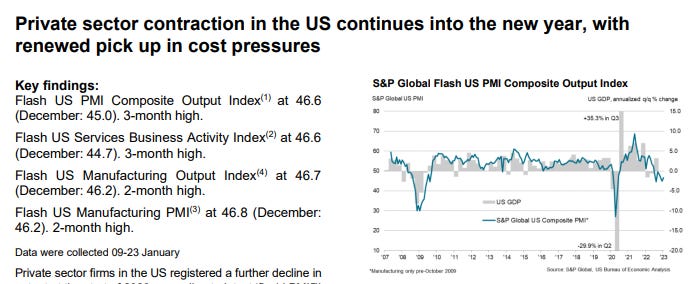

US S&P Global Composite PMI Jan P: 46.6 (est 44.7; prev 45.0)

Flash US Jan PMIs improve but remain solidly in contraction territory as input prices reaccelerate.

US S&P Global Composite PMI Jan P: 46.6 (est 44.7; prev 45.0)

-Manufacturing PMI: 46.8 (est 46.0; prev 46.2)

- Services PMI: 46.6 (est 45.0; prev 44.7)

(spglobal.com)

The January S&P Global (previously IHS Markit) Composite flash PMI report improved for the second time in the past ten months to a 3-month high “as manufacturers and service providers signaled moderations in their respective downturns.” Coming in at 46.6 (below the 50 dividing line between expansion and contraction), up from December’s final read of 45.0, the result was above estimates for a small decline to 44.7.

The contraction in activity was solid overall, but the slowest since last October. Goods producers and service providers recorded similar rates of decline, with service sector firms indicating a notable slowdown in the pace of decrease since December. Nonetheless, companies continued to highlight subdued customer demand and the impact of high inflation on client spending

As noted above, the improvement was more heavy on the services side which improved almost two points to 46.6 from 44.7 in December. Manufacturing improved to 46.8 from 46.2 in December. It was the seventh consecutive month below 50 for the services sector and the third for manufacturing.

New orders, which had vacillated around the 50 line for the previous four months to November remained below for a third month, although improved to the highest since falling below 50 after the largest decline since May 2020 in December.

Pressure on purchasing power among customers and company balance sheets led to a strong decline in new orders, and one that was the fastest since May 2020. Weak demand conditions were broad-based, though manufacturing firms saw a steeper decrease in new orders compared to their service sector counterparts.

New export orders, which have been much weaker than overall new orders, continued to be so in January, contracting for an eighth straight month, although the rate of decline softened for a second month.

Input costs were a negative, reaccelerating after seven months of moderation after decelerating at the fastest rate in 13 years outside of April 2020 in December. Services led here as well. Notably the report mentioned wages which I’m sure conjures “wage-price spiral” visions in the head of Fed members.

Although well below the average rise seen over the prior two years, the rate of cost inflation quickened from December and was historically elevated. Hikes in vendor prices, alongside higher wage bills, reportedly spurred the sharper rise in costs.

Selling prices also increased but at a “stable” pace and at the slowest since October 2020, perhaps indicating margin pressures.

the rate of output charge inflation at private sector firms was unchanged from that seen in December 2022. January data signaled a solid uptick in selling prices, but one that was the joint-slowest since October 2020. Efforts to remain competitive and offer concessions to customers dampened output price hikes.

Employment which softened notably in October remained “subdued” for a fourth month in January with services just over and manufacturing just under the 50 level.

US firms recorded a marginal rise in employment at the start of 2023. The rate of job creation was one of the softest in the current sequence of employment growth that began in July 2020. The upturn in workforce numbers was driven by service providers, as manufacturers registered a fractional contraction in staffing levels. Firms continued to mention efforts to build employee numbers, especially in roles with long-held vacancies.

…

Jobs growth has … cooled, with January seeing a far weaker increase in payroll numbers than evident throughout much of last year, reflecting a hesitancy to expand capacity in the face of uncertain trading conditions in the months ahead.

And despite the lesser decline in new orders, backlogs remained in contraction for a fourth month in January at a “solid” pace.

And business confidence improved but remained below the series average.

business confidence strengthened at the start of the year. Despite still being below the historic series trend, the degree of optimism was the highest for four months. The pick-up in positive sentiment was broad-based, with companies hopeful of a resurgence in customer demand as 2023 progresses.

So after dropping back to post-pandemic lows in December, we got a bounce in January, although in part it was due to higher prices which is the wrong kind of “improvement”. It did not feed through into selling prices yet, so that’s a positive at least as far as the Fed is concerned. But the increase in costs comes despite, as the report noted, a business activity decline “among the steepest seen since the global financial crisis, reflecting falling activity across both manufacturing and services” which also included a continued moderation in employment. So while the index showed overall improvement, it’s hard to avoid the stagflationary vibe of the report this month. As Chris Williamson notes below,

The worry is that, not only has the survey indicated a downturn in economic activity at the start of the year, but the rate of input cost inflation has accelerated into the new year, linked in part to upward wage pressures, which could encourage a further aggressive tightening of Fed policy despite rising recession risks.

Here was the full commentary:

Commenting on the US flash PMI data, Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said:

“The US economy has started 2023 on a disappointingly soft note, with business activity contracting sharply again in January. Although moderating compared to December, the rate of decline is among the steepest seen since the global financial crisis, reflecting falling activity across both manufacturing and services.

“Jobs growth has also cooled, with January seeing a far weaker increase in payroll numbers than evident throughout much of last year, reflecting a hesitancy to expand capacity in the face of uncertain trading conditions in the months ahead. Although the survey saw a moderation in the rate of order book losses and an encouraging upturn in business sentiment, the overall level of confidence remains subdued by historical standards. Companies cite concerns over the ongoing impact of high prices and rising interest rates, as well as lingering worries over supply and labor shortages.

“The worry is that, not only has the survey indicated a downturn in economic activity at the start of the year, but the rate of input cost inflation has accelerated into the new year, linked in part to upward wage pressures, which could encourage a further aggressive tightening of Fed policy despite rising recession risks.”

To subscribe to these summaries, click below.

To invite others to check it out,

To see more content, including summaries of most major U.S. economic reports and my morning and nightly updates go to Neil’s Newsletter Substack for newer posts or https://sethiassociates.blogspot.com for the full history. You can also follow me on Twitter @NeilKSethi