Markets Update - 7/1/26

A look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for tomorrow.

Quick Summary:

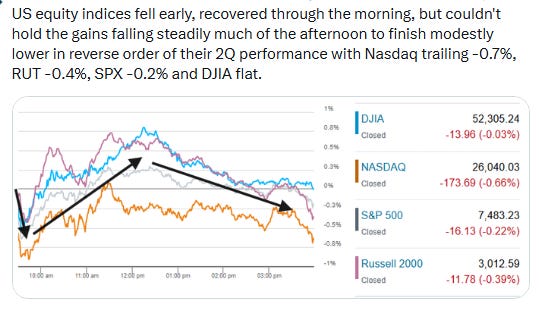

US equity indices opened the Wednesday session modestly lower after the S&P 500 and Nasdaq completed their best quarter since 2020 and the Russell 2000 small cap index its best first half since 1991 as discussed in last night’s update.

A mid-morning rally was turned back in the afternoon and stocks would finish broadly lower at the index level (but not so under the surface as discussed below). The S&P 500 finished -0.2% and the Nasdaq Composite -0.7%, while the Dow Jones Industrial Average finished essentially flat after touching another intraday record high. The Russell 2000 slipped -0.4% after also reaching another intraday record high. In contrast to the headline index, the S&P 500 Equal Weight Index would finish +0.2% at a new record high.

A major drag on the headline indices was a sharp pullback in semiconductors after their huge first-half and second-quarter run. The PHLX Semiconductor Index fell 6.3%, with weakness across memory, chip equipment, and AI-infrastructure names, including Micron, Sandisk, Nvidia, Broadcom, Corning, and KLA.

Still, the index-level damage was relatively contained as strength in other large-cap technology and growth names and other sectors helped offset the semiconductor weakness, with Meta surging after reports it plans to build a cloud business selling access to AI computing infrastructure, and Apple, Microsoft, Amazon, Tesla, Palantir, Nike, FactSet, Coinbase, Robinhood, and General Mills all seeing solid advances (full details in the subscriber section).

The macro backdrop remained supportive. While coming in under expectations, the ADP employment report showed solid private-sector job creation in June, capping the best three-month stretch for hiring since January of last year, while the ISM’s manufacturing PMI remained close to a four-year high and showed manufacturing activity expanding for a sixth straight month. Importantly, the prices-paid component cooled sharply as the pullback in oil helped ease inflation concerns (full details on those at the linked blogposts).

Traders were also on high alert for headlines out of Portugal where Fed Chair Kevin Warsh participated this morning on a panel discussion at the ECB Forum in Sintra. That was not to be forthcoming with all of the participants batting away any question that even sniffed of providing any indication as to what they might do next, an unfortunate precedent if this is what we have to look forward to. Warsh did at least say inflation risks have come down but also repeated that the Fed will deliver price stability.

Oil also moved lower on reports of positive US-Iran discussions and improved traffic through the Strait of Hormuz but Treasury yields and the dollar pushed higher on the relatively firm economic data. More on bond and commodity markets in the subscriber section.

Some market commentary:

“There could be a few valid factors that may explain the recent [semiconductor] share price pullback, but likely we have not yet reached the peak of this cycle,” Nomura analyst Aaron Jeng wrote. “A pullback is healthy following such a surge over such a short period, particularly when we see some risks that have to be digested, e.g., the likely biggest-ever component supply mismatch, hyperscalers’ 2027F free cash flow (FCF) issue, execution of many cutting-edge technologies beyond 2027F, and macro risks related to a yield uptrend,” he said.

“The ‘Great Rotation’ trade persists into [the third quarter] as the blue boring names of the Dow Jones continue to attract inflows directly from recent profit taking money from tech stocks,” Jeff Kilburg, founder and CEO of KKM Financial, told CNBC. “This is extremely healthy and underscores the broadening breadth of equities for this continued bull market in its fourth year.”

JPMorgan Global Markets Strategist Nikolaos Panigirtzoglou said, “after reaching extreme levels earlier this year, there are currently signs of retreat in retail investors’ leverage in both options and margin accounts, presenting a potential headwind for tech stocks going forward.”

“The story of the past six months is the market going all-in on AI infrastructure, but now people are asking if this is sustainable and if we should be worried,” said CJ Muse, senior managing director and technology analyst at Cantor Fitzgerald.

Heading into the second half of the year, Paul Hickey, Bespoke Investment Group co-founder, said that he still likes the sector, but it may be getting a bit too hot. “Over the long term, we still like the semis, but I wouldn’t be aggressive towards it here. This bull market is an AI-driven bull market, that’s the theme. If this bull market is going to continue, it’s going to be led by tech and probably semis, but they don’t have to beat consistently, and you can’t go in that kind of pattern for good,” he said on CNBC’s “Closing Bell: Overtime” Tuesday afternoon. “So I think in that respect they’ve gotten a little bit…extended. So I would maybe take a breather here.”

“At a minimum, [Warsh’s] comments provided no fuel for speculation on a near-term July rate hike, and in our view suggest the new Fed chair – while keeping all options open meeting by meeting – does not currently see cause for an immediate hike,” said Krishna Guha at Evercore.

“With oil prices back around their pre-Iran war levels, the [ISM] prices paid index – which fell in June – probably has further to fall,” said Ariane Curtis at Capital Economics.

“A number a bit above 100,000 [in tomorrow’s NFP report] and stability in the unemployment rate is the best-case scenario for this market, as it reinforces solid economic growth, but it won’t make rate hikes more likely,” said Tom Essaye at The Sevens Report.

In today’s Markets Update:

A deeper look at Wednesday’s stock and sector breakdown, including the pullback in semiconductors, the resilience in other large-cap growth names, and the relative strength in several sectors including Communication Services and Financials.

A closer look at key company movers and corporate developments.

Updated technical charts across the SPX, Nasdaq, Russell 2000, equal-weighted SPX, Treasury yields, volatility gauges, WTI crude, the dollar, gold, copper, natural gas, and bitcoin.

A look at the rates and Fed backdrop, including the move higher in Treasury yields and updated Fed hike expectations.

A review of market breadth and participation, including the split between headline index weakness and broader participation and the improvement in NYSE positive volume.

A look at volatility and market structure, including VIX, VVIX, 1-day VIX, positive gamma, and positioning commentary from Tier1Alpha, Barclays, Citadel, and BoA.

A review of cross-asset trends, including oil, crude inventories, the dollar, gold, copper, natural gas, bitcoin, and Goldman’s latest copper framework.

A look at broader market commentary, including views on semiconductors, AI, the “Great Rotation,” retail leverage, equity flows, BoA’s SPX target, and JPMorgan’s setup for Thursday’s jobs report.

A look ahead to Thursday’s calendar, including global economic data, central bank speakers, and corporate earnings and Morningstar’s NFP preview.