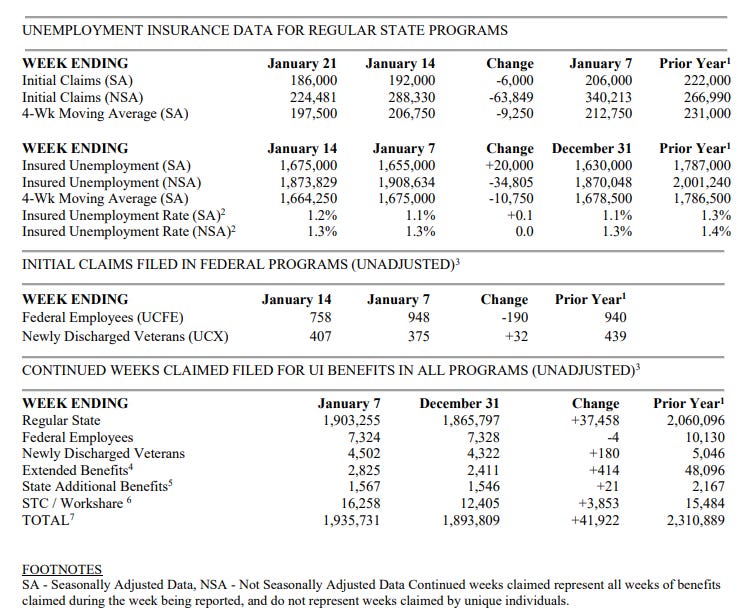

US Initial Jobless Claims Jan 21: 186K (est 205K; prev 190K)

US Initial Jobless Claims Jan 21: 186K (est 205K; prev 190K)

Initial jobless claims fall to lowest since last April. Continuing claims edge higher but below recent peak in December.

US Initial Jobless Claims Jan 21: 186K (est 205K; prev 190K)

US Continuing Claims Jan 14: 1675K (est 1658K; prev 1647K)

Jobless claims are one of the most high frequency indicators we have on the labor market, and in the week through Jan 21st seasonally adjusted initial claims continued their recent decline falling to 186k from 192k the prior week (revised from 190k) now the lowest since last April. Estimates were for 205k. This pushes them even further below the the 255-265k range they were trading at last summer, and keeps them below year ago levels (222k) as well. They are also nears the lows before the pandemic.

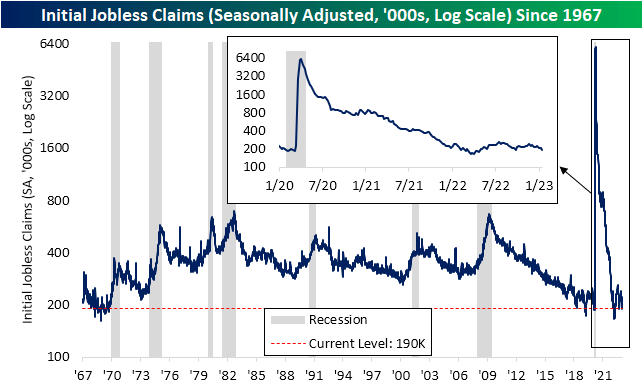

Here’s a longer run chart from Bespoke from last week on initial claims to give some context.

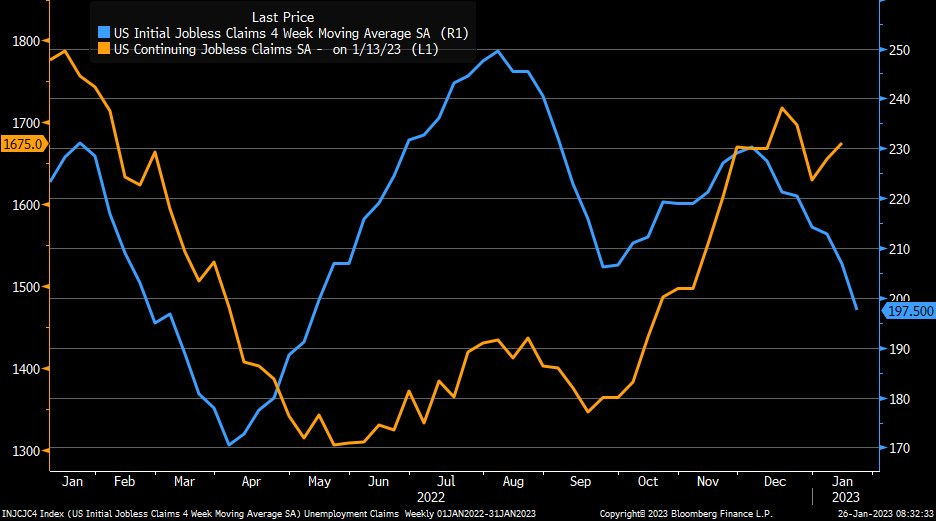

The 4-week moving average of initial claims moved lower to 198k, down from 231k a year ago. That is the lowest since May.

Seasonal adjustments, which many have blamed for the low claims, played a large role for a fourth week as unadjusted initial claims fell by -64k to 224k. So seasonals expected a decrease of -58k. We should be getting through some of the seasonal issues though as the gap between adjusted and unadjusted claims has shrunk to 38k from 94k the prior week and 134k the week before that. Unadjusted claims are -43k below year-ago levels.

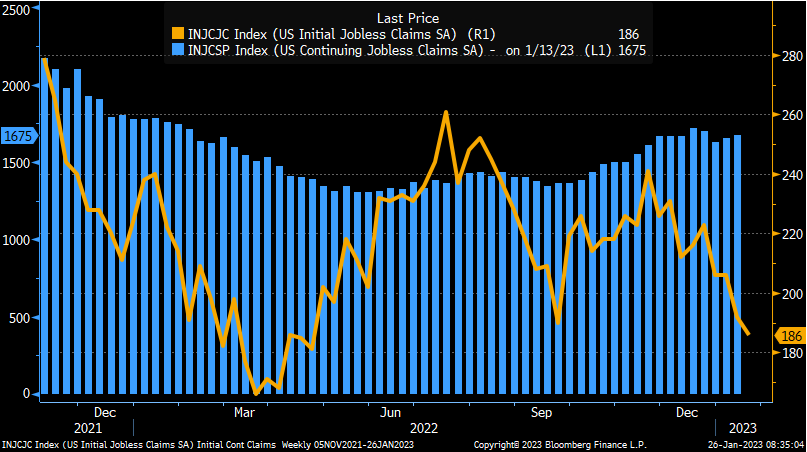

As you know if you’ve been reading these weekly, unlike initial claims, adjusted continuing claims, which are one week delayed (so from Jan 14th), didn’t move higher with initial claims when they were both at 50 year lows in the first half of 2022, but 17 weeks ago they started to finally move higher. After falling back for a couple of weeks four weeks ago by a total of -87k, in the following week they got back +17k of that, and in the reference week another +20k, moving to 1.68M. These remain, though, down -110k from last year (1.79M). The read was slightly above estimates for 1.66M, but remains below the recent peak.

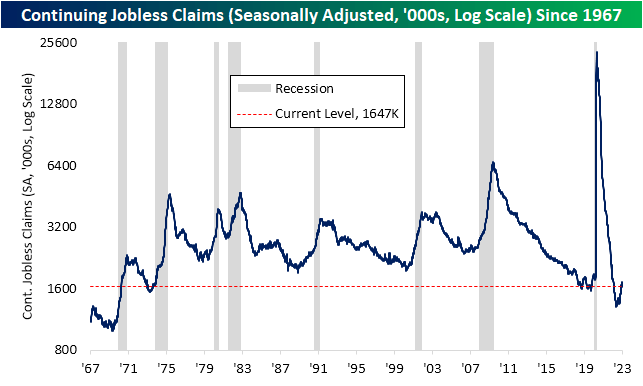

The fact that continuing claims have been moving higher while initial claims are moving lower has been taken as evidence that while companies are reluctant to fire people, they are also reluctant to hire them, so more are ending up in continuing claims. Here’s a longer run chart of continuing claims also from last week.

Seasonals played a role here as well, with non-adjusted continuing claims falling by -35k to 1.87M. So seasonals had expected a decrease of -55k. Unlike initial claims there remains a very sizeable gap (190k) between adjusted and non-adjusted continuing claims, but perhaps these will converge as we’ve seen with initial claims given continuing claims are a week behind. As with initial claims, non-adjusted continuing claims are down y/y (by around 130k).

The 4-week moving average of continuing claims fell slightly to 1.66M. It was 1.79M a year ago. They are right around pre-pandemic levels.

Total receiving benefits, which is two weeks delayed (so from Jan 7t), moved higher for a third week, increasing by 42k to 1.94M, the highest since early in 2022, although also extremely low historically (and these should basically track continuing claims at this point). To give some context, these were 2.3M a year ago.

So after a steady march higher in June into July, initial claims flatlined for a month then started drifting lower. I had said since then I thought we hit a bottom 17 weeks ago (last September), but that appears to have been incorrect (as we’re now below those levels). So initial clams are clearly not ready to move appreciably higher. More established has been the move higher in continuing claims. These remained near record lows even when initial claims moved up in 2022 as people were quickly rehired. It seems that is not happening as quickly now. I said the last two weeks

I wouldn’t make too much out of the recent declines after 13 weeks of overall gains given the big seasonal adjustments. I’d imagine we’ll see this at least stabilize if not move higher. Overall, it still signals to me the same slowdown in the jobs market that other reports are indicating, but does not yet signal a recession.

That seems to have been correct at least for now.

To subscribe to these summaries, click below.

To invite others to check it out,

To see more content, including summaries of most major U.S. economic reports and my morning and nightly updates go to Neil’s Newsletter Substack for newer posts or https://sethiassociates.blogspot.com for the full history. You can also follow me on Twitter at @NeilKSethi