Markets Update - 6/23/26

A look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for tomorrow.

Quick Summary:

US equity indices started Tuesday’s session solidly lower as a Tech selloff started with megacaps in the US on Monday, as covered in last night’s update, flowed to Asia where South Korea’s Kospi Index fell -10%, before flowing back to the US as discussed in the morning update.

The pressure was most apparent in the semiconductor space, where the PHLX Semiconductor Index tumbled -7.9%. Index heavyweights Sandisk (SNDK 1963.60, -310.13, -13.64%) and Micron (MU 1051.77, -159.61, -13.18%) were among the notable laggards, while equipment and analog names such as Lam Research (LRCX 371.33, -38.21, -9.33%) also endured heavy selling pressure. All of that comes ahead of Micron’s highly anticipated earnings report after the close tomorrow.

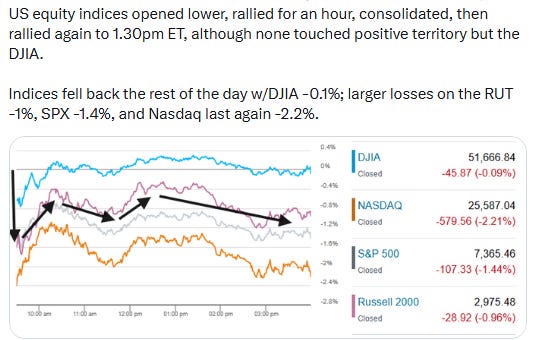

As a result, the information technology sector, three times over the largest sector in the S&P 500 (SPX), finished -3.7%, the weakest S&P 500 sector by a wide margin. That in turn pulled the tech-heavy Nasdaq down -2.2% followed by the SPX -1.4%.

The less tech-heavy Russell 2000 (RUT) would do a little better -1% while the price-weighted Dow Jones Industrial Average finished near flat levels -0.1%

Elsewhere, Treasury yields were mixed but overall little changed, the dollar rose to another 52-week high, while WTI and gold, copper, and US natural gas futures fell. Bitcoin was little changed (all covered in the subscriber section).

Some market commentary:

“Any headline that can be read as ‘AI-memory demand might be plateauing’ gets sold hard right now,” said Amanda Lyons, head of research at Energy Group Capital. “The vulnerability is in the positioning and the valuation, not in the buildout.”

“Many investors are sitting on large gains with their AI stocks, and any jitters could lead them to cut their position to lock in the gains,” said Jian Shi Cortesi, a fund manager at Gam Investment Management. “Right now tech stocks are also particularly sensitive to interest rate outlook and potential Fed rate hikes.”

“A market drop, even with heavy volatility, is healthy and will provide entry points for other investors,” said David Kruk, head of trading at La Financiere de l’Echiquier.

Tech giants will return to investor favor following a selloff that has dragged down some of the biggest names in recent weeks, Evercore ISI’s Julian Emanuel said. Earnings will be “the proof of the pudding” after driving a “furious rally” in April and May, he told Bloomberg Television’s Surveillance.

“The broader market remains supported by solid fundamentals,” said Brock Weimer at Edward Jones. “However, we believe diversification remains key to managing risk, particularly after the strong gains in technology and other growth-oriented segments of the market.”

“Looks like this was more of a technical related selloff than anything else,” Natixis Advisors portfolio manager Jack Janasiewicz said, adding that “breadth right off the open was decent despite seeing plenty of big red numbers — a sign of a narrow selloff.” The market seemed “to be holding up fairly well all told,” he said, adding “especially when we see the huge crowding in beta and momentum that very easily could lead to a nasty unwind.”

“Some of the recent performance in stocks has been highly speculative, fueled by a passion from retail investors for short-term gains,” Mark Dowding, chief investment officer for fixed income at RBC BlueBay Asset Management, told Bloomberg TV. “We may not like it this morning, but actually it’s healthy behavior.”

“The AI beneficiaries are the sell off and I don’t think they’re expensive, but they’re crowded,” said Andrew Slimmon, a senior portfolio manager at Morgan Stanley Investment Management, on CNBC’s “Squawk Box” Monday. “It’s captured kind-of the zeitgeist of the momentum traders and when that happens, you’re going to have sharp sell offs like we’re having. I’d argue it’s healthy.”

“This morning is a perfect storm for the tech selloff,” Bret Kenwell, U.S. investment and options analyst at eToro, told MarketWatch. He pointed to yesterday’s selling of the mega-cap “Magnificent Seven” stocks, which then led into overnight selling of Asian semiconductor stocks. This dampened investor appetite for tech. U.S. semiconductor stocks were selling off on Tuesday, but Kenwell said it was important to remember the impressive rally that the group had before today’s selloff. “If a stock goes up 200% and pulls back 10%, that comes with the territory,” he said. “A healthy reset would be appropriate.”

"South Korea’s sharp equity selloff highlights how fragile AI-led momentum can become when valuations, leverage, and retail positioning all stretch at the same time," says a comment from Menthor Q, a financial analytics platform. "The plunge in SK Hynix and Samsung suggests investors are moving from broad enthusiasm around memory chips and HBM demand toward profit-taking and risk control after an extreme rally. Leveraged ETFs and record margin debt appear to have amplified the downside, turning a valuation reset into a much sharper market move."

“The real test is Micron,” said Amanda Lyons, head of research at Energy Group Capital. “I would watch the rate of change in pricing and any change to capex or bit-supply guidance far more closely than the headline beat or miss.”

In today’s Markets Update:

A more detailed look at a second down day for the SPX and Nasdaq including a review of the sharp selloff in AI and memory-linked stocks and the poor reaction to Cerebras earnings meaning tomorrow’s Micron report now takes on even greater importance.

A look at the rotation beneath the surface into more defensive names and high Nasdaq speculative activity keeping positive volume supported.

Updated technical charts across the major US equity indices, Treasury yields, volatility gauges, the dollar, oil, gold, copper, natural gas, and bitcoin.

Some context on the competing AI-market arguments, including stretched positioning, underpriced risks, and rising bubble-risk indicators from Goldman, Nomura, and BofA, but also views from Goldman and Barclays that the broader bubble comparison remains more nuanced.

A look at the day ahead, including May new home sales, the 5-year Treasury auction, Fed stress-test results, and Micron earnings after the close.