The Week Ahead - 6/7/26

A look at the upcoming week for the US economy and equities — covering key drivers including positioning, breadth, sentiment, and the Fed.

Note: The free portion is unchanged, I just added sections for subscribers on the economy, positioning, breadth, sentiment, and the Fed (and short wrap-up) including commentary from Goldman, BoA, Tier1Alpha, etc.

The Week Ahead

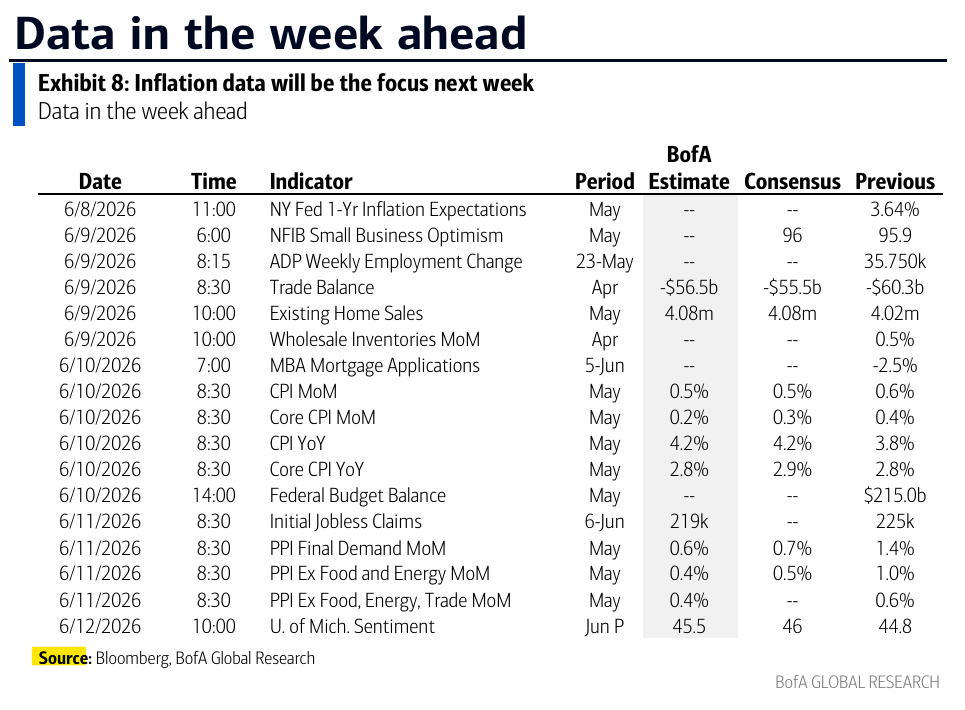

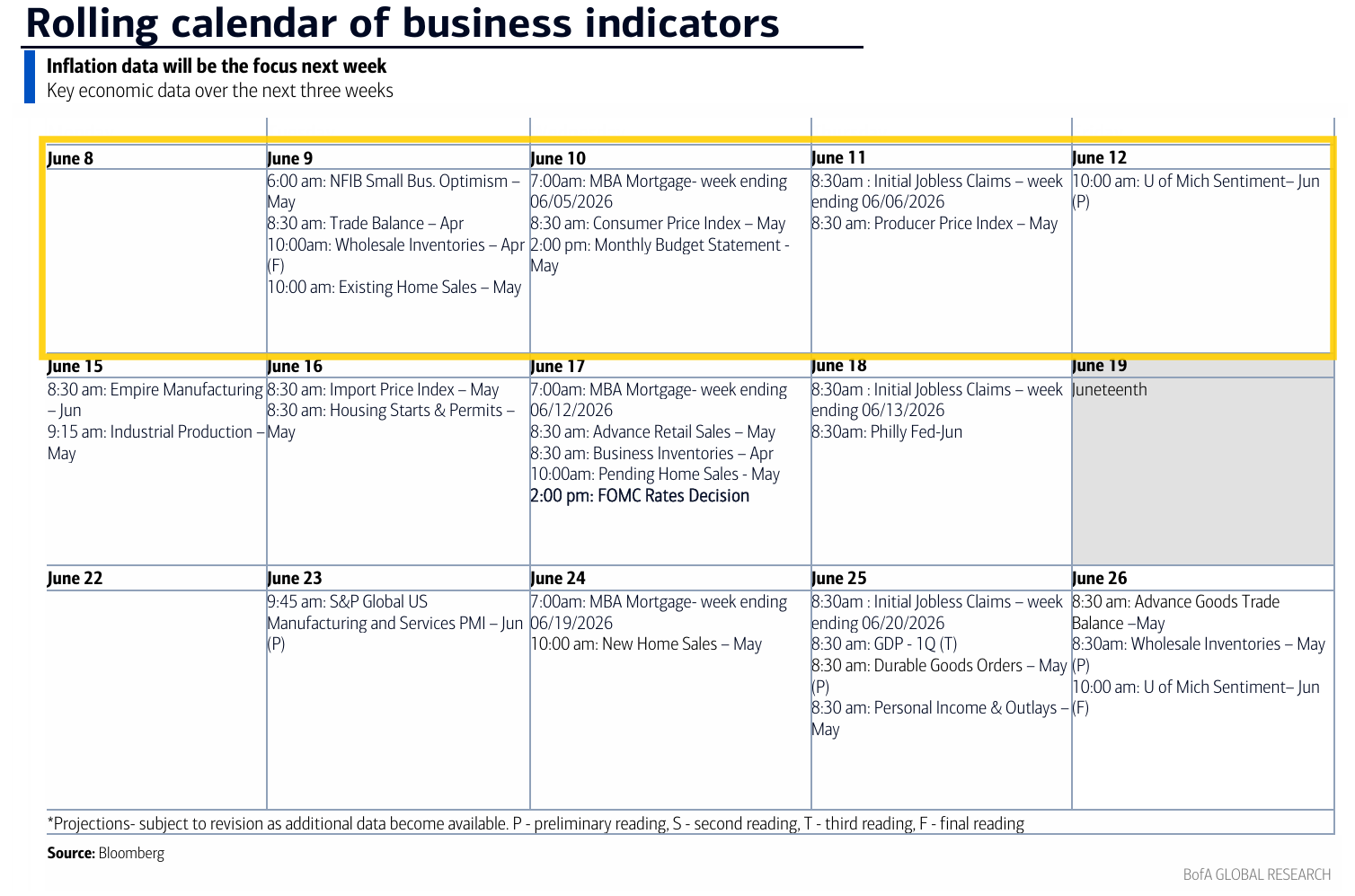

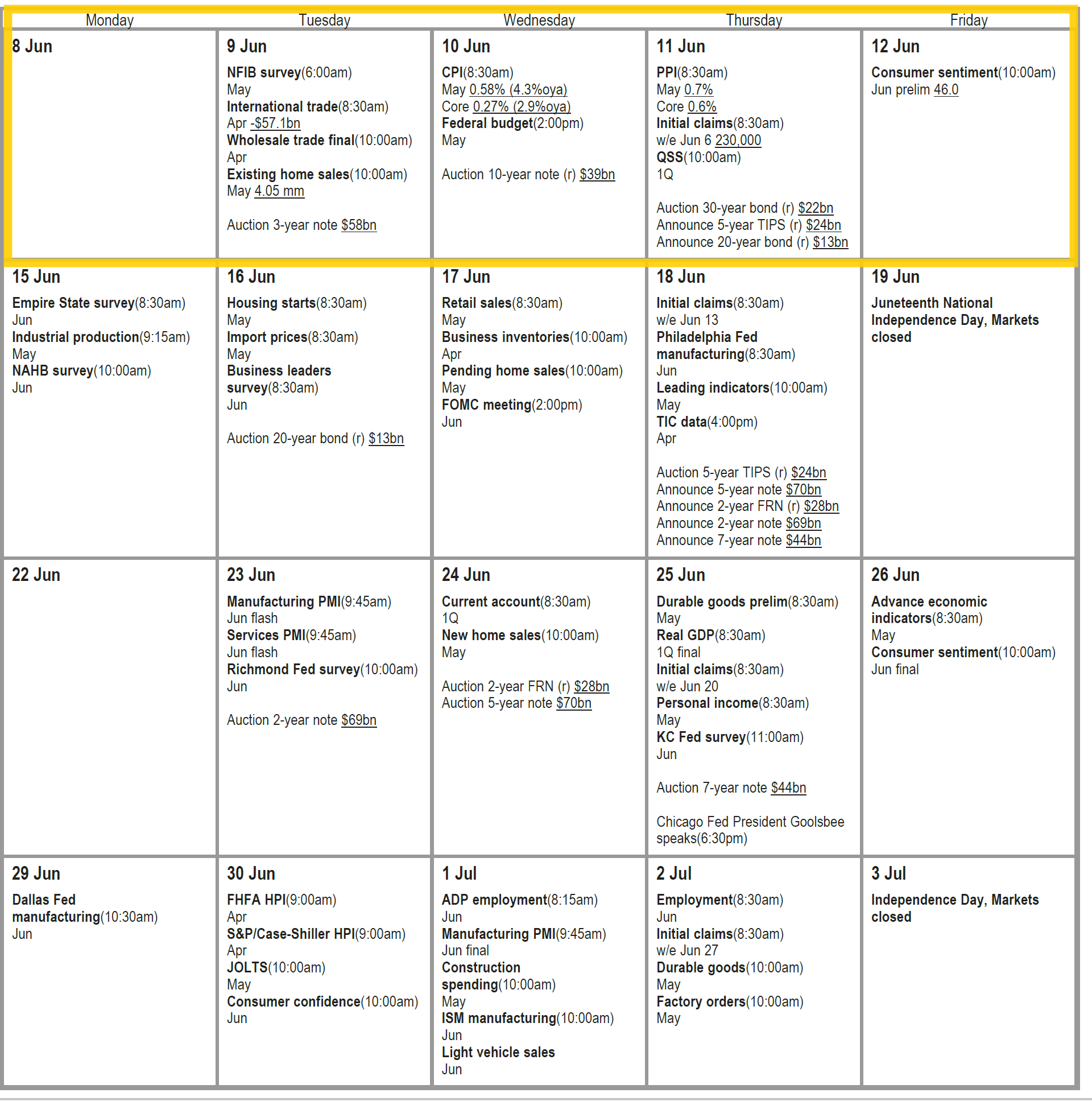

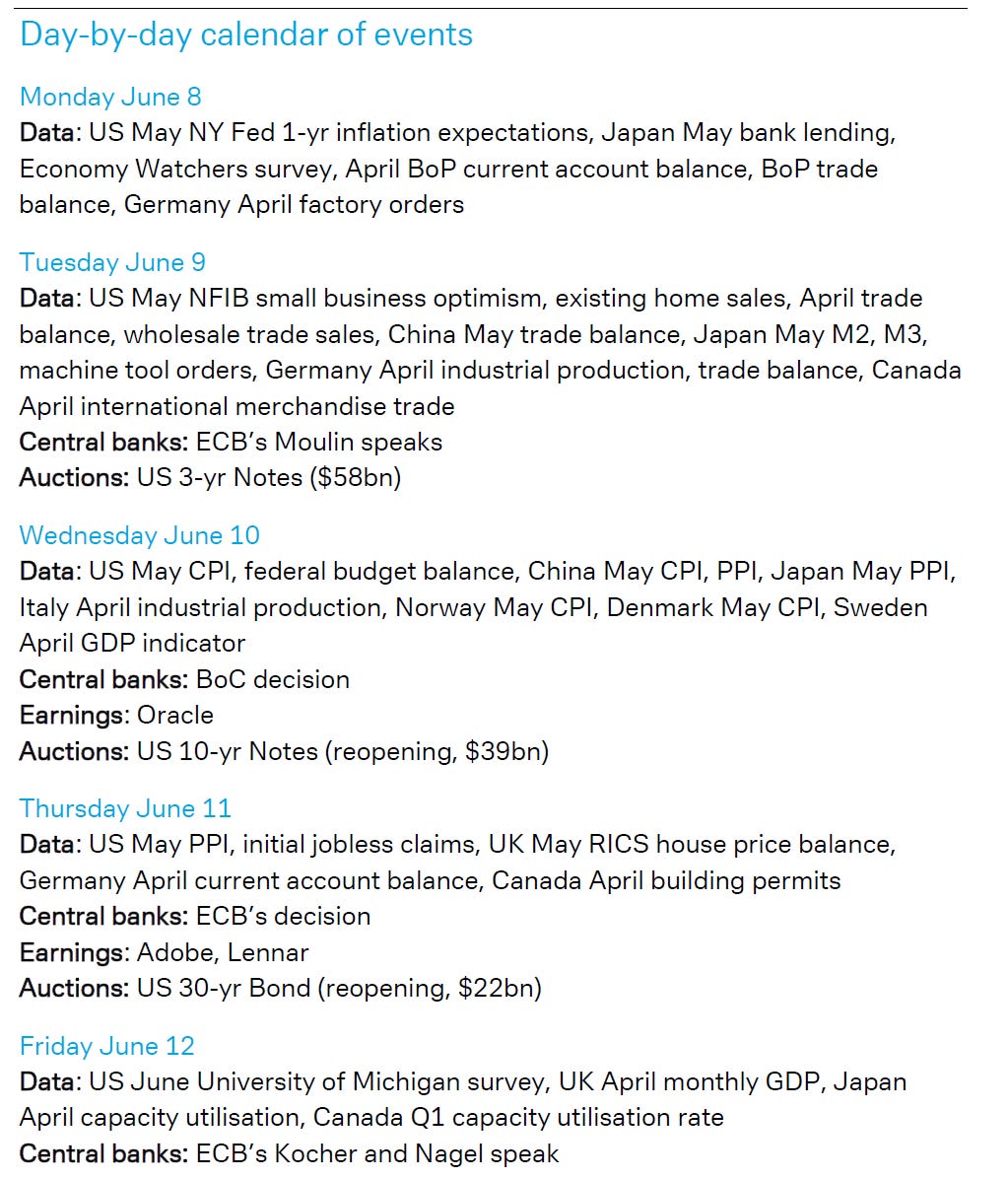

This week we’ll get the traditional second week of the month focus on inflation, although we’ll only get two of the three reports we normally get (but the most important), in May CPI and PPI (import prices is the following week). Other reports include existing home sales, the NY Fed consumer survey, and NFIB small business sentiment as well as the April trade balance, June UMich preliminary consumer sentiment plus the standard weekly reports (ADP, jobless claims, etc.).

The Fed blackout has started so no Fed speakers this week.

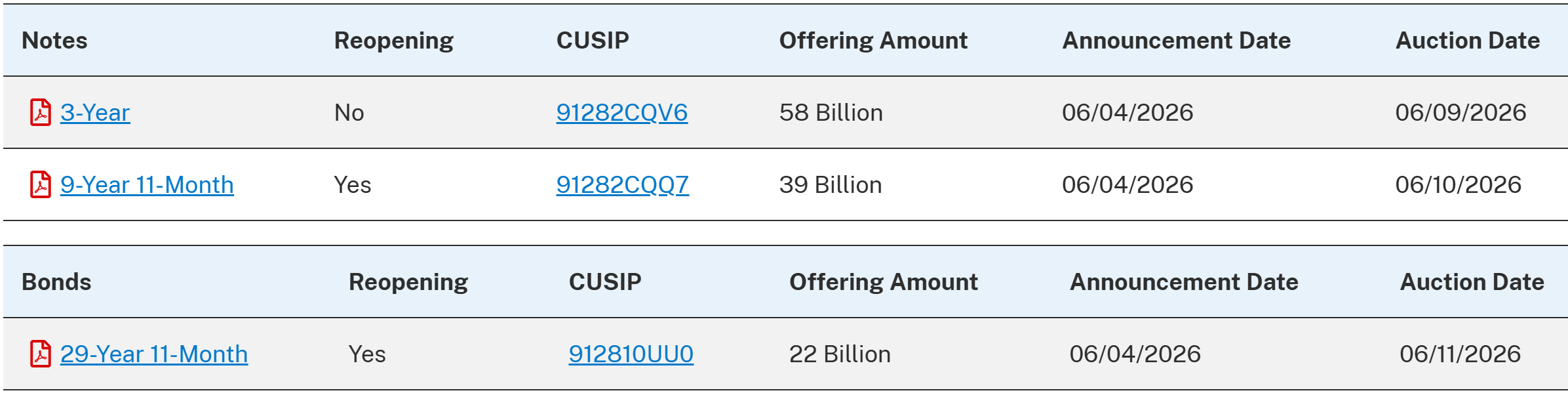

US Treasury auctions pick back up for non-Bills (>1yr in duration) with 3, 10, and 30-yr auctions Mon, Tues, Wed, respectively (a day earlier than normal due to Friday’s settlement).

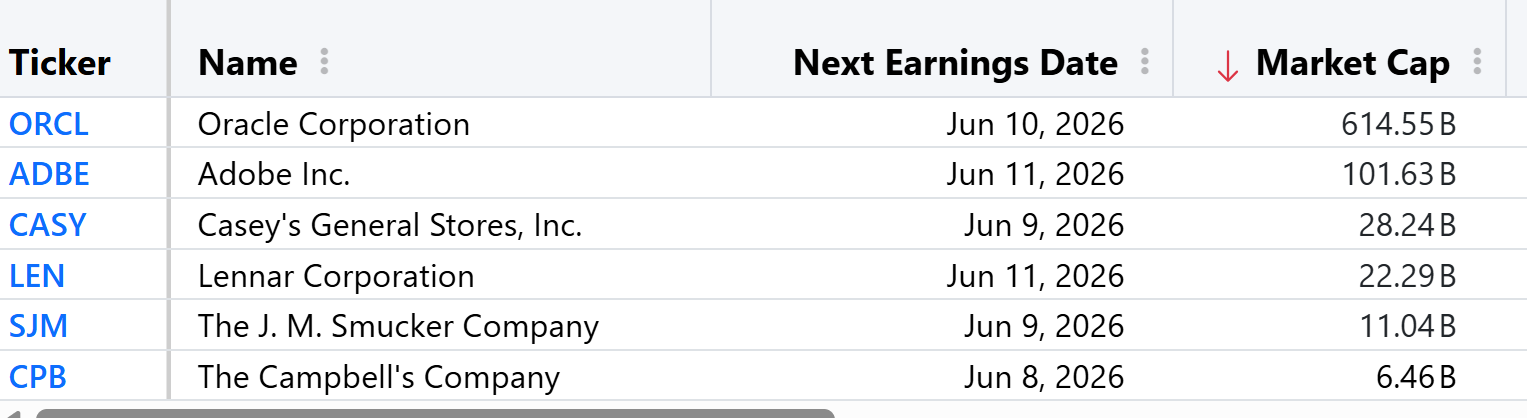

Q1 earnings season will continue to wind down with 6 SPX components reporting, although we will get another company in the AI spotlight in Oracle (ORCL). Their results could help end or continue the current selloff in those names. One other >$100bn market cap reporters is ADBE.

But perhaps more notable will be the highly anticipated debut of SpaceX. SpaceX (SPCX) is expected to begin trading on Friday after pricing one of the largest IPOs in history. The company is seeking to raise about $75B at a valuation approaching $1.8T. 30% of the shares have been set aside for retail investors.

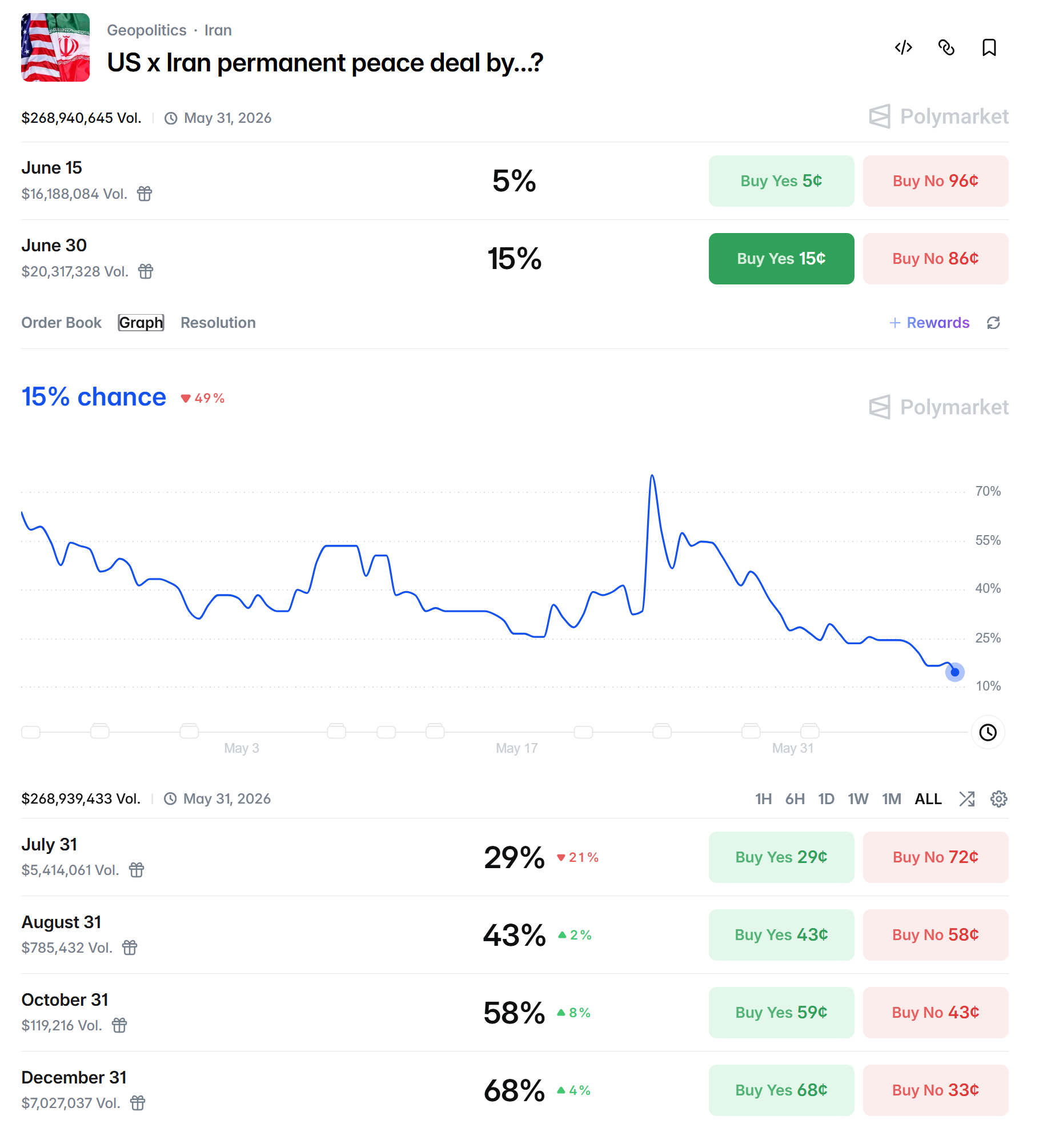

In terms of the Iran war, as I have been saying for a while, “it continues to drag on with no end in sight.” As I have also noted “It seems that both sides feel they have the upper hand, and both need a conclusion which allows them to claim ‘victory’. Not a setup conducive to a quick conclusion,” but “it is also clear that President Trump’s patience is starting to wear thin.”

As I mentioned two weeks ago “recent events appear to indicate Trump is very much between a rock and a hard place. While it seems he wants to come to an agreement with Iran, Iran knows that and also that with each passing day pressure builds from the coming mid-term elections. And Trump is now getting counter-pressure to ‘finish the job’ from hard-line Republicans who came out with some blistering criticism after Trump said that a deal was imminent Memorial Day weekend.” So while Trump wants a deal, it also has to look like “a good deal,” again all of which Iran knows. It’s no wonder it continues to drag on, and now further complicated by Israel’s renewed attacks on Hezbollah in Lebanon the cessation of which Iran requires for talks.

FWIW Polymarket now just sees a 15% chance of a permanent US-Iran peace deal by June 30th, the least since the contract was opened, and down from nearly 80% two weeks ago.

Ex-US highlights from DB:

In Europe the highlight this week will be the ECB’s decision on Thursday. Our European economists expect a 25bps hike, lifting the deposit rate to 2.25%. Other central bank events will include the BoC decision on Wednesday.

In European data, the key UK release will be April’s monthly GDP on Friday. In Germany, several April indicators early next week will give a snapshot of economic activity including factory orders (Monday), industrial production and trade (Tuesday). There will also be May CPI reports in Denmark and Norway on Wednesday.

Over in Asia, the focus will be on China, with the May trade balance due Tuesday and CPI and PPI reports on Wednesday. Our economists expect China’s reflation to continue in May, with the PPI rising to 3.0% YoY from 2.8% and the CPI edging up to 1.4% YoY from 1.2%. They also see trade remaining strong, with export growth at 15% YoY (14% in April) and import growth staying high at 26% YoY.

In Japan, highlights include the Economy Watchers survey due Monday and May PPI on Wednesday

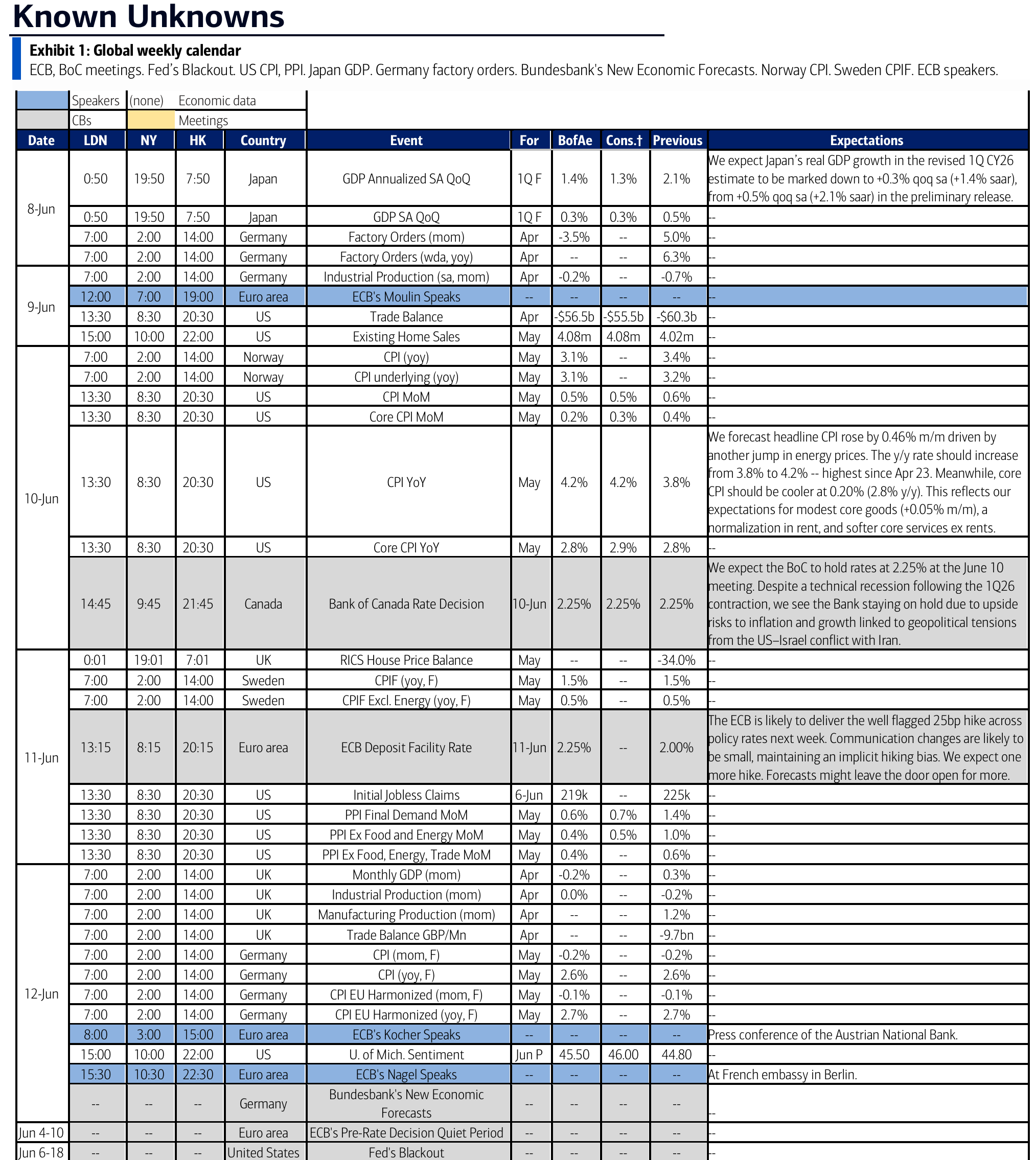

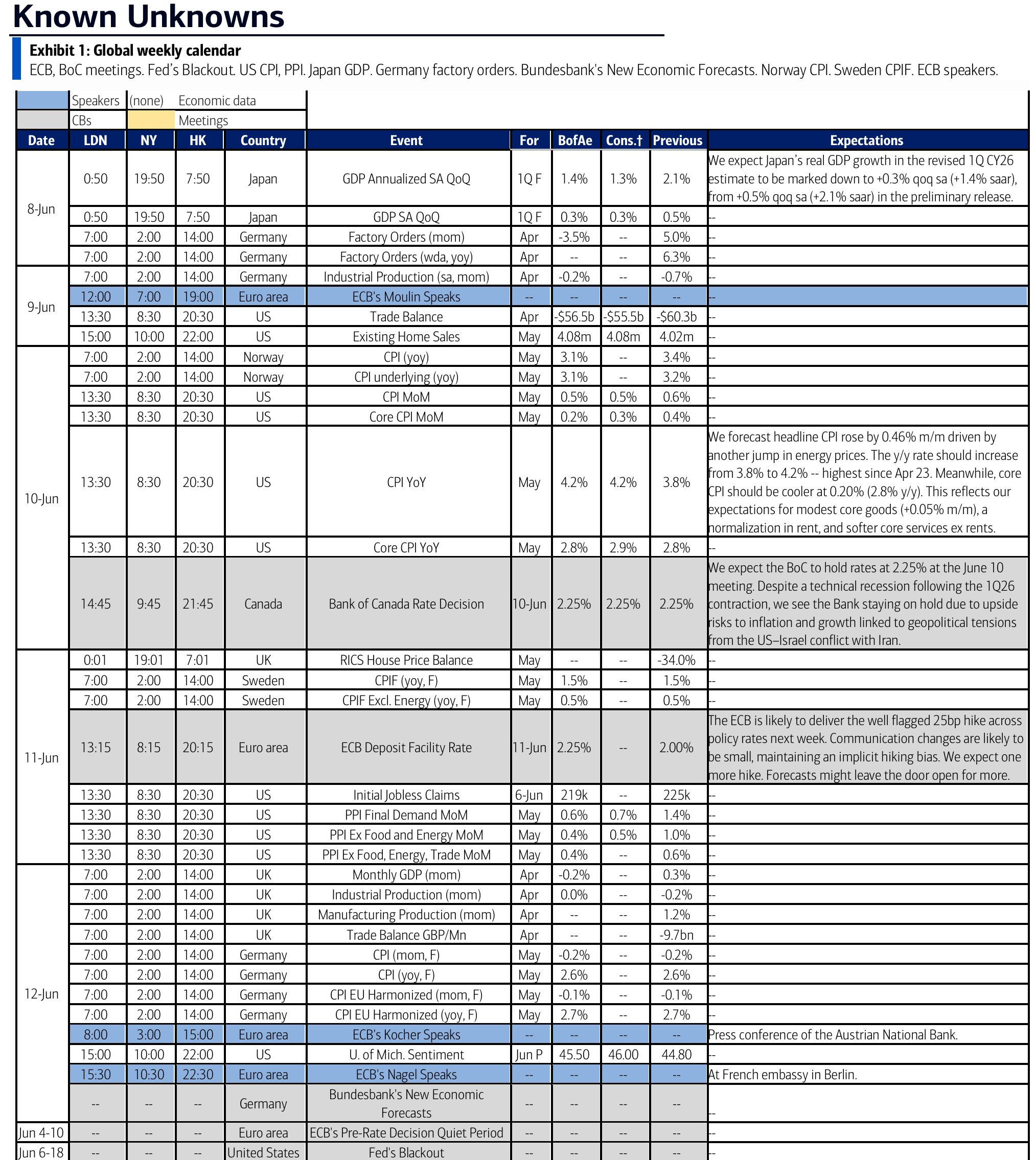

Here’s their one-pager:

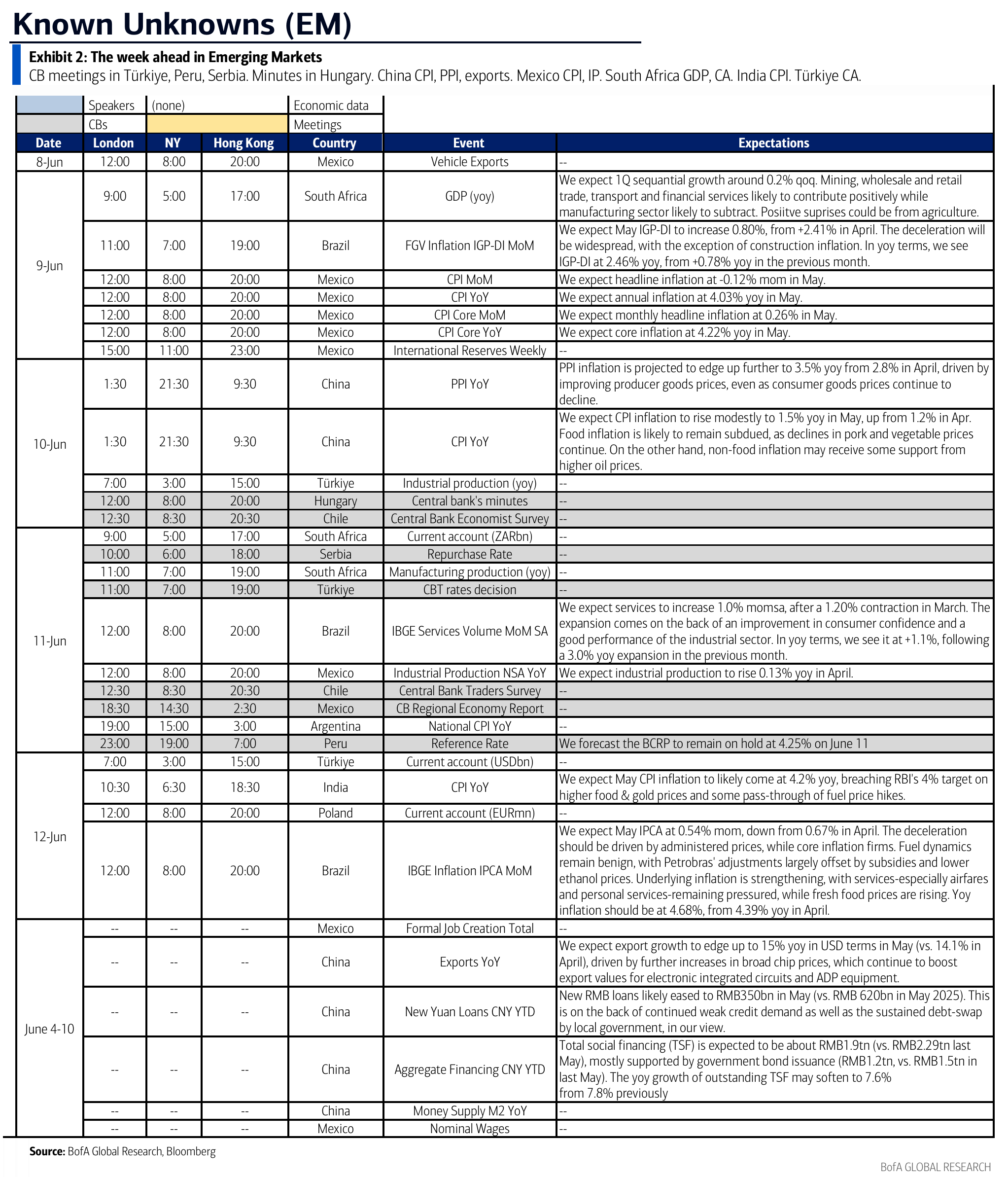

And BoA’s cheat sheets: