Markets Update - 5/19/26

A detailed look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for tomorrow.

Quick Summary:

US equity indices would start the Tuesday session in the red under continued pressure from rising oil prices and bond yields as well as weakness in some of the technology winners coming into the week as covered in the morning update.

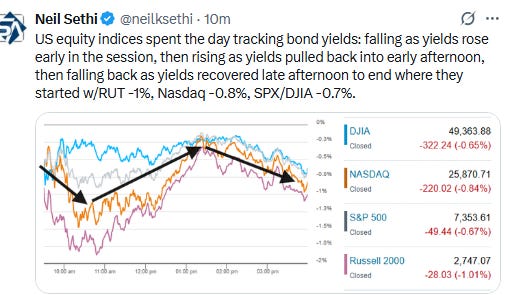

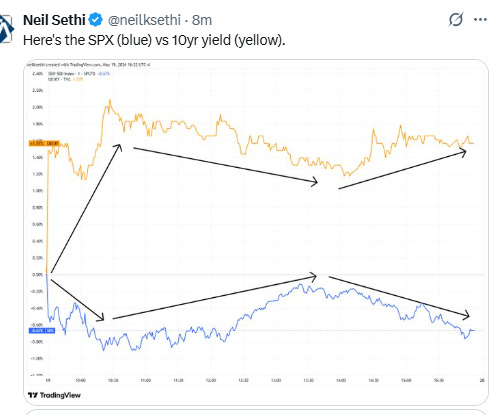

The equity indices would spend the day tracking bond yields: falling as yields rose early in the session (with the 30-year Treasury yield hitting the highest levels since 2007 while the 10-year would touch the highest levels since last January), then rising as yields pulled back into early afternoon, before falling back as yields recovered late afternoon to end where they started with the small cap Russell 2000 -1.0%, the Nasdaq -0.8%, and the S&P 500 and Dow Jones Industrial Average -0.7% (chart below), all but the Dow lower for a third straight session (covered in the subscriber section along with bonds and crude).

As noted in the Week Ahead, this week is light for US economic data. Tuesday brought us just April pending home sales (contract signings so more forward looking (although also subject to cancellations which have been increasing)) which, after hitting an all-time low in January, rose for a third straight month +1.4%, beating expectations for a +1.0% increase with the sales pace at a 5-month high.

Elsewhere, the dollar would recover Monday’s decline, and US natural gas futures would also advance. Gold, copper, and bitcoin futures would fall back (all covered in the subscriber section).

The market-cap weighted S&P 500 (SPX) was -0.7%, the equal weighted S&P 500 index (SPXEW) -0.6%, Nasdaq Composite -0.8% (and the top 100 Nasdaq stocks NDX) -0.6%, the SOX semiconductor index UNCH (after its worst two sessions since October), and the Russell 2000 (RUT) -1.0%.

Some market commentary:

“Nvidia’s earnings are the ultimate test for a stock market that is not only trading at record highs, but one that also had a breathtaking bounce off of the March lows,” writes Richard Reyle, chief investment officer, Questar Capital Partners. “Nvidia is the market’s shorthand for everything AI and this market’s gains have been driven in large part by AI over the past few years.”

“The performance of the semis has been parabolic, so it’s not surprising there’s some profit-taking,” said Roger Lee, head of equity strategy at Cavendish. “Maybe there is also an element of the returning doubts over the monetization of AI.”

After going parabolic through April and the beginning of May, semiconductor stocks have gotten ahead of themselves, according to Seaport Research

“We think the semis market is going to be choppy in the near-term,” analyst Jay Goldberg at Seaport wrote on Monday. “As much as the secular AI trend will be a major force, we see many stocks getting ahead of their fundamentals.

“AMD and INTC have a good chance of growing into their numbers, but NVDA remains constrained by high expectations and serious supply constraints,” he added.

“This is a well deserved breather after an epic rally,” Jed Ellerbroek, portfolio manager at Argent Capital Management, told CNBC. It’s an “interesting time for the reversal, with it coming just a few trading days before the biggest chip stock in the world reports what will be outstanding earnings and guidance.”

“Investors need some reassurance that the AI story is still alive and well and that the company is producing enough revenue growth to back up its elevated valuation,” Paul Stanley at Granite Bay Wealth Management said. “We believe that Nvidia will report financial results that justify its valuation, which is just what the stock market is looking for.”

“Investors are desperate for the Middle East conflict to end as that should, in theory, help to bring down oil prices, dampen talk of rate hikes, and switch the conversation back to economic growth,” said Dan Coatsworth, head of markets at AJ Bell. “For now, the conflict rumbles on and investors remain slightly cautious.”

“Yes, we remain tactically bullish, but we would not be maximally net long given the elevated probability of a pullback led by tech,” said the JPMorgan Market Intelligence desk led by Andrew Tyler, adding dips will likely be bought.

“From a positioning standpoint and how stretched things have gotten, probably means that you don’t see as sharp of the rallies that we were seeing certainly off the throes of the low in March,” Kevin Gordon, head of macro research and strategy at the Schwab Center for Financial Research said on CNBC’s “Closing Bell: Overtime” on Monday afternoon.

“I see markets underpricing the risk of a Fed rate hike starting this year,” Citigroup Inc. strategist Jim McCormick said. Swap traders are currently leaning toward a 25 basis point increase in December, with a move fully priced for March next year.

Nicolas Bickel, group head of investment for private banking at Edmond de Rothschild, told Bloomberg TV he wouldn’t be surprised to see 10-year US yields at 5%. The rate rose two basis points to 4.61% on Tuesday. “If we have higher inflation and growth stays steady, it will not be an issue,” he said.

“The bond vigilantes are at play right now,” said Will McGough, Chief Investment Officer at Prime Capital Financial. “Everybody’s on to energy prices staying higher, which could lead into inflation that’s behind the curve a little bit.”

“There’s this narrative that new Fed chairmans tend to get tested by the markets,” McGough told CNBC. “You could see the bond vigilantes were obviously testing him here, if you believe that theme.”