Markets Update - 5/14/26

A detailed look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for tomorrow.

Quick Summary:

US equity indices started the day with modest gains following a mostly as-expected April retail sales report showing solid consumer spending (if slowing from March’s torrid advance) with GDP component control group sales up 5.7% from a year earlier. As a result of that, and another report showing larger than expected growth in inventories, second quarter GDP estimates were boosted (more details in subscriber section).

In other US economic data, weekly unemployment claims rose more than expected but remained subdued historically while import prices completed a trio of hotter than expected inflation reports this week, rising the most on a monthly basis since March 2022, boosted by both food and energy prices but also a wide swath of other goods led by semiconductors and electrical equipment which jumped the most on record on the back of the booming AI trade (report coming tomorrow morning).

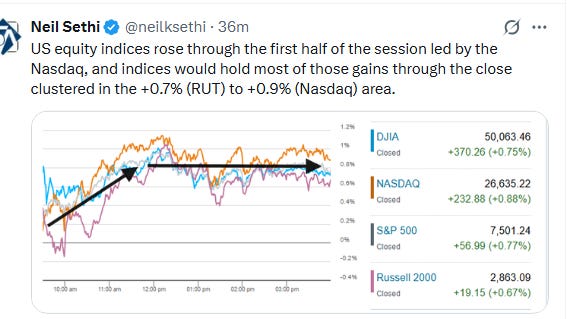

While the Nasdaq started the session little changed as noted in the morning update, it would take the lead after the first hour boosted by a 12% jump in the shares of Cisco following the strong report detailed last night and heavyweight Nvidia advancing over 4% (its 7th straight advance, up 20% over that time the best 7-day stretch since August 2024) following yet another announcement that it would be permitted to sell its H200 chip to Chinese firms (I guess if it keeps working?).

Adding to the upbeat mood was the IPO of chipmaker Cerebras Systems Inc., which soared nearly 70% despite an upsized offering price. It’s the year’s biggest initial public offering and gives the company a market value of roughly $69 billion (more in subscriber section).

As also detailed this morning, US leaders wrapped up their meetings with Chinese counterparts (see international section in particular) with President Trump extending an invitation for President Xi to visit the US in September. US Trump also signaled China is willing to support negotiations with Iran, as he pushes for a diplomatic resolution to end the war and reopen the Strait of Hormuz which kept oil prices contained.

Elsewhere, crude prices and bond yields would edge higher reversing from early losses while the dollar would continue its breakout. Bitcoin and US natural gas futures were also higher, while copper futures would fall back from all-time highs. Gold would also end lower (all covered in the subscriber section).

The market-cap weighted S&P 500 (SPX) was +0.8%, the equal weighted S&P 500 index (SPXEW) +0.4%, Nasdaq Composite +0.9% (and the top 100 Nasdaq stocks NDX) +0.7%, the SOX semiconductor index +0.4%, and the Russell 2000 (RUT) +0.7%.

Some market commentary:

“April retail sales echoed what we’ve heard across corporate conference calls for weeks now: The US consumer remains resilient despite soaring gas prices,” said Bret Kenwell at eToro. “When it comes to stocks though, tech is in the driver’s seat right now, not the consumer.”

“A resilient consumer is good news for the economy, but oil remains the focal point,” Kenwell noted. “That’s not just because of its impact on inflation, but because of what it could mean for consumer spending.”Stock-market gains on Thursday were mostly driven by April retail-sales data that showed sales at U.S. retailers rose for the third month in a row, according to Thomas Hainlin, national investment strategist at U.S. Bank Asset Management Group. “We’ve seen consumers, now two months into the [Iran] conflict, still able to absorb higher gasoline prices and spend money on discretionary items,” Hainlin said in a phone interview. “Consumer spending and business investment are the big drivers for earnings growth this year, and results have come in to support that,” he added.

“Amicable discussions between Washington and Beijing are easing concerns around tariffs, potential AI restrictions and China’s support for Tehran, while also giving investors more confidence in President Trump’s ability to manage foreign-policy challenges,” José Torres, senior economist at Interactive Brokers wrote in a Thursday note.

“The stock market is trading at record highs and as earnings have easily cleared expectations, it’s clear that Corporate America has become very skilled at adapting to a wide range of economic environments,” said Clark Bellin at Bellwether Wealth.

“Stocks are still climbing the wall of worry and we don’t think there is euphoria in markets just yet, and in fact, there is still plenty of skepticism which suggests this bull market has more room to run,” he said.“This has been, for the most part, a tech-driven long, long, long bull market … This growth is because of expected earnings. It’s not really a speculative bubble,” the Creative Planning CEO said on CNBC’s “Power Lunch” on Wednesday afternoon. “I think the chipmakers are actually undervalued as a group, because that’s a mega trend … It seems like we’ve got so much demand ahead of the supply trying to meet it that it’s got a lot of room to run.”

When there’s uncertainty, the best defense remains a strong offense of fundamentally superior stocks, according to veteran Wall Street strategist Louis Navellier. Since the order backlogs are growing for data center and AI-related shares, the earnings in the upcoming quarter are now forecast to be potentially even stronger, he said.

“Beneath the surface of the popular averages, a fragile and contradictory macro environment exists,” analyst Craig Johnson at Piper Sandler wrote in a Wednesday note. “Twenty six-week new highs across our group work is primarily technology, with emerging signs of advance-decline lines diverging.”

The recent rally in the market is not necessarily in good shape, according to Jonathan Krinsky, chief market technician at BTIG. “The divergences and dispersion are only growing. Cyclical parts of the economy are clearly responding to higher rates and energy prices,” he said, noting that money is continuing to flow into artificial intelligence-related stocks as opposed to those like homebuilders and retailers. “At some point the music stops and we see meaningful reversion,” he also said. “While calling the exact turn remains difficult, we think we are quite close.”