Markets Update - 6/18/26

A look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for next week.

Quick Summary:

First a quick reminder that Friday is a market holiday in the US.

US equity indices would start Thursday’s session rebounding following the Fed-induced selloff Wednesday covered extensively in last night’s update.

The rebound came even as short-term Treasury yields (2-year) continued to climb to fresh 16-month highs (they would settle back to unchanged on the session but up +9 basis points on the week), with markets pricing a better than 50-50 chance for two Fed rate hikes this year following the more hawkish than expected Fed decision and new Chair Warsh’s press conference (also covered at length in last night’s update).

Markets though seemed to be boosted by US President Trump formally signing the interim peace deal with Iran and the start of more significant traffic through the Strait of Hormuz as discussed in the morning update.

Semiconductor names were a focus with Intel leading chip stocks higher, rising 10.6% after President Trump said the company will partner with Apple on designing chips in the U.S. Fellow semiconductor names such as Nvidia and Micron Technology were also higher by about 3% and almost 9%, respectively. The iShares Semiconductor ETF (SOXX) jumped more than 6%.

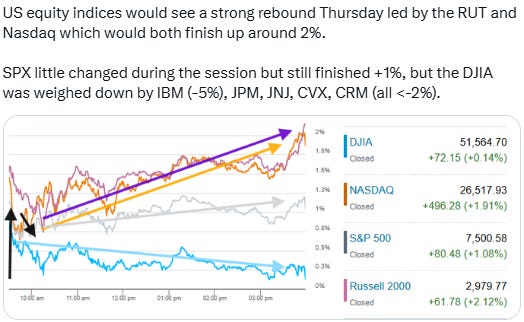

But it was the small cap Russell 2000 (RUT) that edged out the tech-heavy Nasdaq for the top gainer Thursday +2.1% vs +1.9%. Those were roughly double the +1% gain for the S&P 500 (SPX) and well above the +0.1% gain for the Dow Jones Industrial Average (DJIA) which was dragged down by a -5% loss in IBM, and over -2% in JPMorgan, Johnson & Johnson, Chevron, and Salesforce.

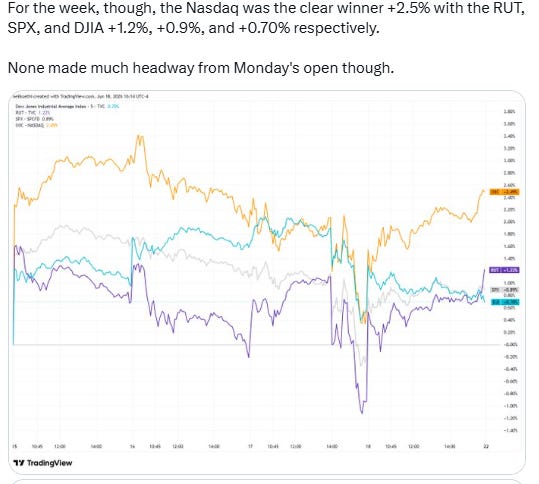

For the week, though, the Nasdaq was the clear winner +2.5% with the RUT, SPX, and DJIA +1.2%, +0.9%, and +0.70% respectively. None made much headway from Monday's open though.

On the economic front, weekly unemployment claims remained very low historically with continuing claims falling the most from the previous year since December 2022

Elsewhere, bond yields eased back while oil prices stabilized. The dollar continued its sharp gains to a fresh 1-year high, US natural gas futures were also higher, while gold, copper, and bitcoin fell.

Some market commentary:

“In spite of the mild U.S. equity weakness overnight, we maintain our bullish view, supported by resilient consumer spending, strong corporate balance sheets and continued investment in AI and infrastructure,” Willem Sels, global chief investment officer at HSBC Private Bank and Premier Wealth said in emailed comments. He added that the U.S. dollar is likely to remain supported.

Robert Conzo, chief executive officer at The Wealth Alliance, said he believes there’s “more bullishness around companies working together because of [artificial intelligence] infrastructure and the effects of AI within many, many different competing industries.” He also said, “I think Apple-Intel was a little proxy for what you could see happening in the future.”

“There’s uncertainty, but I think underlying that uncertainty is some pretty positive forces moving forward,” Conzo added, citing strong earnings, the better-than-expected May jobs reading and recent upbeat retail sales figures as drivers.“With the MOU now signed, there’s reason to believe that we may be close to or past peak inflation,” Raphael Thuin, head of capital market strategies at Tikehau said. “The market will be able to concentrate on earnings again, like for Micron next week.”

“The progress toward releasing oil supply from the Persian Gulf has supported equity prices,” said Ian Lyngen at BMO Capital Markets. “Lower energy costs have also eased forward inflationary concerns and led to meaningful declines in longer-dated Treasury yields.”

“The Fed held rates steady but spoiled the mood with a much more hawkish dot plot. Elevated inflation makes that understandable, but the committee is far from united, with only about half still penciling in rate hikes later this year,” said Sonu Varghese, chief macro strategist at Carson Group. “The bigger point is that policy still looks loose for an economy where inflation remains a problem and the labor market is stabilizing.”

“The market doesn’t like regime change,” added David Zervos, chief market strategist at Jefferies, on CNBC’s “Closing Bell: Overtime” on Wednesday afternoon.

“My view remains that inflation should moderate gradually over the coming months, and this might allow the Fed to maintain current policy settings rather than implement fresh tightening,” Fawad Razaqzada at Forex.com said.

In today’s Markets Update:

The usual look at notable stock movers, sector performance, and corporate news from today.

Updated daily technical charts on a variety of US equity, bond, and volatility indices as well as select commodities.

Catch up on posts from the day.

Wrap-up and next week’s global highlights.