Markets Update - 5/20/26

A detailed look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for tomorrow.

Quick Summary:

US equity indices would start the Wednesday session trading modestly higher as covered in the morning update led by technology stocks ahead of Nvidia earnings which came after the market close (more on that in the subscriber section).

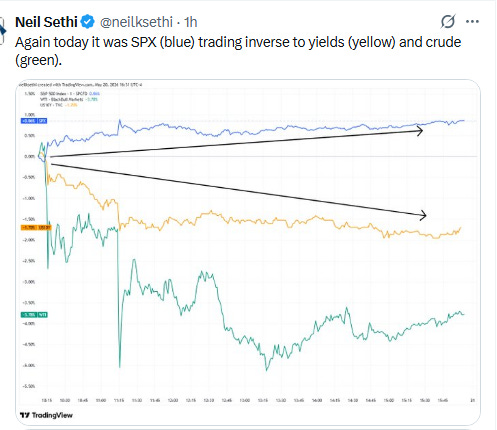

Around 10.15am ET stocks would get a boost from an unverified report from an Arabic news outlet that a US-Iran agreement was close (see below). Oil and yields would fall back. Equities would get another boost late morning when President Trump told reporters on Air Force One that the U.S. is in the “final stages” of talks on Iran. Equities would ride hopes for an agreement into the close led by the small cap Russell 2000 +2.6% (best day in 6 weeks). The tech-heavy Nasdaq would finish +1.5%, the Dow Jones Industrial Average +1.3%, and the S7P 500 +1.1%.

President Donald Trump also said Wednesday the U.S. needs the "right answers" from Iran on a peace deal and warned Tehran of fresh military action without an agreement. Speaking to reporters, Trump said, "If we don't get the right answers, it goes very quickly,” adding that "hopefully [Iran] will make a deal that's going to be great for everybody."

For its part Iran said it is reviewing the US’s new draft in response to Tehran’s 14-point proposal and has yet to give a response, the Tasnim news agency reported. President Masoud Pezeshkian posted on X that Iran has “explored every avenue to avert war,” adding that “all paths remain open from our side.”

As noted in the Week Ahead, this week is light for US economic data, but we did get the minutes from the April FOMC meeting which confirmed a committee becoming increasingly hawkish with a majority in favor of rate hikes if inflation “continues to run persistently above 2 percent.”

Elsewhere, the dollar would edge lower while US natural gas futures would fall along with crude prices. Gold, copper, and bitcoin futures all rose (all covered in the subscriber section).

The market-cap weighted S&P 500 (SPX) was +1.1%, the equal weighted S&P 500 index (SPXEW) +1.1%, Nasdaq Composite +1.5% (and the top 100 Nasdaq stocks NDX) +1.7%, the SOX semiconductor index +4.5%, and the Russell 2000 (RUT) +2.6%.

Some market commentary:

“Stagflation risk has gone up significantly,” said Justin Onuekwusi, chief investment officer at St. James’s Place. “When we’re talking about increased inflation and falling growth, in that environment, most asset classes will struggle, including bonds.”

After Nvidia’s earnings after the bell, the end of earnings season will be drawing near. That likely means things like interest rates, the Iran conflict, inflation and oil prices will stoke more volatility in stocks, Anthony Saglimbene, chief market strategist at Ameriprise Financial, said in a phone interview. “These are becoming more front-and-center items,” Saglimbene said, adding that even if the Iran conflict ended soon, oil prices are feeding into inflation, and are likely to stay higher for some time given the supply shock. All that can mean an increase in volatility.

“Everyone wants to see [the Iran conflict] end, but negotiations so far have been far apart on key issues, with both sides expecting each other to blink first,” said veteran strategist Louis Navellier. “Even if a deal is struck, it may take some time to be sure it won’t be violated for things to fully return to normal.”

“We have our usual hopes that today’s comments about the final stages of the war prove to be true, though we retain our now-well-earned skepticism that it will be the case immediately,” said Steve Sosnick at Interactive Brokers.

Treasury yields and oil prices “all traces back to energy,” said Brad Peterson, chief investment strategist at Northern Trust. Yet because of the damage done to energy markets during the war, investors should be prepared for some “uncomfortable inflation readings for the rest of this year,” Peterson said in an interview with MarketWatch. That underscores his underweight call for fixed-income and his continued overweight to equities, including infrastructure-type stocks and emerging-markets equities benefiting from the artificial-intelligence spending boom.

Following a few days of selling in the stock market, the “bulls are back in charge today.” That’s Ryan Detrick, chief market strategist at Carson Group, telling MarketWatch that optimistic tones about ending the Iran war might feel like “we’ve heard this movie before,” but, “for today, it has allowed crude oil to drop.”

To bring rates lower , it might only take a bad labor-market report, a drop in consumer spending because of high oil and gas prices or a warning from the battered private-credit market, said George Catrambone, head of fixed income for the Americas at DWS. He also expects incoming Fed Chair Kevin Warsh to sound "ice cold" about any rate hikes.