Markets Update - 5/8/26

A look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for next week

Quick Summary:

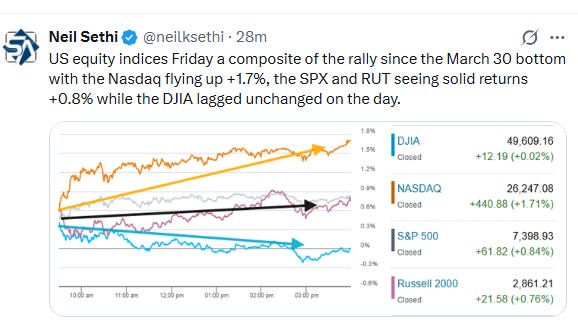

US equity indices Friday were a snapshot of the rally since the March 30 bottom despite a continuation of the stalemate between the US and Iran, seeing the Nasdaq flying to finish up +1.7%, the S&P 500 (SPX) and small cap Russell 2000 (RUT) registering solid returns +0.8% while the Dow Jones Industrials (DJIA) lagged finishing unchanged on the day.

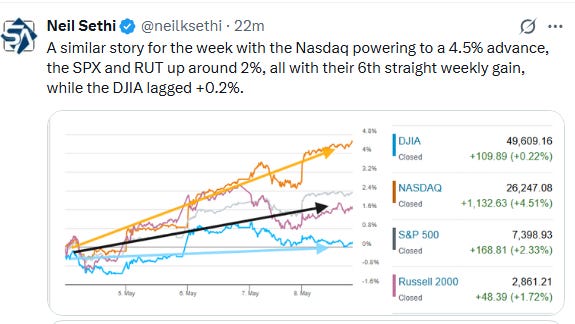

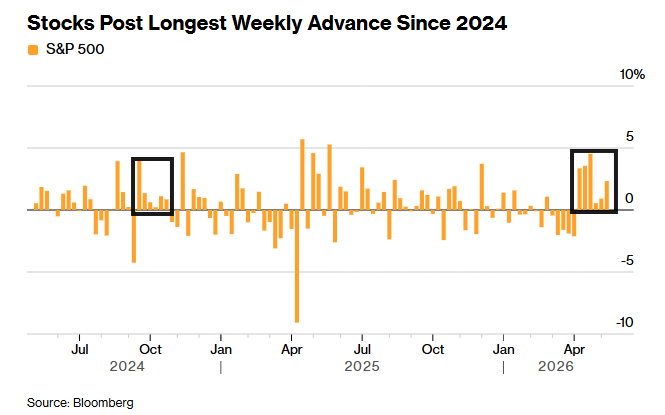

A similar story for the week with the Nasdaq powering to a 4.5% advance, the SPX and RUT up around 2%, all with their 6th straight weekly gain (for the SPX the longest since 2024), while the DJIA lagged +0.2%.

US economic data Friday was dominated by the Employment Situation report which showed US employers adding a much larger than expected 115,000 to payrolls in April (around double estimates), capping the best two months since 2024, which also saw an increase in the workweek leading to a reacceleration in aggregate employment incomes. The unemployment rate was unchanged at 4.3% as expected though as the more volatile household survey saw job losses and a decline in the labor force.

We also got an updated U of Michigan consumer sentiment report which fell to new all-time lows on further declines in sentiment about current conditions.

US equity indices opened trading Friday higher despite the clashes noted in Thursday night’s update between Iran and US forces, encouraged by each side choosing to not press the situation further, while another strong nonfarm payrolls number pointed to a continued firming in the jobs market as detailed in the morning update.

Despite statements from US officials since Wednesday that Iran was expected to respond by today to President Trump’s plan for reopening the Strait Tehran’s Foreign Ministry Spokesman Esmail Baghaei told the semi-official Tasnim news agency, Iran’s response is “under review,” without giving a timeline. Separately, US forces struck two empty Iranian-flagged oil tankers attempting to circumvent the American naval blockade against Iranian ports on Friday, according to Central Command.

Elsewhere, bond yields and crude prices were little changed as were bitcoin and US natural gas futures while the dollar fell further. Gold and copper were higher (all covered in the subscriber section).

The market-cap weighted S&P 500 (SPX) was +0.8%, the equal weighted S&P 500 index (SPXEW) +0.3%, Nasdaq Composite +1.7% (and the top 100 Nasdaq stocks (NDX) +2.4%, the SOX semiconductor index +5.5% (an all-time high), and the Russell 2000 (RUT) +0.8%.

Some market commentary:

“Friday’s strong jobs report shows that the labor market is in the early stages of growing again, which is welcome news for the economy and the stock market since employment is the lifeblood of our economy,” said Chris Kampitsis at Barnum Financial Group.

“The economy is so much better than what the doom crew has been saying,” said Chris Zaccarelli at Northlight Asset Management. “There are a lot of headwinds – higher oil prices, sticky inflation and higher-for-longer interest rates – and yet the labor market is adding jobs.” For those who are scratching their heads about the equity-market resilience amid all the uncertainties, Zaccarelli says the short answer is: Stock prices follow earnings and – at least for now – they’re growing too quickly for investors to ignore.

Goldman Sachs Group Inc.’s Christian Mueller-Glissmann.

“Equities are back at all-time highs with rates and energy prices still reflecting the lingering conflict,” he told Bloomberg Television. Mueller-Glissmann attributed the market resilience to remarkably strong earnings and the narrow nature of the equity market rally, which he described as momentum driven and “quite scary” due to the potential for sharp reversals.

“For now, investor sentiment remains strong as the equity market is looking through high oil prices,” said Marija Veitmane, head of equity research at State Street Global Markets. “We continue to stress that the strength of earnings is heavily concentrated in IT sectors. These sectors are also the least exposed to physical supply chains and commodity pass-through.”

Going forward, PNC Asset Management chief investment strategist Yung-Yu Ma expects earnings momentum to continue. “It is important to note that the gains are very broad based,” he said on CNBC’s “The Exchange” on Thursday afternoon. “If you look out to Q2, Q3 and Q4, the market and analysts are still expecting about 20% or higher earnings growth on a year-over-year basis in those subsequent quarters. So we’re not seeing the momentum expected to let up. There is dispersion, for sure, but the momentum is going to be quite strong here.”

“Any hint of a deal in the Middle East ahead of next week’s China-US summit is sufficient for equities to rally in the short term. A fast, comprehensive deal looks unlikely, but for markets the key is that the Strait of Hormuz could reopen while negotiations continue. That matters more than the underlying geopolitics.” — Skylar Montgomery Koning, macro strategist.

“We still believe an eventual diplomatic solution should emerge, and a resilient economic backdrop and robust earnings growth mean that investors should stay positioned for long-term equity gains through diversified exposure,” said Ulrike Hoffmann-Burchardi at UBS Chief Investment Office.

“Bulls say the market has already priced in oil market shifts, and are focusing instead on U.S. economic tailwinds like strong earnings growth, fiscal stimulus, and meaningful deregulation. We’re “solidly in a risk-on market regime,” said Darius Dale, CEO of 42 Macro, a risk management research firm.

“Bears continue to point to the narrowness of the rally, particularly in areas like semiconductors, but momentum — both in price action and earnings revisions — has remained the dominant force driving markets higher,” said Mark Hackett at Nationwide.

“Strong data and inflation have likely put paid to any easing in the foreseeable future, though this could change depending on how energy prices and the situation in the Middle East develop,” said Lindsay Rosner at Goldman Sachs Asset Management.

Keith Buchanan, senior portfolio manager at Globalt Investments, is skeptical that the market’s recent run can continue, especially given how much of it is being propped up by optimism surrounding artificial intelligence capital expenditures. “The market is trading valuations that don’t indicate the risk that we see that out there,” Buchanan said, citing the potential for the Middle East conflict to continue longer than expected and the increasingly adverse impacts of that on the consumer. “It’s a tale of the AI spend and the ripple effects – and earnings as well – that’s absolutely powering an economy that is, without that spending and optimism, probably pretty lackluster,” he continued.