Markets Update - 5/26/26

A detailed look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for tomorrow.

Quick Summary:

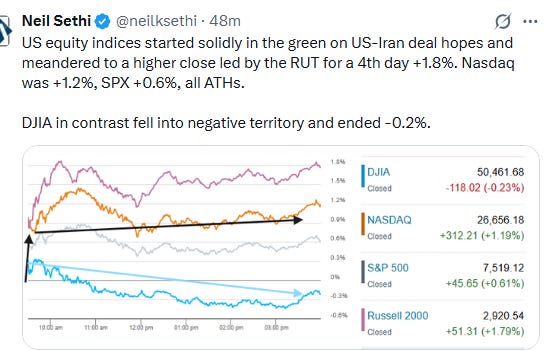

US equity indices would start the holiday-shortened week solidly higher as bond yields continue their decline for a fourth straight session as hopes remained high for a US-Iran peace deal as discussed in the Week Ahead and further in the morning update.

There would be little indication of progress during the day on that front, but that lack of progress (and the uptick in oil prices after falling back sharply Monday) was shrugged off by equity indices on the back of another surge in memory chip names with Micron Technologies adding another 19% to a nearly 800% rally over the past year which took it over the $1 trillion market capitalization mark.

And while the Nasdaq would finish +1.2%, it would be the small cap Russell 2000 that would lead for a fourth straight session +1.8% helped by a fourth day of declining bond yields. The S&P 500 would finish +0.6% while the equal-weight version would end +0.5%. All of these indices would end at all-time highs. In contrast the Dow Jones Industrial Average, heavier in energy and consumer products companies would end -0.2%.

In economic reports, the Chicago Fed National Activity Index (a good GDP proxy) rebounded above the trend level with the diffusion index (breadth of indicators) the strongest since Sept 2022. Meanwhile, consumer sentiment from the Conference Board edged back from the highs of the year on a drop in the present situation index with consumers indicating they were cutting back on expensive purchases but future expectations rose. Expectations for higher stock prices moved to the highest since 2024 even as the share of consumers who said a US recession over the next 12 months is ‘very likely’ and ‘somewhat likely’ rose.

Elsewhere, the dollar would edge higher and copper and bitcoin futures would also gain while gold and US natural gas would fall back (all covered in the subscriber section).

The market-cap weighted S&P 500 (SPX) was +0.6%, the equal weighted S&P 500 index (SPXEW) +0.5%, Nasdaq Composite +1.2% (and the top 100 Nasdaq stocks NDX) +1.8%, the SOX semiconductor index +5.5% (to a new all-time high), and the Russell 2000 (RUT) +1.8%.

Some market commentary:

The main driver of the mood music is the story in Iran,” Mizuho Bank Ltd. strategist Jordan Rochester said. Despite the strikes and belligerent rhetoric from Iran, “both sides are closer than they have been to date to getting something over the line. The US has made it clear it does not want the kinetic action to re-start,” he said.

“Doubts about the deal and its detail, especially relating to uranium enrichment and the tolling of the Strait of Hormuz, persist,” said Kyle Rodda at Capital.com. “However, market participants are placing their bets on peace and subsequently buying into very strong equity fundamentals.”

“The consensus view still assumes there will be some type of a détente formally reached within the next few days between Washington and Tehran, which means the real question is how much of this is already priced in?,” wrote Adam Crisafulli of Vital Knowledge.

“Don’t expect an agreement to immediately send the S&P 500 running to 8,000, but while the near-term reaction may be a mild disappointment, the reality is that removing distractions and allowing investors to focus on strong earnings and stable growth will increase the rally potential for this market,” Tom Essaye at The Sevens Report said.

“Market participants are placing their bets on peace and subsequently buying into very strong equity fundamentals,” said Kyle Rodda at Capital.com.

“There is no doubt that fundamentals are at least partially responsible for the market rally,” wrote Adam Parker, founder of Trivariate Research. “With earnings projected to grow 23% this year, and 16% next year, there’s a credible argument to make that despite the increasing projections for earnings, and strong earnings growth, the price-to-forward earnings has been modestly contracting.”

“Net net, optimism is still elevated that an agreement can be made to end the war,” said Jim Reid, strategist at Deutsche Bank. He also noted that the other main driver of bonds this week will likely be the U.S. personal consumption expenditure price index data, due for release on Friday. “Our economists expect core PCE inflation at around +0.3% month-on-month, unchanged from March, with the year-on-year rate edging higher. This release matters not just for the inflation print itself, but for how it fits with the broader narrative of sticky services inflation and resilient demand,” said Reid.

“You’ve got investors that are, I think, pathologically optimistic here that the war is going to end soon and that things are going to resume back to the way they were prior to the war,” said Ron Albahary, LNW chief investment officer.

There’s a “tug of war going on” in the market, Albahary added. Investors are “believing in this tsunami of capex that has been driving markets higher,” he said, while the base of the U.S. economy is “still relatively fragile,” with inflation “likely becoming systemic.”

“While we’d like to share the optimism, there have been enough setbacks in the process of crafting an agreement between Washington and Tehran that we’ll remain cautious until there is more tangible progress,” said Ian Lyngen at BMO Capital Markets.

“I’m not a buyer that there’s some deep structural shift that’s going to make the economy more inflationary,” says Nathan Sheets, global chief economist at Citigroup Inc. He says that’s largely because AI is likely to be an enormous positive supply shock. “I don’t think we’re going to see it today or tomorrow, but over a several-year period it is likely to bring a reduction in inflationary pressures, as the economy’s capacity to produce inevitably expands.”