The Week Ahead - 7/5/26

A look at the upcoming week for the US economy and equities — covering key drivers including earnings, positioning, breadth, valuations, sentiment, seasonality, and the Fed.

The Week Ahead

Note: A number of the usual reports were not published this week due to the holiday.

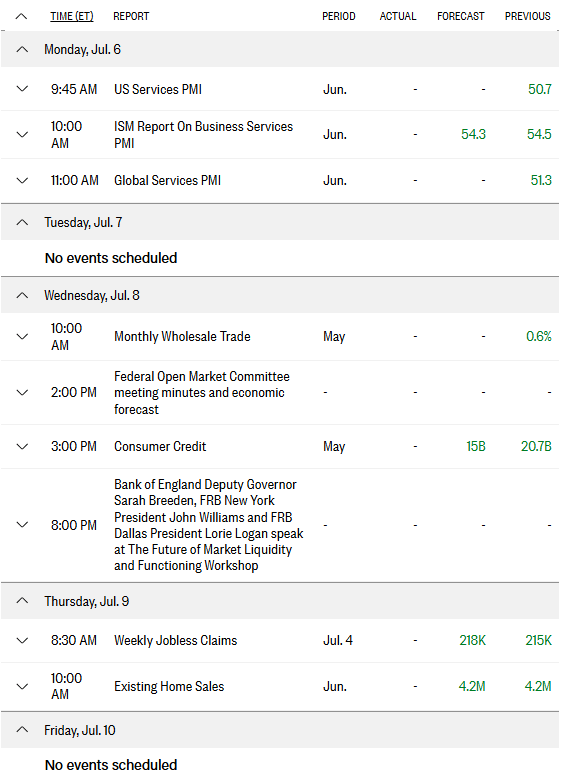

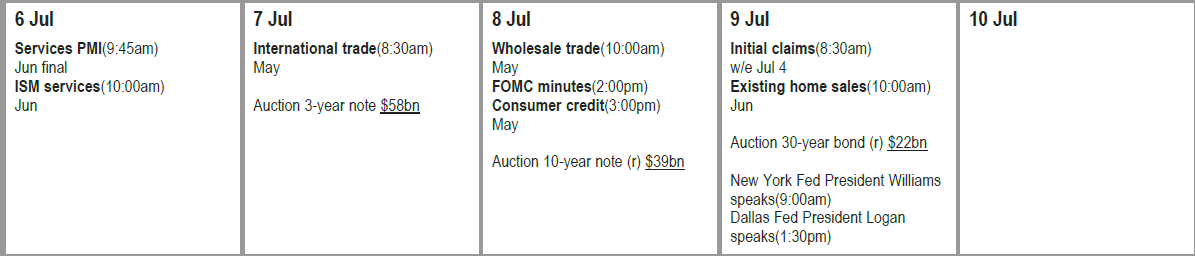

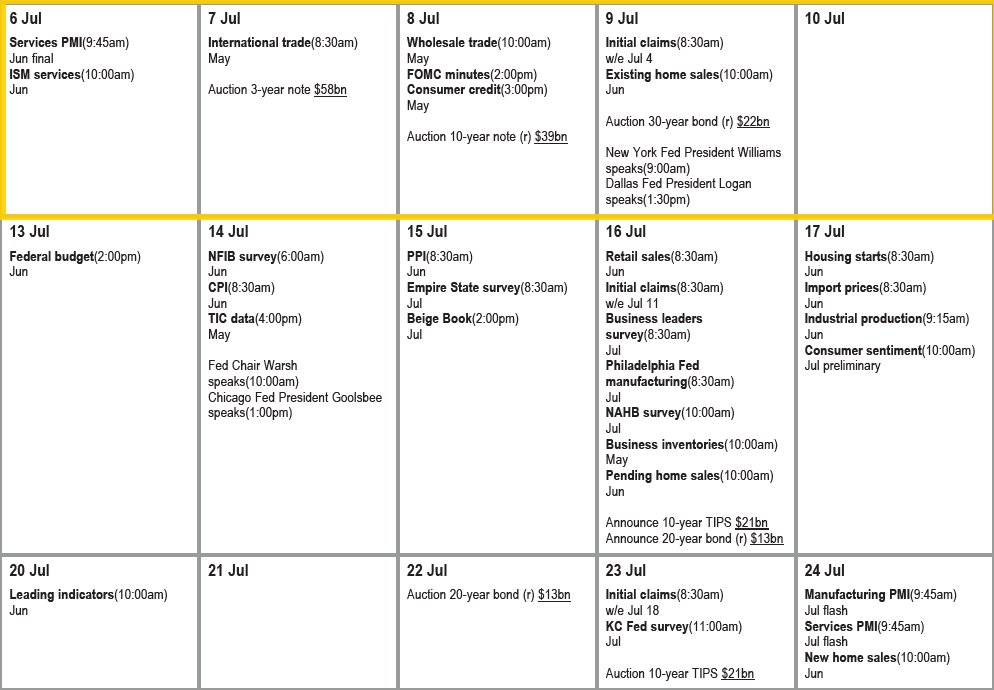

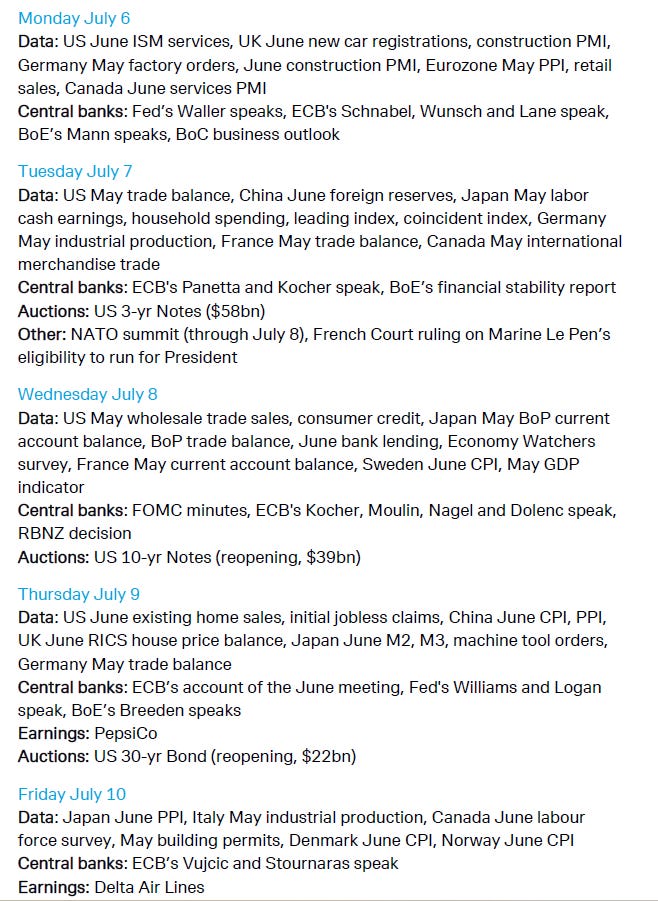

After a long holiday weekend, a very light week of US economic data in the upcoming week consisting of June final services PMIs, existing home sales, and NY Fed consumer expectations, May consumer credit and the normal weekly reports (ADP, jobless claims, etc.).

In terms of Fed speakers, as of now just Governor Waller on Monday and New York Fed President John Williams and Dallas President Lorie Logan at an event Wednesday are on the calendar. More importantly, we’ll get the minutes from the June FOMC. We’ll see how much they’re changed by the new “no forward guidance” mandate.

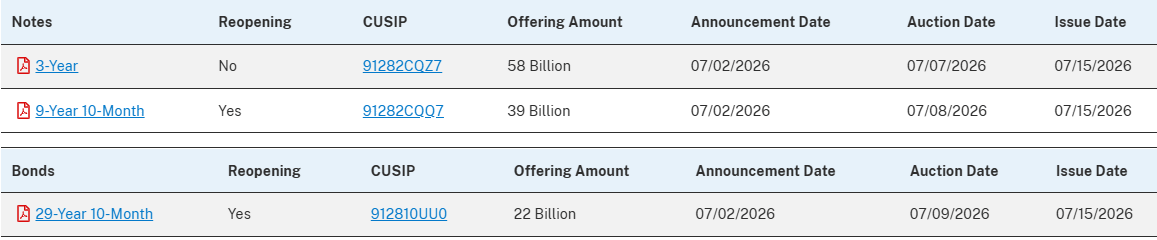

Non-Bill (>1 year) Treasury auctions will resume with 3, 10, and 30 year durations (the latter two reopenings).

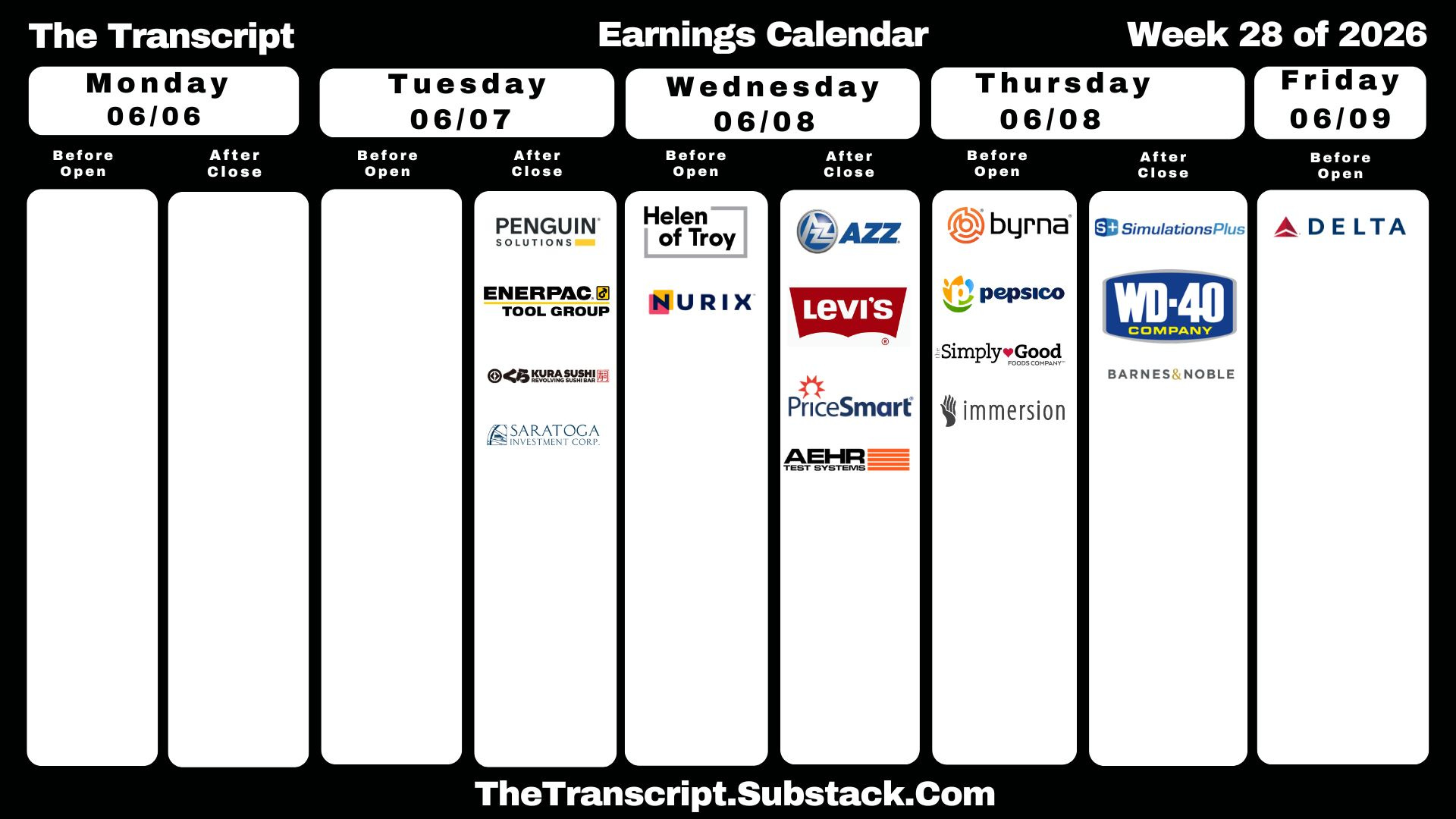

In terms of earnings just two SPX components (PEP, DAL) reporting in our last week before things start to pick up with the unofficial start to Q2 earnings season.

In terms of Iran, it appears we’ve settled into a détente, which is nominally for 60 days but looks likely to extend beyond that (President Trump has already hinted at such), probably through the mid-term elections as the parties work through the significant number of issues that need to be resolved.

There are two things, though, which I am watching which could see things escalate: One is Iran pushing things beyond the current state of play (such as demanding tolls at the end of the current 60-day period as they have indicated they will do), the second is some sort of kinetic conflict which escalates beyond the “tit-for-tat” back and forth that we’ve seen thus far in the ceasefire, always a possibility when you’ve got rockets and drones flying back and forth.

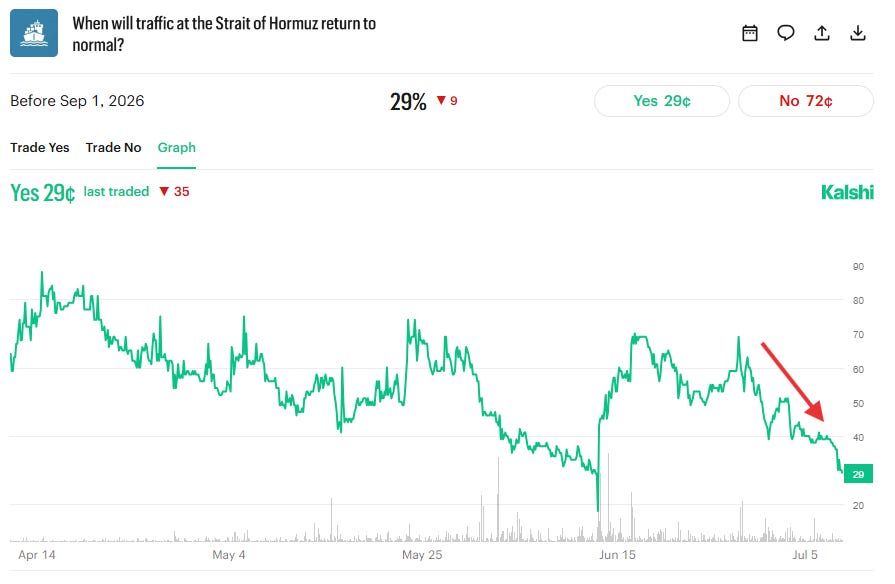

So as I said three weeks ago “we’ll just have to see how things progress”. While odds on Kalshi that traffic through the Strait would normalize by Sept 1st had risen as high as 69% June 25th, that has dropped to 29% today.

Ex-US highlights from DB:

In Europe, highlights include the ECB’s account of its June meeting (Thursday), the BoE’s financial stability report (Tuesday) as well as May activity indicators in Germany including factory orders (Monday), industrial production (Tuesday) and the trade balance (Thursday). There will also be inflation prints due from Sweden on Wednesday and Denmark and Norway on Friday.

Investors will also pay attention to French politics as an appeals court will rule on Marine Le Pen’s eligibility to run for President on July 7.

Over in Asia, the focus in China will be on June inflation, with CPI and PPI due Thursday. In Japan, key releases include labour cash earnings and household spending on Tuesday, the Economy Watchers survey on Wednesday and PPI on Friday.

Rounding out notable events for the week ahead, geopolitical highlights will include the NATO summit (Tuesday through Wednesday) in Türkiye. Elsewhere, there will be a rates decision in New Zealand (Wednesday) and June’s labour market data in Canada (Friday). For the former, our economists look for a 25bp hike, taking the OCR to 2.5%.

Here’s their one-pager:

In this week’s Week Ahead:

How the economy continues to remain resilient although perhaps seeing some softening, including last week’s Employment Situation report, the latest GDP trackers, the Dallas Fed Weekly Economic Index, Goldman’s Current Activity Indicator, accelerating BoA card spending, Redbook sales, World Cup spending, improving lower-income spending, and firmer CFO sentiment.

How earnings expectations keep powering higher, with Q2 and 2026 estimates continuing to move up, unusually rising during the quarter, earnings revisions remaining the strongest ten-week stretch since 2021, and analysts continuing to lift bottom-up S&P 500 price targets.

Why the earnings story is powerful but also increasingly demanding, including the high bar heading into Q2 earnings season, Tech and Energy expected to drive another very strong quarter, unusually positive Tech guidance, and continued concerns that AI-related earnings expectations and semiconductor margin assumptions may be getting ahead of themselves.

The improvement in breadth, including the McClellan Summation Index, stocks above key moving averages, new highs minus new lows, the equal-weight S&P 500 making a new high, small caps improving relative to large caps, and growth/value easing off its recent extremes.

A detailed look at positioning and flows with a mixed near-term setup from BofA, Tier1Alpha, Citadel, and others covering systematic exposure, CTAs, vol-control demand, leveraged ETFs, retail activity, put/call ratios, buybacks, and gamma.

The notable changes in leveraged ETF positioning last week, particularly around memory stocks, semis, and the potential for forced flows to amplify moves in either direction.

A full sentiment check, including AAII, NAAIM, Goldman’s sentiment indicator, CNN Fear & Greed, BoA’s Bull & Bear Indicator, Helene Meisler’s weekend poll, and Yardeni’s broader bull/bear work.

A look at seasonality, including how the second half tends to perform after a strong first half and midterm-year second half volatility.

A look at the Fed and rates, including inflation expectations, Fed funds pricing, the recent firming in rates, curve steepening, low bond volatility, and what to watch in the upcoming Fed minutes under Chair Warsh’s new “no forward guidance” approach.

Note: While I cannot post BoA charts on X, I include many in the Week Ahead.