Markets Update - 5/7/26

A look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for tomorrow

Quick Summary:

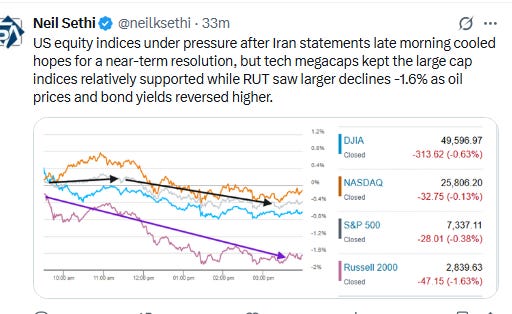

US equity indices were pressured Thursday by Iranian statements that cooled expectations for a near term resolution to the conflict which saw oil prices and bond yields reverse from early losses to end higher.

The megacap tech stocks continued to outperform keeping the large cap indices more supported while the small cap Russell 2000 saw its worst session since March.

It was a heavier day of US economic data:

Productivity decelerated but remained positive with the rate over the past year the best since Q3 2024 seeing labor costs decelerate and that year-over-year figure fell to the least since Q3 2023 but so did real compensation.

April Challenger announced job cuts increased (3rd highest April since 2009) led by the Tech sector while overall hiring plans fell back.

Weekly initial claims jobless claims remained near the least since 1969 while continuing claims fell to the least since Jan 2024

Construction spending came in better than expected increasing +0.6% in March on the back of strong residential and public spending.

Non-mortgage consumer borrowing rose much more than expected in March boosted both by consumer loans for autos and tuition which grew the most since mid-2023 while credit card balances rose the most since 2024.

US equity indices opened trading Thursday edging higher as crude prices were initially lower for a third day despite little movement on the Iran front as detailed in the morning update.

However mid-morning a senior Iranian official said that the country would not allow the U.S. to reopen the Strait of Hormuz passageway with an “unrealistic plan” or let the U.S. leave the conflict without paying reparations for the damage inflicted on the country as reported by Iran’s state-owned Press TV. Separately a US intelligence analysis concluded Iran can survive the naval blockade for at least three to four months before facing more severe hardship, according to the Washington Post. All this saw crude oil prices reverse higher and bond yields followed.

Then late in the session we got reports that sounds of explosions were heard near a port city in southern Iran with the nation’s state TV saying the US military attacked an Iranian oil tanker and was hit back by missiles, while U.S. Central Command in a statement said its forces “intercepted unprovoked Iranian attacks and responded with self-defense strikes” as three U.S. Navy destroyers transited the strait late Thursday.

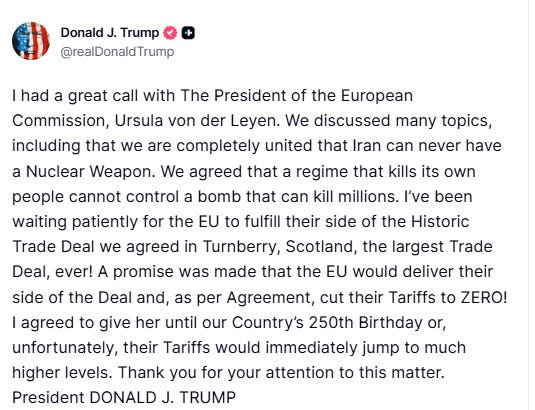

Separately President Trump extended the deadline to July 4th for the EU to approve the deal he struck last year at Turnberry with EU Commission President Von der Leyen saying there would be tariffs at “much higher levels” if the EU does not approve the deal by then (see post below).

Elsewhere, the dollar and US natural gas futures reversed from losses along with bond yields and crude prices, while copper and bitcoin would do the opposite (reverse from gains) and gold would trim its advance (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was -0.4%, the equal weighted S&P 500 index (SPXEW) -0.7%, Nasdaq Composite -0.1% (and the top 100 Nasdaq stocks (NDX) -0.1%, the SOX semiconductor index -2.7%, and the Russell 2000 (RUT) -1.6%.

Some market commentary:

“We have definitely moved from peak pessimism to somewhat elevated optimism,” said Joe Gilbert, portfolio manager at Integrity Asset Management. “The concern is with the sustainability of the rally. So this narrowing of the market is more indicative that we are getting less full participation with every surge higher.”

Samantha McLemore, Patient Capital Management founder, expects the rally to keep ripping higher from here. “It’s a secular bull market,” she said on CNBC’s “Closing Bell” on Wednesday afternoon. “People have been talking about this — are we in a bubble, has it gone too far — for over a year now, so I think that’s kept a lid on valuations, and we’ve mostly just seen the moves track the earnings.”

“Even though there is not yet a final peace agreement, markets are clearly pricing in a meaningful step forward toward a resolution,” said Francisco Simón, head of investment strategy at Santander Asset Management. “The key point is that this reduces the probability of the most negative scenarios, particularly those involving a more prolonged shock to global growth.”

“Numbers have been very robust across the board. In the tech space, of course, but in other sectors too,” said Guy Miller, chief market strategist at Zurich Insurance. “That’s keeping the momentum going and keeping investors buying into the equity bull market.”

“Markets continue to be underpinned by strong and accelerating corporate earnings and resilient economic fundamentals, even as investors navigate ongoing geopolitical uncertainty,” said Mona Mahajan at Edward Jones.

“I expect equity markets to consolidate unless yield curves move lower on renewed expectations of Fed rate cuts,” said Roberto Scholtes, head of strategy at Singular Bank. “Bond yields remain closely correlated with oil prices and should decline if prices ease on a peace agreement.”

“In that environment where you basically don’t know if there’s going to be a deal or not — very difficult to predict with this new leadership in Iran — you know you’re going to be subject to news and you’re going to be moving around like crazy,” Citigroup Inc.’s Max Layton told Bloomberg Television.

“There are a raft of risks facing the market, from a massive and highly concentrated rise in forward earnings not being realised, to a re-escalation in hostilities and re-accelerating inflation, to a surge in buyback commitments falling short of expectations. Funds who don’t chase the rally might look prudent in the end.” — Simon White, macro strategist.