Markets Update - 3/18/26

Update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with charts!

To subscribe to these summaries, click below!

To invite others to check it out (sharing is caring!), here’s the button:

Link to posts on X - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog.

Also, if you see an error (a chart or text wasn’t updated, etc.), always appreciate a note in the comments section or email so I can fix it.

In that regard, I do make mistakes sometimes, and usually I catch them at some point and correct them, and/or I sometimes add new material, so it’s always safest to read from the website where it will have any updates.

US equity indices opened trading Wednesday lower after having given up gains earlier in the pre-market session which came from reports of Iraq resuming some exports through a pipeline to Turkey’s Mediterranean port of Ceyhan, continued limited sailings of vessels permitted by Iran, and President Trump saying the US could end the war with the Islamic Republic “in the near future.”

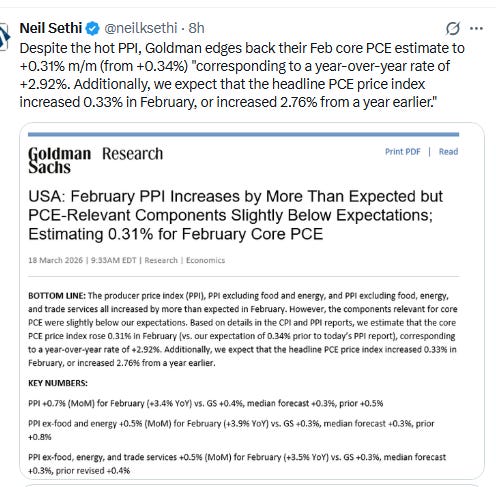

But that early positivity was wiped away, first as crude prices rebounded following Iran saying some of its energy facilities had come under attack, and then taking another leg lower after a much hotter than expected February wholesale price report, led by the biggest jump in food prices since May 2021, saw Fed rate cut bets sink and bond yields rebound (link is to my Substack).

And markets would continue to be pressured throughout the day, first as Iran warned Gulf countries that a number of regional energy assets would now be “legitimate targets” after the Israel attack on its giant South Pars gas field, then in the afternoon, despite a seemingly less hawkish than expected FOMC decision and statement/economic projections (covered below), as rate cut bets were further unwound, and then taking a final leg lower after Iran did in fact retaliate, attacking a complex in Qatar that houses the world’s largest liquefied natural gas export plant which suffered “extensive damage”.

By the end of the day major US equity indices were all down around -1.5%, the worst declines on a “Fed day” since December 2024.

Elsewhere, bond yields and the dollar rebounded to finish higher, as did crude and natural gas, while gold, copper, and bitcoin all were lower (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was -1.4%, the equal weighted S&P 500 index (SPXEW) -1.3%, Nasdaq Composite -1.5% (and the top 100 Nasdaq stocks (NDX) -1.4%), the SOXX semiconductor index -0.5%, and the Russell 2000 (RUT) -1.6%.

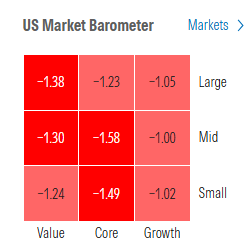

Morningstar style box shows every style in the red all down at least -1%.

Market commentary:

“The last couple of weeks have been about trying to protect portfolios from oil’s record rally,” said Carl Dooley, head of EMEA trading at TD Cowen. “As the speed of that curve slows, or even retraces, with the commodity’s implied volatility starting to subside, equities are finding a floor.”

“Equity markets are following the oil price quite closely, and at this stage what we’re seeing is perhaps that they are pricing in the most positive outcome,” said Nina Stanojevic, investment specialist at St. James’s Place. “That, I think, leaves equity markets quite vulnerable.”

"The Fed is in focus today, but it has no bearing on this [Iran] conflict. The Fed must react to the situation it finds itself in and today has been a clear sign that this conflict is definitely not over," said Kathleen Brooks, research director at XTB.

“There has been considerable debate over whether risk assets have fallen enough. That this question is still being asked suggests sentiment has not reached peak bearishness and the worst is likely not over.” — Skylar Montgomery Koning, macro strategist.

“It’s very clear the market is pricing this conflict in as temporary,” said Tim Urbanowicz, Innovator Capital Management chief investment strategist, on CNBC’s “Power Lunch.” “We think that is our base case as well. But we also want to be careful, because the reality of it is, the longer oil prices stay at these elevated levels, the more of a chance we have where inflation becomes sticky.”

While inflation risks have dominated in March, "we think downside risks to yields have risen and are underpriced," according to Friedrich Schaper and William Marshall at Goldman Sachs.

“The immediate impact of a potential closure of the Strait of Hormuz, something the US administration may have significantly underestimated, is higher energy prices,” said Tamas Varga, an analyst at brokerage PVM. “The US’s objectives in Iran remain unclear, and the end of the conflict is nowhere in sight.”

“With no end in sight to hostilities, shut-ins rising on a daily basis, and the Strait technically closed, we remain of the view that Brent is set to remain in a new, higher $95-to-$110 range,” said Robert Rennie, head of commodity research at Westpac Banking Corp. “Were we to see a major refinery plant hit or confirmation of additional mining of the strait, we would expect that range to extend higher by another $10-$20,” he added.

“The large upside surprise to the PPI in February confirms that stronger inflationary pressures were already making their way through supply chains even prior to the surge in oil prices,” Thomas Ryan, North America economist at Capital Economics, said in a note.

“PPI rising so much more than expected this morning, the day of an FOMC announcement, underscores how the inflation picture and expectations for Fed policy have changed in the past few months,” FHN Financial chief economist Chris Low wrote in a client note. “From comfortably expecting inflation and the Fed policy rate to fall this year, the market now is moving toward the realization neither will happen soon.”

The spike in energy costs risks adding to price pressures while restraining growth. The bigger issue for the economy is that inflation is proving sticky while energy costs are rising, which compresses the Fed’s room to maneuver, according to Christian Hoffmann at Thornburg Investment Management.

One point that has not received enough attention is the disinflationary impact of high oil prices through weaker demand, Hoffmann noted. Energy is clearly an inflation risk, but also an economic headwind, he added.

“The balance of risks has shifted, and the bar for cutting rates has risen meaningfully,” said Luis Alvarado at Wells Fargo Investment Institute. “Against that backdrop, the Fed’s current ‘wait‑and‑see’ approach appears appropriate.”

“The Fed didn’t move today — but it didn’t need to,” said Gina Bolvin, president of Bolvin Wealth Management Group. “This is a central bank that’s comfortable waiting, watching, and staying flexible. One projected cut tells you everything: the Fed is not in a rush, and neither should investors be.”

“I think we’re in a higher volatility regime,” said Anshul Sharma, chief investment officer at Savvy Wealth. “If oil stays elevated here ... we know that’s going to filter through into the economy,” he continued, noting that a persistent energy shock flowing through to inflation and growth starting to slow would be a “dangerous combination.”

“It’s going to make the Fed’s job harder in terms of balancing their mandates,” he said.

“There’s not really much of a chance of a rate cut possibly through the end of this year, and certainly not for the next three to four months,” said Scott Ladner, chief investment officer of Horizon Investments in Charlotte, N.C.

“The economic cost of surging energy prices is not yet known, so it’s understandable that Chair Powell struck a cautious tone about future rate cuts,” said Ellen Zentner at Morgan Stanley Wealth Management. “Because oil-supply shocks typically lead to a significant slowing in growth, there will likely be more room for policy easing than many people now expect.”

JPMorgan Investment Management’s Bob Michele said the Federal Reserve sent a “don’t worry about it” signal to markets spooked by surging oil prices and heightened geopolitical risk because of the war in Iran. The economy is feeling “a little bit of a near-term inflation shock” that could actually potentially help accelerate growth, Michele said in a Bloomberg Television interview Wednesday after the central bank left rates on hold. He said he was “gobsmacked” by the Fed’s decision. “They’re telling us don’t worry about it,” said Michele, the bank’s global head of fixed income. He isn’t buying it, he added: “There is a real impact to inflation and ultimately the labor market.”

Investors aren’t only on edge about the Iran conflict and the surge in oil prices. Jitters around artificial intelligence and private credit also loom large, said Jose Rasco, chief investment officer for the Americas at HSBC. “We are bullish longer term,” Rasco said Wednesday, while adding that he expects the next three to six months to bring a lot of volatility. Private credit appears to have a leverage problem, but he doesn’t think it’s anywhere near 2008-era risks. Rasco also sees the “AI trade” as in the midst of a repricing, because it’s now a global trade.

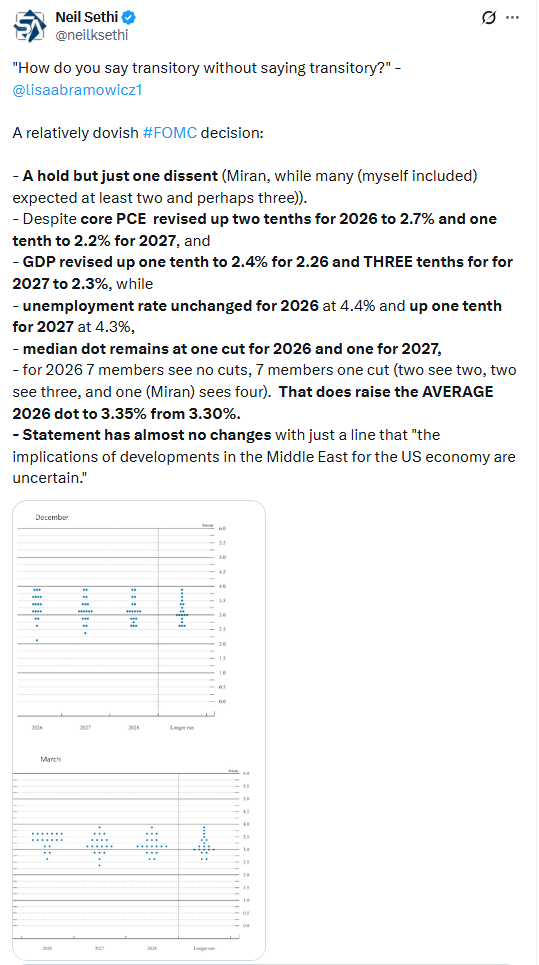

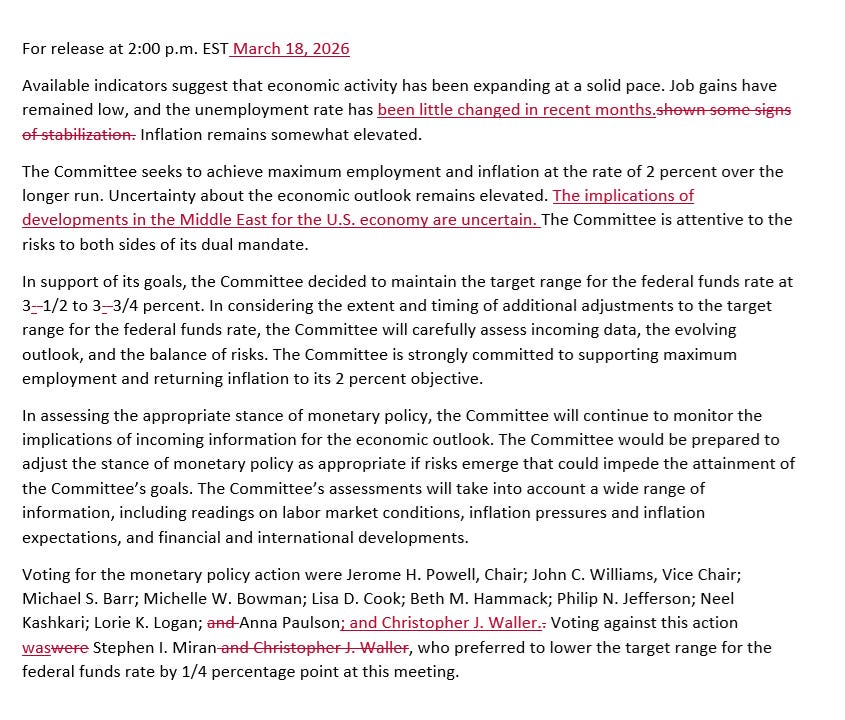

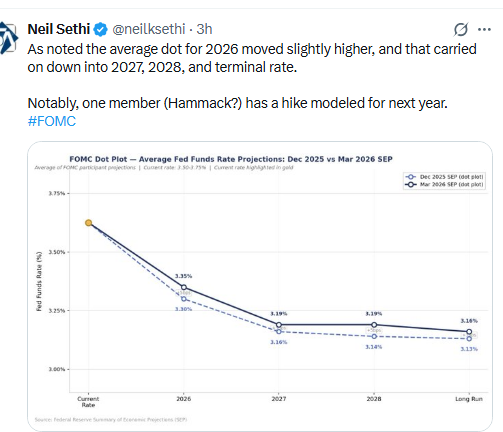

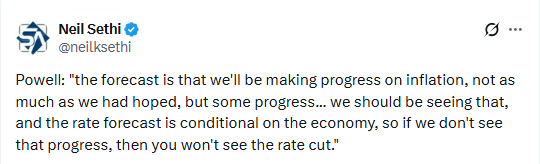

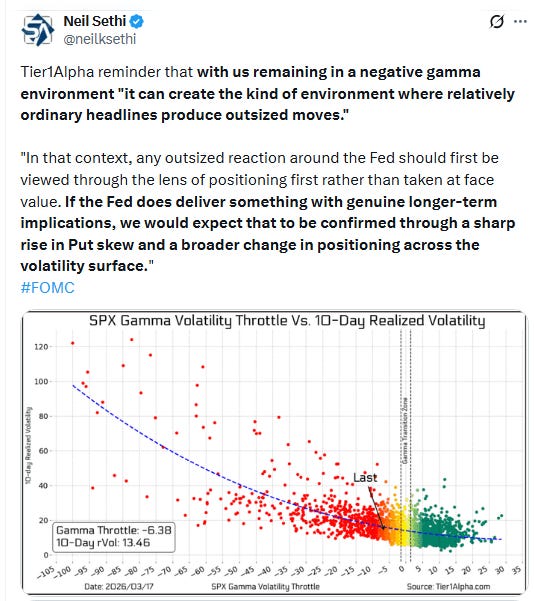

Note, normally FOMC commentary is in the subscriber section, but given the importance of some of the statements from today’s and the market reaction, I am putting them here:

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

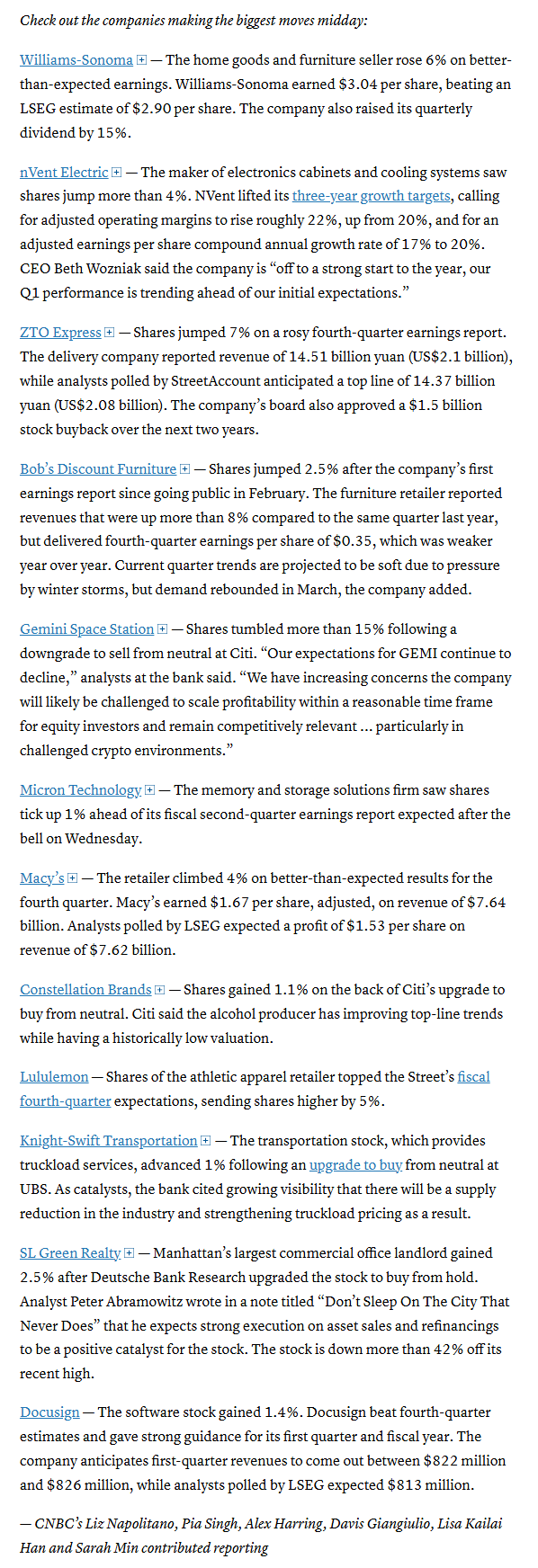

In individual stock action:

Corporate news from BBG:

Micron Technology Inc. warned that it will need to spend heavily on production to meet burgeoning demand, overshadowing a generally upbeat forecast from the largest US maker of computer memory chips.

Macy’s Inc. forecast stronger-than-expected sales in the current quarter, a sign that its fiscal year is off to a solid start as middle- and higher-income households continue to spend.

General Mills Inc. reported results for last quarter that missed Wall Street projections, weighed down by a decision to lower prices. But executives said they expected to realize the benefits of those reductions in the near future.

Artificial intelligence drone software maker Swarmer Inc. surged 1,000% in two days, making it the best debut for a US stock in nearly a year.

Mid-day movers from CNBC:

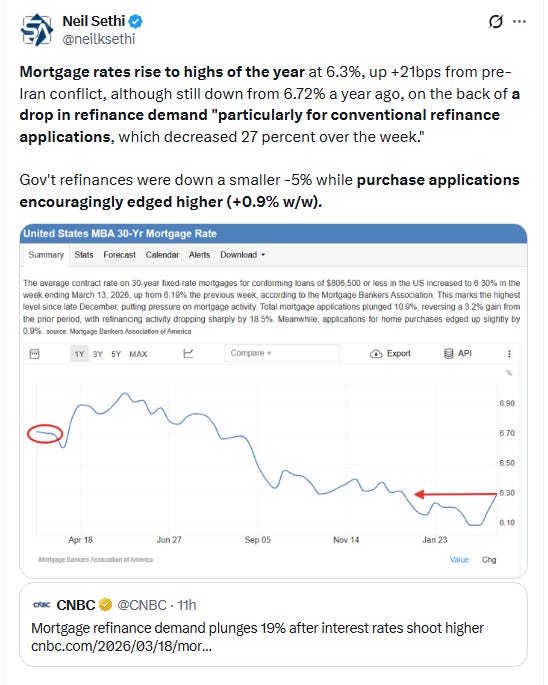

In US economic data:

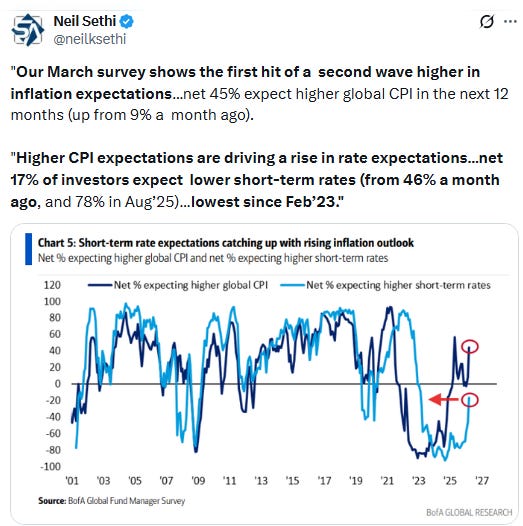

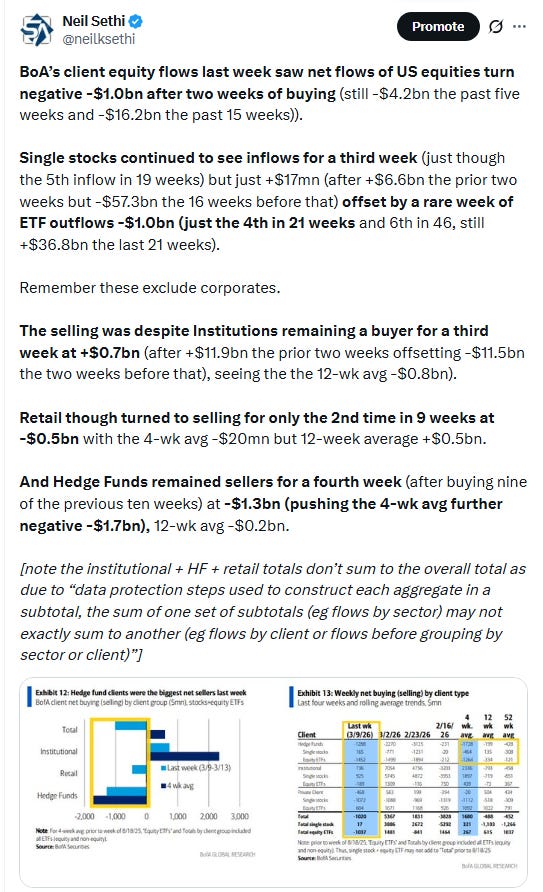

Substack articles.

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X