Markets Update - 5/18/26

A detailed look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for tomorrow.

Quick Summary:

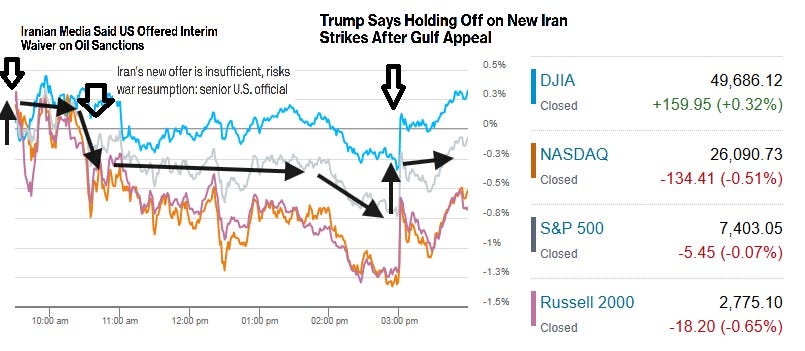

US equity indices would spend Monday pushed and pulled by Iran headlines. They would start the day higher on reports (from Iran) of US acceptance of Iran’s demand for an interim waiver on oil sanctions as detailed in the morning update, then fall after an Axios report that the US had rejected Iran’s latest offer saying it lacked meaningful improvement, before jumping at 3pm ET on President Trump posting on Truth Social that he was pausing a (previously undisclosed) planned Tuesday attack (more below). Still just the Dow Jones Industrial Average finished higher +0.3%, while the small-cap Russell 2000 would lead to the downside -0.7%, followed by the Nasdaq -0.5%, and S&P 500 -0.1%.

Equities were also under pressure from bond yields and crude prices climbing further although the moves were much less dramatic than Friday. Still the 30-year US Treasury would close at a yield of 5.15%, another post-2007 high, while the benchmark 10-yr yield would close at 4.62% the highest since February 2025 (more details in subscriber section).

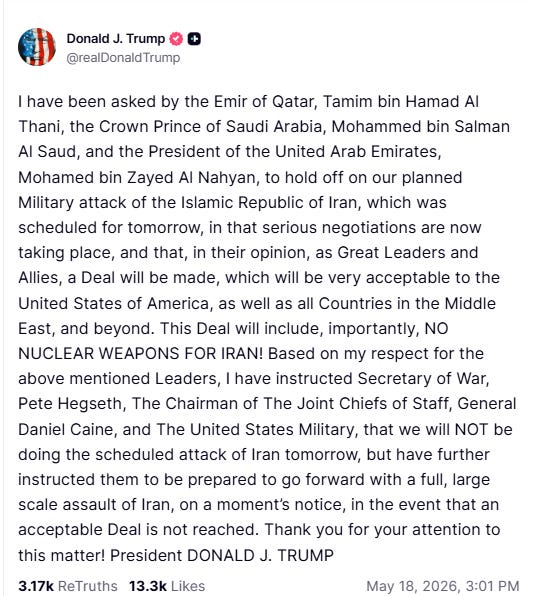

Pres Trump said in a social media post that an attack on Iran was "scheduled for tomorrow," but has been paused at the request of mid-East leaders "in that serious negotiations are now taking place, and that, in their opinion...a Deal will be made, which will be will be very acceptable to the United States of America, as well as all Countries in the Middle East, and beyond. This Deal will include, importantly, NO NUCLEAR WEAPONS FOR IRAN!" [full post below].

As noted in the Week Ahead, this week is light for US economic data. Monday brought us just the National Association of Home Builders (NAHB) Housing Market (new home) Index which rebounded slightly from April’s 7-month low but remained well below the 50 dividing line between poor and good conditions for a 25th consecutive month.

While the S&P 500 was dragged lower by some weakness in many of the largest Tech stocks (details in subscriber section), overall 7 of 11 sectors would advance seeing the equal-weighted version of the index (where every stock has the same weighting) finish +0.6%.

Elsewhere, the dollar would fall back as would bitcoin, but copper and US natural gas futures would advance. Gold was little changed (all covered in the subscriber section).

The market-cap weighted S&P 500 (SPX) was -0.1%, the equal weighted S&P 500 index (SPXEW) +0.6%, Nasdaq Composite -0.5% (and the top 100 Nasdaq stocks NDX) -0.5%, the SOX semiconductor index -2.5% (after -4% Friday, worst two sessions since October), and the Russell 2000 (RUT) -0.7%.

Some market commentary:

“The fact we have broken this psychological 4.5% on the 10-year, it becomes dangerous, not just for the bond market but also the broader risk complex,” Priya Misra, a portfolio manager at JPMorgan Asset Management, told Bloomberg Television. “As you see tightening in financial conditions, the market starts to move from, ‘Is this just inflationary?’ to ‘Is this stagflationary?’”

“Rather than drawing in value buyers, 5% yields on the long bond are only emboldening bond bears and reviving the vigilante mindset.” — Mark Cranfield, Markets Live Strategist

“While equities are seeing life through rose‑tinted glasses, rates continue to rise,” said Benoît Peloille, chief investment officer at Natixis Wealth Management. He warned that a “reality check” could follow if yields keep climbing.

Long-term interest rates “sit at the crossroads of the cost of capital for AI capex and private credit,” said Kevin Thozet, from the investment committee at Carmignac. They affect the financing of government deficits and he noted their potentially “adverse impact” on consumer wealth.

“We suspect that it is becoming increasingly clear that disruption from the Iran War is here to stay,” said George Moran, European macro strategist at RBC Capital Markets. “Higher rates for longer is likely heightening fiscal concerns, particularly if markets begin to expect more fiscal intervention.”

“The volatility will clearly continue until the Iran situation is resolved,” said veteran Wall Street strategist Louis Navellier. “If in a month from now, flows haven’t resumed through the Strait of Hormuz, energy prices will almost certainly be higher, fueling higher inflation and higher interest rates.”

“Mixed messages are being sent surrounding the conflict with Iran, with the fragile ceasefire in place but negotiations stalled,” said Mark Hackett at Nationwide. “The market’s next ‘all clear’ likely depends on three things, including calmer oil and bond markets, broader participation beyond a handful of megacap winners and evidence that wage growth continues to outpace inflation.”

“We expect bonds and commodities to continue to price in these risks most rapidly,” Emma Moriarty, portfolio manager at CG Asset Management said. “The longer this persists, the more likely higher interest rates and energy prices start to have a more sustained impact on corporate profits. This is particularly an issue given elevated equity valuations.”

“Each of these primary asset classes is telling a consistent story, but they are not all telling the same story,” said Gene Goldman, chief investment officer at Cetera Financial Group. “Either equity valuations contract or the bond market has to rethink just how restrictive Fed policy needs to be.”

“If earnings were to hit an air pocket, a lot more investors would consider selling equities, since it’s the bedrock of their investment thesis,” said Sameer Samana, head of global equities and real assets, Wells Fargo Investment Institute.

“Bonds were more nervous about the inflation picture and the equity market was comforted and encouraged by the very strong earnings and AI-led optimism,” said Willem Sels, global chief investment officer at HSBC Private Bank. “What you now have is a bit of a catch-up movement in the equity market, a bit of an exhaustion of the momentum.”

“The S&P 500 is trading at 27.1x earnings and the Equal Weight is at a 32% discount at 18.4x earnings,” JonesTrading’s Mike O’Rourke wrote, adding that when the valuation discrepancy “becomes this stretched, investors seeking to take profits and reduce risk while staying invested typically rotate from the S&P 500 into the Equal Weight index.

“Oil prices and the bond market move are pricing in short-term supply shortages and thus stickier inflation, three to six months,” said Steve Chiavarone, deputy CIO of equities at Federated Hermes. “AI stocks are pricing in higher productivity and a disinflationary environment over a more medium-term time frame, one to three years.”

“We continue to see opportunities in some of the hyperscalers, which have led the AI build-out and are now beginning to generate tangible returns on their investments,” said Raphael Thuin, head of capital market strategies at Tikehau in Paris.

“Tech is the only sector with strong secular demand, which ensures strong and predictable earnings,” said Marija Veitmane, head of equity research at State Street Global Markets. “All the money that is still fairly abundant in financial markets is finding its way to the tech sector, pushing those stocks higher — but nothing else.”

“So long as earnings keep accelerating, we’re not too concerned,” said Jeffrey Blazek, co-chief investment officer of multi-asset at Neuberger Berman Group. “The moves up have been matched by a step-up in earnings, and there’s no indication that’s weakening.”

”Hyperscalers have been raising their capex pretty consistently, and one day that will stabilize or reverse,” he said. “That’s when we could see a pretty big correction in the chip space.”“People underestimated how much capacity is needed for AI, and we’re still not there. There is astronomical need,” said Anna Rathbun, founder and chief executive officer at Grenadilla Advisory. “That means you can feel confident about the durability of the revenue growth, especially in the infrastructure space.”

“[The rise in yields] is less about marginal credibility, per se, and more a function of the outright contrasting headlines, with the administration asserting a fact only to have it contested shortly thereafter,” BMO’s Ian Lyngen remarked. “The resulting environment has lowered conviction and created a collective reluctance to establish positions based on the fundamentals when any such effort could immediately prove folly via Trump’s next [TruthSocial] post.”

“There’s truly inflationary problems,” Ben Fulton, CEO of WEBs Investments, said to CNBC, calling elevated oil prices a “watershed” issue. “It’s going to be hard to see that offset.” This means that stocks could be in a “heavy range trade” from here on out without positive developments out of the Middle East, especially regarding the Strait of Hormuz, he said. “I could see people starting to protect profits pretty quick,” Fulton added.

Risks are growing of an unwind in the powerful fund flows that drove US stocks to record highs in recent weeks, according to Citadel Securities’ Scott Rubner. “The near-term setup now warrants more tactical caution,” Rubner wrote. “Many of the flows that helped drive the rally now appear significantly more mature. Higher long-end rates are beginning to create competition for equities again.”