An update to the below. This was released February 1st.

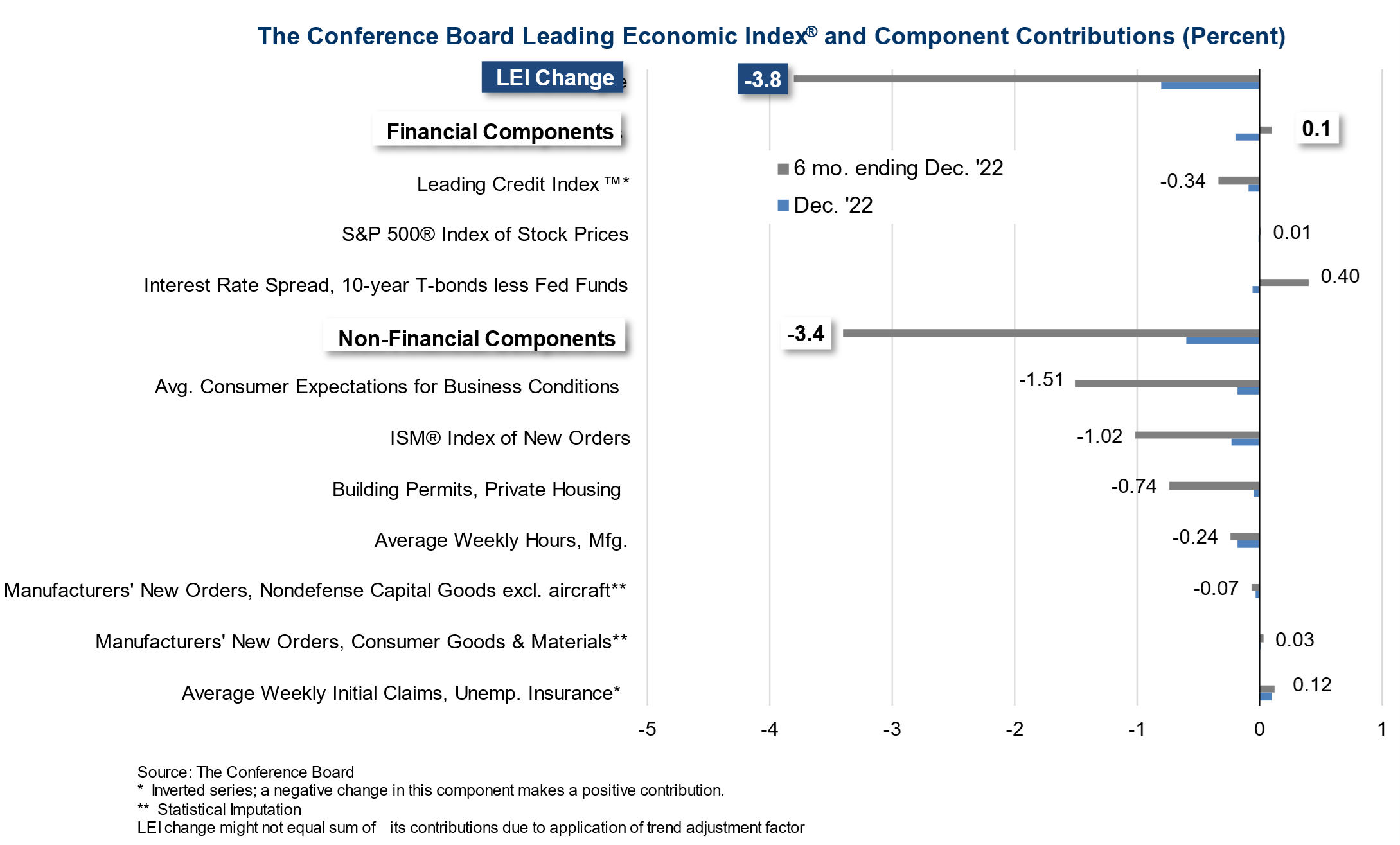

The Conference Board Leading Economic Index® (LEI) for the U.S. decreased by 0.8 percent in December 2022 to 110.7 (2016=100), following a decline of 0.8 percent in November. The LEI is now down 3.8 percent over the six-month period between June and December 2022—a much steeper rate of decline than its 2.3 percent contraction over the previous six-month period (December 2021–June 2022).

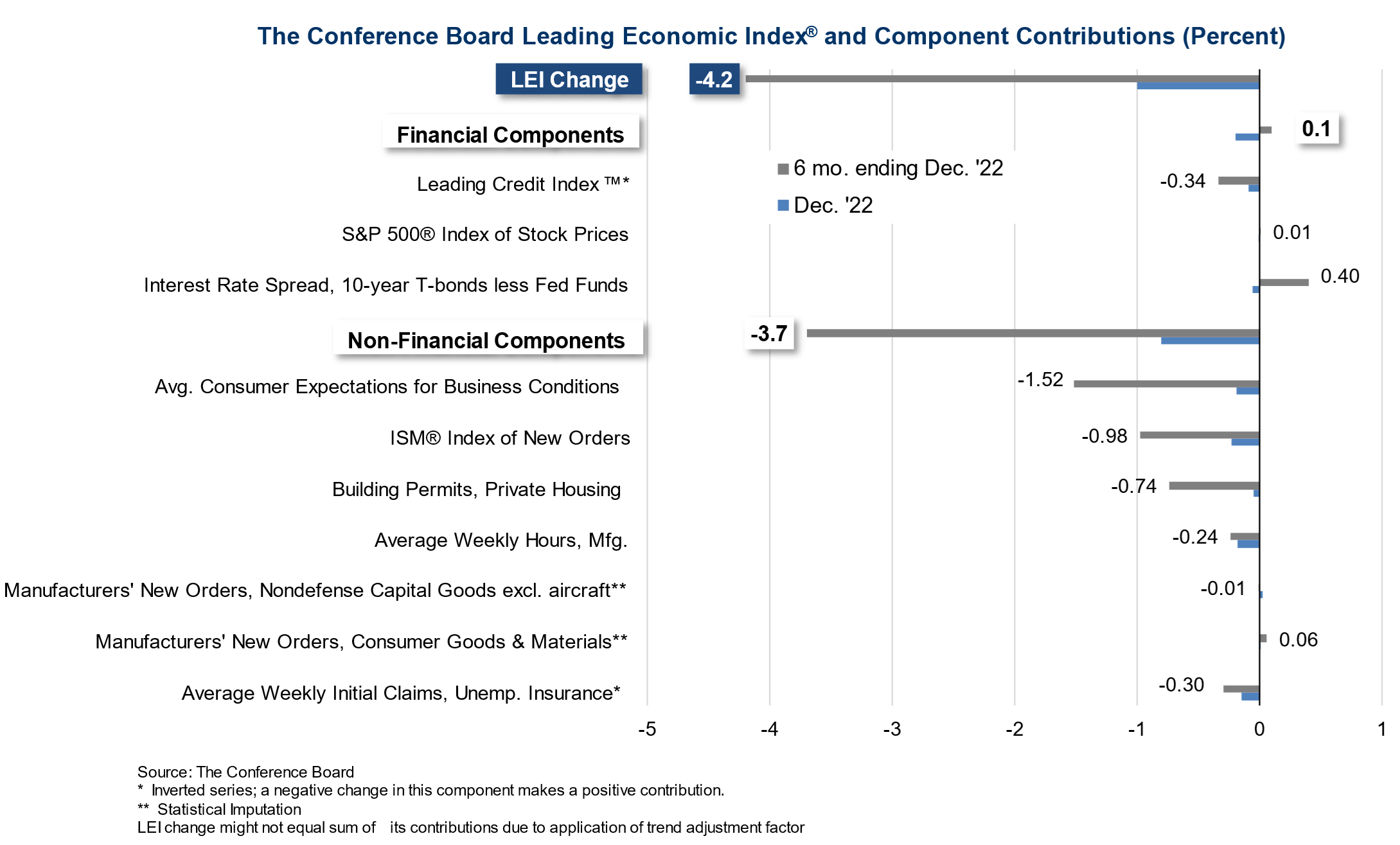

US Leading Economic Index (M/M) Dec: -1.0% (est -0.7%; prev R -1.1%)

The Conference Board’s Leading Economic Index capped 2022 with a tenth consecutive monthly decline in December (following a year in 2021 of nothing but increases which took it to an all-time high). As with November (-1.1%, revised down from -1.0%), December saw a larger decline that most of the year at -1.0%, so the pace of declines has accelerated. The drop was more than estimates for a -0.7% decline. The LEI is now down -6.0% from the highs (and -4.2% over just the last 6 months), firmly into the recession “danger zone”. As has been the case for most of 2022 the non-financial inputs (consumer expectations, ISM new orders, etc.) were responsible for the declines (financial inputs (credit, stock prices, and rate spreads) actually increased in December). The report made a recession its base case four months ago and continued to suggest one this month (emphasis is mine):

“The US LEI fell sharply again in December—continuing to signal recession for the US economy in the near term,” said Ataman Ozyildirim, Senior Director, Economics, at The Conference Board. “There was widespread weakness among leading indicators in December, indicating deteriorating conditions for labor markets, manufacturing, housing construction, and financial markets in the months ahead. Meanwhile, the coincident economic index (CEI) has not weakened in the same fashion as the LEI because labor market related indicators (employment and personal income) remain robust. Nonetheless, industrial production— also a component of the CEI—fell for the third straight month. Overall economic activity is likely to turn negative in the coming quarters before picking up again in the final quarter of 2023.”

As I said three months ago,

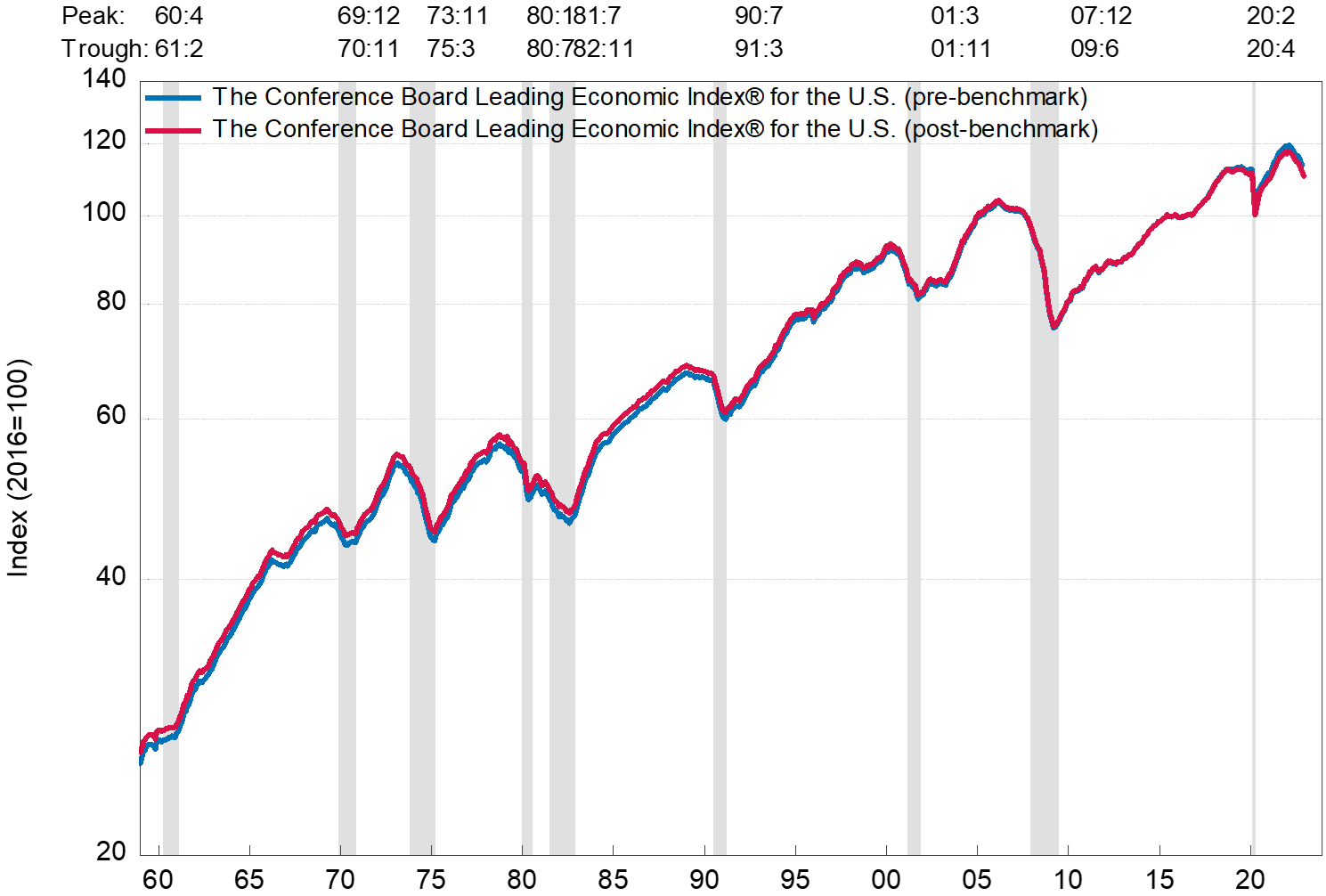

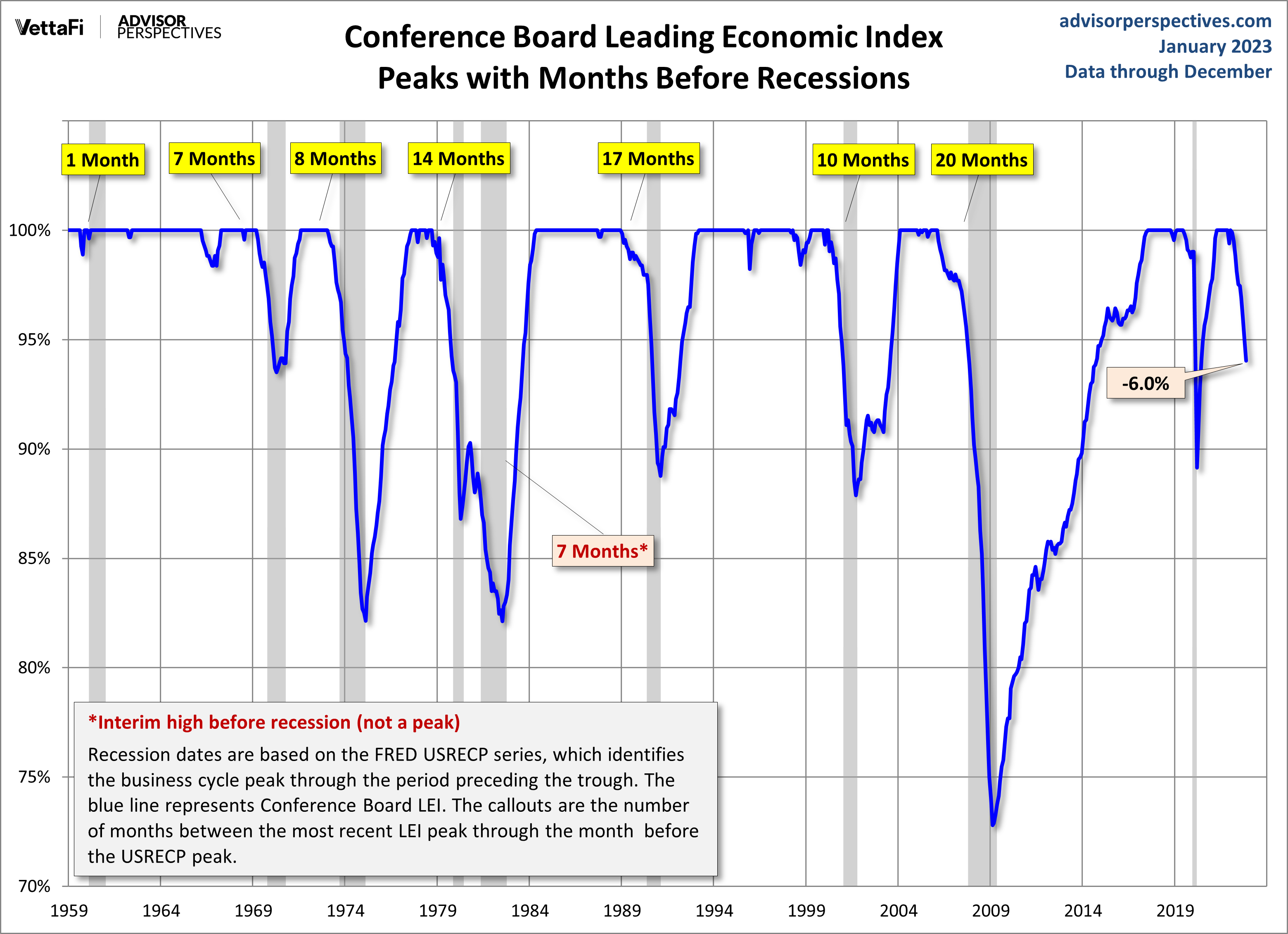

My take since early 2022 has been the decline in this indicator should be no surprise, and just evidences the slowing economy that the Fed is actively looking for. Whether this turns into a recession remains to be seen, but there’s no doubt that things are softening enough to show up in just about every economic indicator outside of employment. I do have to caveat that, though, as there are some bright spots such as business spending that have been holding up better than expected (and many others such as consumer spending have not collapsed by any stretch of the imagination). Also, notably a good portion of the decline is due just to consumer expectations, which I don’t think are a great leading indicator. But nevertheless, I have to acknowledge that it is unprecedented to have this level of decline in the LEI’s without being in or near a recession. As a reminder, LEI's generally peak 6-18 months before a recession (see chart below from Advisor Perspectives), and while a fall from the peak does not mean a recession (lots of false positives), when we get to around 3.5+% under the highs it has always resulted in one in the past.

This month I have to caveat the caveat, as the last two months business spending has been weak, which has been one of the pillars of my more optimistic outlook on the economy. In addition, ISM new orders have fallen sharply from last month. That has a pretty good track record as a leading indicator. I still remain unconvinced a recession is coming, but the evidence does continue to grow.

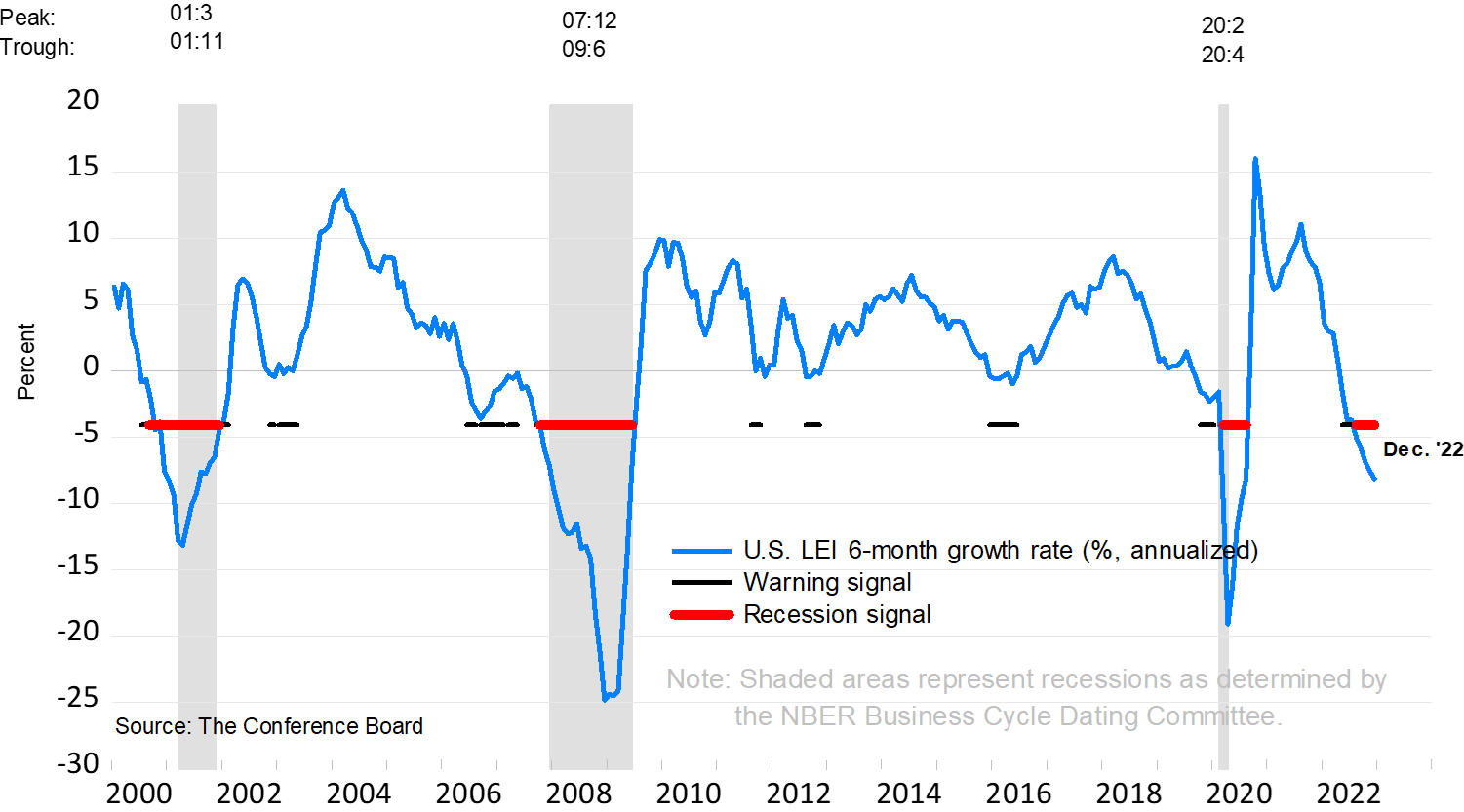

And looking at it as % growth rate shows a similar story.

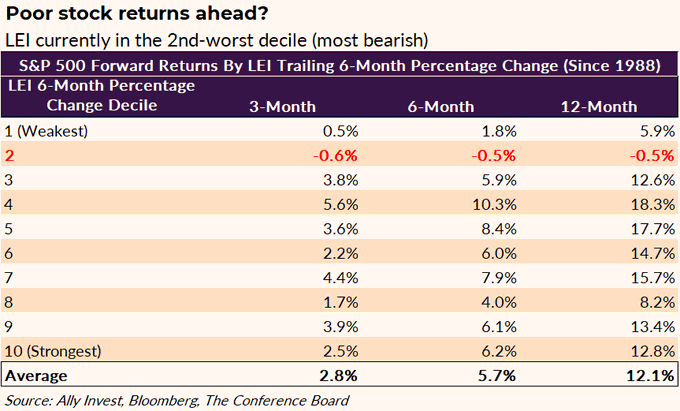

And here’s how stocks have returned based on LEI deciles. This is from before this most recent release so we’re conceivably in the 1st decile now.

As a reminder, here are the components of the LEI (it does have a bit of a manufacturing tilt):

To see more content, including summaries of most major U.S. economic reports and my morning and nightly updates go to Neil’s Newsletter Substack. You can also follow me on Twitter @NeilKSethi.