Markets Update - 6/26/26

A look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for tomorrow.

Quick Summary:

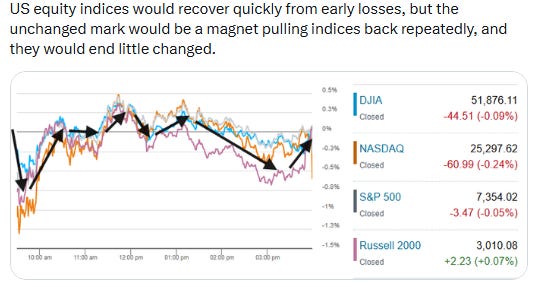

US equity indices opened the Friday session lower as Thursday’s reversal from pre-market gains (as covered in last night’s update) continued, although as discussed in the morning update, in contrast with Thursday’s pullback, semiconductor names — including Thursday’s big winner Micron Technology — were leading to the downside.

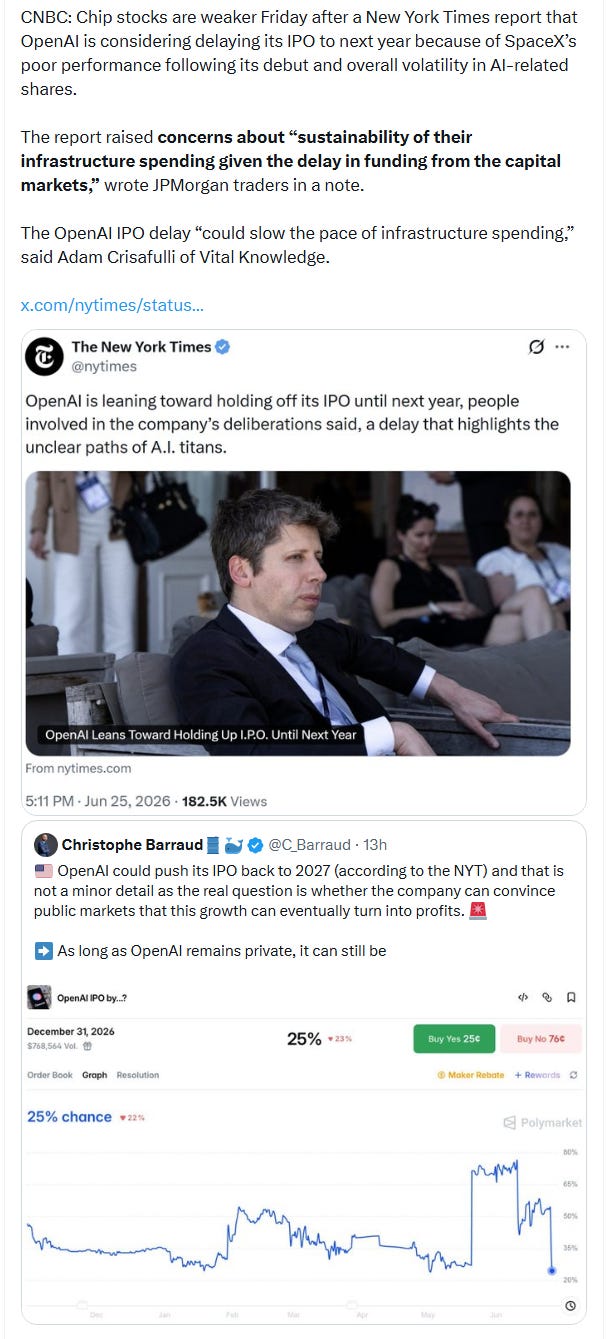

Semiconductors and AI infrastructure names were under pressure after reports that OpenAI may delay its IPO until 2027 raised more questions about AI funding, infrastructure spending, and crowded positioning. That pressure remained throughout the session with the PHLX Semiconductor Index falling 5.3% to cap its worst week since March 2025. Shares of Micron declined more than 6%.

Still the headline indices recovered to unchanged levels in the first hour, but they would make little progress from there in either direction. The S&P 500 finished -0.05%, Nasdaq -0.24%, Dow Jones Industrial Average (DJIA) -0.09%, and Russell 2000 +0.07%.

The index moves though again masked rotation beneath the surface. While the SPX and Nasdaq both fell for a fifth straight session, the longest streaks since January and August respectively, the Russell 2000 (RUT) and equal-weighted SPX both closed at all-time highs.

Six of eleven S&P 500 sectors were higher for a fourth straight day. Health Care led with its best week since June 2022, while Consumer Discretionary, Real Estate, Staples, Utilities, and Financials also gained.

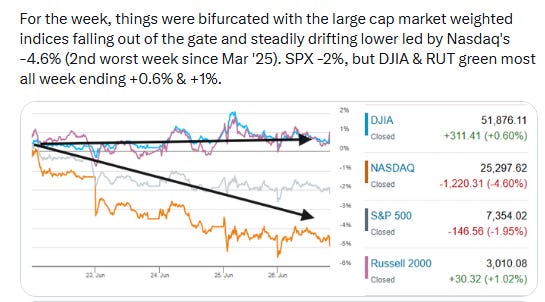

For the week it was a similar story with the large cap market weighted indices falling from the start and steadily drifting lower led by Nasdaq's -4.6% (second worst week since March 2025). The S&P 500 ended -2%, while the DJIA and RUT were green most all week ending +0.6% and +1% respectively.

The “other 493” were helped this week by a continued easing in interest rates with 2-year and 10-year yields both lower for a fourth straight session. Elsewhere, the dollar eased for a second day, WTI remained near the lowest levels since the start of the Iran conflict, gold and copper continued their two-day bounce from recent lows, natural gas remained rangebound, and bitcoin held near its lowest levels since October.

As a final note, as I am wrapping up, crossing the wires is a report that US Central Command said "forces conducted strikes against Iran...as a powerful response to yesterday’s attack on a commercial ship that was transiting the Strait of Hormuz." Iran has vowed to respond. If this escalates I’ll have more on X and in Sunday’s Week Ahead.

Some market commentary:

The most sensible strategy “is to maintain well-diversified portfolios across geographies, styles, sizes, companies, and sectors,” said David Manso, chief investment officer at CaixaBank AM. “In a couple of weeks, the earnings season will kick off, and leading indicators are pointing in the right direction. We expect corporate results to become a positive catalyst.”

“Technology remains a crowded trade, positioning is relatively tight, and that makes the sector more sensitive to negative news flow or sharp moves in individual names,” said Francisco Simon, European head of strategy at Santander Asset Management.

“This is a hedge-fund unwind,” said Jay Hatfield, CEO of Infrastructure Capital Advisors. Hatfield clarified that in reality there are two separate rotations unfolding simultaneously in the U.S. equity market this week: the shift away from secular growth stocks and into cyclicals, and the turn away from semiconductors and toward the “Magnificent Seven,” software names and other hard-hit tech heavyweights like Netflix.

“Apple’s price hikes illustrated one of the big downsides of AI — namely, that a lot of other products use microchips, and their costs are soaring. That’s the sort of negative externality that’s difficult to just wave away once it materializes.” — Cameron Crise, Macro Strategist, Markets Live.

After a remarkable rally in recent months, investors have become increasingly sensitive to stretched valuations and rising infrastructure costs associated with AI, according to Fawad Razaqzada at Forex.com. “While some degree of profit-taking was perhaps inevitable, the latest moves also raise broader questions about whether expectations for the sector have simply run too far ahead of commercial reality,” he said.

“This is a market that we think is quite set up to test conviction. We have this flavor of market leadership in specifically semiconductors and memory chip leaders,” said Julia Hermann, global market strategist New York Life Investment Management, on CNBC’s “Closing Bell” on Thursday afternoon. “This is a structurally more volatile flavor of tech than we saw in the Magnificent Seven for the past several years.” Hermann added: “Then you pair that with an astonishing repricing in Fed expectations — not just the what, but the why of why the Fed might be hiking next — and you have this environment, which is candidly a recipe for volatility.”

At Gabelli Funds, John Belton says he would characterize the recent tech moves as more of a “pause” than a “selloff.” Chipmakers are still within a striking distance of all-time highs while software firms have given back the majority of a rally staged earlier in the quarter. Meanwhile, megacaps have failed to keep up with the market despite strong fundamentals. “Are the hyperscalers set up to be left behind in the AI era? I would not count them out and believe that they are building platforms which will help drive AI diffusion across the economy for years to come,” Belton added.

“Investor sentiment has turned increasingly pessimistic amid the technology selloff and sharp rotation, but the broader market is telling a different story,” said Mark Hackett at Nationwide. “Rather than the start of a major downturn, this looks more like a period of consolidation beneath the surface.” He noted that the fundamental backdrop remains supportive, with consumers still spending, businesses investing, and earnings expectations continuing to move higher. While the gyrations in tech can be unsettling, Hackett says periods like this often set the stage for the next leg of the bull market.

In today’s Markets Update:

A look under the hood at another bifurcated session for US equities including a review of the renewed selloff in semiconductors and AI infrastructure names and onsemi’s sharp drop after announcing its all-stock deal for Synaptics.

A look at the other side of the technology trade, where software stocks rebounded sharply, and Apple and Microsoft recovered from Thursday’s losses.

A review of sector performance.

Updated technical charts including weekly analysis across the SPX, Nasdaq, Russell 2000, equal-weighted SPX, Treasury yields, volatility gauges, WTI crude, the dollar, gold, copper, natural gas, and bitcoin, including the contrast between weaker charts for the SPX/Nasdaq and stronger for the Russell 2000 and equal-weighted SPX.

A look at the rates backdrop, the softening in Fed funds expectations, and comments from Fed presidents Williams and Kashkari.

A review of volatility conditions, including VVIX falling to its lowest close of the week, and the 1-day VIX rising to the highest level since the day before the June FOMC.

A look at several market structure and positioning issues including SpaceX stock and bond weakness, BofA fund-flow data, record M&A activity, and Dean Curnutt’s warning about leverage in single-stock and semiconductor ETFs.

A look at the May advance goods trade deficit and Goldman’s cut to its Q2 GDP tracking estimate to 2.2%.

A look ahead to next week’s calendar, including US economic data in the holiday shortened week, Chair Warsh’s appearance, and a light SPX earnings calendar.