Markets Update - 6/25/26

A look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for tomorrow.

Quick Summary:

US equity indices started Thursday’s session higher as discussed in the morning update, led by semiconductor shares after Micron’s blowout earnings report as covered in last night’s update.

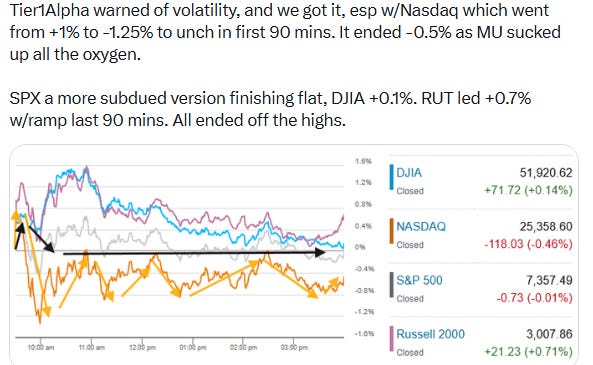

However, as also noted last night, the rally in semis has often pulled funds away from other areas, and that is what we saw in part today with the rest of the growth complex falling back and pulling the Nasdaq lower from the open. After a volatile session, it would close down 0.5%, its fourth straight decline, the first four-day losing streak since February, while the SPX finished essentially flat at -0.01%. The Dow Jones Industrial Average finished up 0.1% after hitting an all-time intraday high, while the small-cap Russell 2000 led, ending +0.7% at an all-time closing high.

Micron surged almost 16% and Qualcomm gained nearly 4% after raising its long-term non-handset revenue guidance, but Apple dropped 6% after announcing price increases on MacBooks and iPads, citing higher component costs, while Microsoft fell 3.5% after raising prices on Xbox consoles. All of the Mag-7 stocks finished lower. More details in the subscriber section.

But while growth shares were weak, the “other 493” held up better with six sectors advancing boosted by recent declines in oil prices and Treasury yields. Economic data also provided some uplift as while headline PCE prices (the Fed’s preferred inflation metric) rose 4.1% year-over-year and core PCE 3.4%, the highest since April and October 2023 respectively, personal income and spending were stronger than expected.

Elsewhere gold, copper, and US natural gas futures advanced, while the dollar and bitcoin futures fell (all covered in the subscriber section).

Some market commentary:

“The worst of inflation and consumer angst may be mostly behind us,” said Brian Jacobsen at Annex Wealth Management. “As long as gasoline prices trend lower, inflation expectations will likely follow suit.”

The latest economic data reinforced the view that consumers and the broader economy remain on solid footing, and while that may not soften the Fed’s stance, it helps ease fears of a “stagflationary slowdown,” according to Bret Kenwell at eToro.

“The impact of higher energy prices is probably short-lived,” said Scott Helfstein at Global X ETFs. “Inflation feels like a raw nerve after the past few years, but we are moving toward price stability. People are making more and spending more. That is nominal growth which will keep driving the economy.”

Inflation will likely start going lower now that oil prices have eased, so that may alleviate some of the pressure on the central bank, noted Chris Zaccarelli at Northlight Asset Management. “But next month’s data needs to be lower than what we are seeing today if that is going to be the case,” he said.

With the price of memory increasing, Jed Ellerbroek of Argent Capital Management noted that “everything that we buy that’s electronic that has semiconductor content” such as TVs and cars “are going to go up in price.”

“I think there are pretty big spillover effects from just really big inflation and technology supply chains,” the portfolio manager also said. Right now, however, the consumer is “strong enough to absorb these price increases,” he added. “Inflation is too high, but it’s not out of control,” Ellerbroek said.

Bonds were seeing a “relief rally” as the latest U.S. inflation reading from the personal consumption expenditures price index came in largely as Wall Street anticipated — even if inflation remains above the Federal Reserve’s 2% target, Lindsay Rosner, head of multisector fixed-income investing at Goldman Sachs Asset Management, said in an interview Thursday. The economy also appears fundamentally strong, she said, with Thursday’s revised estimate of growth in U.S. gross domestic product during the first quarter being stronger than expected at 2.1%.

In today’s Markets Update:

A look under the hood at another split session for US equities, with semiconductors rallying after Micron’s blowout report while the Mag-7 and other megacap growth names pulled the Nasdaq lower.

Updated technical charts across the major US equity indices, Treasury yields, volatility gauges, the dollar, oil, gold, copper, natural gas, and bitcoin.

A review of the sector rotation beneath the surface, including leadership from Industrials, Health Care, Materials, and the Russell 2000, along with continued weakness in Communication Services, Consumer Staples, and Consumer Discretionary.

A look at several market themes including lower energy prices, easing Treasury yields, this week’s Treasury auctions, updated Q2 GDP estimates, and commentary from Goldman, Mike Wilson, Ed Yardeni, Tom Lee, Tier1Alpha, and BofA.