Markets Update - 6/12/26

A look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for next week.

For those who follow me on X, please note my account was suspended, apparently because I posted some BoA materials. The whole thing is quite odd given how many people post BoA charts, but you can read about it in the post below (just click on it) and replies to it (I explain it all in one of them). You can also refollow me at the new account (and a retweet would be appreciated!). If I somehow get the old account unfrozen, I’ll let you know.

Quick Summary:

US equity indices would start Friday’s session building on Thursday’s rally (the best one-day return since early April as covered in last night’s update) with media reports that the US and Iran may sign an agreement to reopen the Strait of Hormuz as early as this weekend as discussed in the morning update.

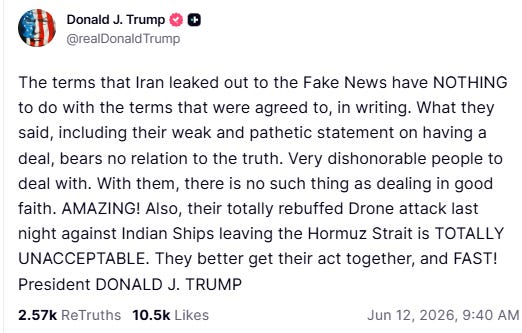

Equities would be pushed and pulled by conflicting headlines around whether the parties in fact had agreed to a deal, which included a blistering post from President Trump (below) that “terms that Iran leaked out to the Fake News have NOTHING to do with the terms that were agreed to,” calling the Iranians "very dishonorable people," and saying "Drone attack last night against Indian Ships leaving the Hormuz Strait is TOTALLY UNACCEPTABLE. They better get their act together, and FAST!"

Confusion would continue throughout the day (although that is not entirely unusual in the final stages of a deal as parties jockey for positioning, and in this case likely exacerbated by the clear divisions between different Iranian factions with the lack of a true central power).

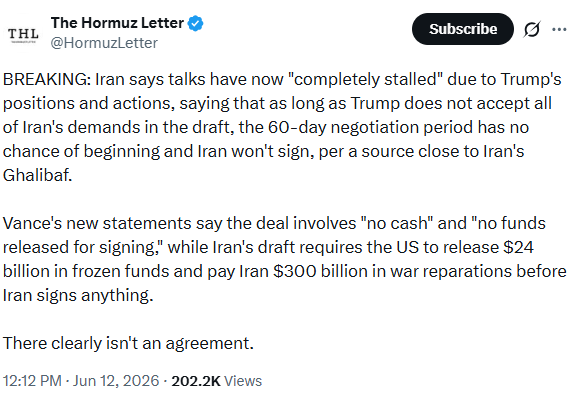

On the one hand, there were reports that Iran says talks have now “completely stalled” due to Trump’s positions and actions, saying that as long as Trump does not accept all of Iran’s demands in the draft, the 60-day negotiation period has no chance of beginning and Iran won’t sign.

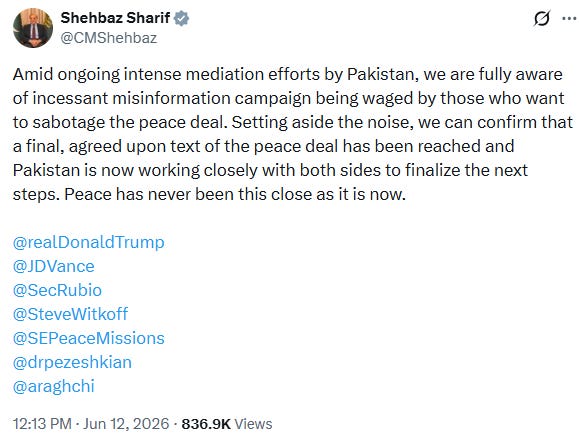

But Iran’s Foreign Minister earlier said “the memorandum of understanding has never been closer,” while Pakistani Prime Minister Shehbaz Sharif posted on X that “we can confirm that a final, agreed upon text of the peace deal has been reached and Pakistan is now working closely with both sides to finalize the next steps. Peace has never been this close as it is now.”

Somewhere in the middle, CNBC reported that a senior Trump administration official said the U.S. is not “100%” confident the agreement they reached will be signed. “I maybe would have said 75% this morning. It’s probably more like 80-85% now,” said the official. “But it’s not 100%.” Iran’s system is “very complicated,” and there are internal fractures within the regime, the official explained.

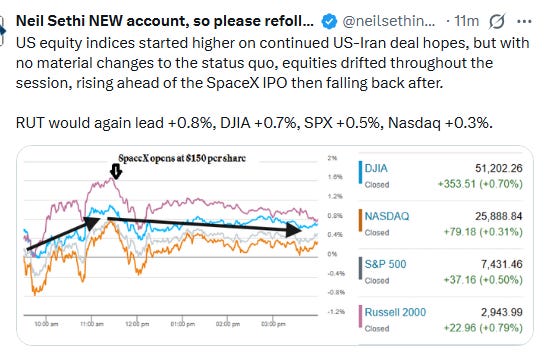

With no clear guidance in that regard, equities would draw some strength from the (very) highly anticipated debut of SpaceX which would open trading at 11.30 am with a 20% gain (which would extend to a 35% gain before ending up 24%). That though would mark the highs for the day, and equities would soften into the close but still finish solidly in the green led by the small cap Russell 2000’s (RUT) +0.7% which finished at a new all-time high (as did the equal-weight S&P 500 index). The Nasdaq was +0.3%, the S&P 500 (SPX) +0.5%, and the Dow Jones Industrial Average (DJIA) +0.7%.

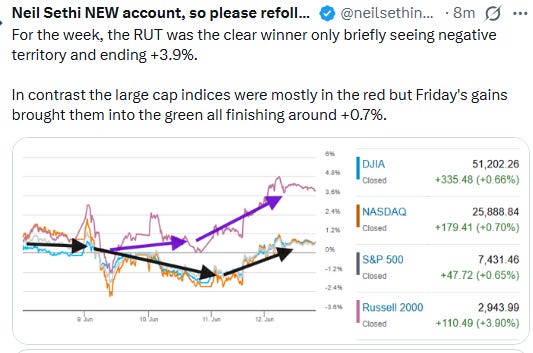

For the week, the RUT was the clear winner only briefly seeing negative territory and ending +3.9%. In contrast the large cap indices were mostly in the red, but Friday's gains brought them into the green all finishing around +0.7%.

Elsewhere, bond yields would edge higher even as crude prices continued their sell-off. Gold and copper saw solid gains and US natural gas futures were also higher, while the dollar and bitcoin were little changed.

Some market commentary:

“History indicates that large IPO issuance occurs during periods of strong equity market sentiment, but the added equity supply can cause some indigestion. Household equity exposure already sits close to an all-time high, which suggests they may sell existing holdings to fund these new positions,” wrote Wells Fargo Investment Institute global equity strategist Douglas Beath.

“Combined with the ongoing geopolitical tensions and the upcoming midterm elections, it could be one more reason for markets to display greater choppiness in the second half.”

“We remain favorable on the AI theme and the Information Technology sector but would not chase this run up,” he added, noting that as of May 29 the sector has gained 37% since April compared to the S&P 500′s 17% advance in the same period.

“The AI theme, in my opinion, is just getting stronger,” said Jeff Kilburg, CEO of KKM Financial. “Nothing moves in a straight line, and we’ve seen a couple hiccups in the Nasdaq, maybe more to geopolitical tension versus the SpaceX IPO. But I think the [‘Magnificent Seven’] leadership should persist.”

“This week it’s starting to feel like now there could be more upside left in this market,” said Dave Grecsek, director of investment strategy at wealth-management firm Aspiriant, in a phone interview Friday. Oil prices falling amid optimism about a potential peace deal between the U.S. and Iran getting signed this weekend is a “huge pillar” of the stock market’s gain this week, he said. Also, the historic SpaceX IPO being well-managed so far “signals that investors are feeling confident and that risk appetite is healthy.”

“The IPO parade, which now looks like it’s turning into a stampede, has been coming for a while,” said Mark Klein, CEO and president at SuRo Capital. “SpaceX is going to be the bellwether.”

“As you look at the IPO market going forward, there are a lot of companies that want to go public, but you may see some of the more important names wait and see what happens because so much capital is flowing to a handful of companies,” he added.

“The market may be in a much-deserved rest” after “a historic run, and two-sided trading is more the norm,” said Ken Mahoney, chief executive officer at Mahoney Asset Management. “Just like in the movie The Perfect Storm, this market was hit with high winds, a cold front and heavy rain all at once.”

“We got into a ‘throw a dart’ period where anything you bought worked,” said Mahoney. “It’s never supposed to be that easy.”Peter Boockvar, chief investment officer at One Point BFG Wealth Partners, reiterated a concern other investors have had about all the mega-IPOs set to come online this year: does the market have the liquidity to manage all of it?

“There is an impact from a supply/demand perspective when combined with the upcoming Anthropic and OpenAI IPOs, along with the dramatic reduction in the pace of stock buybacks by the hyperscalers,” Boockvar said. “So, a lot more equity supply and a reduction in stock buyback demand could be a lid to the market until everything gets digested.”

UBS Analyst Michel Lerner believes it’s too soon to know whether recent market volatility is another chance to “buy the dip” in momentum stocks or if the market volatility is hinting that it’s going back to “historical norms.”

“Given the higher inflation print, there is a renewed risk of replaying the 1999-2000 script when the Fed raised rates aggressively into the peak of the dotcom bubble,” Lerner said.

“U.S.-Iran headlines moved markets around a bit,” Anthony Saglimbene, chief market strategist at Ameriprise Financial told MarketWatch Friday. Yet unless high oil prices start impacting the economy, stocks are likely to “look through” headlines about when the war might end.

“We expect inflation pressures to ease after the Iran conflict simmers and the subsequent improvement in supply chains,” said Jeff Roach at LPL Financial. “But if the conflict in Iran remains throughout the summer, we should expect stronger inflation headwinds will put a damper on the growth trajectory.”

“In keeping with the recent easing in oil and gas prices, the pullback in consumers’ short- and long-term inflation expectations offers some relief from a monetary policy standpoint,” said Vail Hartman at BMO Capital Markets. “However, the inflation metrics remain elevated versus pre-war levels and in a broader historical context.”