Markets Update - 6/16/26

A look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for tomorrow.

Quick Summary:

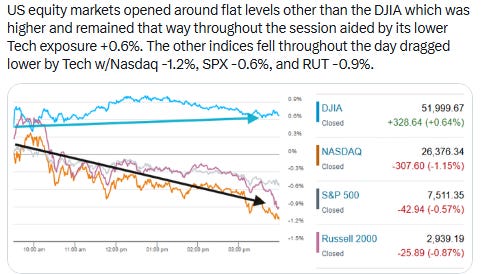

US equity indices would start Tuesday’s session around flat levels other than the Dow Jones Industrial Average which opened higher and remained that way throughout the session ending +0.6%, extending further into record high territory, aided by its lower Tech exposure.

In contrast, the Nasdaq -1.2%, S&P 500 -0.6%, and small cap Russell 2000 -0.9% all were dragged lower by their respective Tech sectors (for the S&P 500 the sector finished -2.3%, the only sector to finish worse than -0.25%), led by a selloff in shares of semiconductor names.

The weakness in Tech was even as (or perhaps in part because of) a renewed advance in SpaceX which at one point surpassed both Microsoft and Amazon in implied market cap during the session (but note the caveats in the morning update about the size of the company available for public trading). Some commentators believe that investors are taking profits in other Tech names to free up capital to invest in SpaceX.

On the economic front, May housing starts saw the largest drop since March 2024 to the slowest annualized pace since May 2020 driven by the biggest decline in multi-family starts since 2011. Permits were more stable remaining in their range over the past year, while the pipeline of units under construction as well as those being completed remained around the lowest levels since 2022.

In addition, May import prices rose well more than expected to the highest pace from a year earlier since August 2022 on a broad based advance.

Elsewhere, bond yields would edge lower as crude prices continued their sell-off. US natural gas futures were higher, while gold, copper, bitcoin, and the dollar were little changed.

Some market commentary:

“I would say overall, the market reaction was fairly positive,” said Keith Lerner, CIO and chief market strategist at Truist Wealth, on CNBC’s “Closing Bell: Overtime” on Monday afternoon. “Even though the S&P 500 hasn’t quite gotten back to where it was, underneath the surface it’s telling you one of economic resilience. I expect things to be somewhat more choppy here in the near term, but again, it’s hard to complain after we have had a pretty good move off the March lows and still hanging in there pretty well.”

“For markets, a ‘higher-for-longer’ rate backdrop, rather than a renewed tightening cycle, can remain supportive of valuations, in our view, particularly if it reflects resilient economic growth alongside gradually moderating inflation pressures,” said Mona Mahajan at Edward Jones. She says easing geopolitical tensions could help alleviate inflation pressures and reduce bond yields, potentially driving a broadening of leadership into cyclical sectors and previously lagging corners of the market.

“There are a lot of S&P names that are negative on the year, but if we focus on momentum, we are not stuck with, do I buy SpaceX or not. We are no longer stuck in this world of, okay, I have to buy Korea and the five publicly traded memory names,” Josh Brown, co-founder and CEO of Ritholtz Wealth Management said on CNBC’s “Halftime Report” on Tuesday afternoon. “No, there are names in almost every sector hitting my best stock list and hitting 52-week highs, and I think you’re seeing crowding into those names, because this is what people want to do. They want to own the winners right now; that’s just the environment that we’re in. I love the fact, though, that you can find those winners almost every different area of the market that you want to look.”

“All eyes will remain on the Fed for now and how Kevin Warsh will handle the competing pressures from rising inflation and the prospect of lower energy inflation once the Strait of Hormuz reopens,” said Joachim Klement at Panmure Liberum.

“In a matter of months, the narrative has shifted from ‘how many rate cuts this year?’ to ‘how many rate hikes are on the table?’” Bret Kenwell at eToro noted. “That’s a big swing, and it puts Warsh in a difficult spot: He can acknowledge the recent pullback in oil prices and sound patient, but he can’t afford to look complacent if broader inflation pressures are moving the wrong way.”

“Investors will be watching the SEP closely for clues on whether rate hikes are truly on the table in the second half of the year,” Kenwell said. “Depending on the tone and how much this meeting reshapes investor expectations, it could dictate the market’s narrative for the next several weeks, at least until earnings season takes over.”While investors expect no changes to monetary policy, Warsh has strong views on the current inflationary environment and on what the Fed should and shouldn’t be, according to Christian Hoffmann at Thornburg Investment Management. That means the potential for volatility around Warsh’s communication is likely underpriced by the market, he added. “The backdrop is tricky, with inflation rising strongly in recent months,” Hoffmann noted. “At the same time, progress on the US-Iran conflict would certainly take some of the acute pressure off energy prices and inflation, and give central bankers a stronger reason to watch the dust settle.”

In today’s Markets Update:

The usual look at notable stock movers, sector performance, and corporate news from today.

A look at the pop in speculative activity on the Nasdaq.

Updated technical charts on a variety of US equity, bond, and volatility indices as well as select commodities.

Catch up on posts from the day.

Wrap-up and Wednesday’s global highlights.