Markets Update - 7/14/26

A look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for tomorrow.

Quick Summary:

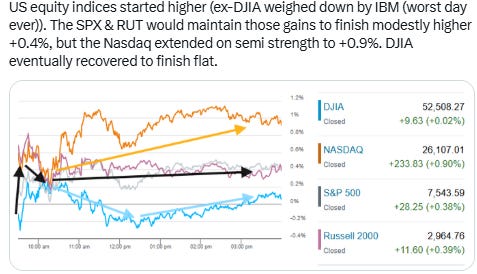

US equity indices started the Tuesday session higher, turning around from earlier losses after a much cooler than expected CPI report eased Fed rate hike concerns despite a continued rise in crude prices adding to a bounceback in semiconductor shares as detailed in the morning update.

The S&P 500 and Russell 2000 would maintain those gains trading in a narrow range most of the day to finish +0.4%. The Nasdaq Composite though would extend on the semiconductor strength to end +0.9%. In contrast the Dow Jones Industrial Average would spend most of the session in negative territory weighed down by a record loss for IBM struggling to a flat finish.

The June CPI report showed headline and core prices falling the most month-over-month since April 2020 on a broad softening in price pressures. The report pulled Treasury yields lower, especially at the front end most influenced by Fed rate expectations, as pricing for a July Fed hike withered, though markets continued to price 80% odds of a hike by the end of the year. Fed Chair Kevin Warsh’s testimony before Congress reiterated the Fed’s focus on restoring price stability (more in the subscriber section).

Semiconductors rebounded after Monday’s selloff, with the PHLX Semiconductor Index rising 2.5% and strength across names including Nvidia, Micron, Lam Research, Applied Materials, Teradyne, and SK Hynix’s ADRs. The rebound helped Technology lead the sector scoreboard despite the sharp decline in software names led by IBM after weaker-than-expected guidance.

Big bank earnings were also in focus to start Q2 reporting season, with Goldman Sachs leading after a strong beat, while JPMorgan and Bank of America also gained, while Citigroup and Wells Fargo moved lower despite topping expectations.

Oil remained a key macro focus, with WTI briefly moving above $80 before settling just under after President Trump backed away from a proposed fee on Strait of Hormuz shipments instead calling for “Trade and Investment Deals” in the United States as repayment. Still he reiterated a blockade on vessels transiting to or from Iran (see post below).

Some market commentary:

“The well-behaved CPI print likely lowers pressure on the Fed to hike soon, but the reignition of hostilities in Iran means the prospect of hikes is far from over,” said Kay Haigh at Goldman Sachs Asset Management. “Although a path remains for rates to stay unchanged this year, the reescalation of the conflict has narrowed it.”

“The very benign June CPI inflation report gets Warsh off the hook in terms of pressure to hike near-term and allows him to position the Fed as resolutely committed to bringing inflation back to target without fueling expectations of a July move,” economists at Evercore ISI wrote in a note to clients, referring to the Federal Open Market Committee meeting scheduled for July 28-29.

“Softer than expected CPI is a big relief,” said Tiffany Wilding at Pacific Investment Management Co. “While today’s report will not eliminate discussion of further tightening entirely, it should effectively remove a July rate hike from consideration.”

“Today’s report provides breathing room, not an all-clear,” said Bret Kenwell at eToro. “While inflation has cooled, it has not disappeared.”

The well-behaved CPI likely lowers pressure on the Fed to hike soon, but hostilities in Iran mean the prospect of hikes is far from over, noted Kay Haigh at Goldman Sachs Asset Management. Although a path remains for rates to stay unchanged this year, the re-escalation of the conflict has narrowed it, he added.

“Tuesday’s weaker-than-expected CPI print suggests the inflation surge driven by the Iran war is fading, but this may just be a temporary relief as tensions have escalated in recent days,” said Skyler Weinand, chief investment officer at Regan Capital. “The weaker inflation data likely keeps the Fed on hold for now and reduces any rate hike odds, but we remind investors that almost every communication that has emanated from Chair Warsh during his short tenure so far has been hawkish.”

“Warsh is looking to get consumer prices under control and the best tool the Fed currently has is raising interest rates,” he added.

“Warsh reinforced the Fed’s inflation-fighting credibility without committing policymakers to a particular course before additional economic data become available,” said Brian Therien at Edward Jones.

In today’s Markets Update:

A deeper look at Monday’s stock and sector breakdown, including renewed weakness in semiconductors, pressure on the megacap growth sectors, and rotation into Energy, defensive sectors, Financials, and Real Estate.

A closer look at key company movers and corporate developments.

Updated technical charts across the SPX, Nasdaq, Russell 2000, and equal-weighted SPX.

A look at the rates and Fed backdrop, including the move higher in Treasury yields, updated Fed hike expectations, Governor Waller’s market moving comments, and additional Fed-related commentary.

A review of market breadth and participation, including increased stock dispersion, large individual winners and losers, Goldman’s momentum analysis, and the share of SPX stocks above their 200-DMAs.

A look at volatility and market structure, including VIX, VVIX, 1-day VIX, and the latest moves in volatility expectations.

A review of cross-asset trends, including WTI crude, the dollar, gold, copper, natural gas, and bitcoin.

A look at broader market commentary, including AI and semiconductor momentum, earnings expectations, strategist views on market leadership, BofA’s Hartnett, leverage/funding pressure, a resurgence of the carry trade, CPI expectations, ETF launches, economic indicators including jobs and freight demand, sentiment, and private credit.

A look ahead to Tuesday’s calendar, including US economic data, Fed speakers, SPX earnings, and key ex-US data.