Markets Update - 3/20/26

Update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with charts!

To subscribe to these summaries, click below!

To invite others to check it out (sharing is caring!), here’s the button:

Link to posts on X - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog.

Also, if you see an error (a chart or text wasn’t updated, etc.), always appreciate a note in the comments section or email so I can fix it.

In that regard, I do make mistakes sometimes, and usually I catch them at some point and correct them, and/or I sometimes add new material, so it’s always safest to read from the website where it will have any updates.

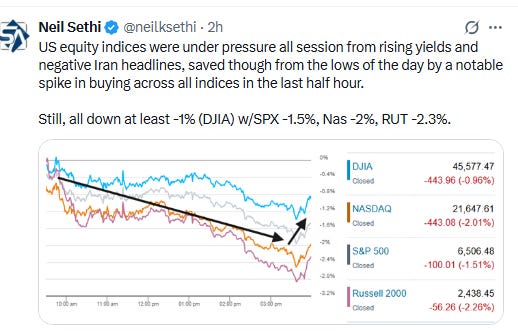

US equity indices opened trading Friday again lower, not able to build on the more positive mood at the end of Thursday’s session noted in last night’s Markets Update, as overnight attacks continued, and Axios reported that the US is considering taking over Iran’s Kharg Island, their key oil-export site, to put pressure on Tehran to reopen the Strait of Hormuz while the Wall Street Journal reported that the Pentagon is deploying three warships and thousands of additional Marines to the Middle East and CBS reported the Pentagon is preparing to deploy ground forces into Iran. Meanwhile, Bloomberg reported that Iranian officials are reluctant to even discuss reopening the Strait while US attacks are ongoing.

Also pressuring stocks were continued moves higher in crude prices and bond yields with the 10-year US Treasury yield (which 30-year mortgage rates are priced off of) pushing up to 4.4%, the highest since early August. That’s from 3.95% at the start of the month.

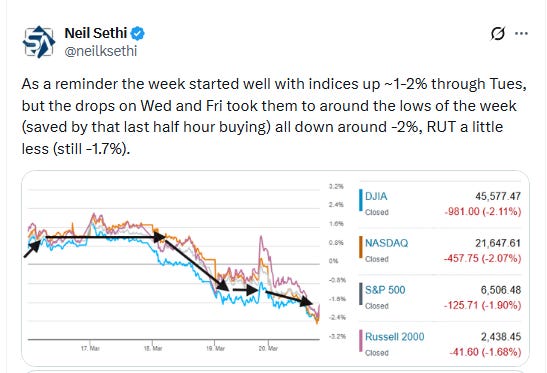

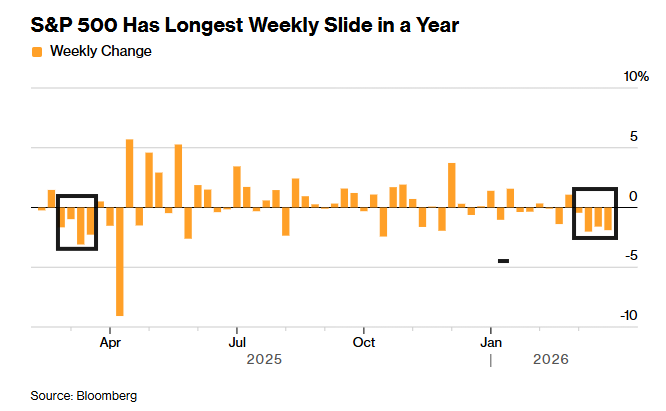

The selling was broad on Friday with tech leaders seeing some of the biggest losses. Nvidia and Tesla lost 3% apiece. That saw stocks fall all day before a late-session burst took them off the lows. Still, all finished down at least -1% (DJIA) with the SPX -1.5%, Nasdaq -2%, Russell 2000 -2.3%. That capped the fourth straight losing week (the first in a year for the SPX) all finishing down around -2%.

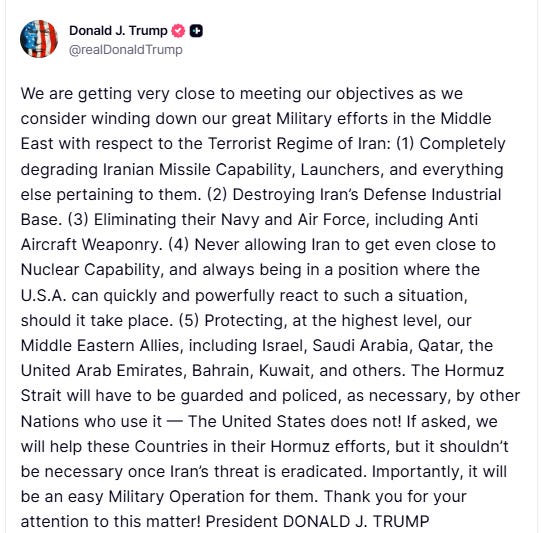

As I’m writing this, though while President Trump indicated to reporters this evening that “I don’t want to do a ceasefire… you don’t do a ceasefire when you’re literally obliterating the other side,” he said in a Truth Social post that the U.S. is “getting very close to meeting our objectives as we consider winding down our great Military efforts in the Middle East.” The Strait of Hormuz, he said, “will have to be guarded and policed, as necessary, by other Nations who use it — The United States does not!… If asked, we will help these Countries…but it shouldn’t be necessary once Iran’s threat is eradicated.”

Elsewhere, as noted bond yields were sharply higher and the dollar bounced from the lows of the week. Crude was also higher, but gold, copper, and bitcoin all fell with gold seeing its worst week since 1983 (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was -1.5%, the equal weighted S&P 500 index (SPXEW) -1.5%, Nasdaq Composite -2.0% (and the top 100 Nasdaq stocks (NDX) --1.9%), the SOXX semiconductor index -2.5%, and the Russell 2000 (RUT) -2.3%.

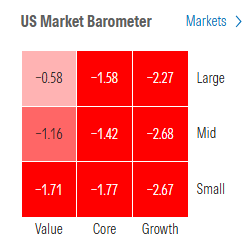

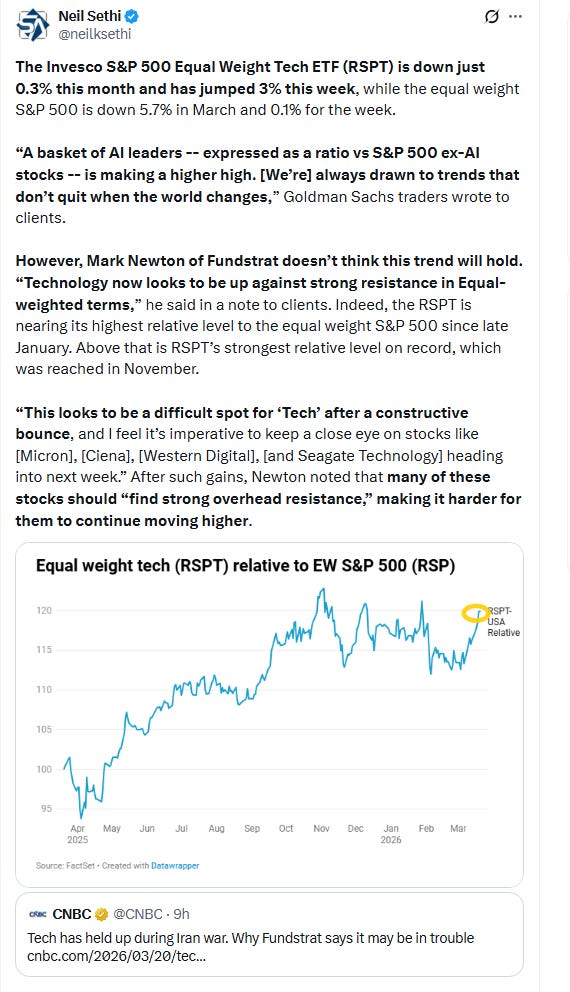

Morningstar style box shows growth led the selling after outperforming Thursday.

Market commentary:

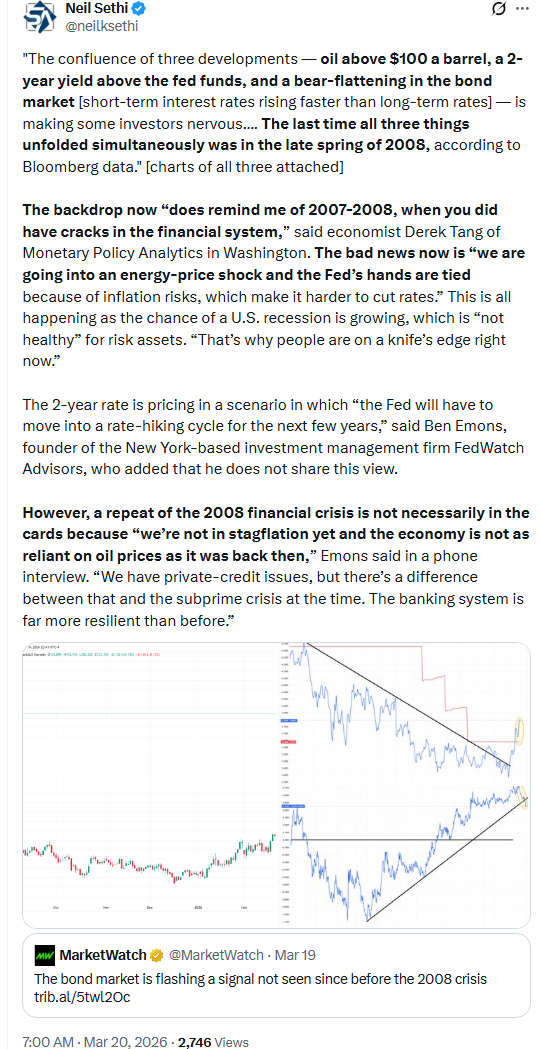

“We’re in a vulnerable environment at the moment with possible interest-rate hikes and Brent above $100,” said Nicolas Forest, chief investment officer at Candriam in Brussels. “If the Stoxx 600 and the S&P 500 are not able to hold technical levels today, this might signal upcoming stress.”

“The market was wrong at the start of the conflict, thinking it would end swiftly,” said David Kruk, head of trading at La Financiere de l’Echiquier in Paris. “Investor sentiment has clearly shifted into a more bearish positioning.”

“Investors initially thought that the Iran war would be short,” said Jose Torres at Interactive Brokers. “But as aggressions intensify amid no light at the end of the tunnel, the pain on Wall Street continues.”

“Some investors can be hesitant to maintain their positions heading into the weekend when more negative headlines from the Middle East can emerge,” said David Laut at Kerux Financial. “The stock market remains in negative territory for the year, and has made new 2026 lows this week, which suggests that the market may not have yet found its bottom and is still in the process of sorting out and pricing in the duration of the Middle East conflict,” said Laut.

Money market funds are the safe haven of choice, Hackett added, suggesting investors are parking money on the sidelines rather than engaging in a structural allocation shift. “Our recommendation for long-term investors is clear: Stay invested,” said Mark Haefele at UBS Global Wealth Management. “History shows that attempts to ‘market time’ geopolitical events often result in failure.”

Deutsche Bank’s Jim Reid said today will mark the 15th trading day of the conflict so far. “That is on average when we bottom out in U.S. equities after a geopolitical shock,” he said. “However it would be hard to trade on the back of averages at the moment with so much uncertainty so headlines will be more important than history here but if you’re looking for optimism the normal geopolitical playbook would at least give you hope. So far we haven’t deviated from it.”

Unlimited CEO Bob Elliott thinks the market is still too optimistic about the impact the war could have on earnings and the economy. “When you look at stocks compared to bonds, the markets are pricing in stronger growth since the beginning of this conflict. That doesn’t make any sense,” he told CNBC’s “Closing Bell: Overtime” in an interview. “Households basically getting something like 1% to 2% of real purchasing power taken away from them, even if this conflict resolves tomorrow.”

“If this is an escalation involving troops on the ground, then we’re probably in for at least a couple more weeks of this sort of market of higher oil prices, high gas prices; you’re hanging on every headline about energy infrastructure in the region,” Baird investment strategist Ross Mayfield said to CNBC. “Quite frankly, equity markets haven’t sold off in a way that would reflect this sort of event yet, so there could still be some some downside ahead.”

“At some point people are hoping this gets resolved,” said Robert Pavlik, senior portfolio manager at Dakota Wealth Management. But the longer it lasts, the more worried people are getting about the oil shock and inflation pressures, he said. The policy-sensitive 2-year Treasury rate jumped 13 basis points to 3.92%, according to FactSet, levels more consistently seen last June. Yet any attempt by the Federal Reserve to raise interest rates isn’t the answer, Pavlik said, noting that the oil problem remains an issue of too little supply, not one of too much demand. “The economy will slow itself.”

“The Fed is caught between slowing growth and renewed inflation pressure, with neither side clearly dominant,” said Julia Hermann at New York Life Investment Management.

“This is likely due to the view that the Fed will need to hike rates to combat elevated inflation,” said Gennadiy Goldberg at TD Securities. “We disagree with this assessment as the spike in oil prices should delay Fed rate cuts amid stagflationary pressures, but a sufficient move higher in oil could create a financial conditions shock that may require the Fed to respond with cuts.”

“A short-lived oil shock could potentially open up space for a cut in the fourth quarter under the next chair, while a more severe shock — especially one that tightened financial conditions — could actually lead to more rate cuts if accompanied by a weaker labor market,” said Idanna Appio, portfolio manager and senior research analyst at First Eagle Investments.

In a Thursday note, UBS’ Global Wealth Management stuck by its bullish stance on equities through year’s end. “Our recommendation for long-term investors is clear: Stay invested. History shows that attempts to ‘market time’ geopolitical events often result in failure,” wrote Mark Haefele, Chief Investment Officer of UBS Global Wealth Management. “Our base case is that equity markets will end the year higher, and that bond yields will end the year lower. Periods of volatility can also represent attractive times for investors looking to deploy cash to ‘phase in.’” Haefele added that investors should also consider diversifying their portfolios outside of just equities. “While we hold an Attractive stance on equities overall, we also emphasize regional and sectoral diversification, managing concentration risks, building allocations to quality bonds, broad commodities, gold, and alternatives, as well as making specific reductions to risk and adding hedges where appropriate,” he said.

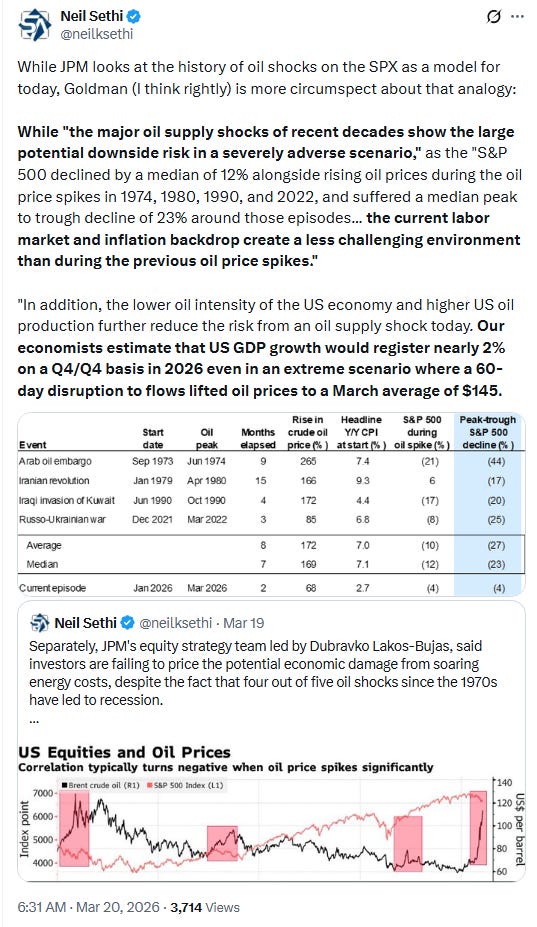

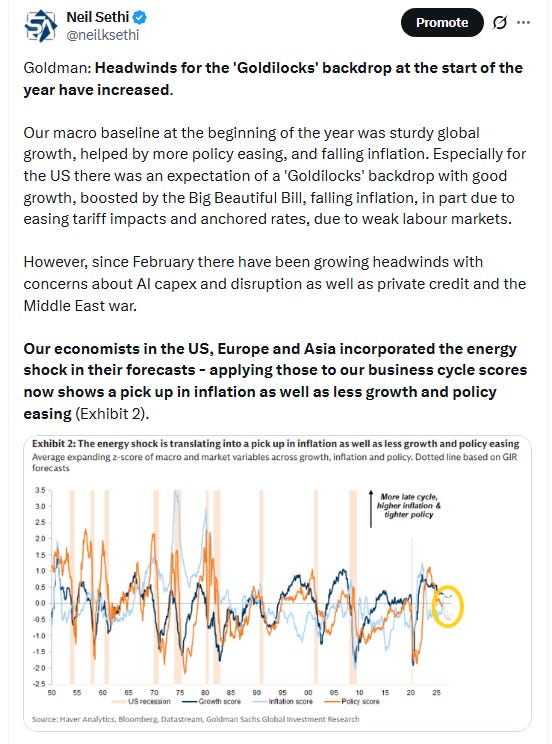

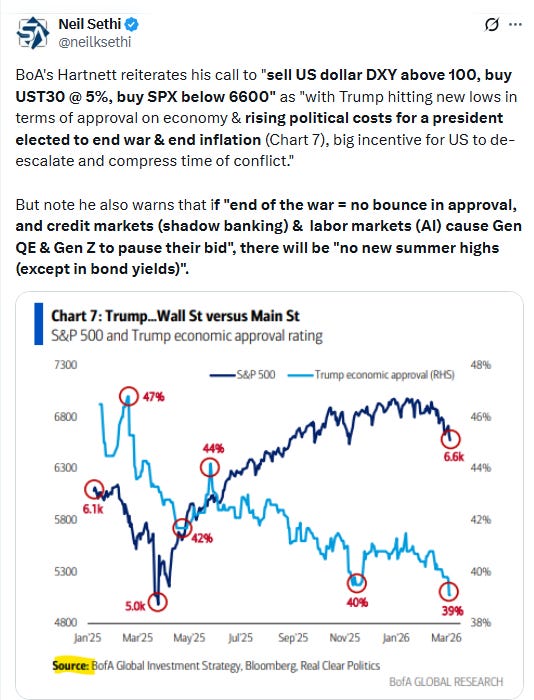

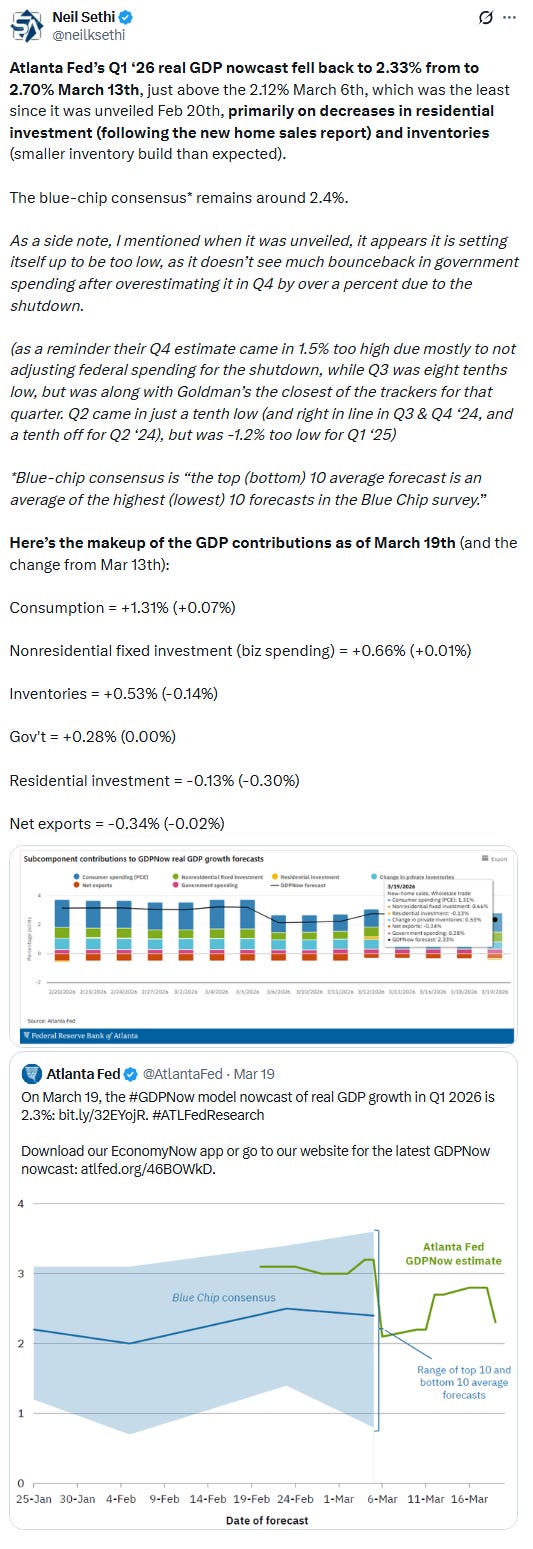

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

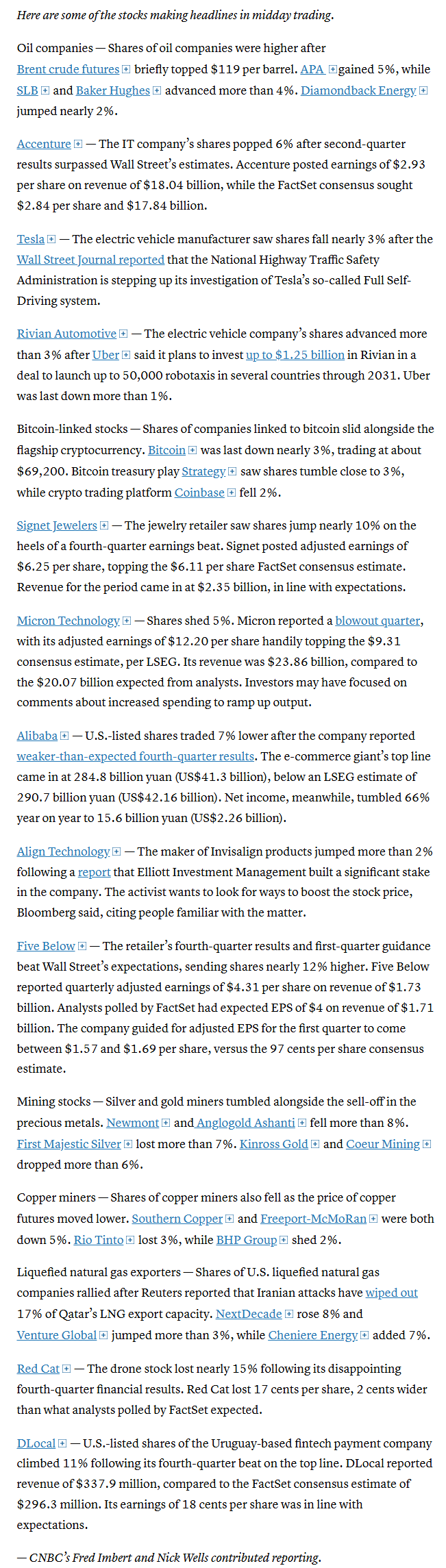

In individual stock action:

In corporate news, shares of Super Micro Computer tumbled more than 26% after U.S. prosecutors charged several company employees with smuggling Nvidia chips to China, while FedEx popped 9% on fiscal third-quarter results that beat the Street

Corporate news from BBG:

FedEx Corp. rose on a bullish profit forecast that signaled the plan to restructure its delivery network is gaining traction.

The US charged a Super Micro Computer Inc. co-founder with illegally diverting billions of dollars in Nvidia Corp.-powered servers to China.

Nvidia Corp.’s $20 billion licensing deal with Groq is being probed by a pair of Democratic senators over whether it violates antitrust laws.

Mid-day movers from CNBC:

In US economic data:

Substack articles.

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X