Markets Update - 4/1/26

Update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with charts!

To subscribe to these summaries, click below!

To invite others to check it out (sharing is caring!), here’s the button:

Link to posts on X - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog.

Also, if you see an error (a chart or text wasn’t updated, etc.), always appreciate a note in the comments section or email so I can fix it.

In that regard, I do make mistakes sometimes, and usually I catch them at some point and correct them, and/or I sometimes add new material, so it’s always safest to read from the website where it will have any updates.

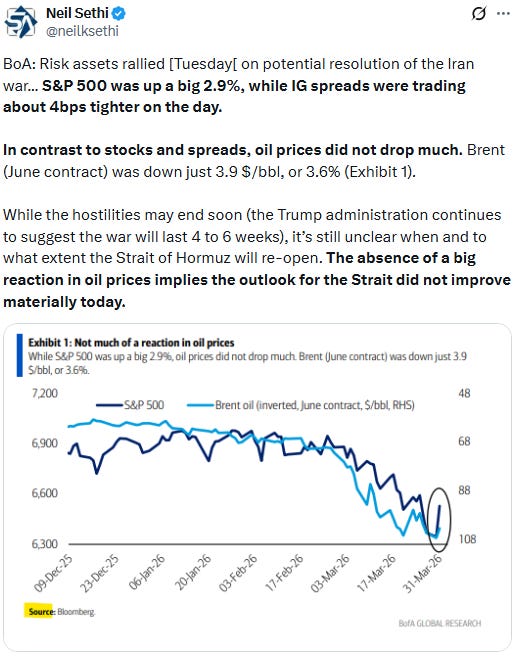

US equity indices opened trading Wednesday solidly higher with tech shares again leading gains following the updates in last night’s Markets Update including President Trump saying last night the U.S. would leave Iran in “two or three weeks,“ and that “[w]e’ll leave whether we have a deal or not. It’s irrelevant,” he said. That was followed this morning though with a social media post where the President signaled that perhaps opening the Strait is a requirement to end the conflict: “Iran’s New Regime President, much less Radicalized and far more intelligent than his predecessors, has just asked the United States of America for a CEASEFIRE! We will consider when Hormuz Strait is open, free, and clear. Until then, we are blasting Iran into oblivion or, as they say, back to the Stone Ages!!!” Perhaps we’ll learn more after his address tonight discussed in the Day Ahead portion below.

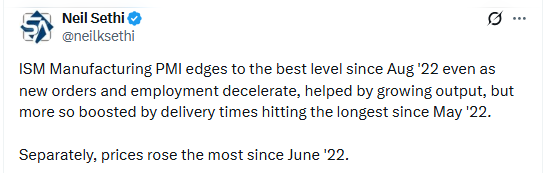

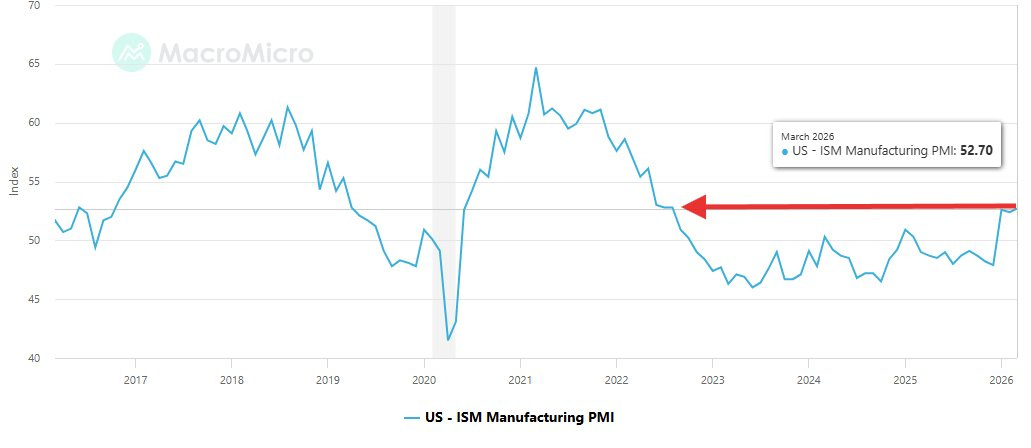

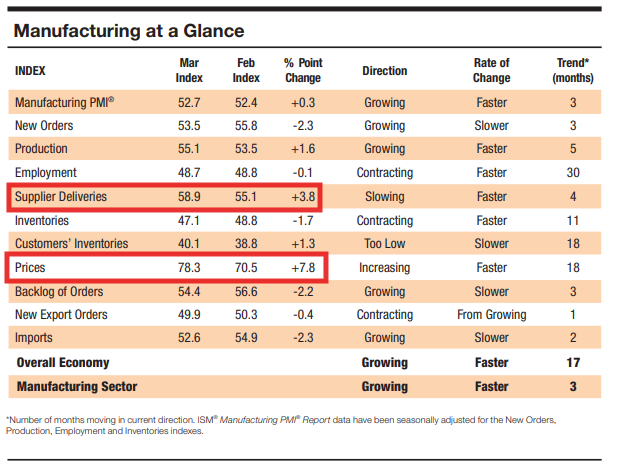

Also this morning, we got the ADP employment report for March which came in slightly better than expected, led by outsized job growth in the smallest (under 20 employee) businesses, February retail sales, which also came in slightly better than expected with broad spending growth, and ISM manufacturing services PMI which was the strongest since 2022 but on the back of a jump in delivery times to the longest since then (and input prices were the highest since then as well).

Indices would rise all morning before topping out at 1pm ET. From there though they fell back to around opening levels. They would again make some overall upward progress into the close before a quick burst of selling the last half hour. All though finished solidly in the green led again by the Nasdaq +1.2%. SPX was +0.7%, Russell 2000 +0.6%. DJIA +0.5%.

Elsewhere, bond yields were little changed, but crude prices fell back for a second session as did the dollar and US natural gas. Gold, copper, and bitcoin all rose again (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was +0.7%, the equal weighted S&P 500 index (SPXEW) +0.3%, Nasdaq Composite +1.7% (and the top 100 Nasdaq stocks (NDX) +1.2%, the SOXX semiconductor index +2.8% (up 9% the last two sessions), and the Russell 2000 (RUT) +0.6%.

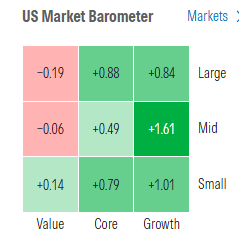

Morningstar style box not as strong Wednesday led again by growth.

Market commentary:

“We are seeing a relief rally, and with more information we may see a reversal, so we just need to be careful here,” Remi Olu-Pitan, multi-asset growth and income head at Schroders, told Bloomberg TV. “There’s still a lot of volatility, the market is still fragile.”

“The violent recovery in the last two days could be either the smart money betting on de-escalation in the Middle East, or it could be a touch of desperation driving fear of missing out on a recovery,” said Michael Bailey, director of research at wealth management firm FBB Capital Partners. However, “any mixed or bad news at these higher levels could drive markets back down.”

“This is an oversold rally that was sparked by some news and some optimism,” deGraaf said Wednesday on CNBC’s “Money Movers.” “But there’s more to do.”

The S&P 500’s back-to-back rally is a positive development for the market, but it was “quite oversold” after a five-week decline, said Ryan Detrick, chief market strategist at Carson Group. “A bounce was due and we are getting it,” Detrick told MarketWatch. But are the lows in? It still comes down to if and when the Strait of Hormuz will reopen. “That is what the market needs to see,” he said.

“The sharp rally in stocks over the past 24 hours demonstrates how a resolution to the conflict, or hopes thereof, may quickly drive markets higher,” said Ulrike Hoffmann-Burchardi at UBS Global Wealth Management. “We continue to believe global stock markets will end the year higher than they are today.”

“A combination of euphoria, exuberance, and relief has driven a considerable rebound in risk appetite over the last day or so, as hopes grow for a swift end to conflict in the Middle East,” said Michael Brown, a senior research strategist at Pepperstone Group Ltd., in a note to investors. Markets are concluding that “no war is a much better scenario for the global economy than a continued conflict.”

“The market is kind of just sniffing out that there’s probably some type of resolution in the next couple of weeks,” said Patrick Ryan, chief investment strategist and head of multi-asset solutions at Madison Investments. However, the market may not be out of the woods yet. According to Ryan, unless there’s “some type of all-clear announcement,” trading should “remain volatile” in the short term.

“The correlation between Brent oil prices and global equity markets has been exceptionally strong since the conflict started,” said Wolf von Rotberg, equity strategist at Bank J Safra Sarasin. “This goes to show that a return to previous equity market highs would need the Strait of Hormuz to reopen and oil prices to drop significantly. It is probably too early for an all-clear yet.”

“I would expect further volatility in the days to come and the market to oscillate between losses and gains for a few more sessions until we get clarity on how the crisis unfolds,” said Alexandre Baradez, chief market analyst at IG Markets. “This is likely more a temporary respite than a final game changer.”

“Investors have been counting on a swift off-ramp to war essentially since it began, but I think from a market or global economy perspective it’s important to define what the true clearing event to revisit risk and take down recession odds really is,” wrote JPMorgan industrials sector specialist sales Paige Hanson.

“The market has been pricing in the worst-case scenario when it comes to the war in Iran, that anytime you see any type of de-escalation news, the market really wants to run with that,” said Clayton Allison, portfolio manager at Prime Capital Financial. “On the flip side, we haven’t really seen any actual progress there,” he told MarketWatch in a phone interview. “I’m hearing a lot more from United States’ side of things than Iran. It seems like Iran has been very steadfast in not even coming to the negotiating table.”

“The sea of green in stocks is a classic sign of markets starved for good news latching onto a sliver of hope, but traders need to look at crude prices — not headlines — as a true barometer of what the global economy is up against.”

— Ven Ram, macro strategist.

“I’m sort of leaning towards the oil is telling the truth of the situation. I think a lot of what happened here — oversold, for sure — but I got to think a lot of this is window dressing. We are at the end of a really difficult quarter, and so that’ll help a little bit, but I don’t know that that’s something that has follow-through,” Karen Finerman, co-founder and CEO of Metropolitan Capital Advisors said on CNBC’s “Fast Money” on Tuesday afternoon.

“Each passing week increases the global economic costs of the Iran conflict,” wrote Tiffany Wilding, economist at Pacific Investment Management Co. At some point, “the economic effects of persistent disruptions will start to build, with recessionary implications for the global economy.”

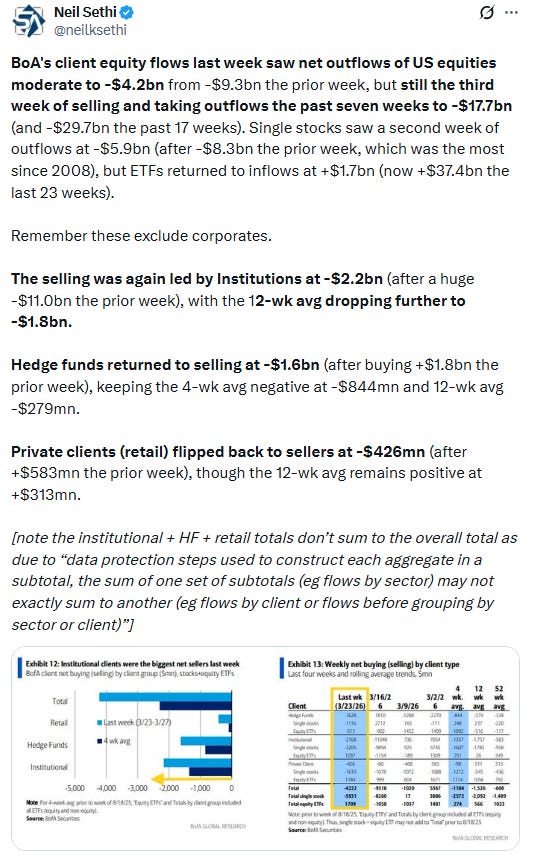

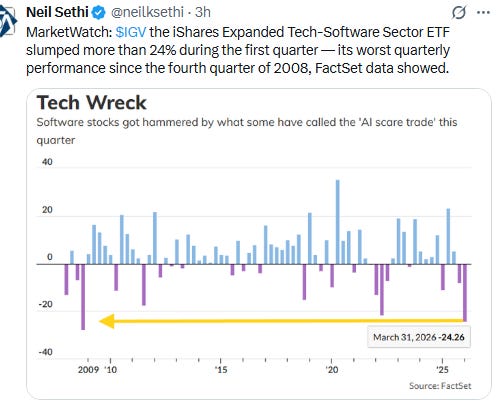

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

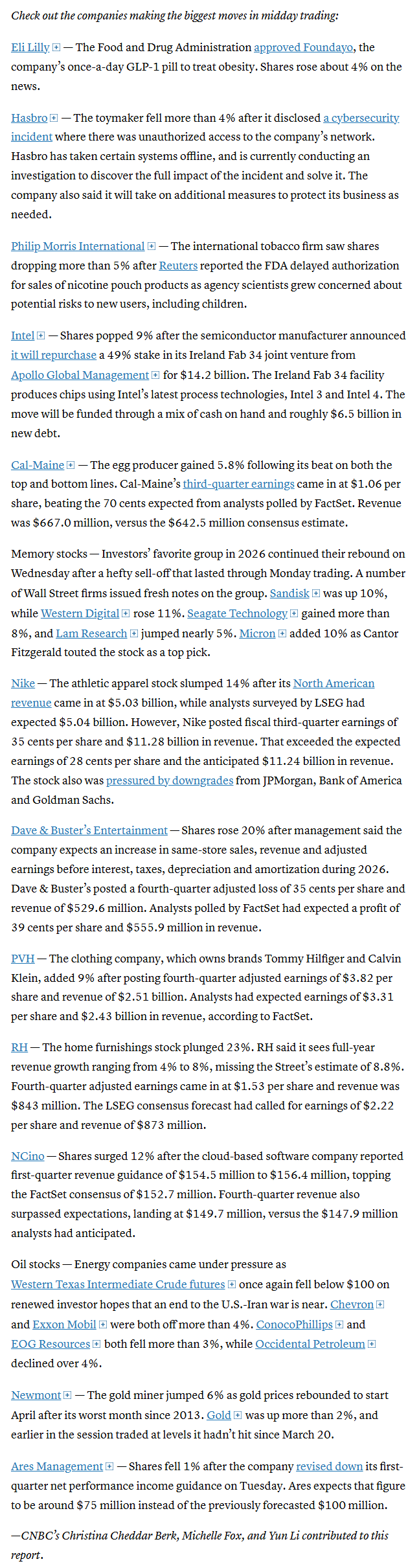

In individual stock action:

US travel, mining and technology stocks rose, with Sandisk Corp. up around 9%. Miners including AngloGold Ashanti Plc and Newmont Corp. climbed as gold advanced for a fourth day. At the same time, Nike Inc. plunged more than 15% after a gloomy outlook, while energy shares were weaker.

Corporate news from BBG:

Eli Lilly & Co.’s weight-loss pill won US approval, ratcheting up pressure on Novo Nordisk A/S, which launched an obesity pill earlier this year.

OpenAI has completed a deal to raise $122 billion from investors at an $852 billion valuation, marking the company’s largest funding round to date.

Microsoft Corp. is in exclusive talks with Chevron Corp. and investment fund Engine No. 1 over a long-term deal that would underpin a giant energy complex in West Texas.

SpaceX has filed confidentially for an initial public offering, according to people familiar with the matter, bringing billionaire Elon Musk’s rocket, satellite and AI company closer to delivering the biggest-ever listing.

Mid-day movers from CNBC:

In US economic data:

Substack articles

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X