Markets Update - 6/30/26

A look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for tomorrow.

Quick Summary:

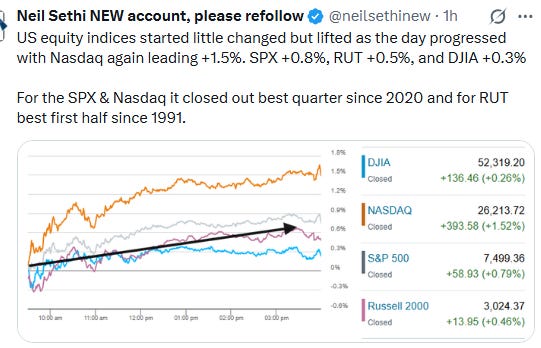

US equity indices opened the Tuesday session little changed after the S&P 500 and Nasdaq snapped 5-day losing streaks with a solid Monday performance driven by growth stocks as discussed in last night’s update.

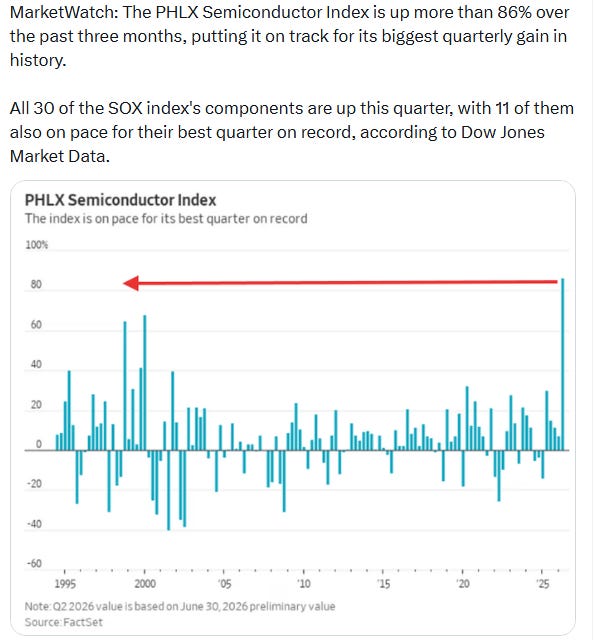

The indices though would push higher throughout the session, led again by growth stocks with a more concentrated focus on the Technology sector Tuesday as the PHLX Semiconductor Index would gain 3.9% on the day to cap its best quarter on record (see post below).

That outperformance would see the Nasdaq lead +1.5%, the S&P 500 (SPX) would finish +0.8%, the small cap Russell 2000 +0.5%, and the Dow Jones Industrial Average +0.3%.

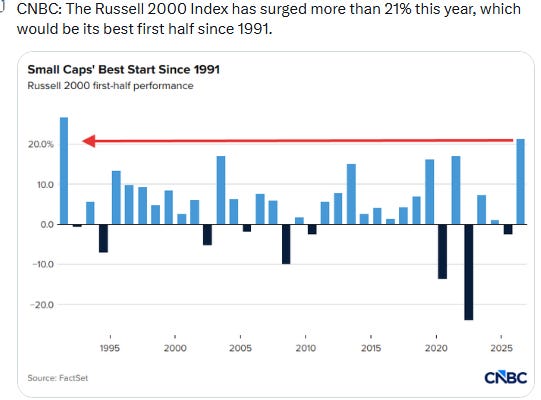

That capped a stellar quarter for US stocks with the SPX and Nasdaq seeing their best gain since the second quarter of 2020. The Russell 2000 completed its best first half since 1991, the Dow since 2021.

Economic data supported a resilience narrative, with job openings coming well above expectations seeing Treasury yields reverse much of last week’s softening. Consumer confidence also saw a slight rebound but was mixed with improved expectations offsetting weak present conditions.

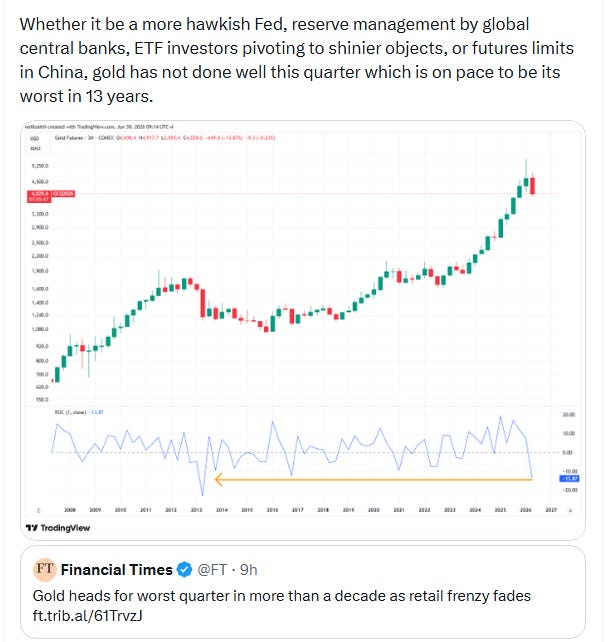

Elsewhere, the VIX and VVIX volatility indices both continued to ease, while WTI crude traded sideways for a fourth session near the lowest levels since the start of the Iran conflict after its worst quarter in six years. The dollar stabilized after three down sessions, gold remained near recent lows after its worst quarter since 2013, but copper continued to rebound.

Some market commentary:

“The markets have proven to be the ultimate grinder as they keep crushing it despite a lot of hand-wringing that has gone along with this incredible rally that has endured deep selloffs, the Iran war and a number of other outside influences,” JJ Kinahan at Cboe Global Markets said.

“Despite some twists and turns, the path of least resistance for stocks broadly remained up and to the right for much of the last three months,” said Jeff Buchbinder at LPL Financial. “While stock market enthusiasm has increased, we do not believe it has crossed the threshold into outright irrational exuberance.” Some sentiment surveys are stretched, but others remain near long-term averages while positioning has begun to moderate, he added. Meantime, Buchbinder noted that other indicators – including record margin debt and highly overbought conditions in key leadership groups like semiconductors – point to a market with an overly optimistic outlook.

“Strong fundamentals and powerful structural themes such as AI can justify elevated valuations for a while, but they do not eliminate the typical ups and downs,” he said. “Rather than signaling the end of the bull market, current conditions appear more consistent with a mature bull market that may be due for a pause. We remain constructive on equities.”

“For me the lesson of the first half of 2026 is that earnings matter more than just about anything, except for maybe interest rates,” said Tim Holland, chief investment officer at Orion. Barring an increase in hostilities between the U.S. and Iran, Holland expects the bull market to continue to broaden for the rest of the year, with investors moving more into cheaper areas of the market.

“The world continues to focus on the AI capex build out and AI trade, and I think rightly so, but if you look under the hood of the market, what’s been working year to date, and at least for the month of June as well is value stocks as opposed to growth stocks,” he added. “Interest rates are probably going to be a little elevated, which tends to be a headwind for higher price growth stocks, but tends to be a tailwind for economically sensitive stocks and the like.”

A rotation into cyclical corners could have legs especially if oil prices keep heading toward levels prior to the war and the economy remains resilient, according to Mona Mahajan at Edward Jones. She would recommend both large-cap stocks, which offer exposure to the AI story, and mid-cap shares, which could continue to do well if the broadening theme delivers.

In a note on Tuesday morning, strategists at UBS said that, despite an optimistic start to the week, concerns over the sustainability of AI capex growth remain. “We believe that exposure to AI-related stocks will remain a key differentiator for equity market performance over the long run, but we also believe diversification, both within and beyond AI, is essential,” they wrote. “This means that investors can consider more defensive areas within the AI complex, such as data center operators and select payment companies, as well as other structural trends.”

In today’s Markets Update:

A deeper look at Tuesday’s stock and sector breakdown, including continued leadership from Technology, semiconductors, large-cap growth, and weakness in Real Estate and defensive sectors as well as a look into June’s sector performance.

A closer look at key company movers and corporate developments.

Updated technical charts across the SPX, Nasdaq, Russell 2000, equal-weighted SPX, Treasury yields, volatility gauges, WTI crude, the dollar, gold, copper, natural gas, and bitcoin, including daily and monthly chart context where relevant.

A look at the rates and Fed backdrop, including the move higher in Treasury yields after the stronger job openings data and the latest analyst views on whether the Fed is likely to hike this year.

A review of market breadth and participation, including the continued weakness in NYSE positive volume despite positive headline index moves.

A look at volatility and market structure, including VIX, VVIX, 1-day VIX, the quarter-end options collar discussion, and the impact of leverage, financing costs, and low-volatility positioning.

A review of cross-asset trends, including oil, gold, the dollar, copper, natural gas, and bitcoin.

A look at broader market commentary, including views on the durability of the rally, earnings, AI, diversification, the “Axios put”, and the balance between strong momentum and signs of a more mature bull market.

A look ahead to Wednesday’s calendar, including global economic data, central bank speakers, and corporate earnings.