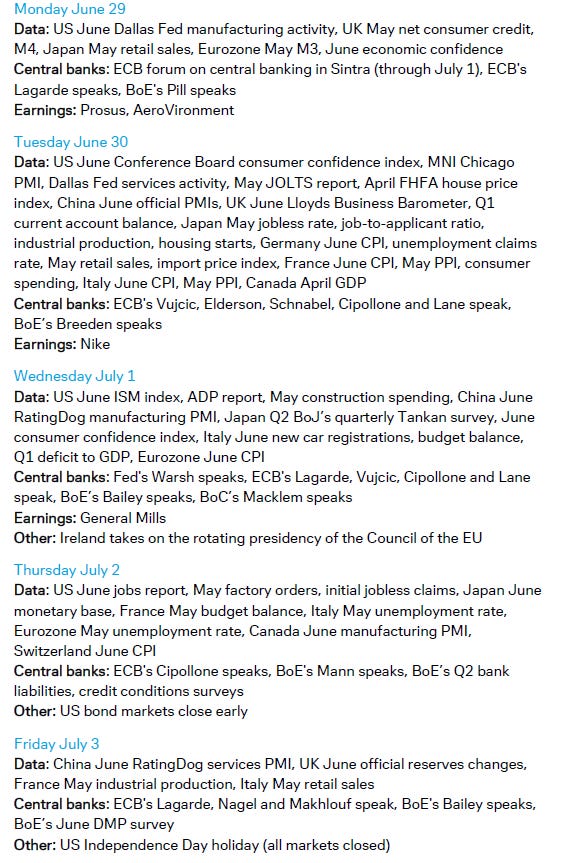

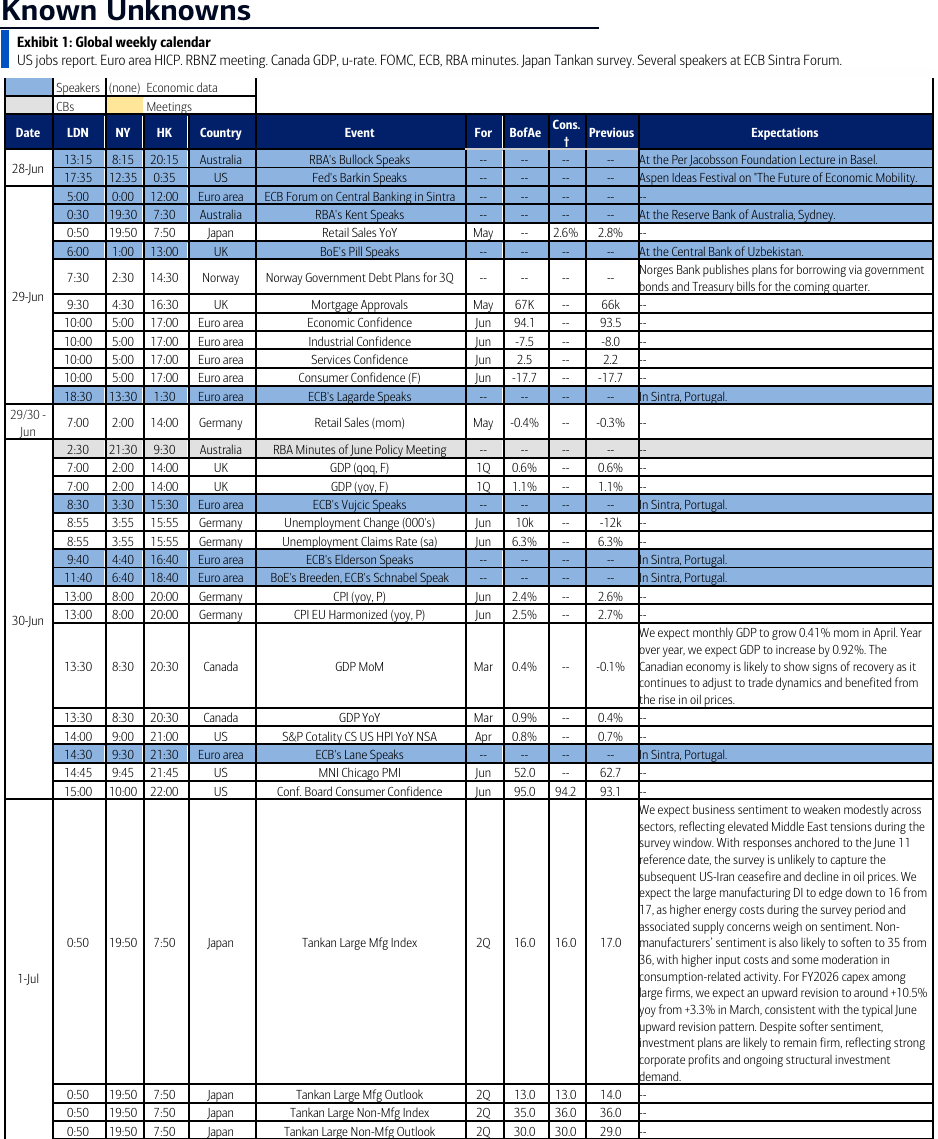

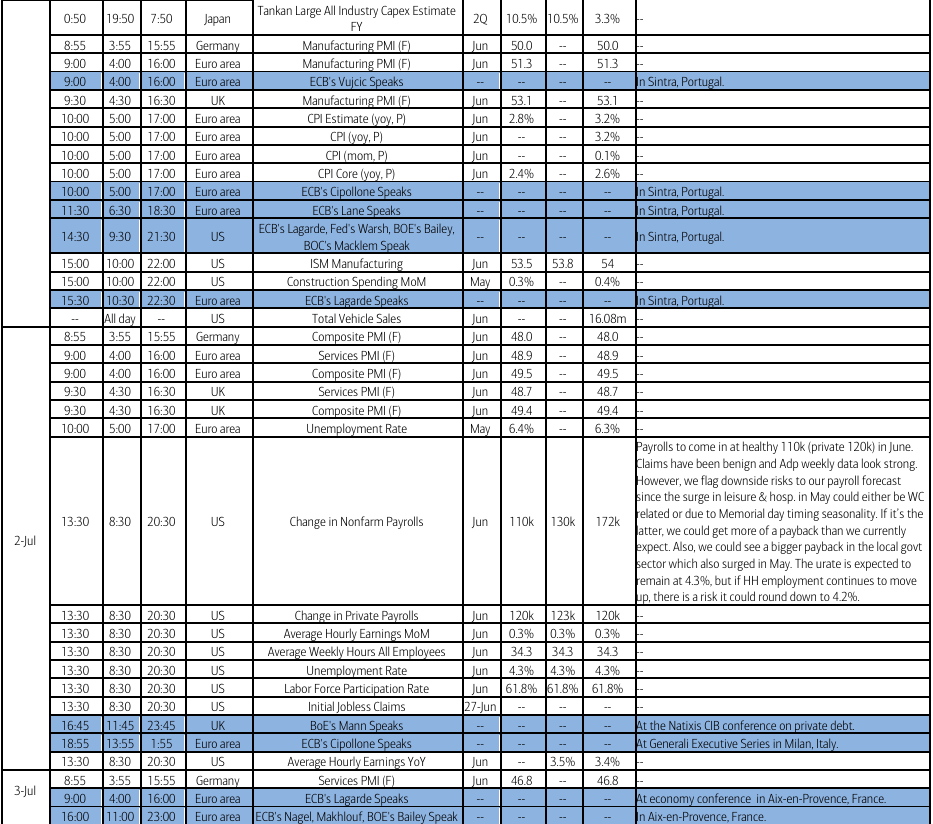

Next week includes part of the first week of the month, which also means it’s jobs week in the US, but with July starting on Wednesday, and a market holiday in the US Friday (July 4th falls on a Saturday), instead of culminating Friday, we’ll get the June Nonfarm Payrolls (technically the Employment Situation report) on Thursday, and we’ll only get some of the normal first week of the month reports.

What we will get as usual are June ADP monthly employment, Challenger job cuts, manufacturing PMIs (but not services PMIs), and auto sales, May JOLTS, construction spending, and factory orders, as well as the standard weekly reports (jobless claims, mortgage applications, and US petroleum inventories (not ADP though with the monthly report this week)). We’ll also get the June consumer confidence report from the Conference Board and April repeat house price indices.

I don’t have a good calendar of Fed speakers, but I do know Chair Warsh will be speaking Wednesday morning on a panel at the ECB’s Forum on Central Banking 2026, in Sintra, Portugal.

In terms of non-Bill (>1yr in duration) US Treasury auctions, we’re off next week.

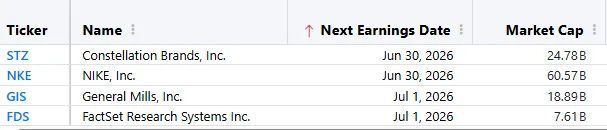

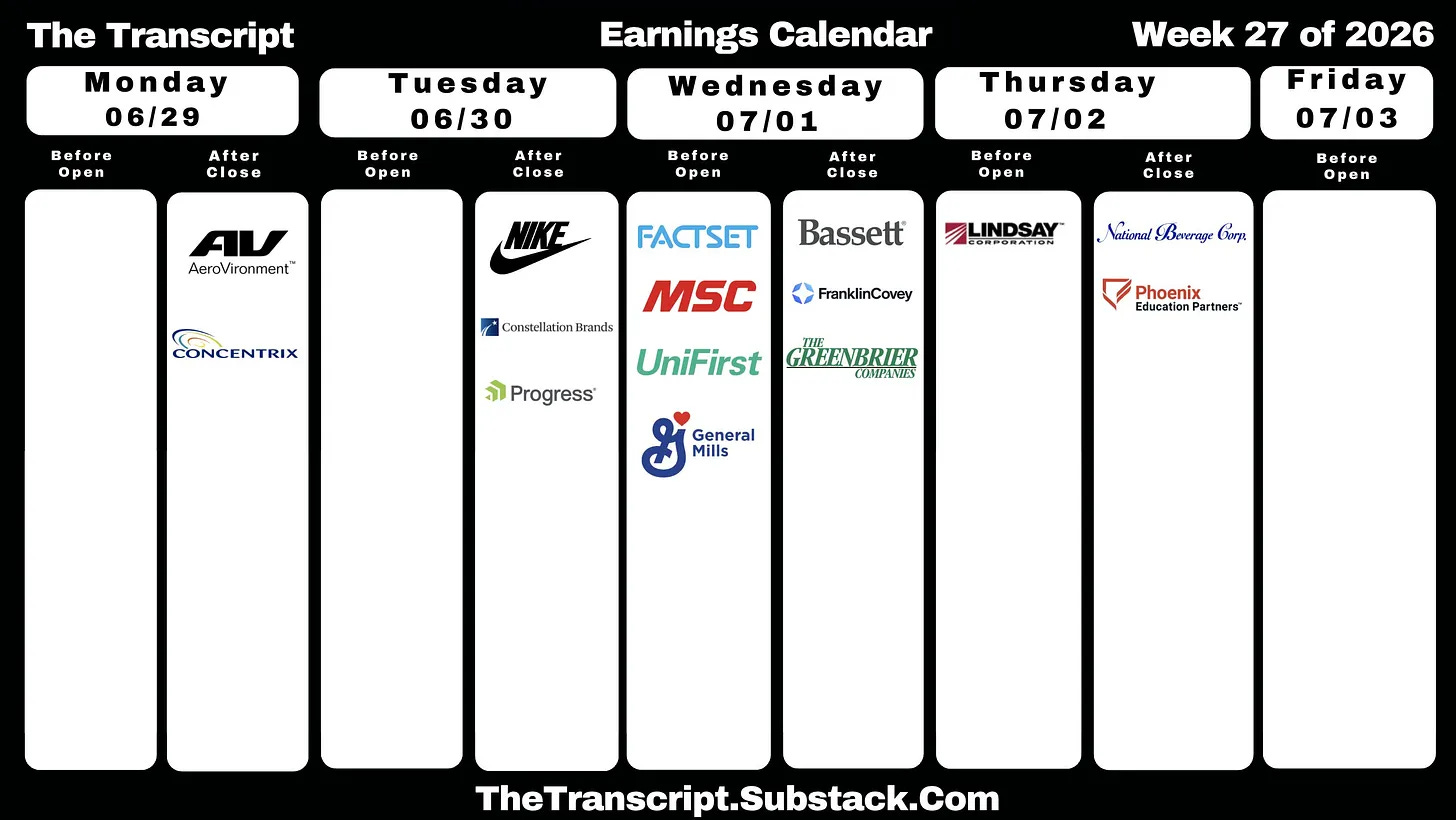

In terms of earnings, we remain in the weird period where Q1 earnings season is ending and Q2 is starting. Next week we have four SPX components reporting in STZ, NKE, GIS, FDS.

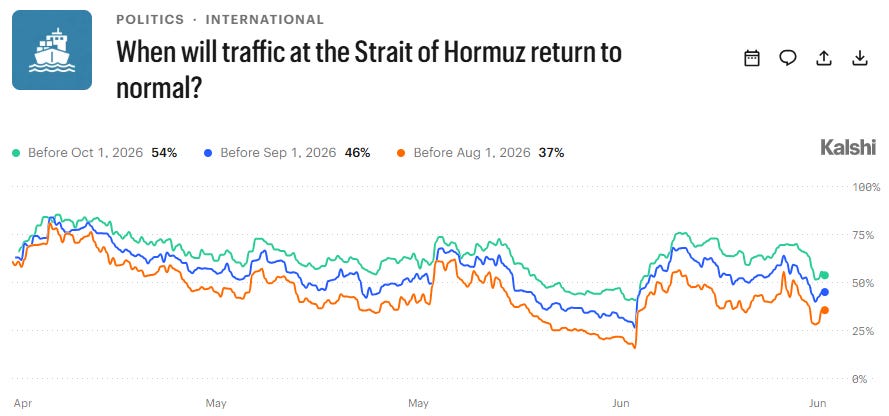

In terms of Iran, as noted last week, four-party talks had been ongoing in Switzerland, but as I said then “that doesn’t mean of course ‘all is well” as things seem to remain fragile.” That fragility was on display this weekend with the two sides trading fire, and reports that talks between the parties were cancelled indefinitely, while the WSJ reported that Foreign Minister Abbas Araghchi said that Iran has the exclusive right to manage traffic in the Strait of Hormuz.

Just a few hours later Axios reported that the U.S. and Iran agreed to stop attacking each other, according to a senior U.S. official, as the two sides plan to meet Tuesday in Qatar's capital to work out their dispute over the Strait of Hormuz. So while this seemed for a bit like things were becoming unglued, it appears in the end it was just more aggressive posturing from both sides as they remind each other of the power each possesses in the event negotiations truly fall apart.

So as I said two weeks ago “we’ll just have to see how things progress”. While odds on Kalshi that traffic through the Strait would normalize by Sept 1st had risen as high as 68% two weeks ago, that has dropped to 46% today.

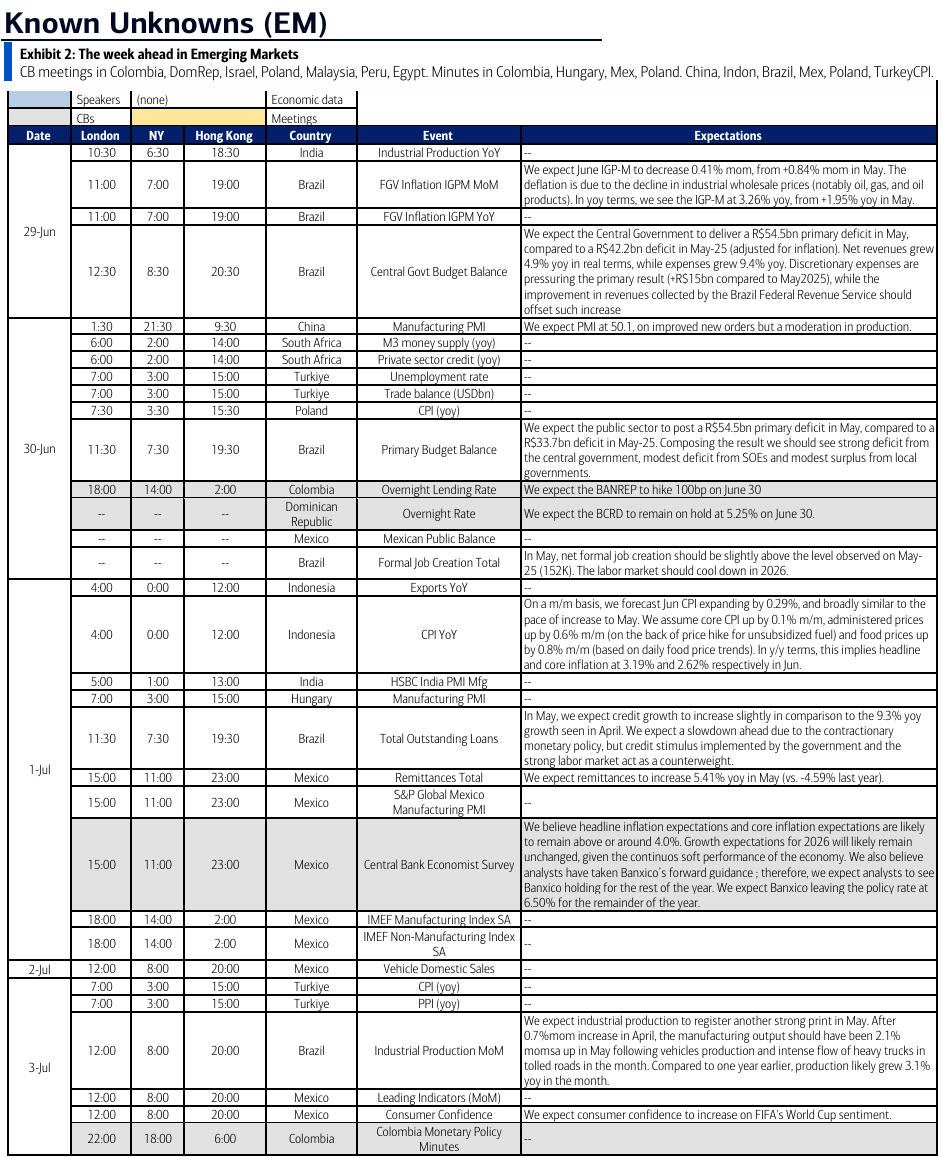

Ex-US highlights from DB:

In Europe, the main event will be the ECB’s annual forum on central banking in Sintra, which runs from Monday through Wednesday, with this year’s title “Shaping Europe’s future: innovation, growth and stability.” Speakers will include ECB President Lagarde, Fed Chair Warsh, BoE Governor Bailey and BoC Governor Macklem, alongside several ECB officials. In the UK, the BoE will release bank liabilities and credit conditions surveys on Thursday and the DMP survey on Friday.

In economic indicators, the focus will be on the June flash CPI prints in the Eurozone. Spain and Belgium kick off the reports on Monday, with data for Germany, France and Italy, amongst others, due Tuesday and the Eurozone-wide measure out on Wednesday. Our European economists forecasts include 2.46% YoY for Germany, 2.30% for France, 3.23% for Italy and 2.95% for the Eurozone. Finally, there will also be the June CPI report in Switzerland on Thursday.

Over in Asia, highlights in China include the June PMIs, with the official gauges due Tuesday. In Japan, data releases feature May retail sales on Monday and industrial production on Tuesday. Our Chief Japan economist expects industrial production to rise +1.4% MoM in May and also highlights the BoJ’s quarterly Tankan survey (Wednesday) as the most important release. He expects the survey to continue showing steady sentiment overall with several components supporting the case for early additional rate hikes by the BoJ.

Here’s their one-pager:

And BoA’s cheat sheets:

In this week’s Week Ahead:

How the economy continues to exceed expectations but also keeps pressure on inflation, including last week’s personal income and spending report, the latest GDP trackers, the Dallas Fed Weekly Economic Index, Goldman’s Current Activity Indicator, accelerating BoA card spending, Redbook sales, improving lower-income spending, and firmer CFO sentiment.

How earnings expectations keep powering higher, with Q2, 2026, and 2027 estimates continuing to move up, including Goldman’s thoughts on the Q2 earnings season, earnings revisions that have decelerated but still mark the strongest eight-week stretch since 2022, bottom-up S&P 500 targets continuing to rise, and the earnings surge helping keep valuations in check.

How the earnings story is powerful but also increasingly demanding, including the high bar heading into Q2 earnings season for the aggregate index, the lower bar for the median company, upside risk from conservative median sales forecasts, and continued concerns that some AI-related earnings momentum may be getting ahead of itself.

What breadth is and is not confirming, with mixed signals from the McClellan Summation Index, stocks above key moving averages, equal-weight vs. cap-weight performance, small caps vs. large caps, growth/value, and new highs versus new lows.

A detailed look at positioning and flows including potential near-term flow issues from BofA, Deutsche Bank, Tier1Alpha, Citadel, and others covering composite positioning, discretionary vs. systematic exposure, CTAs, vol-control sensitivity, leveraged ETFs, retail activity, put/call ratios, buybacks, pensions, foreign demand, liquidity, correlations, and gamma.

Why leveraged ETFs and single-stock speculation remain an important short-term market-structure risk, particularly around memory stocks, semis, and the potential for forced flows to amplify moves in either direction.

A full sentiment check, including AAII, NAAIM, Goldman’s sentiment indicator, CNN Fear & Greed, BoA’s Bull & Bear Indicator, Helene Meisler’s weekend poll, and Yardeni’s broader bull/bear work.

A look at seasonality, including early-July strength, July as a whole, and the more mixed midterm-year backdrop.

A look at the Fed and rates, including inflation expectations, Fed funds pricing, the recent softening, and potential reduced forward guidance under Chair Warsh.

Note: While I cannot post BoA charts on X, I include many in the Week Ahead.