The Week Ahead - 5/17/26

A look at the upcoming week for the US economy and equities — covering key drivers including earnings, valuations, positioning, breadth sentiment, seasonality, and the Fed.

The Week Ahead

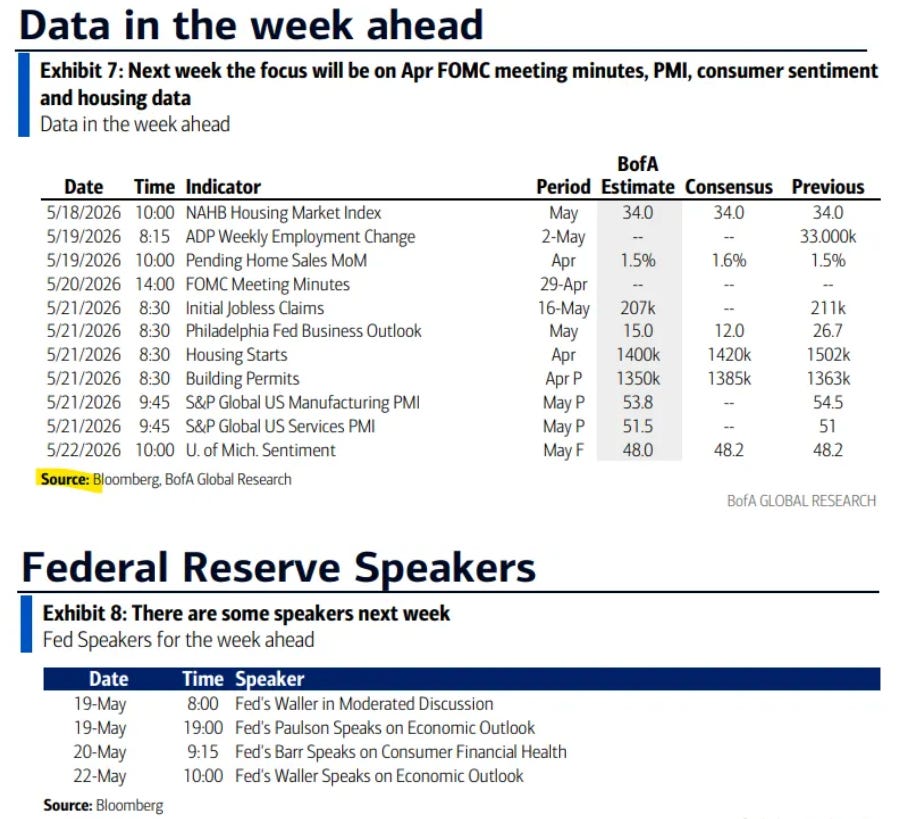

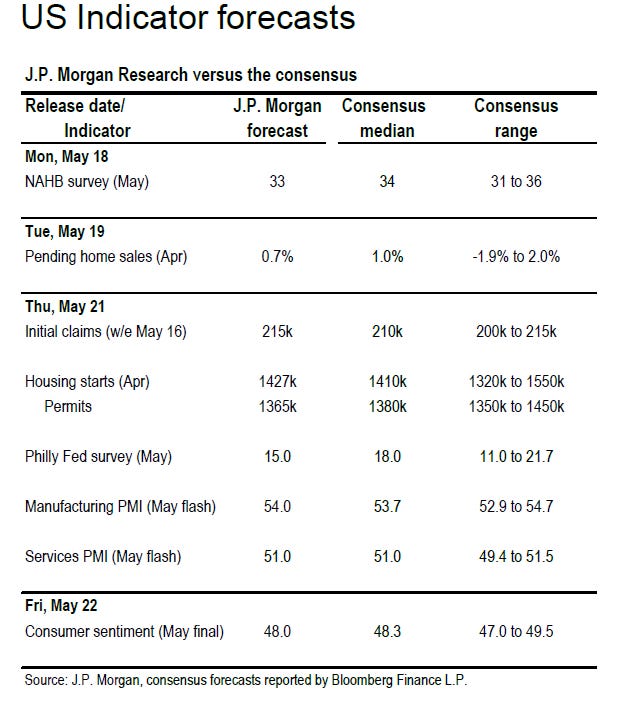

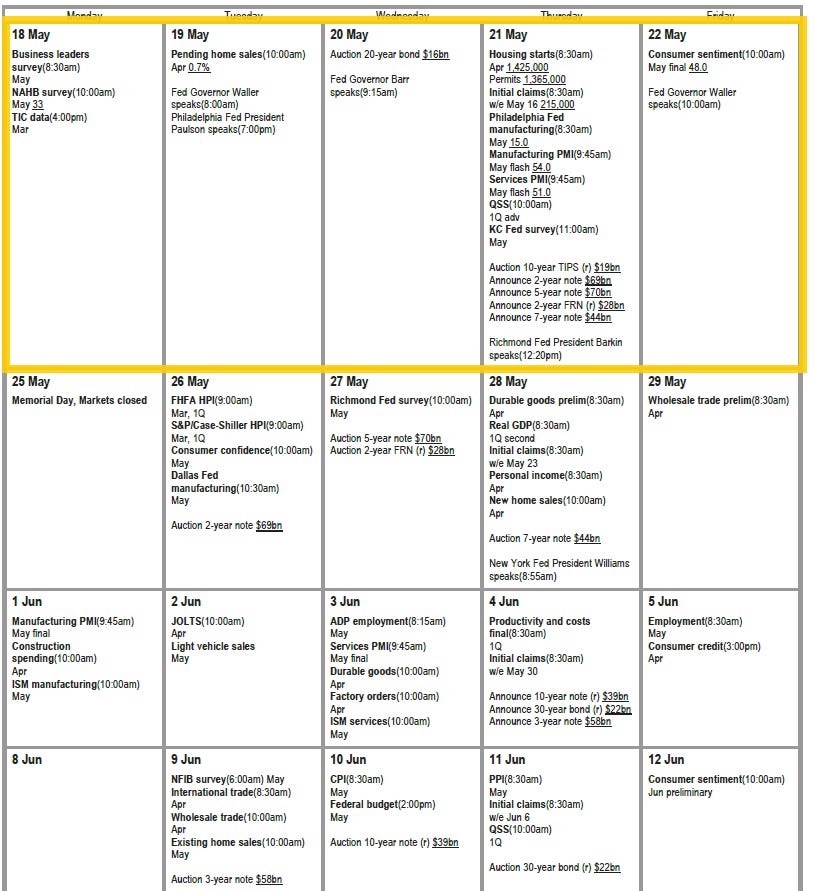

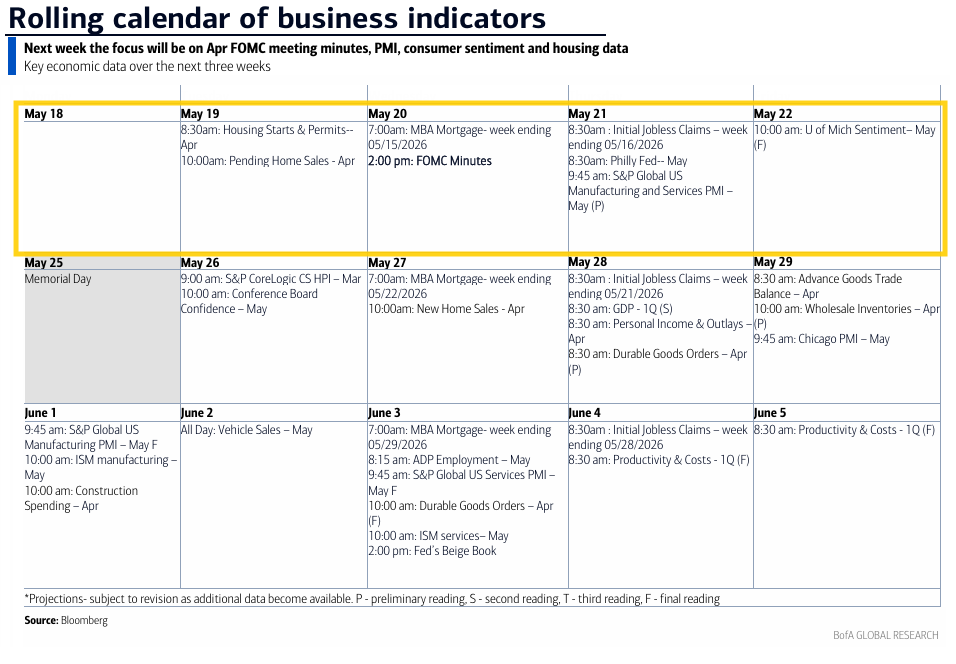

After three very heavy weeks US economic data eases back considerably in the upcoming week with no top-tier reports. We will get May flash PMIs, NAHB new housing market index, and UMich final sentiment, April housing starts/permits and pending home sales, plus the normal weekly reports (ADP, jobless claims, etc).

In terms of Fed speakers a lighter week as well with the schedule currently containing just Gov Waller twice (who will become an even more important voice with Jerome Powell stepping “into the background”) along with Gov Barr who was fairly hawkish this week, and Philadelphia Fed President Paulson (a 2026 FOMC voter and who is one of the more dovish so will be interesting to hear if she’s moving in the direction of the other presidents).

More importantly, we’ll get the minutes from the April meeting which will give us more context on where the collective head of the Fed is at as new Chair Warsh takes the helm.

In terms of non-Bill (>1yr in duration) US Treasury auctions next week we’ll get the 20-year (which will likely not be good given the jump in bond volatility and thin liquidity for this duration) and a 10-year TIPS reopening (nobody pays any attention to TIPS auctions).

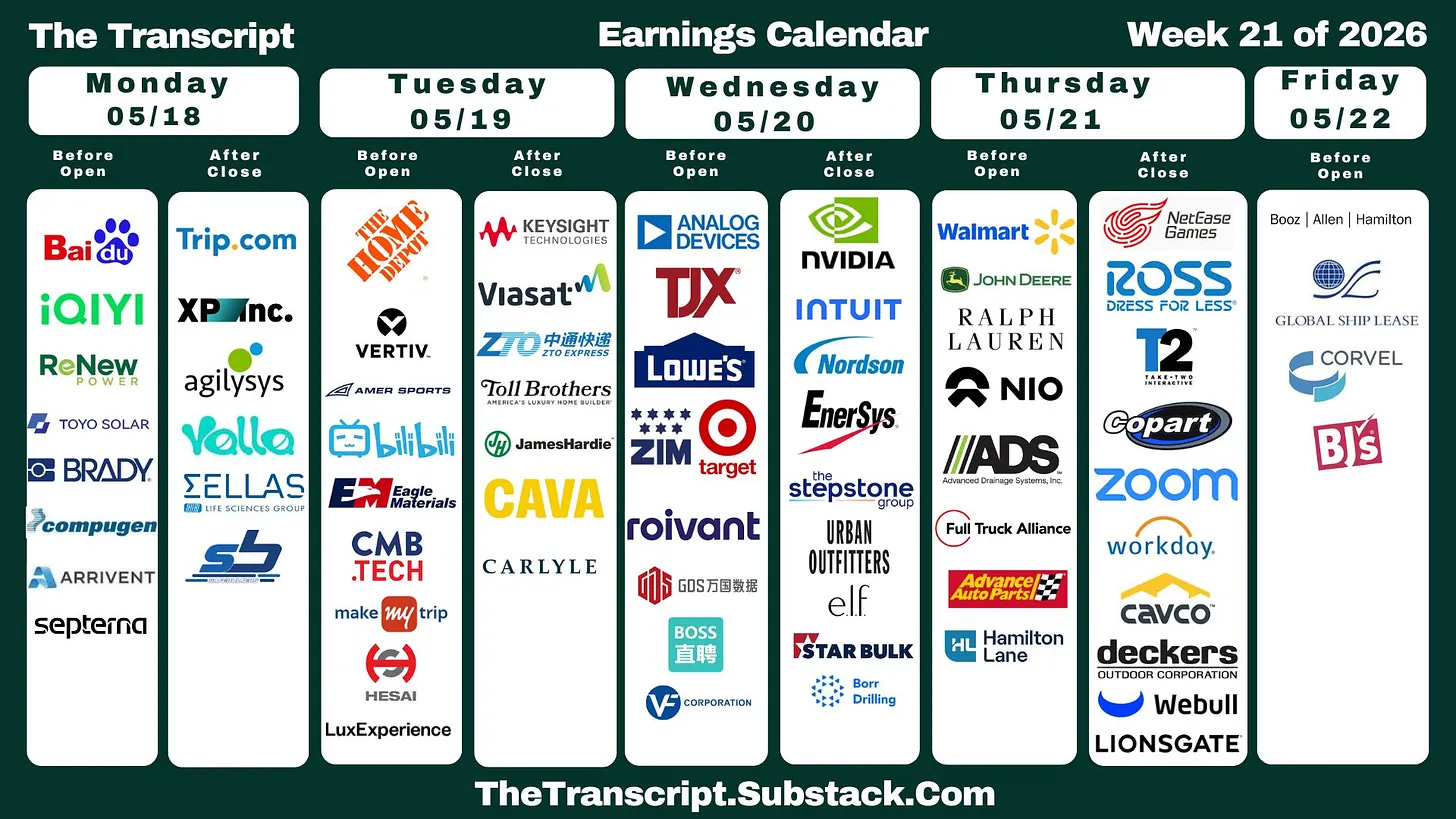

Q1 earnings season kicks back up in the upcoming week with two heavyweights in Nvidia and Walmart. They are part of 19 SPX components reporting according to wallstreetnumbers.com. Six others are also >$100 billion in market cap in HD, ADI, LOW, INTU, TJX, DE (in order of reporting date).

Note that a week from Monday is Labor Day in the US, so I would expect, especially given the above calendar, trading volumes to drop considerably post-Nvidia earnings and continue to slow as we approach the three-day weekend.

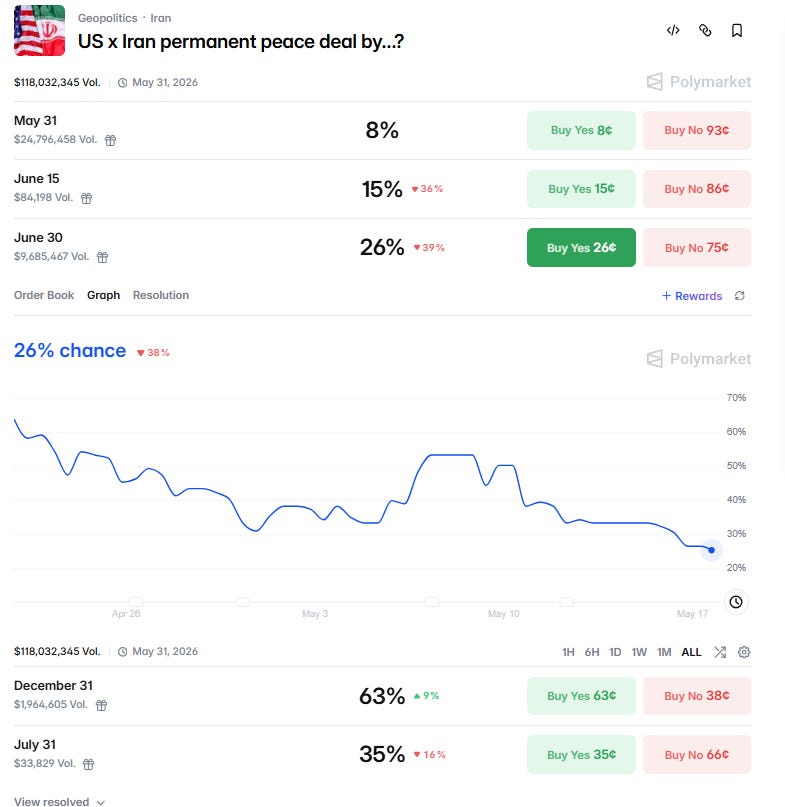

In terms of the Iran war, as I have been saying for a while, “it continues to drag on with no end in sight,” (as noted in the Friday update President Trump said he did not ask President Xi to intervene as many had hoped). As I have also said “It seems that both sides feel they have the upper hand, and both need a conclusion which allows them to claim ‘victory’. Not a setup conducive to a quick conclusion.” That said, there does appear to be back-and-forth continuing so a deal is not impossible, but FWIW Polymarket sees just a 26% chance of a permanent deal by the end of June, down from 50% a week ago. July is just 34%.

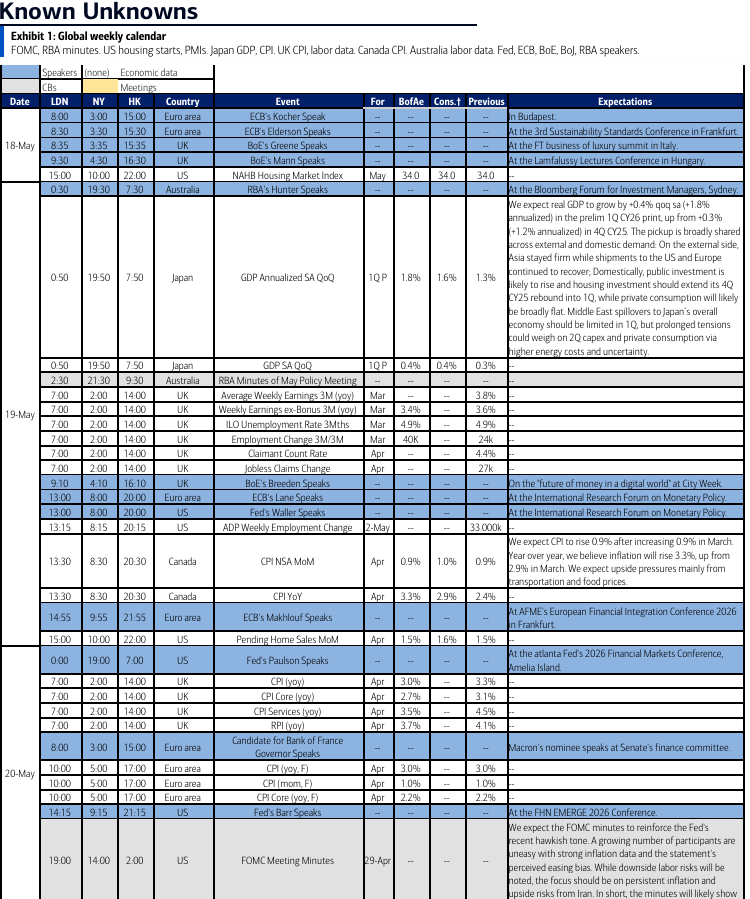

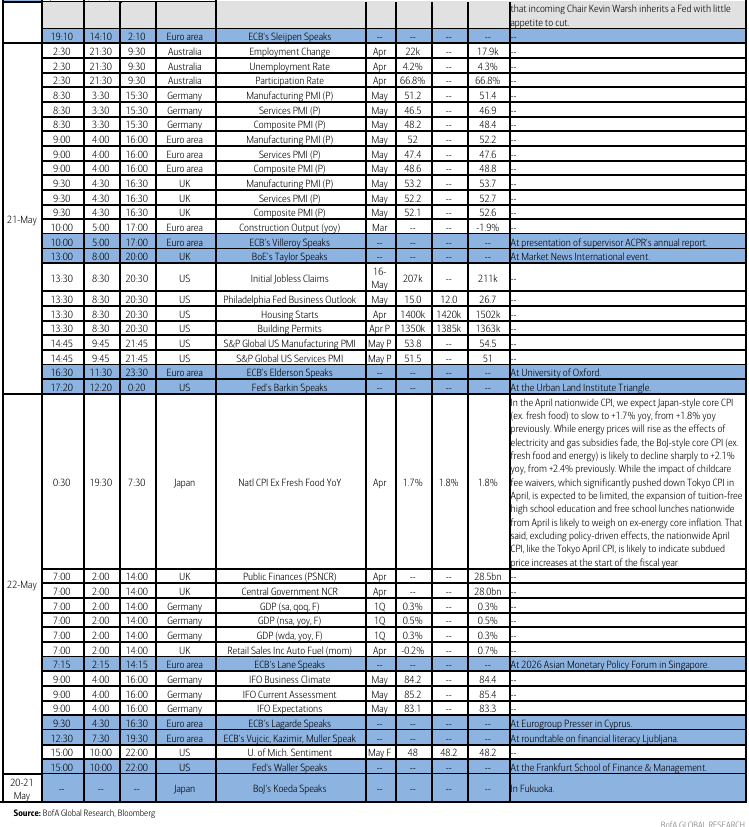

Ex-US highlights from DB:

In Europe, the highlights will include UK labour market (Tuesday) and inflation (Wednesday) reports. Our UK economist expects headline CPI to slow to 2.98% YoY and core CPI to drop to 2.61% YoY. There will also be the GfK’s May consumer confidence index and April retail sales for the country on Friday. Other notable releases in Europe will include consumer confidence in the Eurozone (Thursday), with the Ifo survey for Germany due Friday.

Over in Asia, a busy week is ahead in Japan, with key data including Q1 GDP(Tuesday) and April nationwide CPI on Friday. Our Chief Japan economist expects positive real growth of an annualised 1.3% QoQ for the GDP report and sees core CPI inflation ex. fresh food remaining at 1.8% YoY against a retreat in core-core ex. fresh food and energy to 2.2% (2.4% in March).

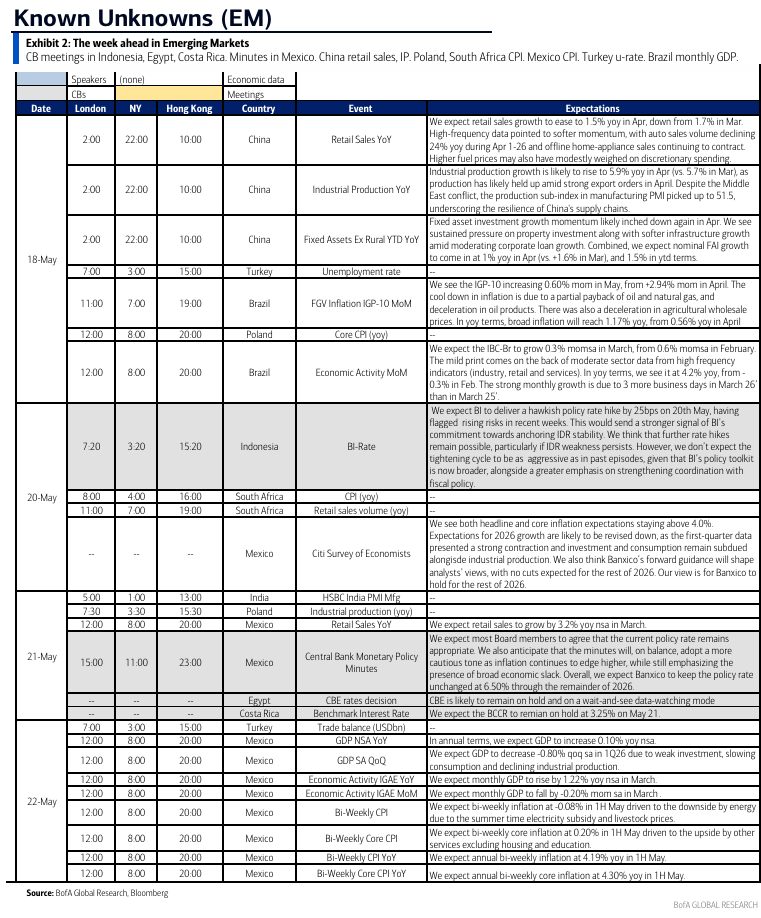

In China, our economists expect next week’s data to show sustained momentum in economic activity in April, with, industrial production up by 6.2% YoY (6.1% in Q1), investment climbing by 0.1ppt to 1.8% YoY YTD and retail sales growing by 1.9% YoY (1.7% in March). See

Here’s their one-pager:

And BoA’s cheat sheets:

Executive Summary

US equity indices last week vacillated between gains and losses pushed and pulled by the various headlines which ranged from a global surge in bond yields in part on the back of a trio of hotter than expected inflation reports in the US (covered in the subscriber section), to President Trump’s trip to China, to another showing of extraordinary strength from the AI sector not just in corporate earnings but also GDP estimates following a strong industrial production report.

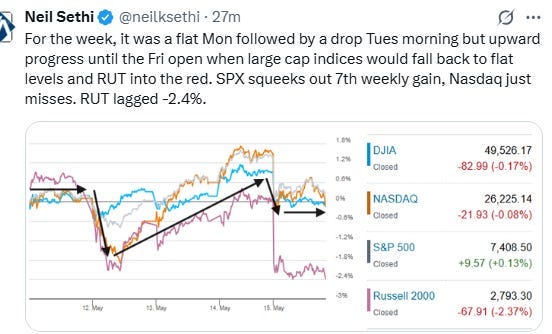

The end result was little headway for large capitalization indices (S&P 500 (SPX), Nasdaq, Dow Jones Industrial Average (DJIA)) which would end right around unchanged levels for the week, with the SPX eking out a modest gain (+0.1%) to keep alive its 7-week win streak (longest since 2023) while the Nasdaq and DJIA would finish just on the other side -0.1% and -0.2% respectively ending their respective six- and five-week streaks. The small-cap Russell 2000 (RUT) though, more sensitive to interest rates, saw its worst session since November on Friday and would finish the week down -2.4%.

In addition to the reports indicated above, we also received an update on consumer spending in the April retail sales report which came in stronger than expected when stripping out gasoline and auto sales. While boosted by prices, it still showed healthy growth even adjusted for inflation.

Companies continued to put the finishing touches on a Q1 earnings season which as noted in previous weeks has been exceptionally strong, especially for a quarter not coming out of an earnings trough. That has kept valuations stable at moderate levels even when equities lifted to new highs.

Positioning and sentiment continue to rebound and are starting to get to levels where even the more bullish are indicating limited near-term upside while downside risks have grown, even as few are expecting more than a modest consolidation. Breadth and the Fed continue to be less supportive as does the ongoing Iran situation, while seasonality is mixed, all as detailed in the subscriber section.