Markets Update - 3/5/26

Update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with lots of charts!

To subscribe to these summaries, click below!

To invite others to check it out (sharing is caring!), here’s the button:

Link to posts on X - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog. Also please note that I do sometimes add to or tweak items after first publishing, so it’s always safest to read it from the website where it will have any updates.

Finally, if you see an error (a chart or text wasn’t updated, etc.), always appreciate a note in the comments section or email so I can fix it.

US equity indices opened trading Thursday modestly lower overall remaining in their range over the past three sessions. They had earlier been higher following a report that Iran had told the US it was ready to relinquish its stockpile of highly enriched uranium in return for “something good.” The move faded in the absence of a confirmation from Washington. Crude briefly pared an advance before resuming its climb hitting the highest since 2024 after after Iran said it hit an oil tanker with a missile. Earlier, Iran vowed to escalate its retaliation against US strikes. The fears of feedthrough to inflation continued to ripple with bets on Fed rate cuts continuing to fall to new lows and the yields on Treasuries climbing for a fourth day.

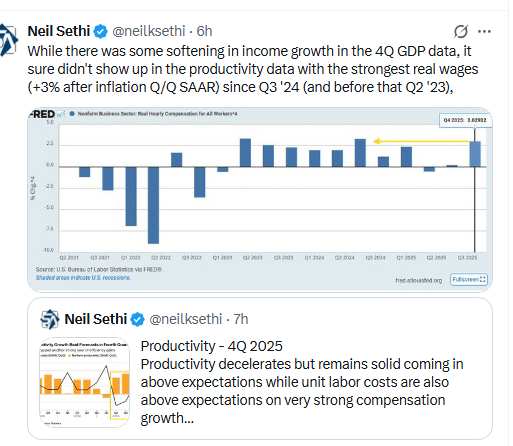

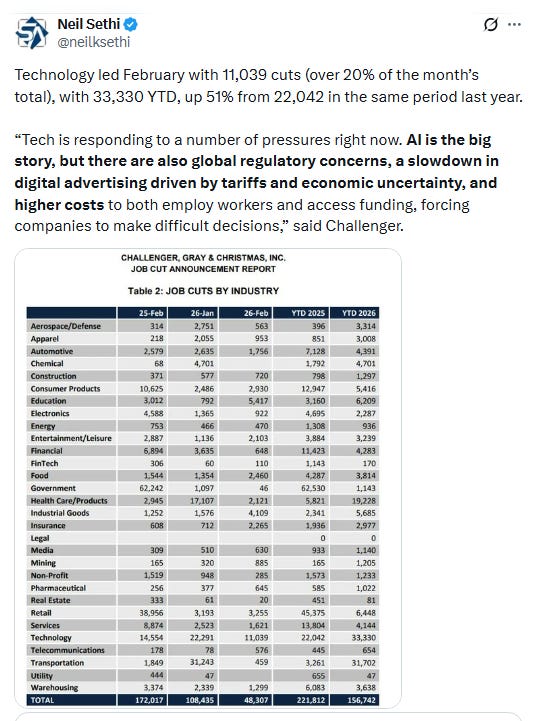

In economic data, layoff announcements at US companies subsided last month, data from outplacement firm Challenger, Gray & Christmas showed, and initial jobless claims were little changed (continuing claims edged higher) from the prior week. US labor productivity rose in the fourth quarter by more than forecast, but labor costs also rose more than expected. Import prices came in slightly lower than expected. Links are to my unlocked Substack summaries of those reports.

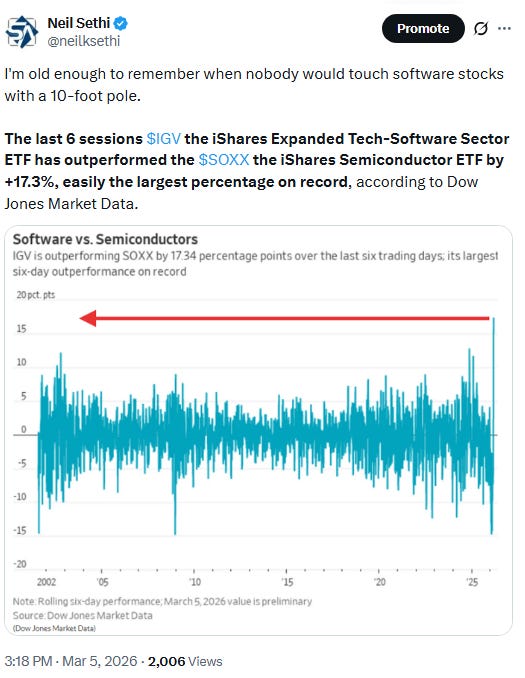

US equity indices would meander lower from the open until getting a lift in the last 90 minutes. It wasn't enough to get any of them into the green though with losses led by the small cap Russell 2000 -1.9%. DJIA was -1.6%, SPX -0.6%, Nasdaq -0.2% with tech outperforming a 2nd day despite a selloff in semiconductors (SOXX index was -1.2%).

Elsewhere, bond yields as noted up for a fourth day to 3-week highs, and the dollar was also higher as were crude and natgas. Gold, copper, and bitcoin though all fell (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was -0.6%, the equal weighted S&P 500 index (SPXEW) -1.1%, Nasdaq Composite -0.3% (and the top 100 Nasdaq stocks (NDX) -0.3%), the SOXX semiconductor index -1.2%, and the Russell 2000 (RUT) -1.9%.

Morningstar style box almost all red today with large cap growth the only style escaping outperforming for a second day.

Market commentary:

As of now, “macro expectations have not materially repriced,” said Francisco Simón, European head of strategy at Santander Asset Management. “The risk scenario would be a combination of higher energy prices and a visible slowdown in activity, which would complicate the policy outlook and weigh on risk assets.”

“If it is blocked for more than a week, the risk of sustained high energy prices would become real,” said Roberto Scholtes, head of strategy at Singular Bank. “If it is resolved quickly, the economic and financial impact would likely be negligible.”

“Things are changing around the edges. We have a geopolitical shock, obviously, and we’re still parsing that in terms of how it could impact the risk premium for equities,” said Bank of America Securities head of U.S. equity and quantitative strategy Savita Subramanian on CNBC’s “Closing Bell: Overtime.” “But beyond that, I think what we’re seeing is the tide slowly going out for some of the beneficiaries of a very low interest rate environment,” she added.

“The dual headwind of higher oil and higher yields has pressured stocks today,” said Ryan Detrick, chief market strategist at the Carson Group, adding that markets were “back to more confusion and uncertainty.”

Still, he cautioned that the U.S. economy looks resilient, and manufacturing and services data appear to be perking up. “Things aren’t perfect, but there are some positives out there,” Detrick said.

Assuming the conflict is resolved over the coming weeks, the spike in oil will likely prove transitory, with Brent trading back down to the forward curve strip price of around $65, according to Chris Senyek at Wolfe Research.

“If the equilibrium for oil settles in higher, there is clearly still upward pressure on the 10-year yield,” he said.

Higher oil prices raise the risk of another breakdown in stock-bond correlations, but bonds can still diversify equity risk, according to Morgan Stanley strategists including Serena Tang. “If a sustained oil shock could push growth lower and inflation higher, we may see a repeat of the 2021–2023 environment when stocks and bonds sold off together,” they said. Whether short- or long-duration bonds provide better diversification depends on whether inflation risks or growth concerns dominate going forward, the strategists concluded.

A jump in U.S. crude oil prices to above $100 could yield a global recession as the U.S.-Iran war continues, according to Dan Niles, founder and portfolio manager at Niles Investment Management. To be sure, Niles does not believe that will be the likely scenario, as he expects the war to last a month. “What we’re all trying to figure out is, is this a short war? Meaning less than a month, or is it sort of medium term, which is a bigger problem, or does it last for a long time, in which case, I’m talking oil above $100, at which point you’re probably gonna end up with a global recession,” Niles said Thursday on CNBC’s “Power Lunch.”

With increasing uncertainty surrounding the conflict, Sam Stovall of CFRA Research said that investors are now wondering if the U.S. bit off more than it can chew. “Can [President Donald] Trump really escort all of the vessels through the [Strait of Hormuz]?” the chief investment strategist remarked. “What kind of liability are we going to be putting on ourselves, and how would that affect our debt levels? Investors are basically saying that whatever is happening now is not good.”

“Stocks are likely to sell off hard again before the weekend. Extended disruption to the Strait of Hormuz will trigger an energy shock to much of the world, and just help us assess relative vulnerabilities. If shipping doesn’t restart in earnest soon, the incentives to reduce equity exposure will build into Friday’s close.” — Mark Cudmore,

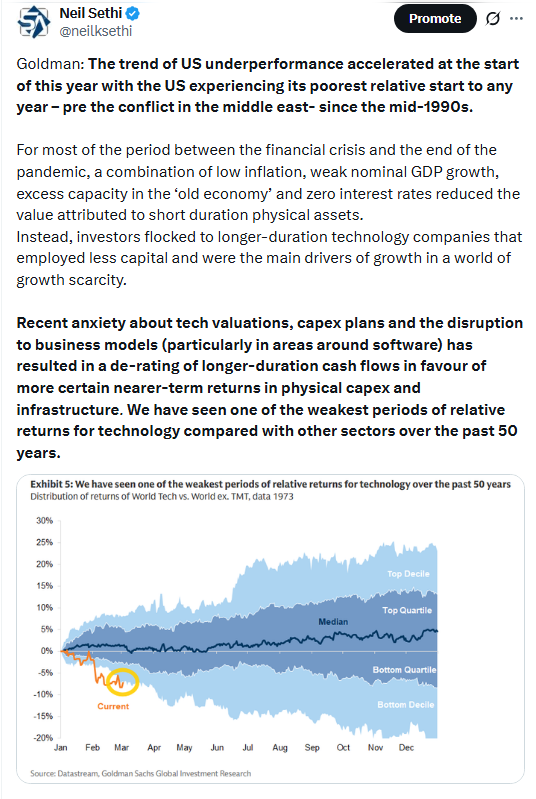

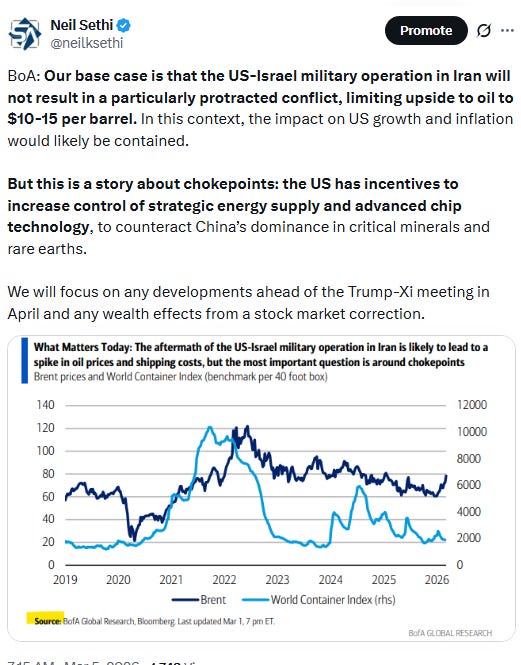

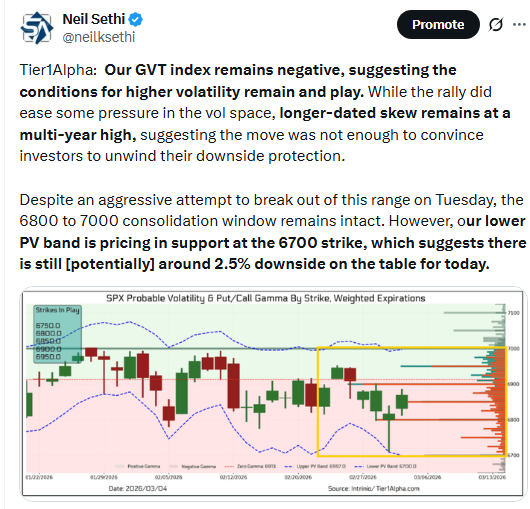

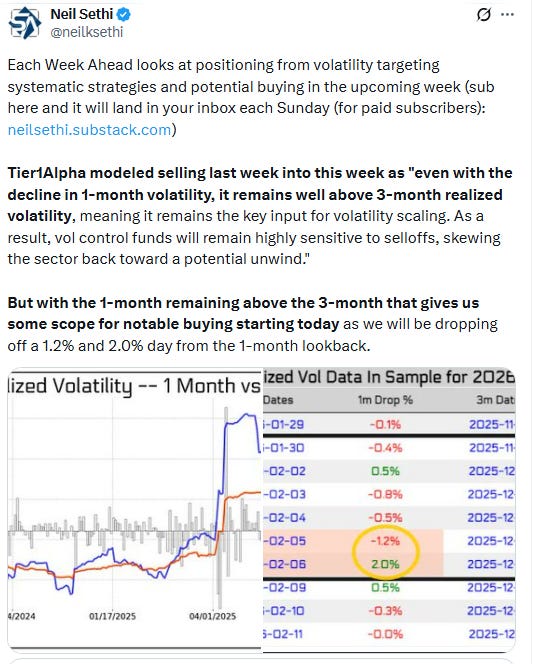

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

In individual stock action:

Berkshire Hathaway was a bright spot in the trading day, gaining more than 2% after the conglomerate disclosed that it started repurchasing its own shares again for the first time since 2024. CEO Greg Abel also bought $15 million worth of stock himself.

A key gauge of semiconductor firms dropped 1.2% as Bloomberg News reported the US is considering requiring permits for artificial-intelligence chip sales.

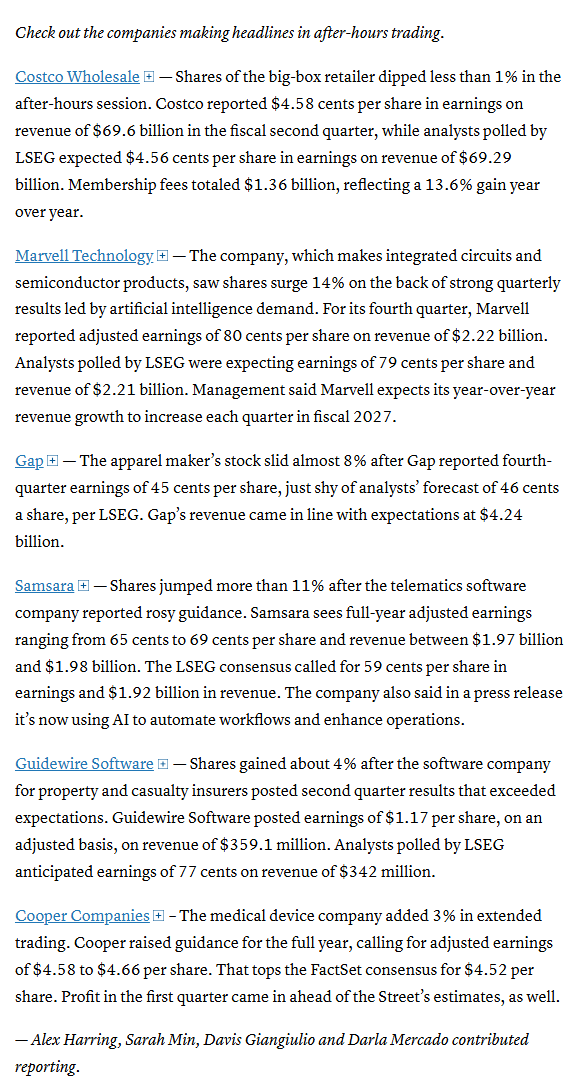

Companies making the biggest moves after-hours from CNBC:

Corporate news from BBG:

Oracle Corp. is planning to ax thousands of jobs, among its moves to handle a cash crunch from a massive AI data center expansion effort.

Broadcom Inc. Chief Executive Officer Hock Tan said the company expects its AI chip sales to top $100 billion next year.

Morgan Stanley is eliminating about 3% of its global workforce, targeting employees in its investment-banking and trading businesses as well as the wealth and asset-management operations.

Berkshire Hathaway Inc. CEO Greg Abel said he will use all of his take-home pay to acquire the conglomerate’s stock for as long as he’s in the role.

Baker Hughes Co. priced $10 billion of dollar and euro bonds to help fund its acquisition of Chart Industries Inc.

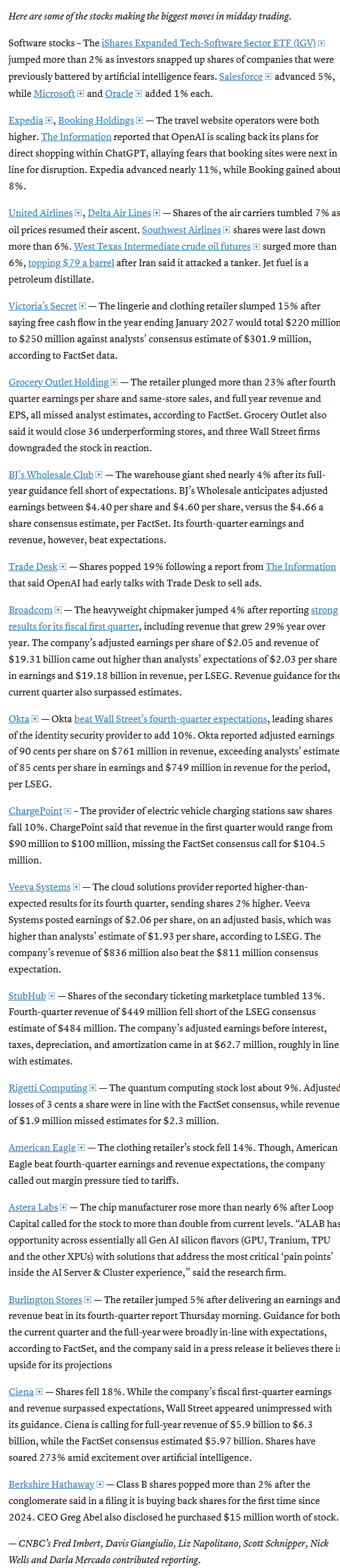

Mid-day movers from CNBC:

In US economic data:

Substack articles.

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X