The Week Ahead - 7/12/26

A look at the upcoming week for the US economy and equities — covering key drivers including earnings, positioning, breadth, valuations, sentiment, seasonality, and the Fed.

The Week Ahead

After a very light week, things pick up considerably next week.

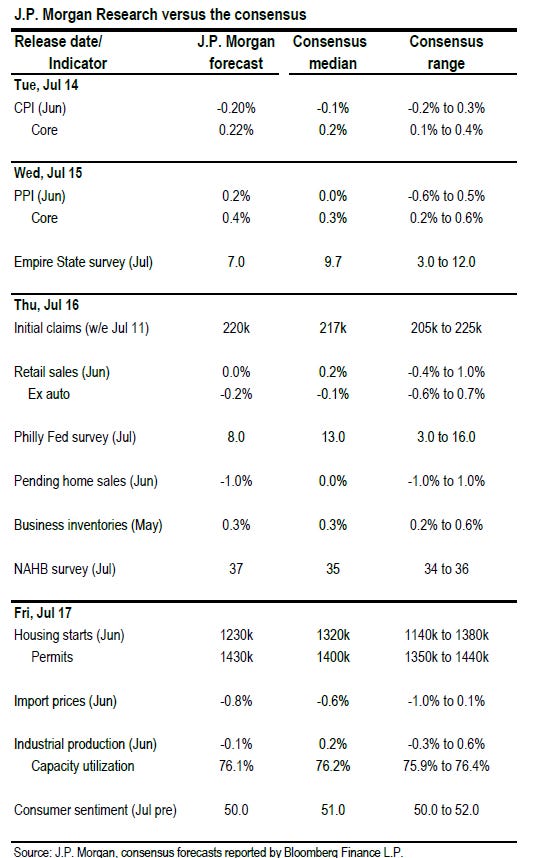

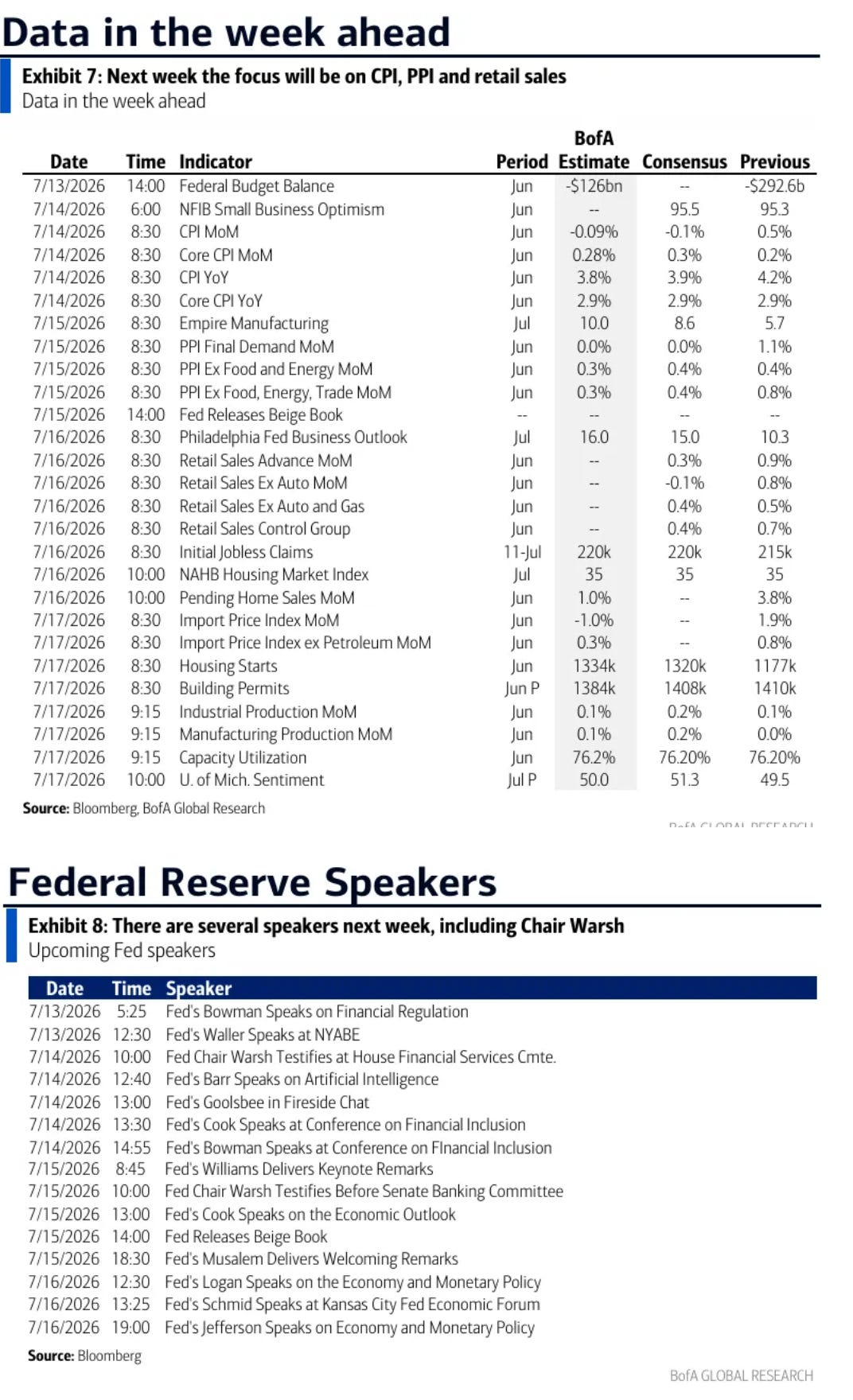

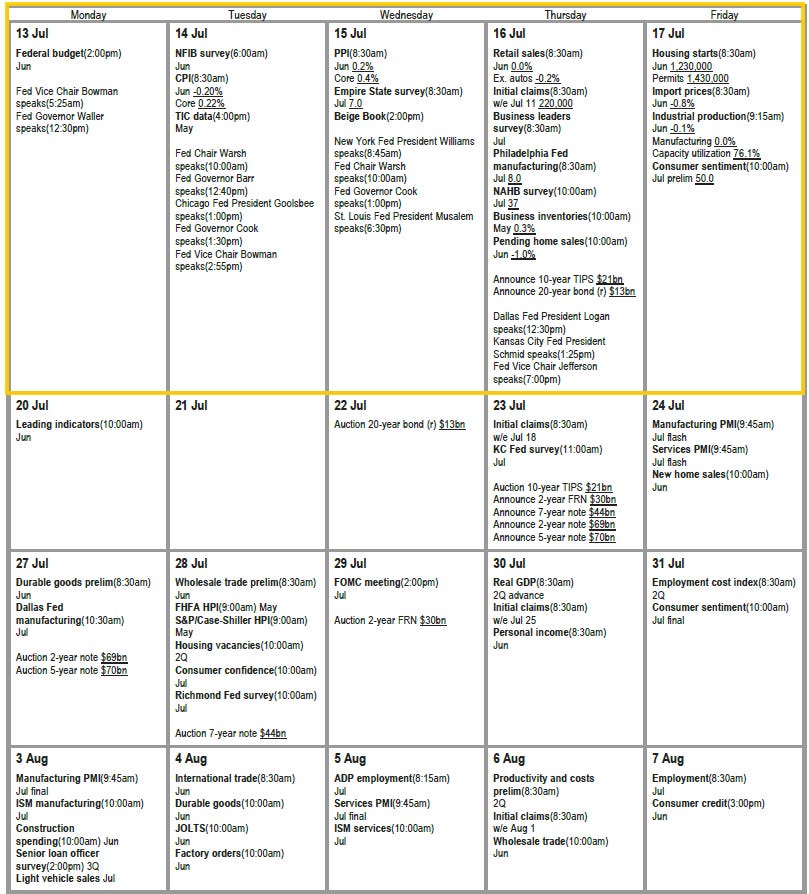

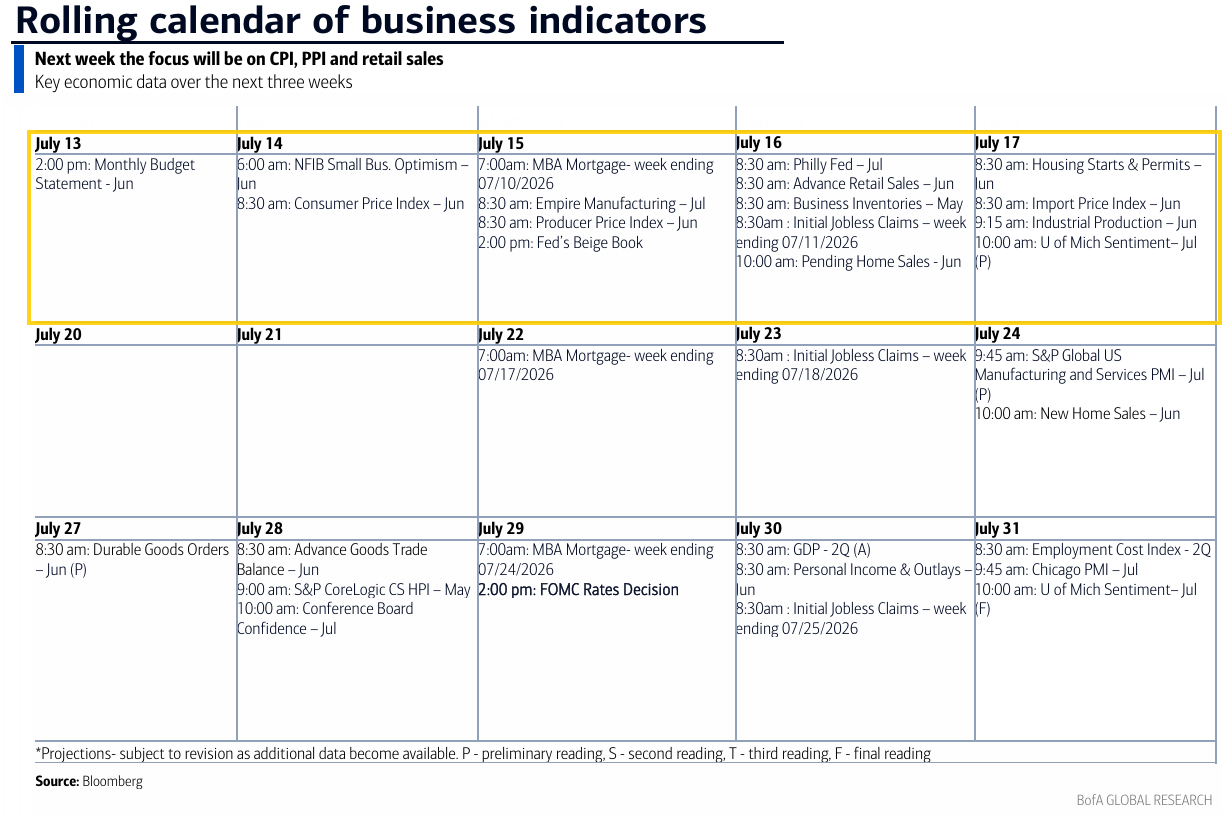

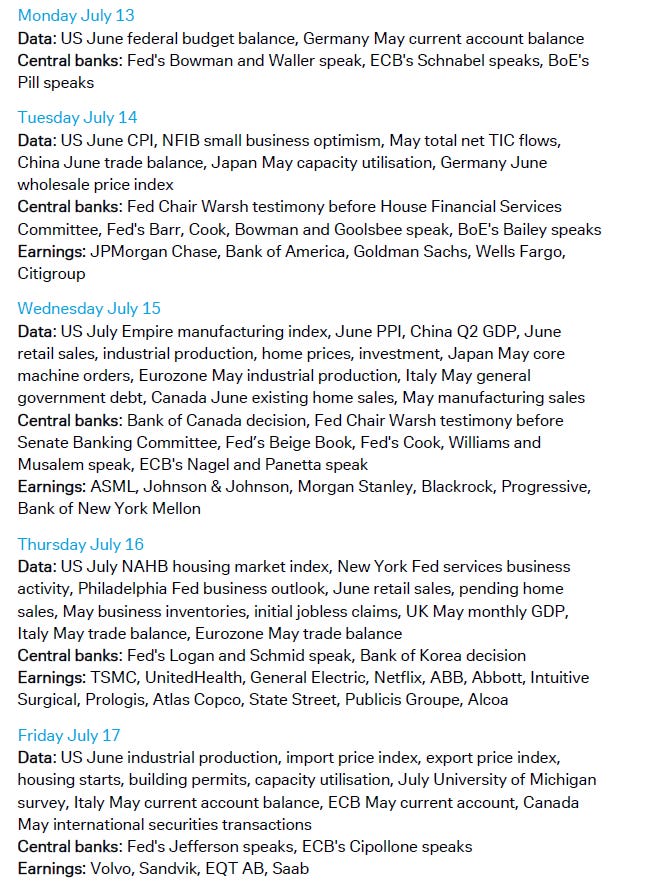

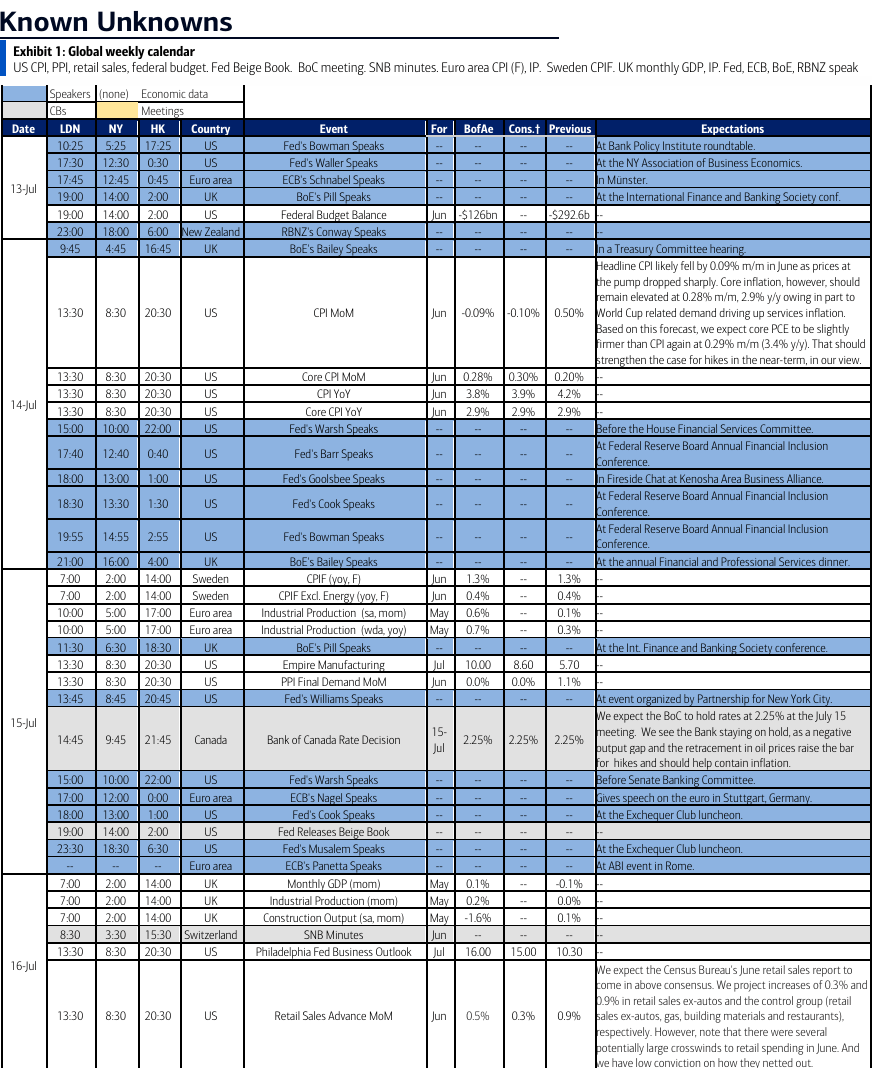

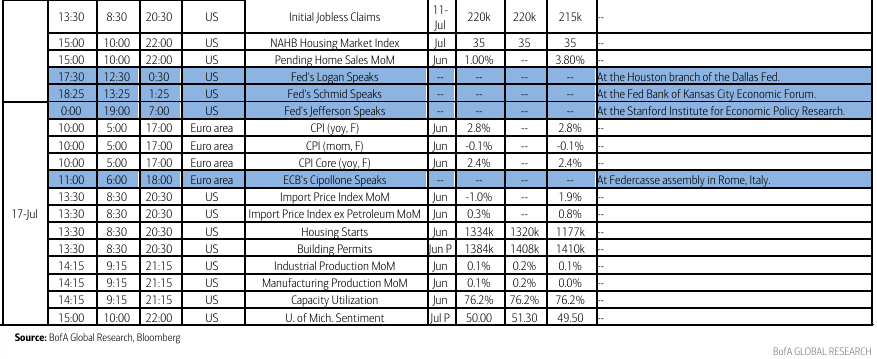

In US economic data we’ll get our key inflation reports in June CPI, PPI, and import prices that build the foundation for the PCE prices index that comes at the end of the month. But we’ll also get another market moving report in June retail sales. In addition, the busy week also includes June industrial production, pending home sales (contract signings), housing starts, and NFIB small business sentiment, July NAHB home builder index and UMich preliminary consumer sentiment, and the normal weekly reports (ADP, unemployment claims, etc.).

Fed speakers will also pick up highlighted by Kevin Warsh presenting the semi-annual Monetary Policy Report to Congress (House Financial Services Committee Tuesday, Senate Banking Committee Wednesday). But he’s certainly not the only one, as we’ll get Governors Waller, Bowman, Barr, Cook, and Jefferson and regional Fed presidents Williams, Goolsbee, Musalem, Schmid and Logan, and there will probably be more. Finally, on Wednesday we’ll get the Beige Book prepared for the July FOMC.

Non-Bill (>1 year) Treasury auctions at least are off for the week. That said, on Friday we’ll get the questions for the Treasury Borrowing Advisory Committee, which will inform us on what Treasury is considering for auction sizes in the upcoming quarter.

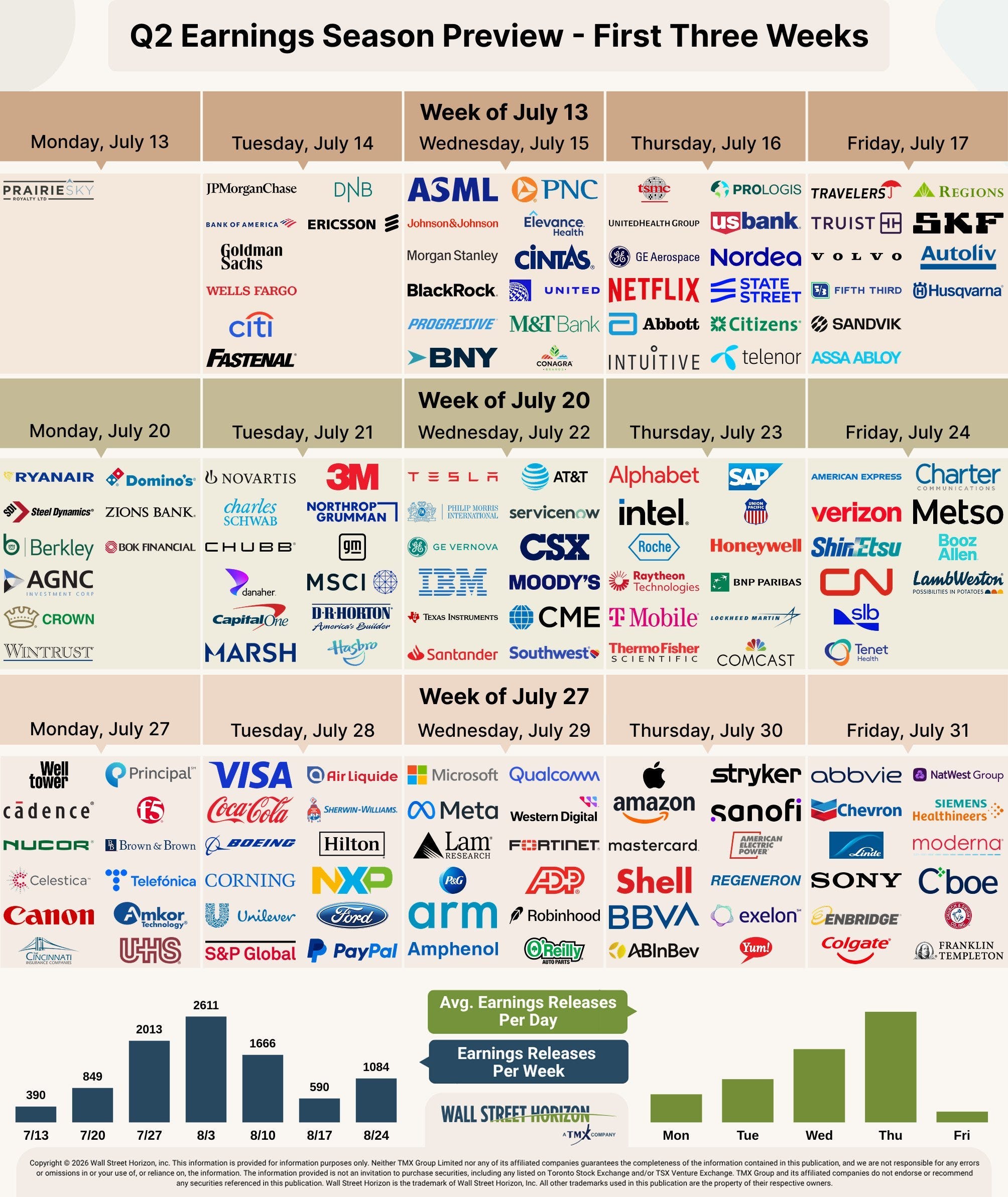

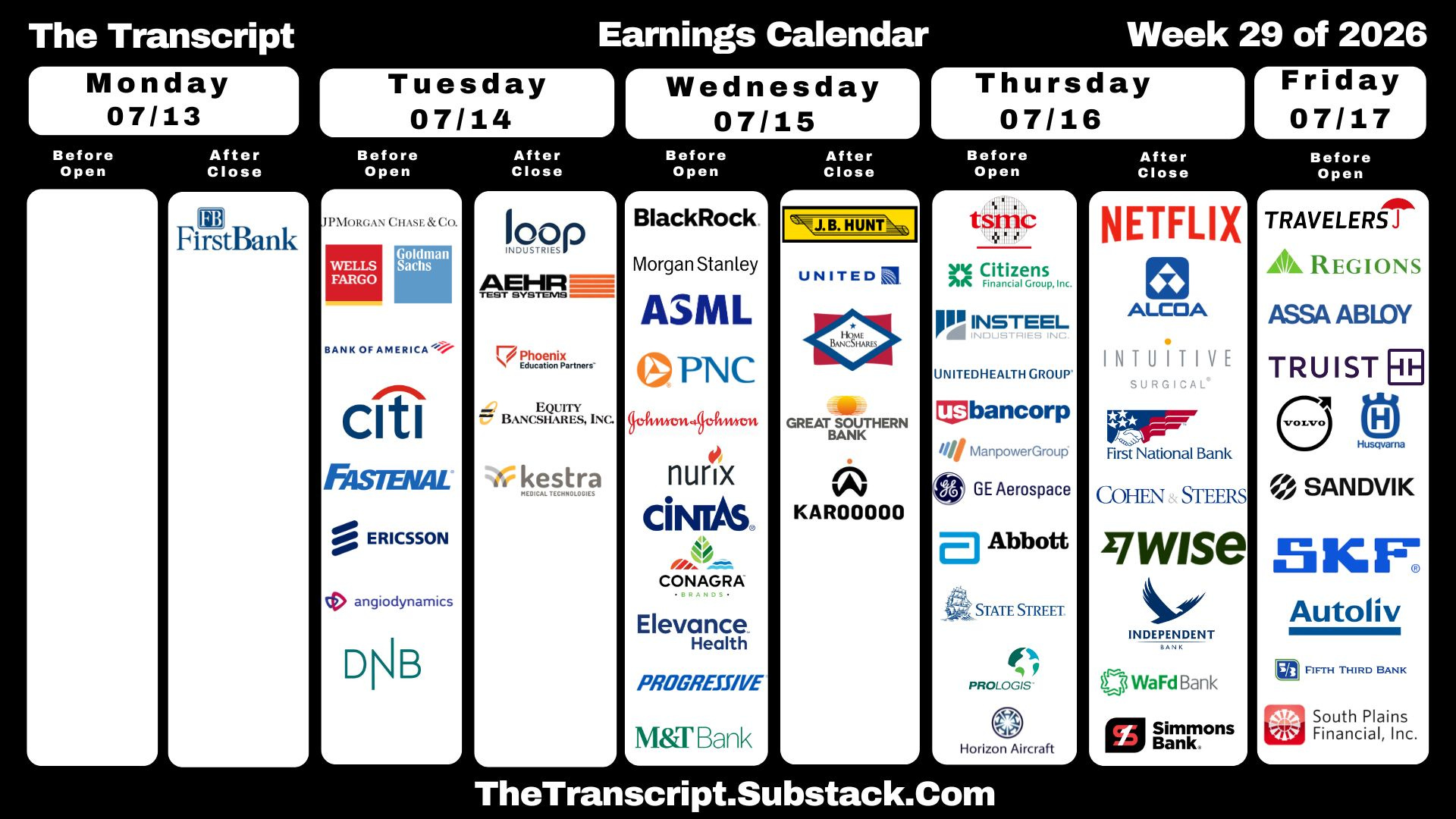

But earnings reports dial up considerably with the unofficial start of Q2 reporting season with the big banks (five of them) on Tuesday. In addition to those (WFC, C, BAC, JPM, GS) other >$100bn in market cap reporters next week include MS, PGR, JNJ, PNC, BLK, BK, UNH, ISRG, PLD, NFLX, GE, ABT. We’ll also get some non-US heavyweights next week including TSMC and ASML.

In terms of Iran, I said last week:

it appears we’ve settled into a détente, which is nominally for 60 days but looks likely to extend beyond that (President Trump has already hinted at such), probably through the mid-term elections as the parties work through the significant number of issues that need to be resolved.

There are two things, though, which I am watching which could see things escalate: One is Iran pushing things beyond the current state of play (such as demanding tolls at the end of the current 60-day period as they have indicated they will do), the second is some sort of kinetic conflict which escalates beyond the “tit-for-tat” back and forth that we’ve seen thus far in the ceasefire, always a possibility when you’ve got rockets and drones flying back and forth.

And we actually saw both of those “two things” come into play over the past week (Iran trying to discourage use of the Omani passage through the Strait and the kinetic conflict escalating) but neither has so far passed either side’s “red lines,” so while we remain closer to a return to full-out conflict, we are still within the now stretched bounds of talks continuing.

That said, things continue to move in the wrong direction this weekend with strikes and counterstrikes continuing, Iran declaring that the Strait is closed “until further notice,” while the US Central Command denied that, saying the waterway was still open to all vessels and the US military is prepared to ensure freedom of navigation. Earlier in the week President Trump had ordered a Saturday deadline for Iran to declare the Strait open or face more bombing. “We bombed the hell out of them last night,” Trump said. “They’re very, very evil and sick people.” The WSJ reports “The scale of Saturday’s attack was much larger than previous rounds over the past week and was aimed at sending a message that the US will hold Iran accountable for attacking commercial ships, military officials said.”

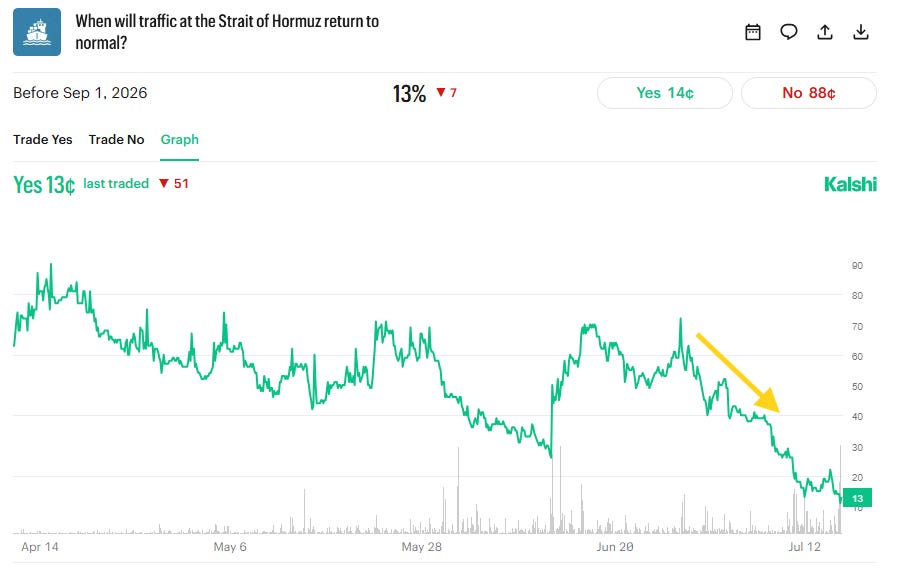

So as I said four weeks ago “we’ll just have to see how things progress”. While odds on Kalshi that traffic through the Strait would normalize by Sept 1st had risen as high as 69% June 25th, that has dropped to 13% today (half of last week), the least since the start of the contract (although also with the least amount of time remaining).

Ex-US highlights from DB:

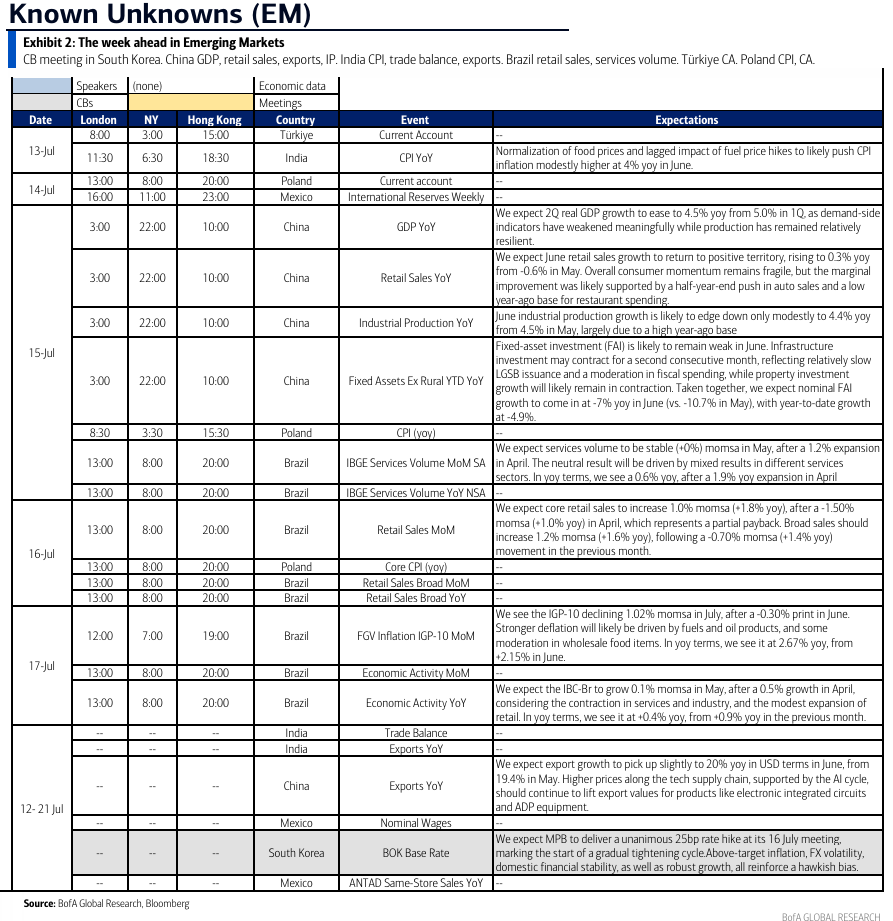

In addition to Chair Warsh’s semi-annual testimonies before the House Financial Services Committee on Tuesday and the Senate Banking Committee on Wednesday. other events to watch next week will be the Bank of Canada’s decision on Wednesday and the Bank of Korea’s decision on Thursday (DB forecast a +25bp hike). In Europe, ECB officials’ appearances scheduled for next week will be among the last communications before they go into the quiet period ahead of the decision the week after next.

Looking at notable economic data releases, there will be the May monthly GDP in the UK on Thursday as well as Q2 GDP and June activity data due Wednesday in China. The trade balance figures for the country are due Tuesday. For China, our economists forecast real GDP growth to slow to 4.4% in Q2 from 5% in Q1. For June economic data, they see industrial production growth improving to 4.8% YoY and June exports growth coming in at 17% YoY. Retail sales are expected to rebound to 0.2% YoY and investment is expected to remain soft at -4.0% Ytd YoY.

Here’s their one-pager:

BoA’s cheat sheets:

In this week’s Week Ahead:

An update on the continuing resilient economy, even if a bit less robust than a month ago, including the latest GDP trackers, the Dallas Fed Weekly Economic Index, Goldman’s Current Activity Indicator, BoA card spending, Redbook sales, consumer credit, housing, and thoughts from JPM’s Mike Feroli on the mid-year growth outlook.

A Q2 earnings season preview, including current earnings and revenue expectations, sector-level estimates, profit margins, earnings revisions, analyst price targets, the bar for Q2 beats, and thoughts from Yardeni and FactSet on forward earnings.

A closer look at the earnings setup beyond Q2, including expected contributions, 2026 and 2027 earnings expectations, and whether revisions are starting to cool from very strong levels.

An update on valuations, including how rising earnings expectations have affected forward P/Es for the Mag-7, large caps, mid caps, and small caps.

A breadth update, including the McClellan Summation Index, stocks above 20- and 200-DMAs, new highs minus new lows, equal-weight vs. cap-weight, small caps vs. large caps, and growth vs. value.

A detailed positioning and flows section, including Deutsche Bank’s composite positioning work, discretionary vs. systematic positioning, EPFR equity and bond fund flows, BoA’s systematic flow estimates, CTAs, vol-control funds, risk parity, and buybacks.

An update on leveraged ETF positioning, including the latest moves in SPX, Nasdaq-100, and single-stock leveraged ETF AUM.

A look at retail positioning and options activity, including BoA private client allocations, put/call ratios, Vanda retail options insights, and Barclays’ reminder on seasonal retail flow patterns.

An update on gamma from BofA and Tier1Alpha and volatility implications.

A sentiment check, including AAII, AAII asset allocation, NAAIM, Goldman’s sentiment indicator, CNN Fear & Greed, BoA’s Bull & Bear Indicator, and Helene Meisler’s weekend poll.

A seasonality update, including the second half of July, Jeff Hirsch’s Trump Presidency Seasonal Cycle, and July seasonal patterns.

A rates and Fed section, including rate hike and inflation expectations, Goldman’s view on the path of policy, BoA’s case for three hikes, and the setup for Chair Warsh’s testimony.

A wrap-up with some thoughts on the market backdrop moving forward including the shift from earnings expectations to earnings realization, some fading tailwinds, the AI trade, and whether the bull case remains intact.

Note: While I cannot post BoA charts on X, I include many in the Week Ahead.