Markets Update - 3/16/26

Update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with charts!

To subscribe to these summaries, click below!

To invite others to check it out (sharing is caring!), here’s the button:

Link to posts on X - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog.

Also, if you see an error (a chart or text wasn’t updated, etc.), always appreciate a note in the comments section or email so I can fix it.

In that regard note I do make mistakes sometimes, and usually I catch them at some point and correct them, and/or I sometimes add new material, so it’s always safest to read from the website where it will have any updates.

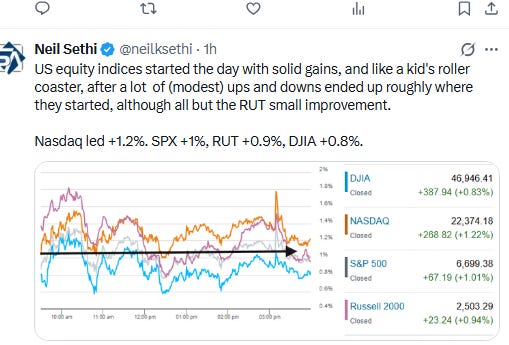

US equity indices opened trading for the week seeing a solid rebound as oil prices and Treasury yields eased off after Treasury Sec Bessent confirmed that the US is allowing Iran tankers to transit “to supply the rest of the world,” there were confirmed reports of some (limited) countries getting tankers through after negotiations with Iran, Pres Trump said talks with Iran were ongoing (Iran for their part said no talks are taking place) and the WSJ reported that the US will announce soon a coalition of countries to escort ships through the Strait (although publicly commitments from other countries have been tepid, and Pres Trump later talked down the immediacy of the project).

Market internals had also reached extremes as discussed in the Week Ahead that made the potential for such a bounce more probable. While indices weren’t able to build much further, they at least maintained those gains led by the Nasdaq on the back of megacap outperformance (Mag-7 index was +1.5% vs S&P 500 equal-weight which was +0.7%), but the gains were broad with two-thirds of stocks advancing on the day.

Elsewhere, bond yields as noted eased back as did the dollar. Crude, gold, and natural gas also finished lower while bitcoin and copper were higher (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was +1.0%, the equal weighted S&P 500 index (SPXEW) +0.7%, Nasdaq Composite +1.2% (and the top 100 Nasdaq stocks (NDX) +1.1%), the SOXX semiconductor index +2.0%, and the Russell 2000 (RUT) +0.9%.

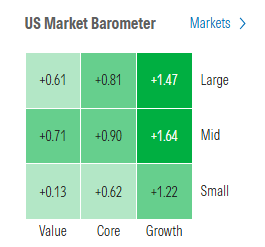

Morningstar style box shows every style in the green led by growth.

Market commentary:

“The conflict in the Middle East and related headlines are still the major source of fluctuations in markets,” said Sameer Samana, head of global equities and real assets at Wells Fargo Investment Institute. “The duration of the closure in the Strait of Hormuz is the key factor and markets will be watching for progress.” Still, Samana believes that investors should be optimistic, focusing instead on the prospect of solid economic growth and corporate earnings in the future. He anticipates that WTI will eventually head back down to $65 to $75 a barrel. “We would continue to try and look through those near-term headlines, as we still see the conflict/closure as lasting weeks/months and not changing the forward outlook meaningfully,” he said.

“While it’s possible for oil prices to exceed $100 in the near-term, we don’t expect prices to remain above this threshold for the long-term,” said Richard Saperstein at Treasury Partners. “Oil prices will decline as tensions subside and oil flows return to pre-crisis levels.”

“The market is trying to stabilize, but it is not one that has turned optimistic,” said Charu Chanana, chief investment strategist at Saxo Markets. “Equities may welcome any sign that Hormuz could be reopened, but with further strikes still being threatened and diplomacy still patchy, conviction is low and positioning is likely to stay very twitchy.”

“The market really feels that Trump has the market’s interest, I think, in his mind long term,” said David Krakauer, vice president of portfolio management at Mercer Advisors. To be more specific, it “still is somewhat relying on thinking that he can end this if he really wants to if things start to get bad.”

The stock sell-off has been relatively tame despite the geopolitical tensions. In fact, the S&P 500 remains just more than 4% below its all-time high set earlier this year. “There is uncertainty. Things change quickly,” Krakauer said to CNBC. “In the fog of war, you sort of just stay put.”

“While markets may experience some relief if the situation in the Middle East doesn’t notably deteriorate, any rebound in stocks risks being short-lived without clearer signs of an off-ramp that will allow oil prices to cool,” said Chris Larkin at E*Trade from Morgan Stanley.

“While a quick resolution to the conflict is certainly a possibility, we view the conflict extending into the second quarter as an equally likely outcome, and a more protracted war cannot be ruled out,” said Antonio Gabriel at Bank of America Corp.

“Every day that goes by with the Hormuz Strait closed is another bad news for the global economy,” said Francois Rimeu, senior strategist at Credit Mutuel Asset Management. “If the crisis continues there will be at some point some kind of trigger that will make investors realize the scale of the supply shock that’s building up.”

President Trump’s talk of finding ways to reopen the Strait of Hormuz appeared to be helping boost the tone in markets. “I don’t know if that’s what’s really going to happen,” said Anthony Saglimbene, Ameriprise’s chief market strategist, in a phone call. “If so, it’s probably weeks away.” That’s why the dip buying might be temporary, Saglimbene said, noting that the Federal Reserve is on tap to deliver an update on the economy and the potential path for interest rates on Wednesday. There may also be Fed comments about the recent spike in oil prices, and their possible impact on inflation, to consider.

“I wouldn’t expect much [from the Fed],” said Will McGough, chief investment officer at Prime Capital Financial. He noted the central bank could address the geopolitical conflict as it relates to inflation as a way to reinforce a data-dependent stance. “They’re kind of between their two mandates – they kind of got them going different directions right now,” he continued. “The labor market is a little weakish, which should suggest a cut. Inflation is a little stubborn – probably going higher – which suggests a raise. So, those two net-net all set to: do nothing.”

Policymakers will likely avoid making bigger updates, reflecting uncertainty around the duration of the energy shock and weaker jobs data that underlines the ongoing need to balance inflation and labor risks, according to Krishna Guha at Evercore. While the Summary of Economic Projections might see a “hawkish drift,” Guha expects the median forecast to continue showing a rate cut this year and another one in 2027.

“For the Fed, much depends on how the conflict evolves. If the war ends quickly, we expect the unemployment rate to edge higher and core inflation to cool, allowing rate cuts of about 100 basis points this year. If the conflict drags on, keeping energy prices high and pushing inflation expectations higher, the calculus becomes far more difficult.” —Eliza Winger and Anna Wong, economists

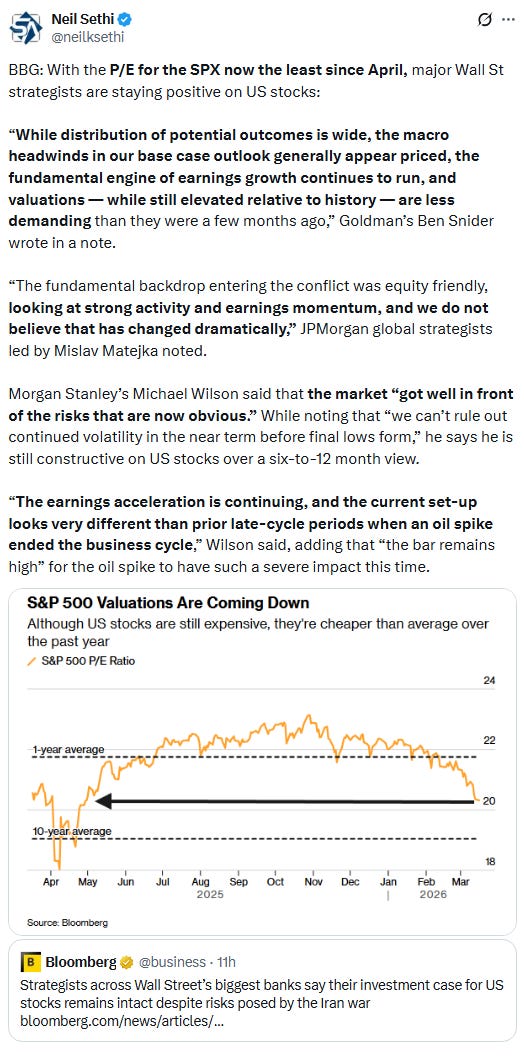

“While distribution of potential outcomes is wide, the macro headwinds in our base case outlook generally appear priced, the fundamental engine of earnings growth continues to run, and valuations — while still elevated relative to history — are less demanding than they were a few months ago,” Goldman’s Ben Snider wrote in a note.

“The fundamental backdrop entering the conflict was equity friendly, looking at strong activity and earnings momentum, and we do not believe that has changed dramatically,” JPMorgan global strategists led by Mislav Matejka noted.

Morgan Stanley’s Michael Wilson said that the market “got well in front of the risks that are now obvious.” While noting that “we can’t rule out continued volatility in the near term before final lows form,” he says he is still constructive on US stocks over a six-to-12 month view. “The earnings acceleration is continuing, and the current set-up looks very different than prior late-cycle periods when an oil spike ended the business cycle,” Wilson said, adding that “the bar remains high” for the oil spike to have such a severe impact this time.

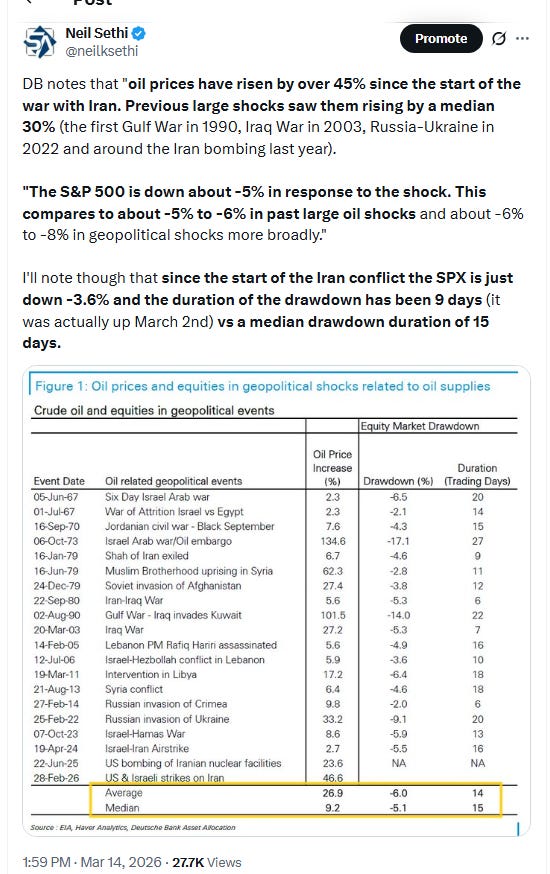

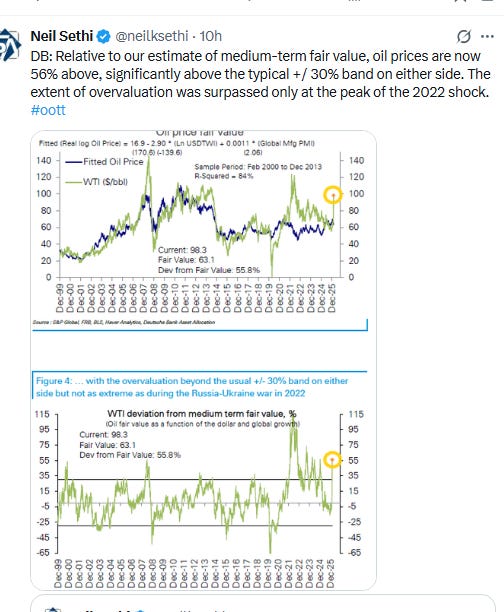

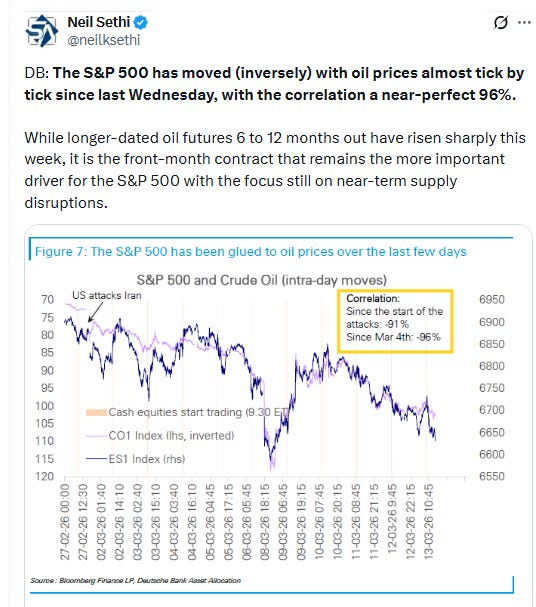

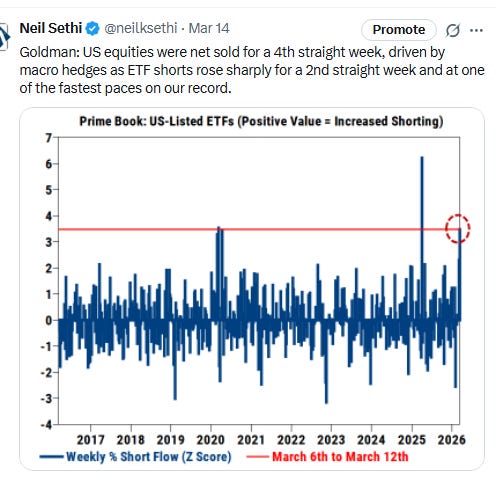

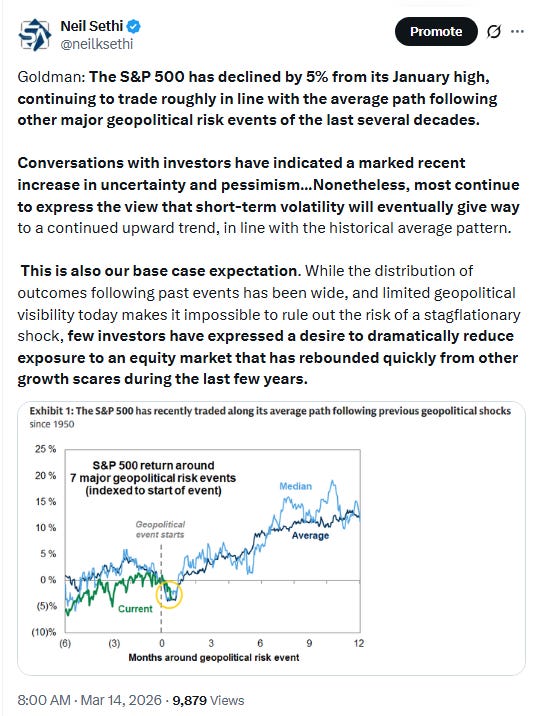

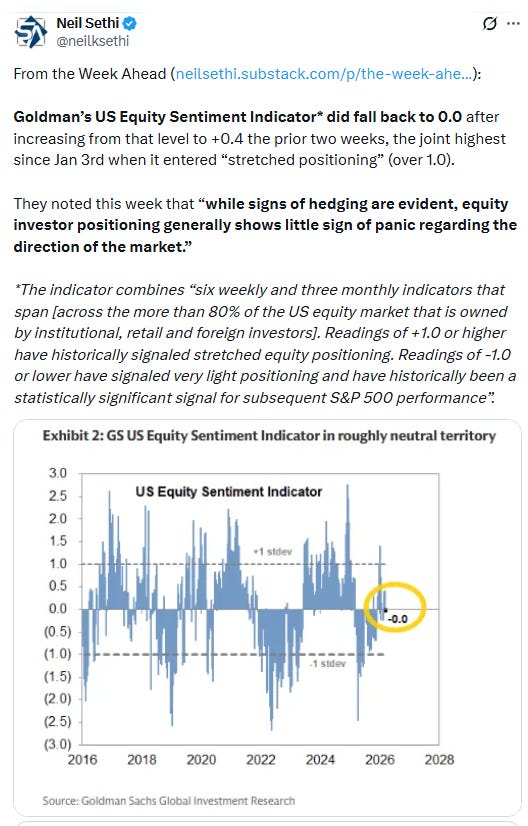

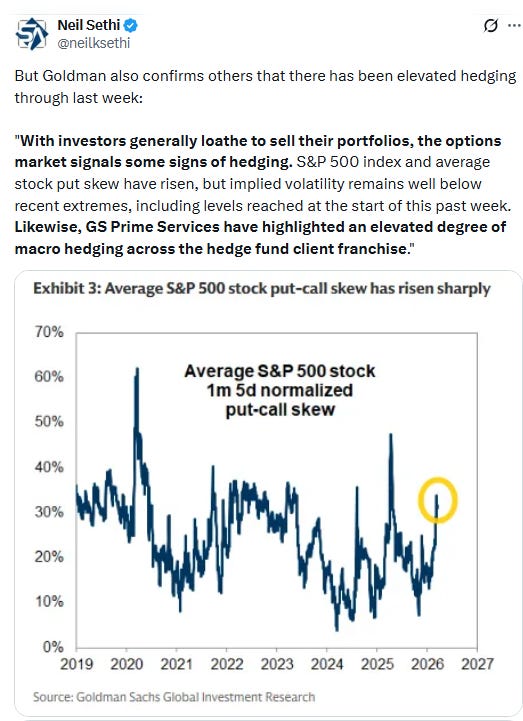

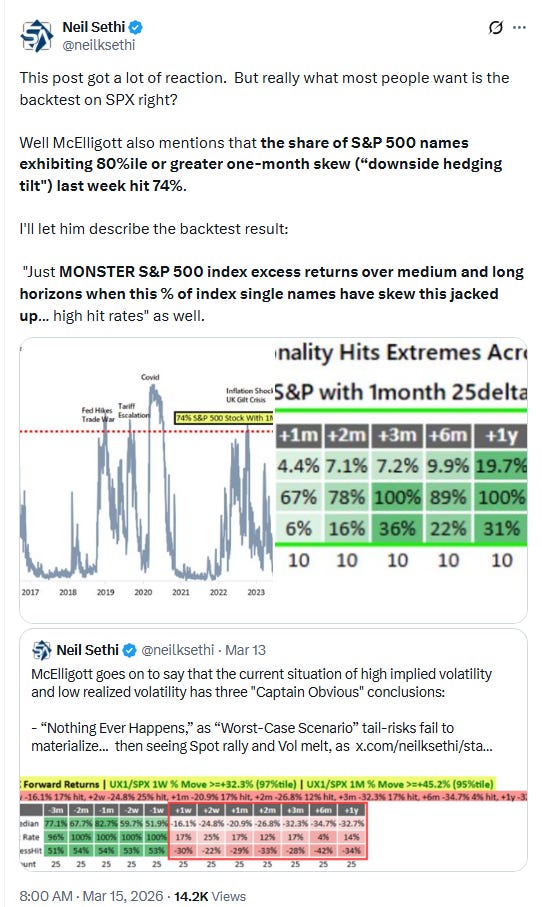

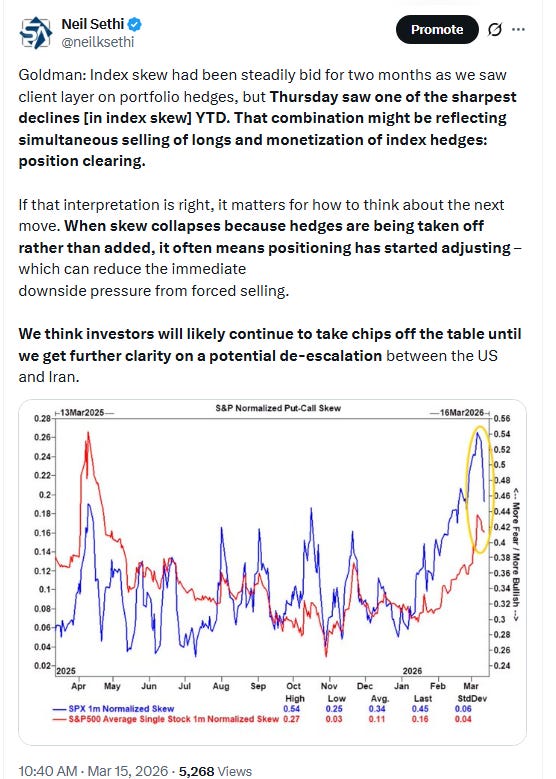

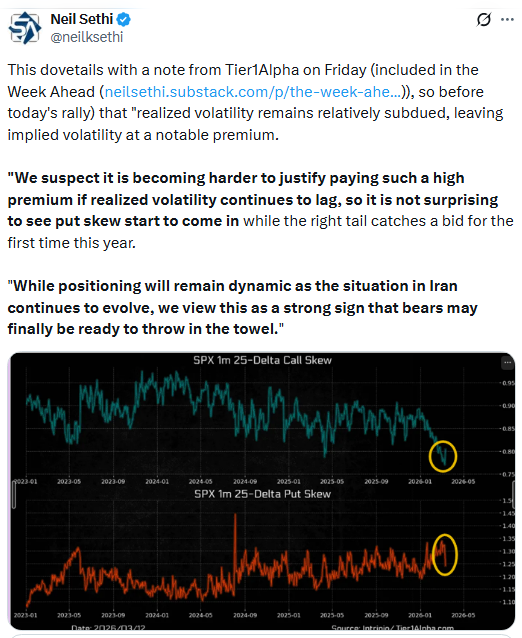

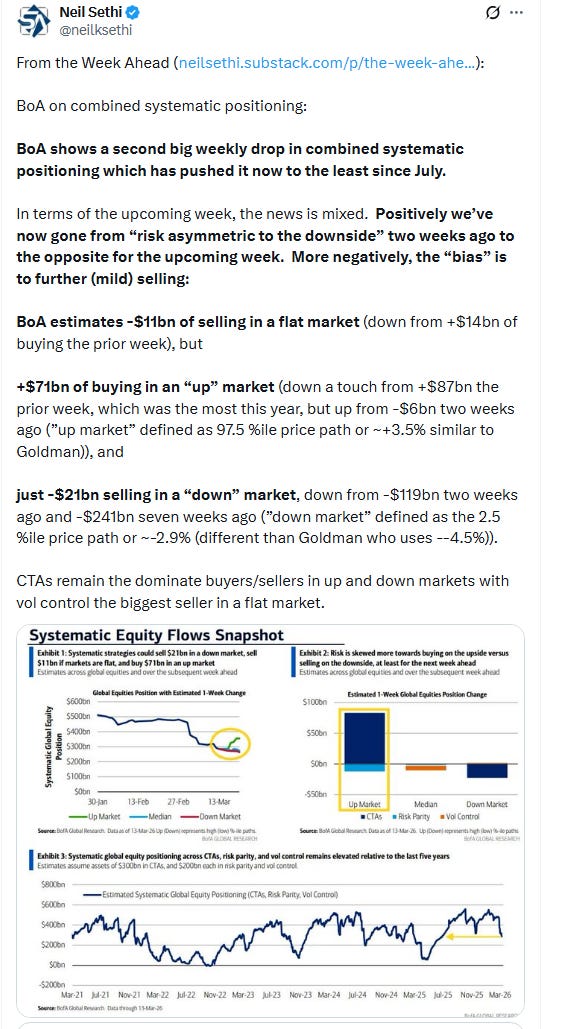

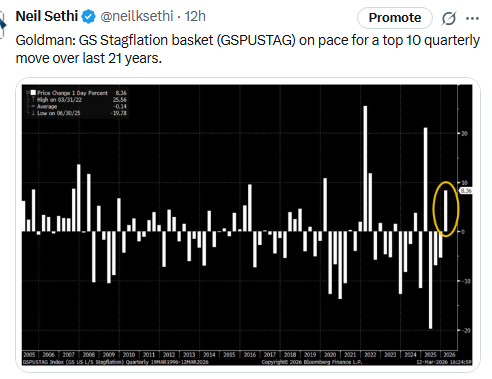

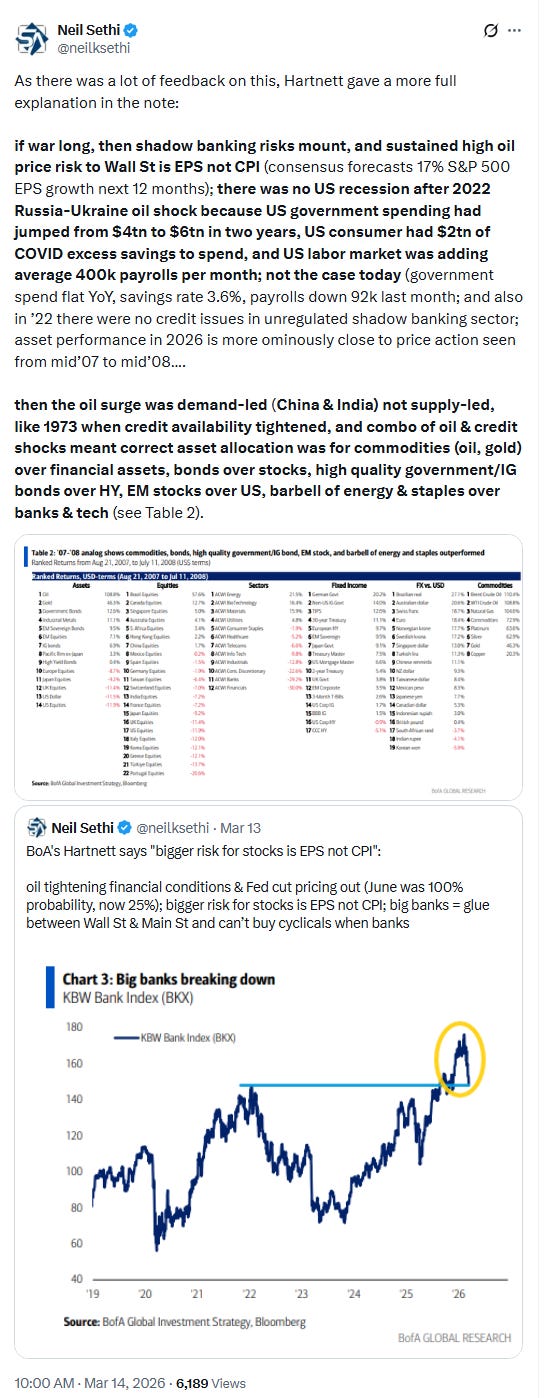

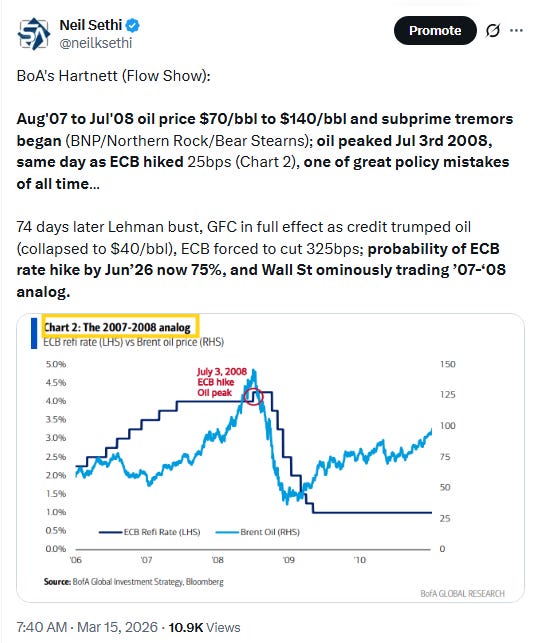

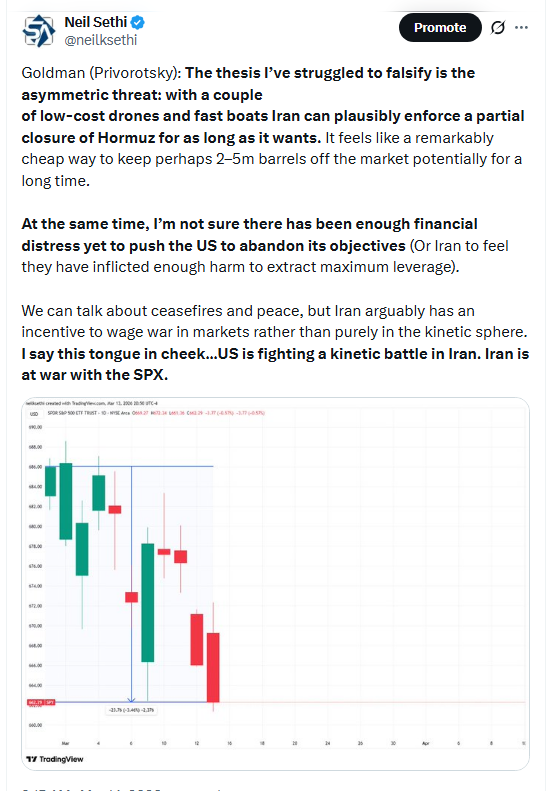

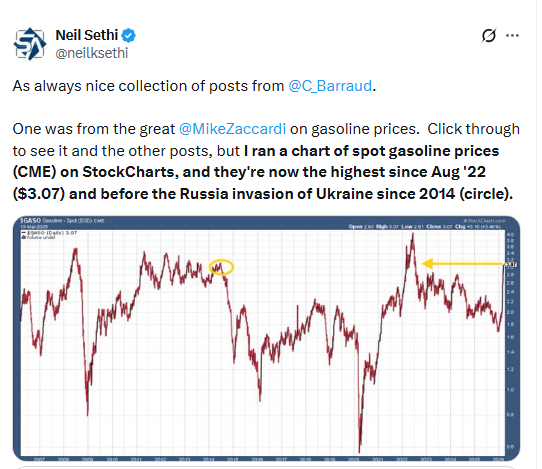

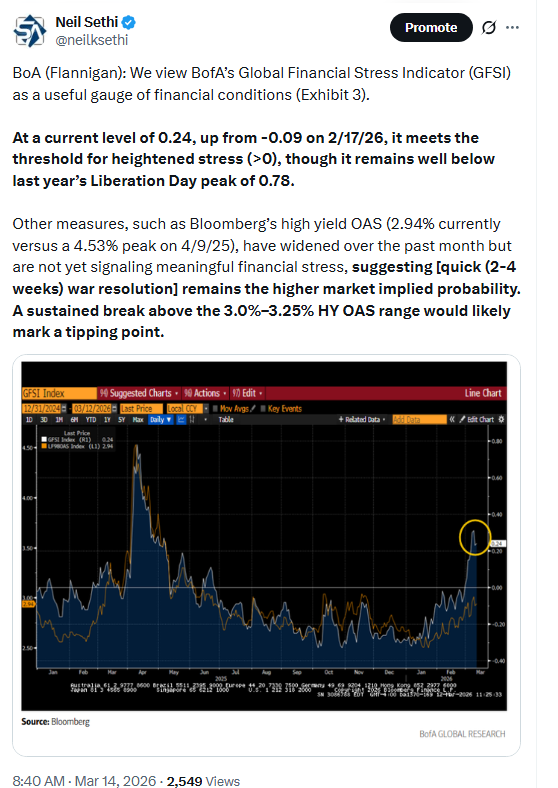

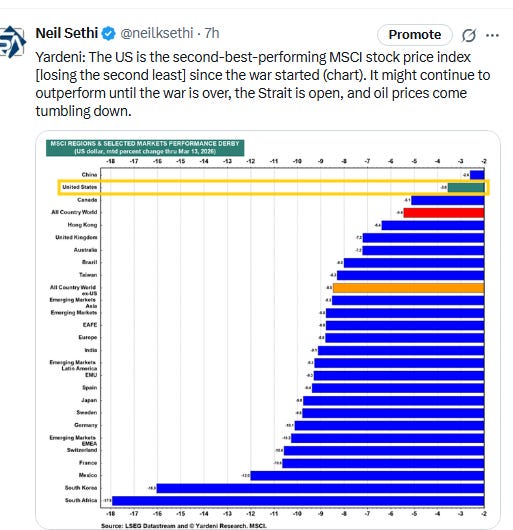

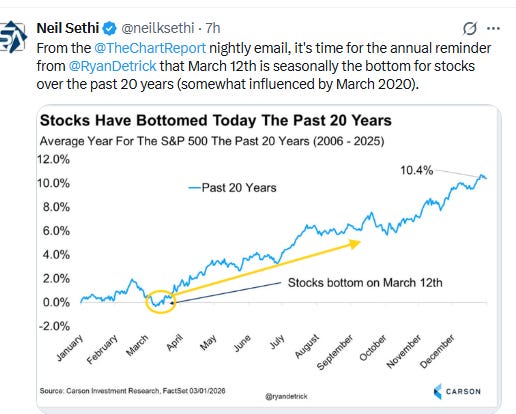

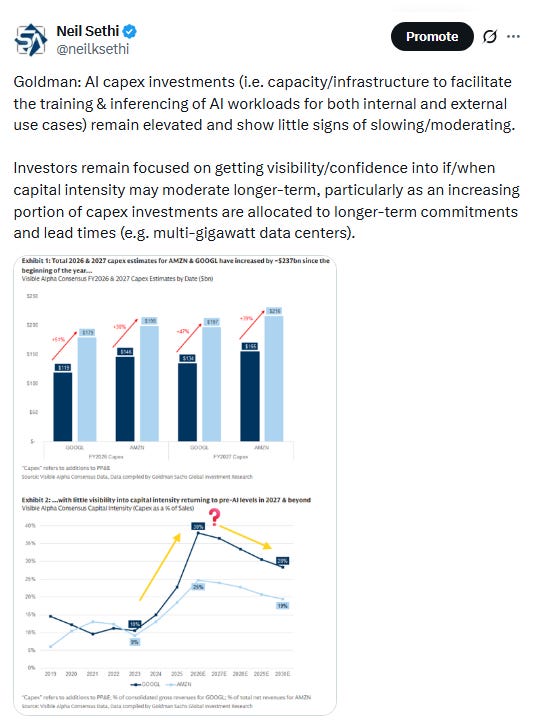

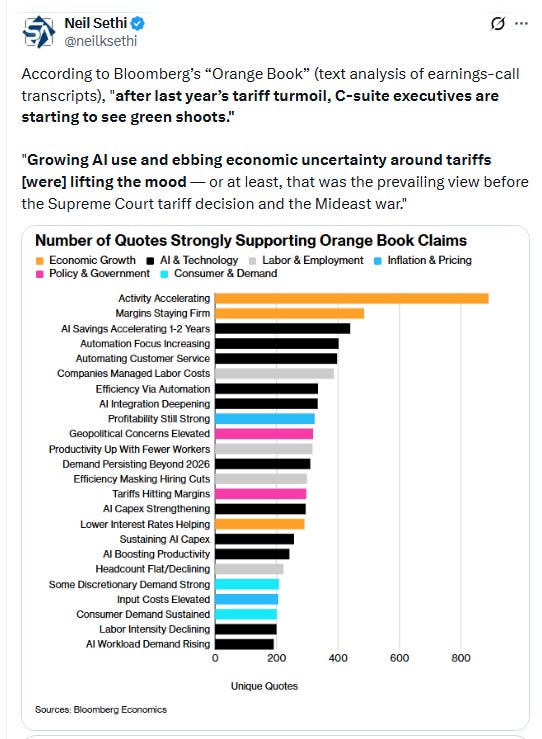

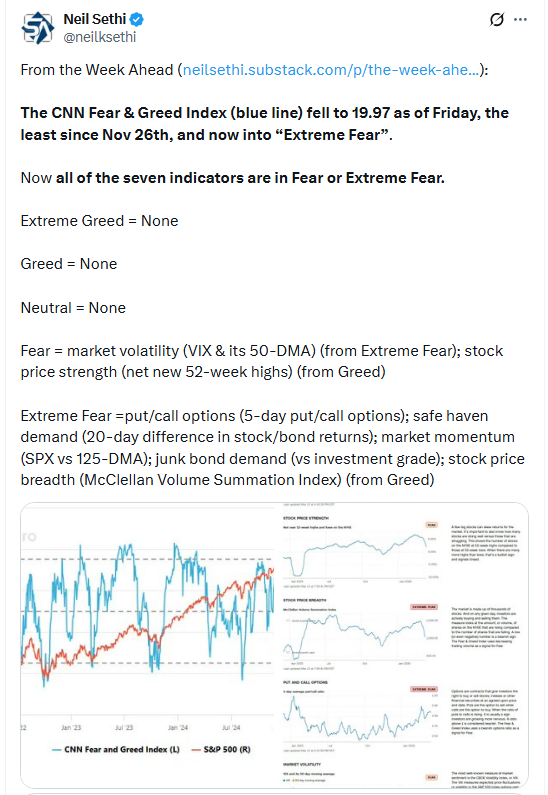

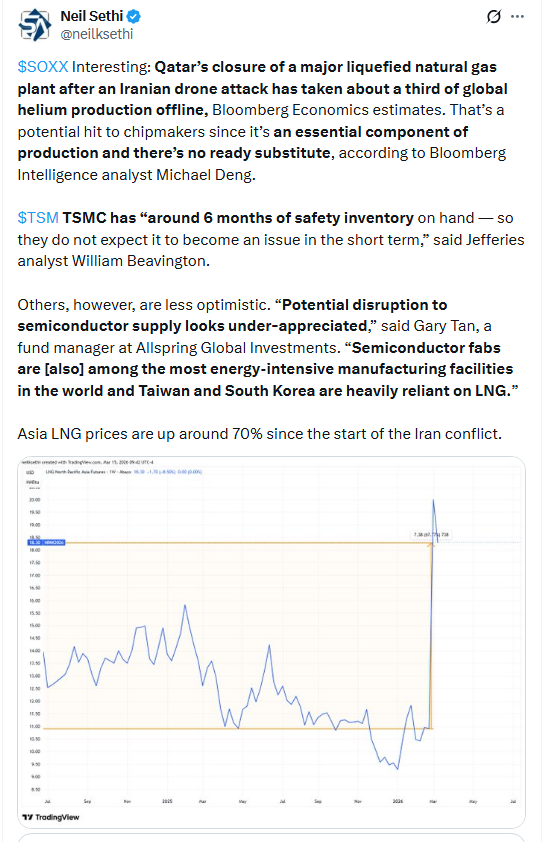

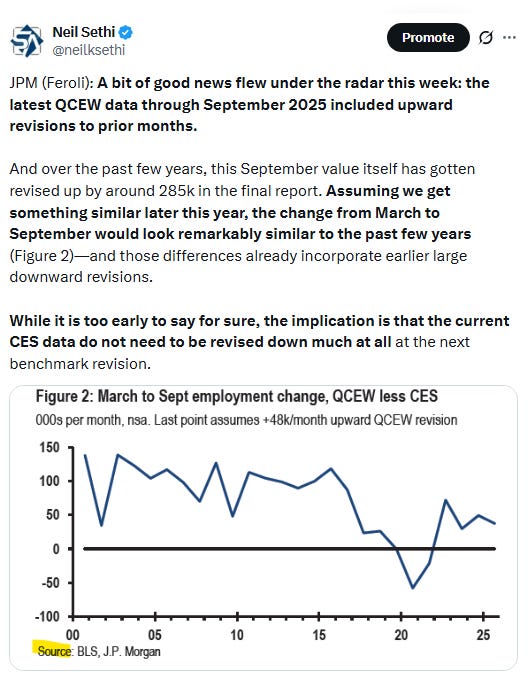

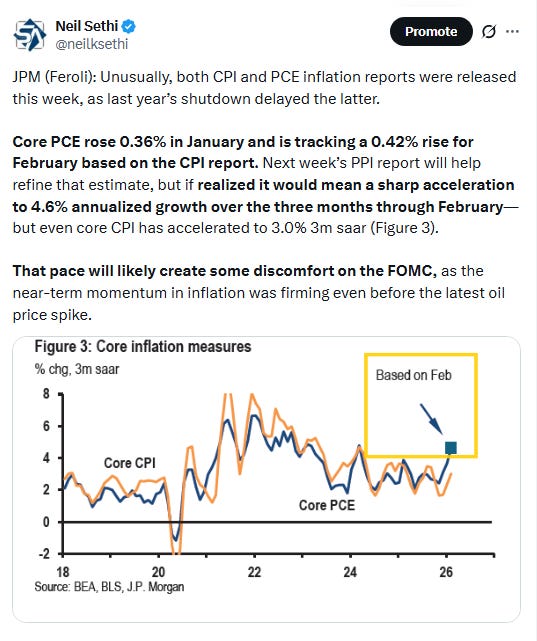

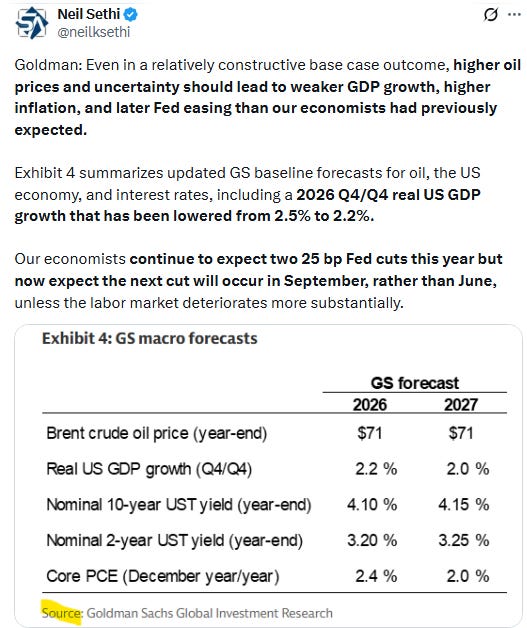

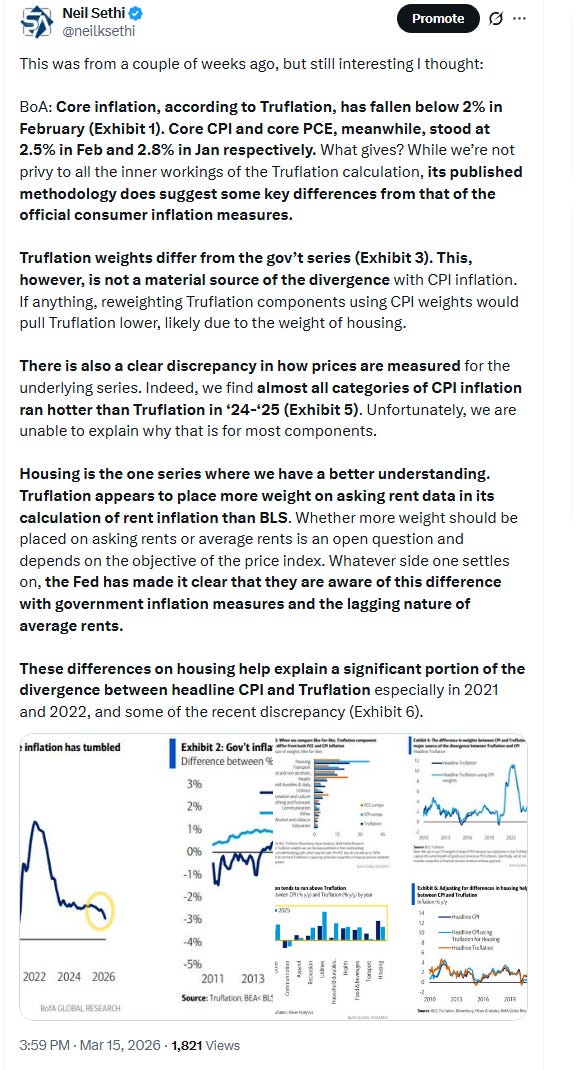

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

In individual stock action:

Tech led the advance, with Nvidia Corp. climbing 1.6% as it expects to make at least $1 trillion from artificial-intelligence chips through the end of 2027.

Meta shares gained more than 2% on a report — which the company has called “speculative” — that it is planning to lay off more than 20% of its workforce.

Corporate news from BBG:

Meta Platforms Inc. will pay as much as $27 billion over the next five years for access to AI infrastructure from cloud provider Nebius Group NV.

OpenAI is in advanced discussions to form a roughly $10 billion joint venture with private equity firms, according to people familiar with the matter.

Elon Musk’s startup xAI is looking to hire bankers and private credit lenders to make its Grok chatbot better at finance strategy.

Intel Corp. announced that its Xeon 6 chip is being used as the processor for Nvidia Corp.’s DGX Rubin NVL8 systems.

CoreWeave Inc., Cerebras Systems Inc. and telecommunications firm BCE Inc. will collaborate on one of Canada’s most powerful data centers in Saskatchewan.

Dollar Tree Inc.’s strategy to introduce higher-priced items is helping it increase sales, especially with wealthier shoppers.

Mid-day movers from CNBC:

In US economic data:

Substack articles.

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X