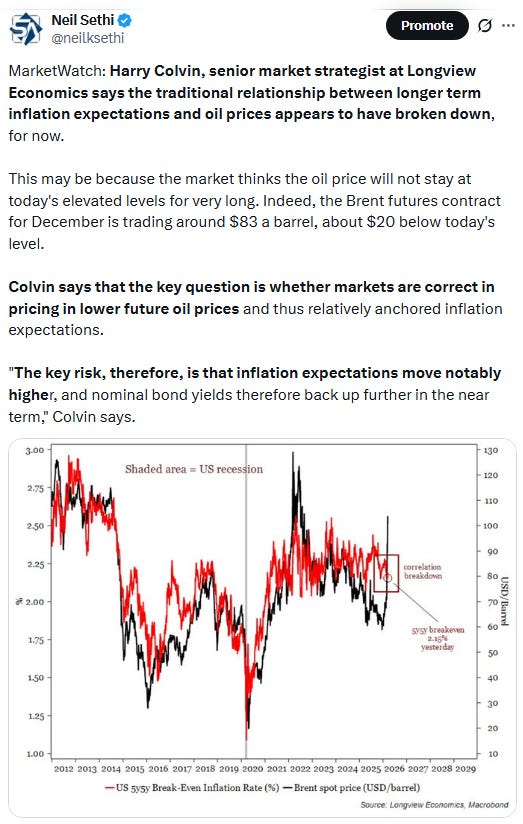

Markets Update - 3/19/26

Update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with charts!

To subscribe to these summaries, click below!

To invite others to check it out (sharing is caring!), here’s the button:

Link to posts on X - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog.

Also, if you see an error (a chart or text wasn’t updated, etc.), always appreciate a note in the comments section or email so I can fix it.

In that regard, I do make mistakes sometimes, and usually I catch them at some point and correct them, and/or I sometimes add new material, so it’s always safest to read from the website where it will have any updates.

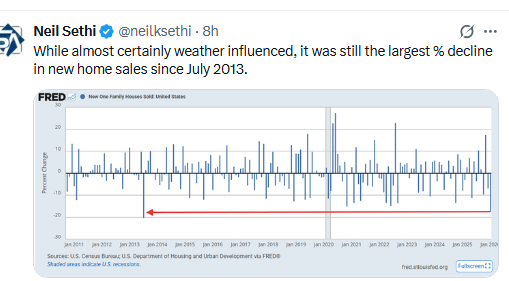

Note: the new home sales report was meant to be open to all subscribers (as most economic reports will be for now), and that is fixed, so feel free to check it out!

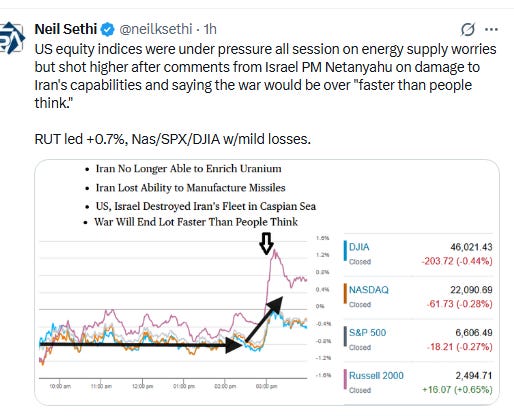

US equity indices opened trading Thursday again lower, at or near the lows of the year, as they continued to trade opposite to global energy prices which were again pressing higher following the regional attacks on energy infrastructure covered in last night’s Markets Update, even as President Trump tried to de-escalate the situation overnight saying the US was not involved in Israel’s attack on Iran’s facilities (and saying there would be none further by Israel) and threatening to “massively blow up the entirety of [Iran’s} South Pars Gas Field,” if they were to again attack energy facilities. Despite the warning, Saudi Arabia on Thursday said a drone struck its Samref refinery on the Red Sea. Meanwhile Qatar said around 17% of output from its portion of the gas field was offline. US equities were also under pressure from tech shares after a poor reaction (-6%) to a blowout earnings report from memory-chip maker Micron on “profit taking” following a 62% surge this year (after tripling in 2025) and perhaps concern over spending plans.

News flow would remain unconstructive until just before 3pm ET when Israel Prime Minster Netanyahu said in a press conference that Iran is no longer able to enrich uranium or manufacture ballistic missiles, adding the war will end “a lot faster than people think.” He also said that Israel was helping the U.S. “in intel and other means” to open the Strait of Hormuz, while leaders of the United Kingdom, France, Germany, Italy, the Netherlands and Japan expressed their “readiness to contribute to appropriate efforts to ensure safe passage through the Strait [of Hormuz].” Equities jumped higher, although just the small cap Russell 2000 index made it into the green +0.7%. Still the SPX, Nasdaq, and DJIA all cut back losses of around -1% to finish down a half to a quarter of that.

Elsewhere, bond yields, which surged intra-day to the highs of the year, reversed along with energy prices to finish little changed while the dollar fell to a 1-week low. Crude was also lower as were gold, copper, and bitcoin. US natural gas was higher (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was -0.3%, the equal weighted S&P 500 index (SPXEW) -0.1%, Nasdaq Composite -0.3% (and the top 100 Nasdaq stocks (NDX) -0.3%), the SOXX semiconductor index +0.9%, and the Russell 2000 (RUT) +0.7%.

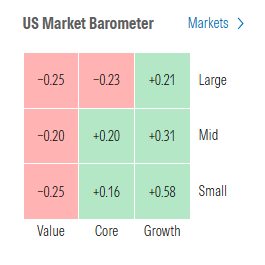

Morningstar style box shows growth led the rebound making it into the green.

Market commentary:

“The mood was clearly risk-off this morning, with markets still digesting a toxic mix of geopolitics and central bank messaging,” said Mathieu Racheter, head of equity strategy at Julius Baer. “The renewed escalation in the Middle East is reviving stagflation concerns just as investors were getting more comfortable on inflation up until March.”

“The biggest uncertainty or unknown is, how long is this crisis going to last? Should it linger for much longer, then the related impact on inflation and potentially on growth is what will break the market,” Barclays head of U.S. equity strategy Venu Krishna told CNBC’s “Closing Bell: Overtime” on Wednesday. “But we are not there yet. That’s not our base case. You just have to keep your fingers crossed.”

“The core dilemma of the entire situation remains the same: the U.S. and Israel have ‘won’ the war in a conventional sense, but there doesn’t seem to be a military solution for reopening Hormuz absent the deployment of ground troops, which means the waterway isn’t likely to return to normal without some type a diplomatic settlement (and it doesn’t appear at the moment like much effort is being put into achieving one),” said Adam Crisafulli of Vital Knowledge.

“Escalating attacks on energy infrastructure in the Middle East are raising the risk of a lasting impact on global oil and gas supply,” said Wolf von Rotberg, equity strategist at Bank J. Safra Sarasin. “The current market mood is unlikely to change until the escalation momentum is broken and oil prices normalize.”

“The widening Brent–WTI spread highlights that the impact of the conflict in Iran will be uneven, with European and Asian assets facing a more severe stagflationary shock than US counterparts.” — Skylar Montgomery Koning, macro strategist.

“While a less damaging outcome in the Strait of Hormuz remains possible, recent events have narrowed that path and heightened the risk of continued volatility,” said Ulrike Hoffmann-Burchardi at UBS Global Wealth Management.

“All the near-term action depends on the Strait opening,” said Scott Wren at Wells Fargo Investment Institute. “We think it opens in a matter of weeks, not months.” Sentiment is likely still leaning negative, with more downside in store, according to Wren at Wells Fargo Investment Institute. “We see a pullback in the 7-10% range from the record high as a good opportunity to step in,” he concluded.

“For the first couple of weeks of the war, people thought, ‘Okay, this is terrible. How can you not have the Strait open. This is going to cause major supply disruptions.’ But there was always this belief that, ‘It’s going to end very soon. It’s going to end any day. This is not sustainable,’” Peter Boockvar, chief investment officer at One Point BFG Wealth Partners, said to CNBC.

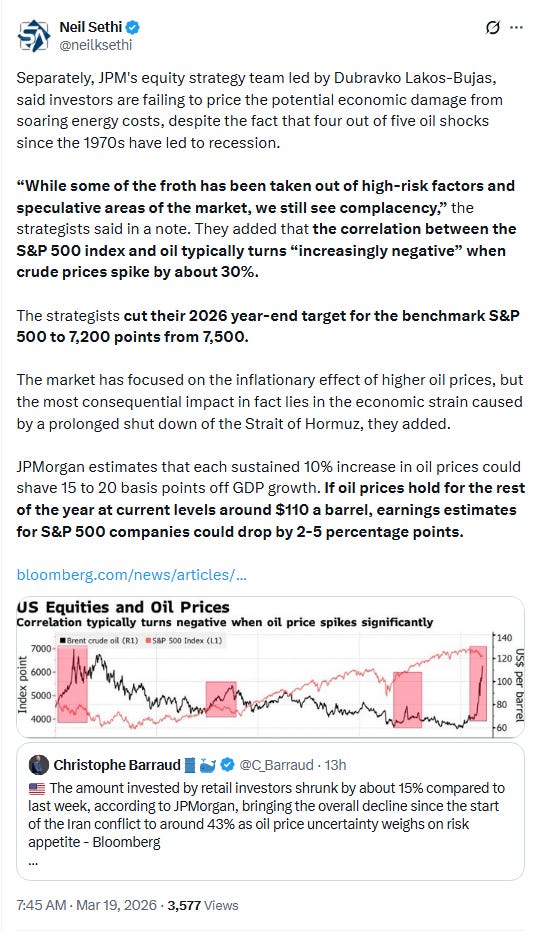

Now, as the conflict approaches its fourth week, the current circumstances have left investors thinking, “Well, maybe this doesn’t end so fast, and even when it does, we’re certainly not going back to levels in commodity prices prior to the beginning of the war,” he continued. “There’s no way, in my opinion, that oil is going back to $65 a barrel.” Besides the worries surrounding oil prices, Boockvar believes the mounting concerns in both technology and private credit prior to the war will persist beyond it, meaning investors are going to have to be even “more discerning” with portfolio management moving forward, he added.

“Our sense is that the largest risk to public markets is less about immediate system-wide credit losses and more about a sentiment-driven news flow de-risking loop: pressure on listed alternative managers and BDCs, widening credit spreads, and tighter bank/market financing conditions if fears escalate,” Wolfe Research said it a note to clients. Markets have stepped up scrutiny of private-market valuations and liquidity after a wave of markdowns and redemption pressure across private credit and equity funds. Investors grow increasingly sensitive to signs of stress in private credit and leveraged finance, even as defaults remain relatively contained. For Wolfe, the bigger threat is that deteriorating headlines, rather than realized losses, could drive a broader pullback in risk-taking.

In their Summary of Economic Projections, Fed officials continue to point to one rate cut this year, but Powell’s tone during his press conference this afternoon made even that forecast sound dubious. “There is also just the feeling that we haven’t seen the progress that we hoped for on core goods,” Powell said. “The key message out of today’s meeting is that the Fed is judging that the balance of risks is tilting toward concerns over inflation, which warrants a more cautious rate cut path over the near-term,” wrote Jason Pride, chief of investment strategy and research at Glenmede. With investors already on edge about conflict in the Middle East and the surging price of oil, Powell’s uncertain tone might have been one too many unknowns for the market, pushing stocks down into the close. “Rate cuts are not off the table for this year, but given the geopolitical nature of that risk, there will likely be considerable uncertainty over the future path for rates,” Pride added.

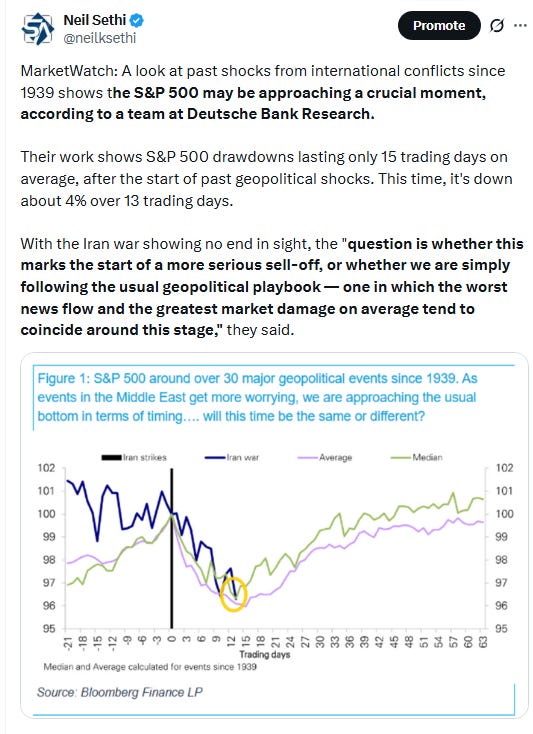

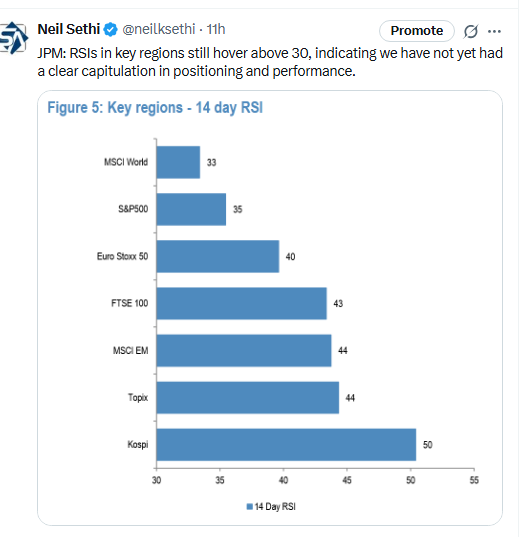

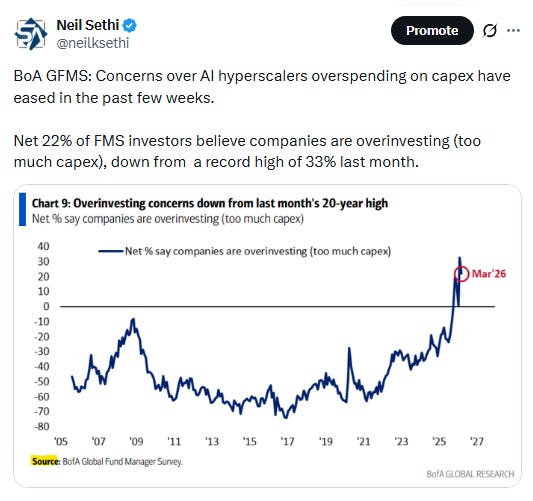

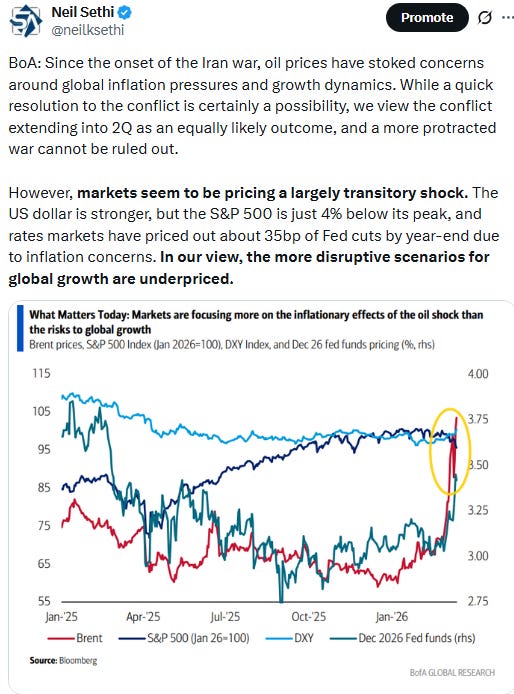

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

In individual stock action:

In tech, Micron Technology shares came under pressure Thursday, losing 3.8%. Citi analysts in particular attributed the move to just “some profit taking,” given that a memory supply shortage helped the semiconductor company nearly triple its revenue in its most recent quarter.

Post-market movers from CNBC:

Corporate news from BBG:

Micron Technology Inc. warned that it will need to spend heavily on production to meet burgeoning demand, overshadowing a generally upbeat forecast.

Alibaba Group Holding Ltd. aims to quintuple cloud and AI revenue to $100 billion annually in five years.

One of Eli Lilly & Co.’s most highly anticipated experimental medicines helped diabetic patients lose more weight than any drug currently on the market.

Darden Restaurants Inc. raised its full-year outlook as it expects an extra week of promotions at Olive Garden to lift sales.

Uber Technologies Inc. plans to invest as much as $1.25 billion in Rivian Automotive Inc. to help launch a robotaxi fleet that will be available in the US, Canada and Europe over the next five years.

Mid-day movers from CNBC:

In US economic data:

Substack articles.

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X