Markets Update - 7/10/26

A look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for next week.

Quick Summary:

US equity indices started the Friday session struggling for direction with the AI-trade cooling off despite (or perhaps because of) the Nasdaq ADR debut of South Korean memory chip heavyweight SK Hynix (SKHY) which raised $26.5 billion in its offering, the largest ever for a foreign firm as discussed in the morning update.

Traders were also weighing the latest developments in the Mid-East including US officials confirming that the US and Iran will continue “technical talks” despite the recent air attacks from both sides, with the official adding that the US is committed to finding a solution to the Middle East conflict. Markets briefly turned lower during the morning after President Trump said the US considers the Iran ceasefire over, but sentiment steadied as he also said talks would continue and Axios reported that the US and Iran are expected to hold another round of talks in Switzerland next week.

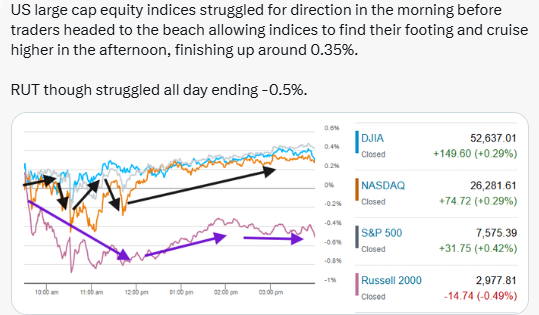

After a choppy morning, the volatility would lighten considerably in the afternoon, perhaps with traders heading out to start their weekends early, which saw large cap indices drift higher to finish the session modestly higher, ending near the best levels of the day. The S&P 500 gained 0.4%, the Nasdaq Composite rose 0.3%, and the Dow Jones Industrial Average added 0.3% The Russell 2000 though would struggle all session pressured by a renewed rise in bond yields and finish down 0.5%.

Oil prices though remained subdued, helping to broaden participation, with 10 of 11 S&P 500 sectors finishing higher. Technology was one of those positive sectors, although semiconductors were more muted than on Thursday with the PHLX Semiconductor Index finishing little changed, even as Nvidia rose roughly 4% and SK Hynix’s ADR gained about 13%.

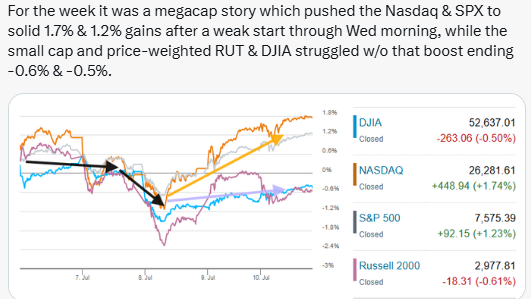

For the week, the S&P 500 and Nasdaq Composite both gained more than 1%, while the Russell 2000 and Dow Jones Industrial Average finished modestly lower.

There was no notable US economic data Friday.

After a relatively light week, attention turns to next week’s very heavy calendar including the start of Q2 earnings season, led by the major banks, a flurry of US economic data points including June CPI, PPI, retail sales, and industrial production, and a stream of Fed speakers highlighted by Kevin Warsh testifying before Congress.

All of the above covered in more detail in the subscriber section.

Some market commentary:

“What remains to be confirmed is whether growth can hold up despite that pressure, with the AI capex cycle continuing to support investment, revenues and earnings,” said Florian Ielpo, head of macro at Lombard Odier Investment Managers. “Expectations are high, but the real test is whether earnings can keep validating the expansion story.”

“The muted stock market reaction to the re-escalation of Iran tensions this week is prime evidence that the market is looking past geopolitical tensions,” said Clark Bellin, president and chief investment officer at Bellwether Wealth.

“While there are pockets of the market exhibiting lottery-like behavior, the broader market remains sober and skeptical,” Mark Hackett at Nationwide said. “It is far from the kind of complacency that typically leads to a sustained drawdown.”

“The street has priced in exceptional earnings growth, and now management teams have to prove those expectations were warranted,” he said.

What’s interesting this quarter, Kenny Polcari at SlateStone Wealth noted, is that we haven’t seen the usual wave of warnings. In fact, more S&P 500 companies have issued positive than negative guidance — a departure from the historical pattern. “That tells me management teams are either genuinely confident or confident enough not to reset expectations ahead of reporting,” he said.

Another aspect of the upcoming results is that expectations are elevated, but “concentrated,” according to Nicole Inui at HSBC. Most of the expected earnings growth comes from a handful of sectors where visibility is high, she said. “Despite lofty expectations, we are not worried,” Inui added (this was covered extensively in last week’s Week Ahead).

In today’s Markets Update:

A deeper look at Friday’s stock and sector breakdown, including the broad but shallow sector participation.

A closer look at key company movers and corporate developments.

Updated technical charts across the SPX, Nasdaq, Russell 2000, and equal-weighted SPX, including daily and weekly chart context.

A look at the rates and Fed backdrop, including Treasury yields, Fed hike expectations, and discussion around the June FOMC minutes.

A review of market breadth and participation, including sector breadth, large individual winners and losers, and the week’s split between megacap leadership and small-cap weakness.

A look at volatility and market structure, including VIX, VVIX, 1-day VIX, and the gap between single-stock and index implied volatility.

A review of cross-asset trends, including WTI crude, the dollar, gold, copper, natural gas, and bitcoin.

A look at broader market commentary, including the upcoming earnings season, first-half winners, sector earnings expectations, and pairwise correlation.

A look ahead to next week’s very heavy calendar, including US economic data, SPX earnings, and Fed speakers.