The Week Ahead - 9/22/24

A comprehensive look at the upcoming week for US economics, equities and fixed income

If you're a new reader or maybe one who doesn’t make it to the end feel free to take a second to subscribe now (although then you’re missing my hard hitting analysis!). It’s free!

Or please take a moment to invite others who might be interested to check it out.

Also please note that I do often add to or tweak items after first publishing, so it’s always safest to read it from the website where it will have any updates.

As a reminder, some things I leave in from prior weeks. Anything not updated is in italics. As always apologize for typos, errors, etc., as there’s a lot here, and I don’t really have time to do a real double-check.

The Week Ahead

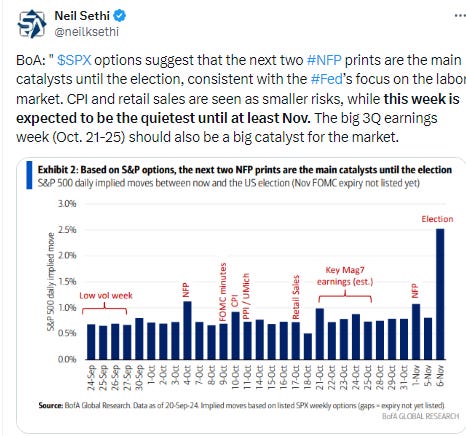

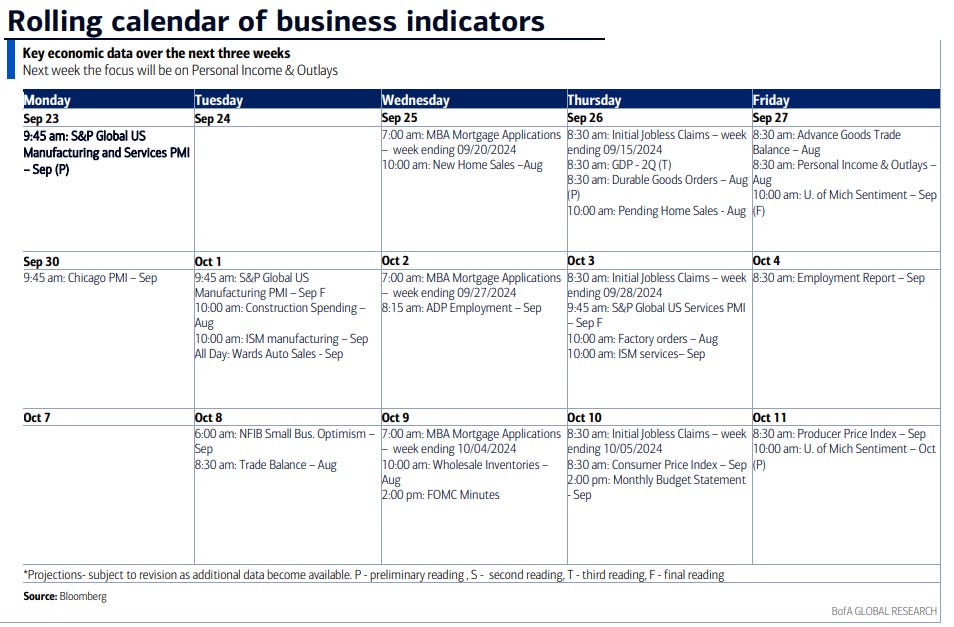

It’s a busy week, but as BoA notes below still “the quietest until at least November,” with a lack of any true major catalysts (at least on the calendar). The highlight (perhaps outside of comments from Powell noted below) has to be the Aug personal income and spending report (which includes PCE prices, the Fed’s favorite inflation metric) on Friday. While coming late in the month, it remains our most wholistic look at not only inflation but also incomes and spending. That comes Friday, but we’ll start the week of with flash PMI’s which of late have been market moving. Other reports include July home prices, Aug new home sales, pending home sales, goods trade balance & durable goods orders, Sept Conference Board & U of Mich consumer confidence reports, the third and final Q2 GDP estimate (along with benchmark revisions which go back to 2019), and weekly jobless claims.

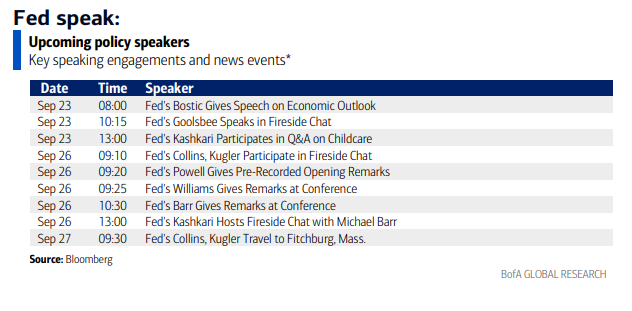

And FOMC speakers will be back out in force. Perhaps we’ll get some more color on who the various dots are, which as one of BoA’s Fed analysts noted to me this weekend, is how they think about them on the Dove-Hawk spectrum (which makes sense as in many cases their commentary is a little obscure). We’ll hear from Barr, Bostic, Bowman (three times), Collins (twice), Cook, Goolsbee, Kashkari (twice), Kugler (three times), Williams and the Chair himself who’ll deliver opening remarks via pre-recorded video at the U.S. Treasury Market Conference at 9:20 am ET on Thursday. I would have in the past said you need to pay particular attention to Williams given his influential role as the NY Fed Pres, but you would have been wrongfooted listening to him ahead of the last FOMC meeting. It seems it's Jerome Powell's FOMC and the rest of the committee is fine with that (outside of Bowman).

Treasury auctions will also be heavier as we end the Sept schedule with 2’s, 5’s & 7yr's on Tues, Wed & Thurs ($69, $70 & $44bn) resp. These were mixed last month with the first two decent but the last fairly week, all seeing strong foreign demand but tepid domestic demand. We’ll see if we get something different this week.

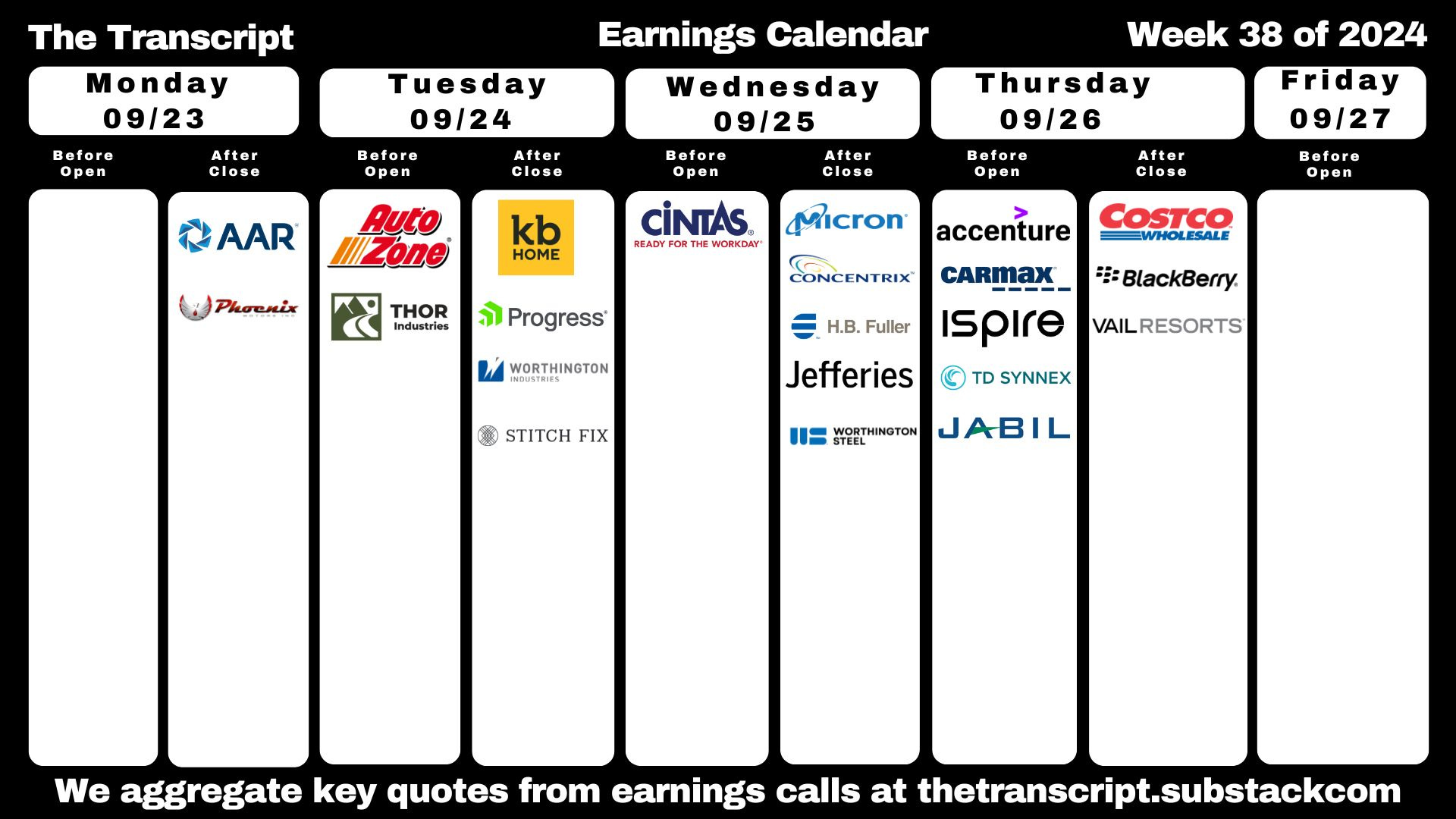

As noted two weeks ago, earnings will continue to come in at a modest pace until we get to the unofficial kickoff to 3Q season Oct 11th w/JPM starting off the big financials. This week we’ve got 7 SPX co’s reporting 3Q results w/two >$100bn (after none last week) in Costco & Accenture.

From Seeking Alpha (links are to their website):

Earnings spotlight: Tuesday, September 24 - AutoZone (AZO), KB Home (KBH), THOR Industries (THO), and Stitch Fix (SFIX).

Earnings spotlight: Wednesday, September 25 - Micron Technology (MU) and Jefferies (JEF).

Earnings spotlight: Thursday, September 26 - Costco Wholesale (COST), Accenture (ACN), Jabil (JBL), and CarMax (KMX). See the full earnings calendar.

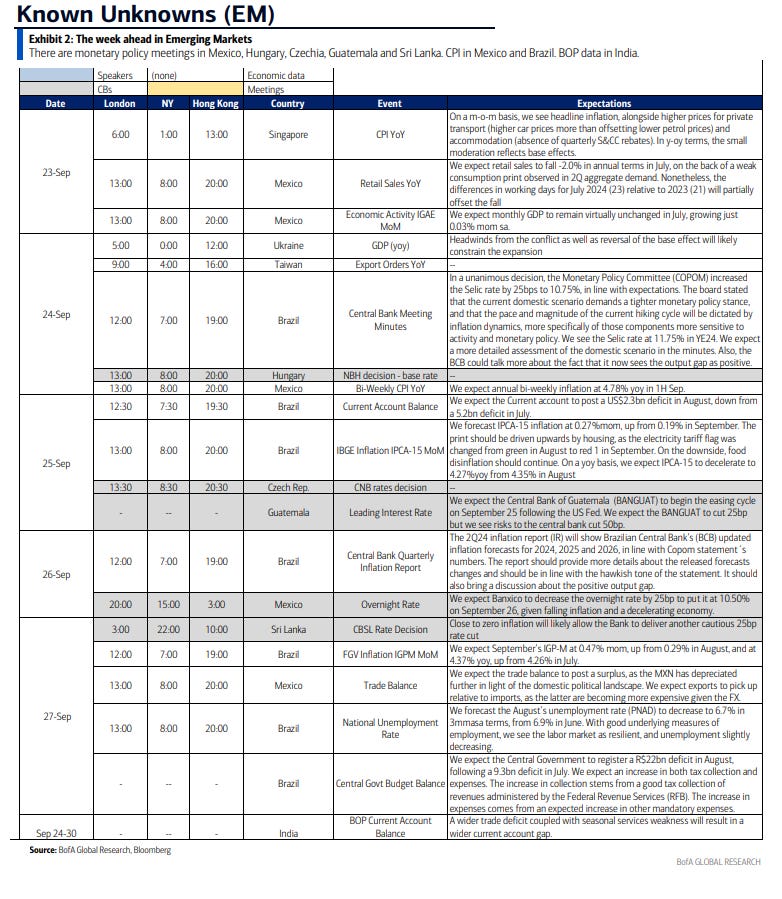

Ex-US, the OECD will reveal new economic forecasts on Wednesday, central banks in Switzerland, Sweden, Mexico, Hungary, Czech Republic may deliver rate cuts, while their Australian, Nigerian & Morocco counterparts are anticipated to stay on hold, and we’ll get flash PMI’s as well as data on Japan, France & Spain inflation, Canada GDP, Germany’s Ifo confidence index, and as in the US we’ll get plenty of central bank speakers.

In Canada, GDP data for July and a flash estimate for August are expected to show weak growth in the third quarter, likely below the Bank of Canada’s forecast of 2.8% annualized expansion. Meanwhile, the central bank’s governor, Tiff Macklem, will speak at a banking conference in Toronto.

The Reserve Bank of Australia is expected to keep its cash rate target unchanged at 4.35% when the board meets on Tuesday, with the focus likely to fall on whether Governor Michele Bullock retains her hawkish tone after solid labor figures prompted traders to pare bets on a December rate cut. Authorities will have to wait until Wednesday to see if Australian inflation cooled for a third month in August. Japan gets fresh inflation data with the release Friday of Tokyo consumer prices, which are expected to have risen at a pace exceeding the Bank of Japan’s 2% target in September. Purchasing manager indexes for September are due from Australia and India on Monday and from Japan a day later.

Four central bank decisions are scheduled in Europe, where investors may question the appetite of policymakers to follow in the footsteps of the Fed with a half-point cut. That’s certainly the case with the Swiss National Bank on Thursday. While a majority of economists foresee a quarter-point move, observers do reckon the US reduction has increased the chances of a step of the same size as officials confront the persistent strength of the franc. This is the final meeting for President Thomas Jordan, whose term concludes at the end of the month. The previous day, Sweden’s Riksbank is expected to lower borrowing costs by a quarter point for the third time this year, taking the rate to 3.25%, and to outline a path to additional cuts. The current guidance is for two or three more moves in 2024 — including on Wednesday. Policymakers talked about a half-point cut at last month’s meeting, and while that discussion could come up again, most economists believe the central bank would more likely wait until November to do a bigger move. In Eastern Europe, meanwhile, both the Hungarian central bank on Tuesday and its Czech counterpart on Thursday are expected to deliver quarter-point reductions.

In the euro zone and the UK, an initial look at purchasing managers indexes for September will be released on Monday, signaling the state of private-sector activity at the end of the third quarter. With Germany’s weakness a focal point for investors, the Ifo business confidence gauge will be a highlight on Tuesday, the same day Bundesbank President Joachim Nagel is due to speak on the economy. New forecasts from the country’s economic institutes are scheduled for Thursday. Readings of French and Spanish inflation for September will draw attention on Friday, hinting at the overall outcome for the region due the following week. Economists predict both countries’ readings will drop below 2%. Aside from Nagel, more than half a dozen euro-zone policymakers are scheduled to speak, including European Central Bank President Christine Lagarde, chief economist Philip Lane, and Spain’s new central bank chief Jose Luis Escriva.

Across the African continent, various central bank decisions are also scheduled:

Nigerian officials on Tuesday will likely pause a tightening cycle that’s lifted the rate to 26.75% from 11.5% in just over two years. They’ll be encouraged by inflation cooling to a six-month low as they weigh the impact of floods in the country and a steep increase in gasoline costs on price growth.

Morocco’s central bank will probably hold its rate at 2.75% to allow time for June’s surprise cut to seep through the domestic market. The kingdom needs low rates to facilitate investment and contain unemployment. It has massive investment plans for reconstruction of earthquake-hit areas and infrastructure ahead of the FIFA World Cup in 2030.

Brazil watchers will have a lot to digest, with minutes of the central bank’s September rate meeting and a quarterly inflation report taking center stage. The former may provide a more detailed policy road-map after a quarter-point hike on Sept. 18, to 10.75%, while the latter updates all manner of economic estimates and scenarios. Look for the BCB to mark up forecasts for inflation, the key rate, and GDP growth. Rounding out the week for Latin America’s biggest economy, jobs data will likely show Brazil’s labor market remains at historically tight levels while mid-month inflation may have stalled near the top of the central bank’s target range. Argentina is slated to post GDP-proxy readings for July, which may build support for the view that the economy is past its 2024 nadir and is beginning a second-half recovery. In Mexico, downshifting domestic demand may see another set of soft retail sales prints — on the heels of June’s negative annual and monthly readings — while mid-month inflation data aren’t likely to provide policymakers with a slam dunk cause to cut or hold when Banxico meets a few days later. The early consensus expects a quarter-point cut to 10.5%, though some analysts see a possible half-point reduction to stay on pace with the Fed.

And here’s BoA’s cheat sheets for the upcoming week.

And here’s a calendar of 2024 major central bank meetings.

Market Drivers

So let’s go through the list of items that I think are most important to the direction of equity markets:

Fed/Bonds

As noted previously this was one of the sections that had grown unwieldy, so I’ve really pared it down. Given I provide daily updates on Fed expectations, Fedspeak, and analyst thoughts on the Fed, it’s duplicative (and time consuming) to gather it all again so, again, I encourage you to look at those (the daily posts) for updates. I will just give more of a quick summary.

I noted last week,

While we didn’t get a cool CPI, as noted in the Thurs summary we did get a Timiraos (and an FT (perhaps they’re trying to diversify)) article soon thereafter, signaling that 50bps was a serious possibility. You can read into that what you want (it’s definitely murky), but what many of the more accurate forecasters I follow think is that Powell wants a 50bps cut but he’s not sure he can get the FOMC to follow without a bunch of dissents (which he definitely doesn’t want with a big cut right in front of an election (I think it has to be unanimous which is a heavy lift))…

to me the actual decision on 25 vs 50 is much less interesting (although it will for sure tell you the level of concern the Fed has on the economy and whether they’re at all concerned of being “behind the curve” as they were before they started the rate hiking cycle (which to remind you they started with a modest 25bps cut before being forced to abandon incremental measures) than “all the other stuff” by which I mean the “dot plot” in particular. Whether we get 75 vs 100 bps of cuts (or heaven forbid 50) as well as how many cuts are priced through the end of next year (i.e., where does the Fed see this cycle terminating) to me are the most important things we’ll get out of this meeting. Of course we’ll also get updates on where the Fed sees the unemployment rate, GDP, etc., which are really only relevant in terms of telling you what their dot was based on (so, for example, we’re already above the unemployment rate that the previous SEP saw it, so that would (you would think) argue for more rate cuts than the two ‘24 which the last SEP provided for). As HR notes:

The worst outcome is a scenario where the Fed cuts 25bps next week, the September jobs report is unfavorable, risk assets sell off in October, the US rates complex fully prices 50bps for November 7 and Powell finds himself compelled to deliver a super-sized rate cut just hours after a narrow Harris election win. The Fed should avoid that at virtually any cost.

To me, the case for 50bps is strong. We know that rates are at least 50bps above neutral, they Fed has said that they don’t want labor markets to deteriorate further (which would argue for rates being neutral now), unemployment is already over their projections for YE in the July SEP (and inflation is running below), the market is half tilted to 50bps so a smaller cut would retighten financial conditions (we could easily see 2 & 10yr yields push back up towards 4%), a 50bps cut allows for them to not cut in November when it’s possible (likely?) the election won’t have been decided given the meeting is two days thereafter (and still be consistent with 100bps of easing if that’s what the dot plot shows as they could just do another 50bps in December (quarterly cuts)). And don’t forget, as I’ve said all year, this is a Fed that wants to cut rates, they just have needed the data to cooperate, and now it has.

And, consistent with my thinking above, Powell was able to corral (most of) the FOMC into going with a 50bps cut (which, as noted, was what I thought was the “right” decision). Where we go from here is murkier. But if the idea is that risks are truly “balanced” between inflation and labor markets, why you would leave rates in restrictive territory is beyond me. Where the edge of that territory is (the “neutral rate) will be discussed at length (and I get into a bit below), but even the most aggressive forecasters see it below current levels. That argues to me for more rate cuts from here. Whether they’re 25 or 50 is less important to fact that they’re happening on a regular basis. The markets have high expectations, so the Fed not following through with further cuts would tighten financial conditions. In fact, even with the larger than expected (by most) Sept cut and a median dot showing another 50bps of cuts, rates rose this week as noted in the Friday update.

So it seems the FOMC cutting cycle has been (more than) “priced in” by markets. In that regard, I think a more aggressive cutting cycle than we’re likely to see absent a severe worsening in labor markets is now priced in, meaning we’re not likely to see much more relief in financial conditions on the rates side (and we might actually get some tightening as the Fed likely “disappoints” the lofty expectations for cuts (which have a full 1% of additional cuts priced in this year (and 2.16% through next September))).

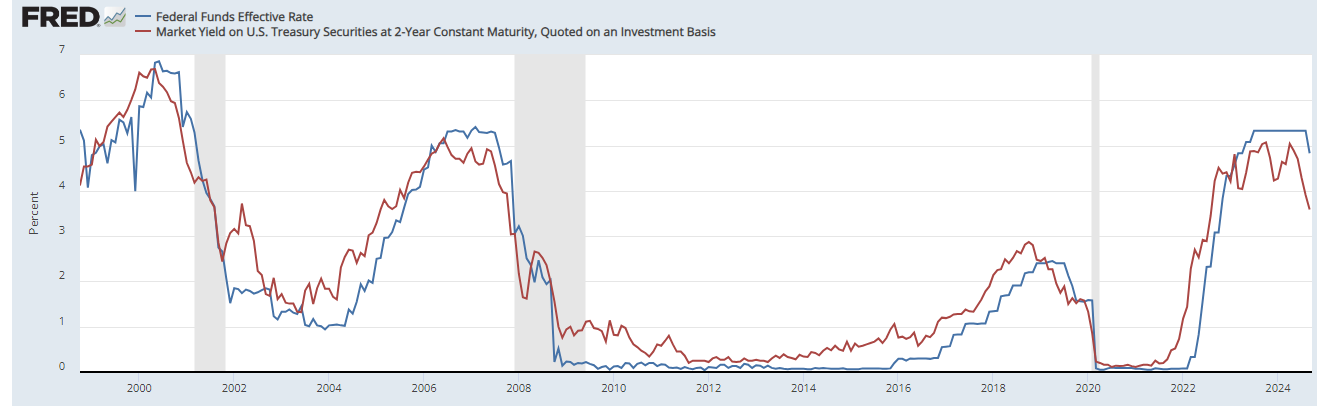

Turning back to where we are now, with yields rising more on the long end this week (as noted in the Friday report both 2 & 10yr yields rose this week despite the dovish Fed cut) the 2/10 curve is now the steepest since June ‘22 at +0.18% according to the St. Louis Fed.

As a reminder, historically when the 2/10 curve uninverts following a long period of inversion the economy is either in a recession or within a few months of one.

The 3mos/10yr yield curve (considered a better recession signal than 2/10’s) remains a lot farther from uninverting but made a big move in that direction +29bps w/w to -1.02%, the least inverted since July. It is still screaming that policy is too restrictive.

I noted the move higher in 10yr yields this week (+8bps), (more than) all of which is explained by increased inflation expectations with the 5-yr, 5-yr forward rate (exp'd inflation starting in 5 yrs over the following 5 yrs) on Thurs hitting a 3wk high of 2.30% up +13 bps from the previous Thursday (which was the least since April ‘23)..

With inflation expectations moving more than nominal yields, real rates fell this week pushing 10yr real rates (based on 10yr inflation-indexed bonds) -7bps w/w to +1.56% the least since July ‘23. Still though well above the 2013-2020 average of around 0.5%.

A similar story if you calculate 10yr real rates using 5-yr, 5-yr inflation expectations (subtracted from the 10yr nominal yield) which came in at 1.43% is the least since July ‘23 (but still above the 2010-2020 peak of 1%).

Shorter-term real yields though (Fed Funds - core PCE from GDP (3mth annualized as of Q2)) remain over 2% at 2.53% (up a tenth with the revision to core PCE) up from 1.63% in Q1, but down from 3.3% in Q4 which had been the highest since 2007).

And using CPI it’s now the highest since Aug ‘07 at 2.97%.

And the gap between 2yr Treasury yields and the Fed Funds rate suggests an aggressive cutting cycle.

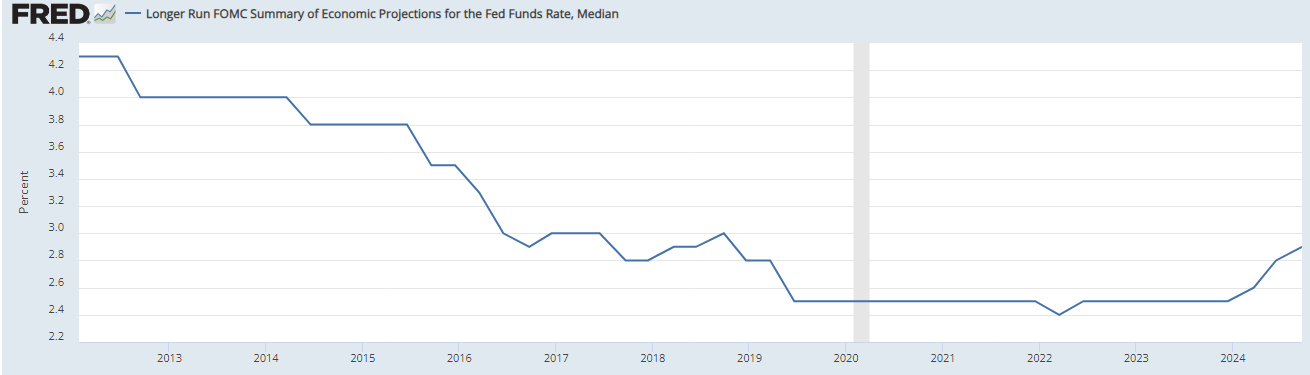

And looking out longer term, one thing to note is the FOMC’s long run projection for the endpoint of the Fed Funds rate (the “neutral rate”) has steadily increased this year, now the highest since Sep 2018 at 2.9% (and not unlikely to go higher).

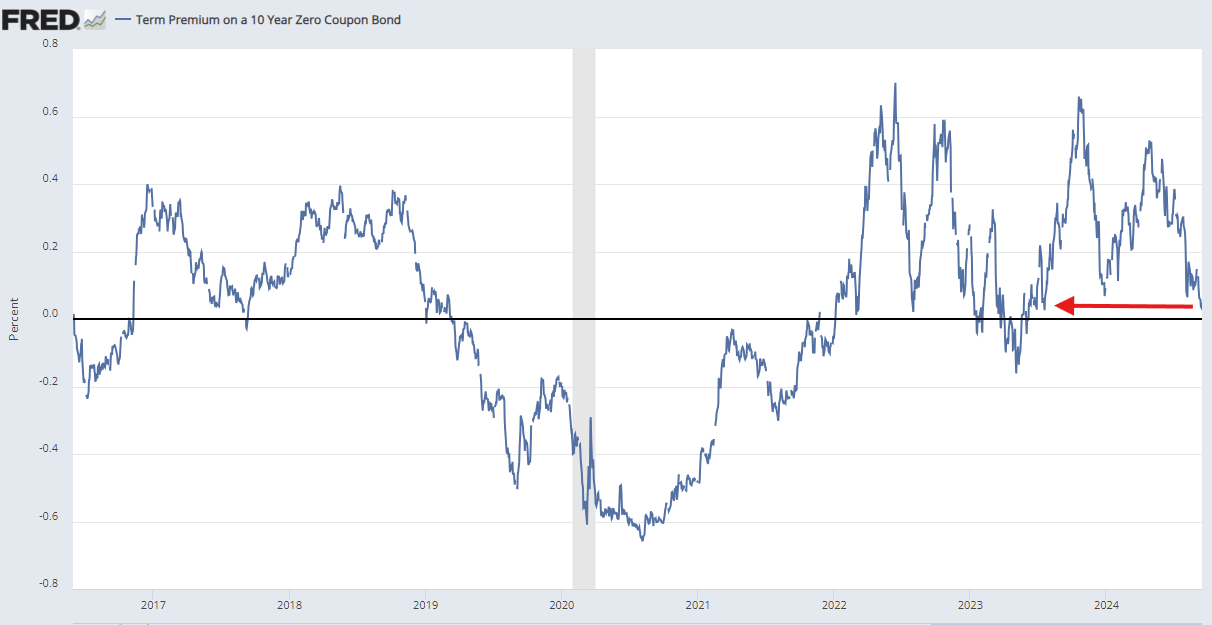

And despite 10yr yields rising last week the 10yr term premium fell to the least since July ‘23 -2bps w/w to +0.043%.

This is something markets were laser focused on when it hit +0.62% last October, but then lost interest in. I had thought that as you get into 2H of this yr, with a lot of talk about deficits and interest costs (i.e., more supply needed), etc., this could resurface as an issue that will push yields higher and cause some equity indigestion as it did then, but so far not much evidence of that.

The extended discussion on term premium (what it is, why it’s important, etc.), can be found in this section in the Feb 4th Week Ahead.

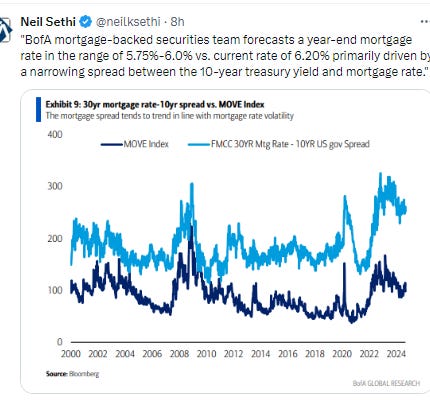

As the MOVE index of bond volatility fell to the least since mid-July now down into the lower part of its range this year. Still well above pre-2022 levels.

And with the drop in bond volatility mortgage spreads fell to the least since Aug ‘22 at 2.42% -111bps w/w, still like bond volatility remaining well above prepandemic levels but also well below the highs from last year.

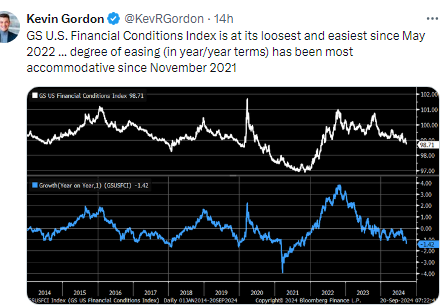

And the Chicago Fed National Financial Conditions Index and its adjusted counterpart (which are very comprehensive each w/105 indicators) in week through Sep 13th saw the former fall to the loosest since Nov ‘21 and the latter fell to the least since Feb ‘22.

And Goldman’s financial conditions index is the loosest since May ‘22.

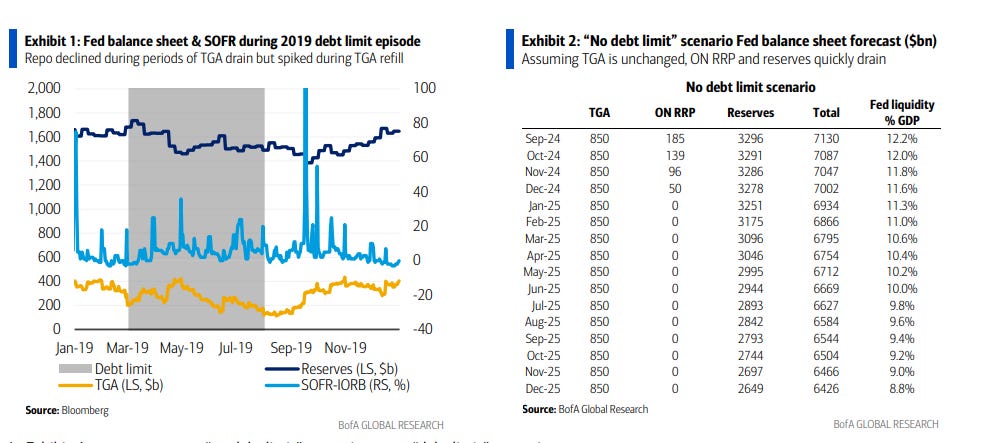

Turning to the discussion of the Fed’s balance sheet/QT and its impact on RRP, we continue to get steady, sizeable auctions of T-bills (<1 yr) of around $800bn/month as well as the $60bn in balance sheet runoff which combined steadily drained ~$1.75 trillion from RRP in the year through March 1st. But as noted in previous weeks, RRP levels had remained stable in the $375-$500bn range until 7 weeks ago when they dropped to a new range of $285-$350bn.

Not sure the reason, but on Monday they fell to $239bn, the least since May 2021. They rebuilt the rest of the week though to end at $339bn, up +$55bn from the prior Friday back to the top end of that “new” range. At these levels they don't seem to be a concern to the #FOMC (QT got a passing nod Wed w/the statement saying QT would continue and Powell describing bank reserves as "abundant").

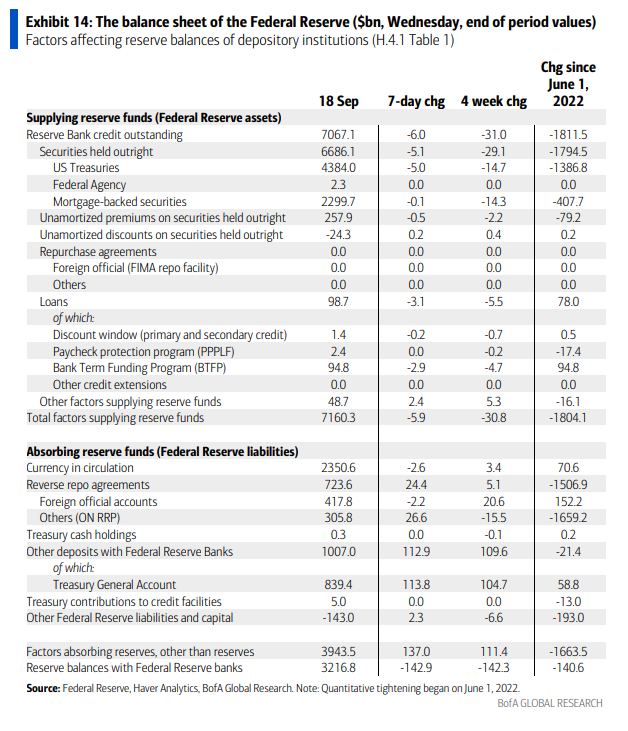

And BoA, who had previously estimated that RRP would fall to zero in Oct has pushed that out now to Jan ‘25 (which may be pushed out further in the event the debt limit is not raised, and the Treasury is not able to continue auctions until it is reinstated (more on this later)). Citi in contrast has thought it will remain around the $300bn level until RRP rates fall.

If RRP levels do fall much below the $200bn market it will be time for the FOMC to start to look to further slow QT (although as also noted below the Fed seems unconcerned at this point). At zero the Fed will need to stop QT.

For more on BoA’s forecasts for RRP to drop to near zero ($60bn) by Oct you can follow the link and look in this section (but it’s mostly due to RRP yields falling below those of money markets and will be soaked up by bonds (from Fed QT), the Treasury (with a higher TGA), and currency growth (in dollars). If bank reserves increase that would also pull from RRP. They see it building again into early 2025 before declining again towards zero.

For more on Citi’s thinking that $300bn is a “constraint level” you can follow the link and look in this section but it’s mostly due to the increased Treasury supply which had absorbed RRP up until March as noted being absorbed by dealers due to just constraints in their ability to intermediate Treasury purchases as well as increased holdings due to “sponsored repo activity”. Still they see it eventually falling lower if/when RRP rates fall.

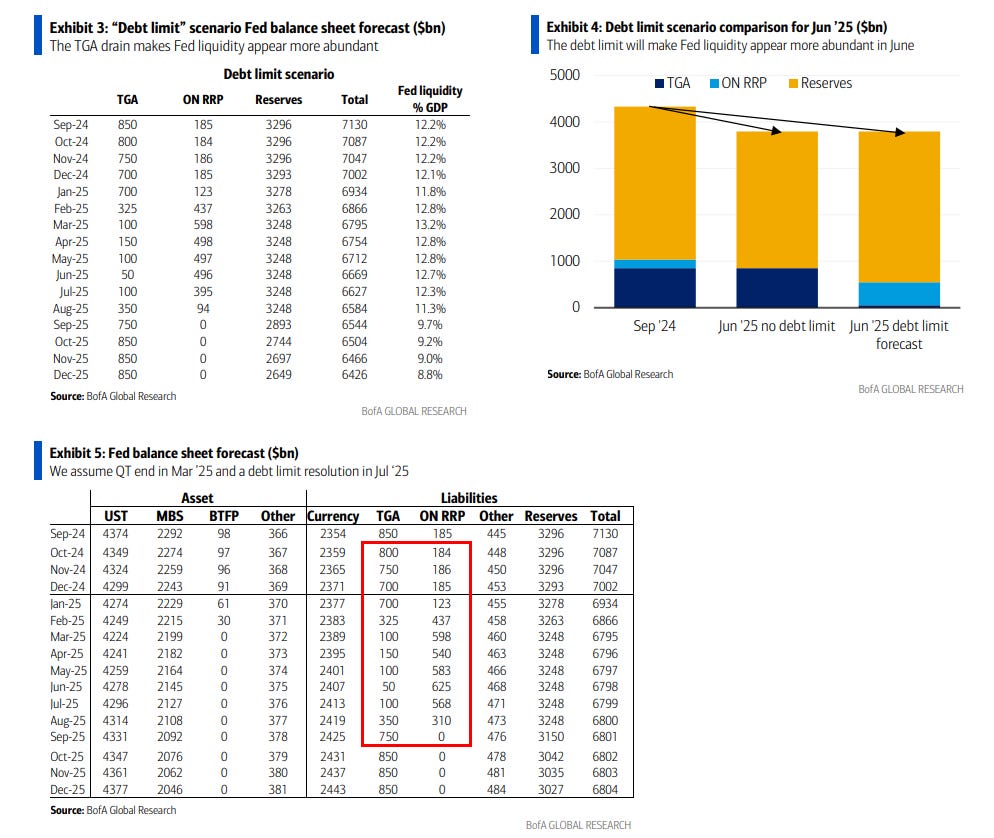

And following “the minimal focus on QT end” in the FOMC statement & Powell press conference Wed, BoA pushes back their est for the end of QT to Mar ‘25 from YE ‘24 “which could create a funding blind spot for the Fed” in the event the debt limit (which expires at YE) is not resolved.

Their thinking is that, similar to earlier this year, the Treasury’s depletion of its General Account (TGA) will offset what would otherwise be a continued drawdown of liquidity. That will keep liquidity stable but will rapidly reverse once the debt limit is ultimately raised (which BoA est’s will again be in July as they assume Congress will take it to the very last second as is their habit), which could lead to a funding squeeze.

However if the debt limit is miraculously raised in advance, the liquidity issue will come quickly as noted above, and we could very easily find ourselves in another 2018 scenario (which resulted in a near bear market).

Bank reserves fell slightly week through Thurs to $3.22tn, -$14bn w/w still leaving breathing room between the "scarcity" level which appears to be at $3tn.

They are -$141bn since June 1, 2022, when the Fed started QT, a much better result than even the most optimistic estimates at the time.

For background on various estimates of when reserves will be “too low” see the Feb 4th Week Ahead.

Getting back to rates, I said 20 weeks ago 2-year Treasuries were a good buy at 5%, and at this point the ship has sailed on seeing those yields anytime soon (meaning years). In terms of 10’s I had advised grabbing some at 4.7% which also seems like something we won’t see anytime soon. I noted four weeks ago

While 10 yrs are a little rich we could see 3.5% before we see 4.25% absent a very hot Aug CPI print. I am inclined though to fade a 2yr under 4% unless we see the labor market crack (but I won’t be shorting due to the carry, just not buying).

And while we didn’t quite see 3.5%, I think 3.6% is close enough. I think we might have seen the lows at this point, particularly as the Fed has been raising their neutral rate estimate as noted earlier. If the endpoint for Fed Funds is around 3% then it’s hard to see the 10yr trading much lower absent a recession. Similarly 2yrs at 3.6% seem to be very rich and almost certainly too low absent a recession consistent with my statement last week:

At around 3.6% on both the 2 & 10yrs absent a recession I think there’s not much value in either (I’d rather park my cash in safe dividend paying stocks at these levels.

For all the old “final hike” and “first cut” materials, you can reference the Feb 4th blog post.

And success! After much prodding BoA updated their FOMC Dove-Hawk Chart. Note it’s missing Hammack in ‘26 (Cleveland and Chicago vote every 2 yrs), but otherwise looks right. Also note that Philadelphia Fed Pres' Harker’s term is up next year (which is why they don’t have a name for Philadelphia), something I didn't realize.

Also, I had a little back & forth with them arguing that Schmid should be "Hawkish" considering that he didn't dissent (versus Bowman) and that Goolsbee seemed more dovish than Harker. Here was their response (which makes some sense):

In a recent dot plot (I think June), Goolsbee identified himself as not the outlier, which led us to conclude Harker is the outlier. On the other end of the spectrum, there were two people forecasting 50bp of total cuts this year. We think they’re probably Bowman and Schmid. If we had more granularity, we’d rate Bowman as more hawkish, but with only five categories, I’m comfortable with putting them in the same bucket.

Earnings

As a reminder, I have removed most of the background material, which you can get in the Feb 4th blog post. As you know I’ve moved on to 2Q and beyond. You can reference this post from 5/12/24 for stats on 1Q.

As we move closer to Q3 earnings, Factset reports those have fallen now more in line with avg levels, down -3.2% since the start of the quarter (from -3.0% last wk & vs 5yr & 10yr avgs of -3.3%)) to +4.6% y/y growth (-0.3% from last wk). As with Q3, future quarters were also marked lower in each case by -0.4%: Q4 +15.0% (from +15.4%), Q1 2025 +14.6% (from 15.0%) & Q2 ‘25 +13.7% (from +14.1%).

Putting it together FY ‘24 earnings expectations are now at $242.21 (the least since the start of the quarter but as noted in line with historic avgs). Looking longer term, this continues to be much less than the typical -6% or so drop we historically see from July of the prior year (July '23).

2025 earnings expectations fell more down to $278.41 from $279.26 last week, the least since May, but still up around $4 from the start of the year, but now starting to see some softening from July ‘24 levels as is typical.

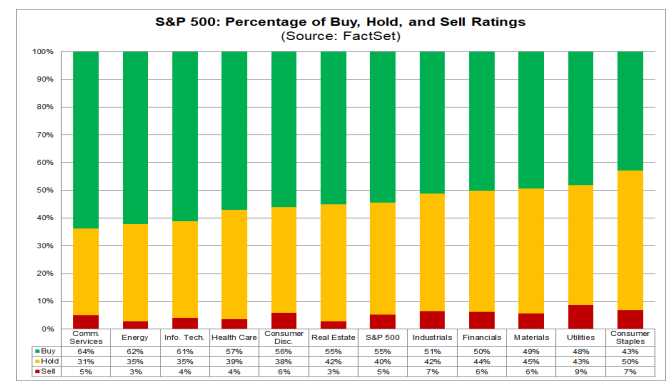

Factset’s analysis of analyst bottom-up SPX price targets for next 12 months as of Thursday was little changed at 6280, still up ~1,242 points over the past 29 weeks. Energy (+16.9%, but down from +23.7% last week) is expected to see the largest price increases, RE (+3.2% up from +2.2%) the smallest.

As a reminder the last 10 yrs they have been on avg +2.9% too high (+3.4% last 5 yrs). Of course, that avg range masks a wide discrepancy between big up and down years.

In terms of analyst ratings, no change this week w/buy and hold ratings continuing to dominate at 55 & 40% respectively (as has been the case all year). Communication Services (64%), Energy (62%), and Information Technology (61%) sectors have the highest percentages of Buy ratings, while the Consumer Staples (43%), Utilities (48%), and Materials (49%) sectors have the lowest percentages of Buy ratings.

And some other earnings stuff:

Economy

As I’ve written over the past 18 months, part of my earnings optimism has been due to the economy holding up better than expected. While earnings only track the economy loosely (and markets look forward 6-12 months), there is a clear correlation between recessions, lower earnings, and lower stock prices (although stock prices (being as noted forward looking) generally fall in advance of the recession and bottom 6-9 months before the end of the recession). So if you can see a recession coming it is helpful, although very difficult (especially ahead of the market). You can reference this Week Ahead (see the Economy section) for a lot of material on how every recession is preceded by talk of a “soft landing” as close as a month before the start. On the IRA infrastructure act, the November 26 report has good info on how that should be supportive at least through the end of this year. That report also has the notes about how small caps have shorter debt maturity profiles and more of it.

As I’ve been stating since I switched to the Week Ahead posts in mid-2022, the indicators to me are consistent with solid (which at times has been robust) economic growth, and I have been a broken record that I “certainly [did] not think we’re on the verge of a recession (although as noted above every recession starts out looking like just some economic softening).” But a few months ago I added: “That said, I’ve also noted over the past __ weeks or so [now 21], we have clearly started to see some moderation in key areas like consumption, manufacturing, construction, exports and housing.” Last week though the data was fairly strong more consistent with what we’d been seeing at the start of the year. Retail sales were solid, housing starts and permits were better than expected, jobless claims fell to a 2mth low, and industrial production was very strong. Overall, the situation seems to remain subdued manufacturing and housing environments environment (but perhaps inflecting higher although 1mth is not enough data to make that call), solid (if slowing) labor markets and construction spending, strong income and services sector growth with good productivity, and increasing imports and exports. Overall I continue to feel that the softening does not appear to be morphing into a recession (especially this week).

Overall, as I said seven weeks ago:

without question, the evidence is building that the days of >3% real GDP growth are behind us, and we should be happy to settle into something more around trend (1-3% real (infl adjusted) growth). That though is far from a disaster. The important thing will be to see the softening level out (L-shape) rather than continue to fall turning the “soft landing” into a recession.

Citi Economic Surprise Index remained negative as of Friday, but a big improvement to -8.5 from -26.8 the prior week (and -47.5 ten weeks ago (but still further from the highs of the yr around 50 in Jan).

And GDP estimates are for now consistent with a no recession call (again though remembering GDP going into recessions generally doesn’t look like one is coming (it was up around 2% in Q2 & Q3 2008 well after the recession had started)). With the solid data most moved up to the 2.5-3% level.

Goldman (who was at 2.3% for 2Q vs 2.8% actual) raised their 3Q GDP estimate to +2.8% (not sure where they get "consensus" from, but I haven't seen many sub-2%).

In that regard, BBG’s consensus estimate is 2.5%.

Atlanta Fed improved to 2.9% from 2.5% the previous week FYI I haven’t heard back on my question below).

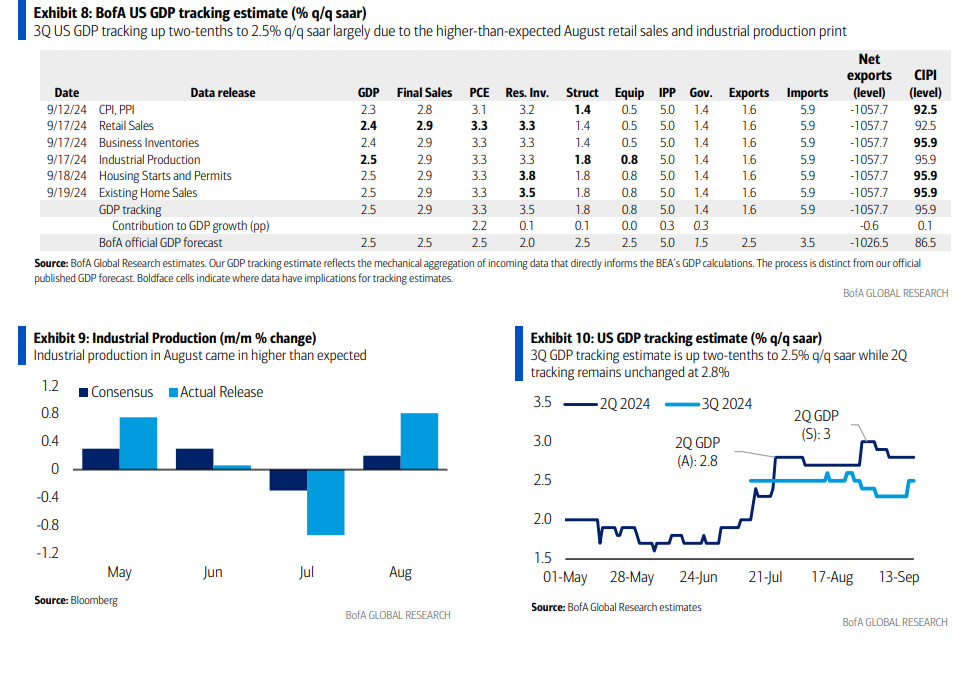

While BoA’s 3Q GDP tracker as of Thursday night up two tenths w/w to 2.5% (as a reminder it had 2.4% ahead of 2Q vs the 2.8% actual 1st est) driven by the retail sales & industrial production reports. Their “official” house est is also at 2.5%.

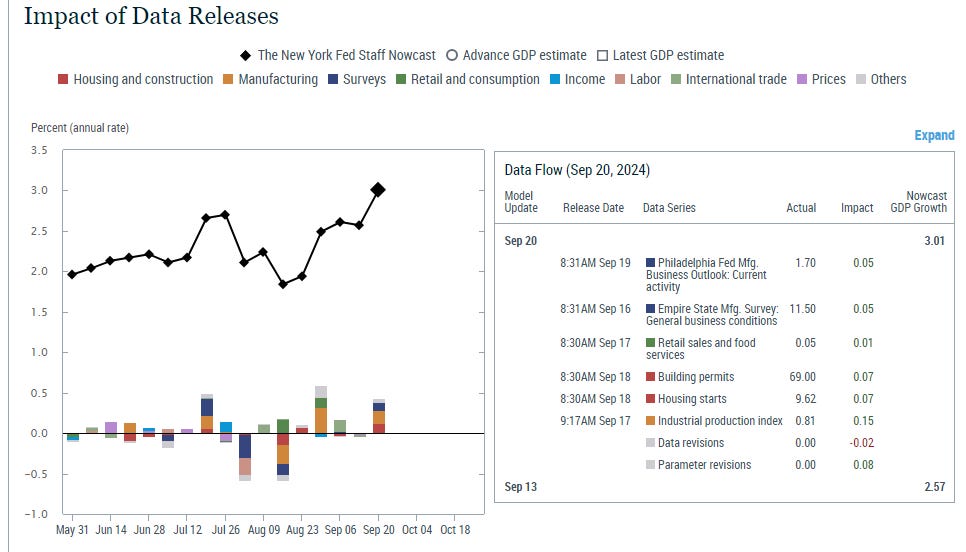

While the NY Fed’s 3Q GDP Nowcast (as a reminder, they had 2.01% for 2Q vs 2.8% 1st est) remained one of the higher ones jumping almost a half percent to 3.01% from 2.57% mostly on the industrial production report (+0.15%) and housing starts & permits (each +0.07%). Also note the NY Fed’s model is dynamic and so adjusts in real time as data evolves, the “parameter changes” this week added +0.08%.

The 4Q est jumped even more to 2.74% from 2.17% as the positive outlooks from the NY & Philly Fed regional PMI’s added +0.26%.

And the St. Louis Fed GDP tracker, which outside of Q1 (where it was the closest) has significantly undershot actual real GDP since Q3 ‘22, saw its Q3 ‘24 est little changed at 1.55% from 1.57%. Unfortunately they don’t give a breakdown of the inputs like the others.

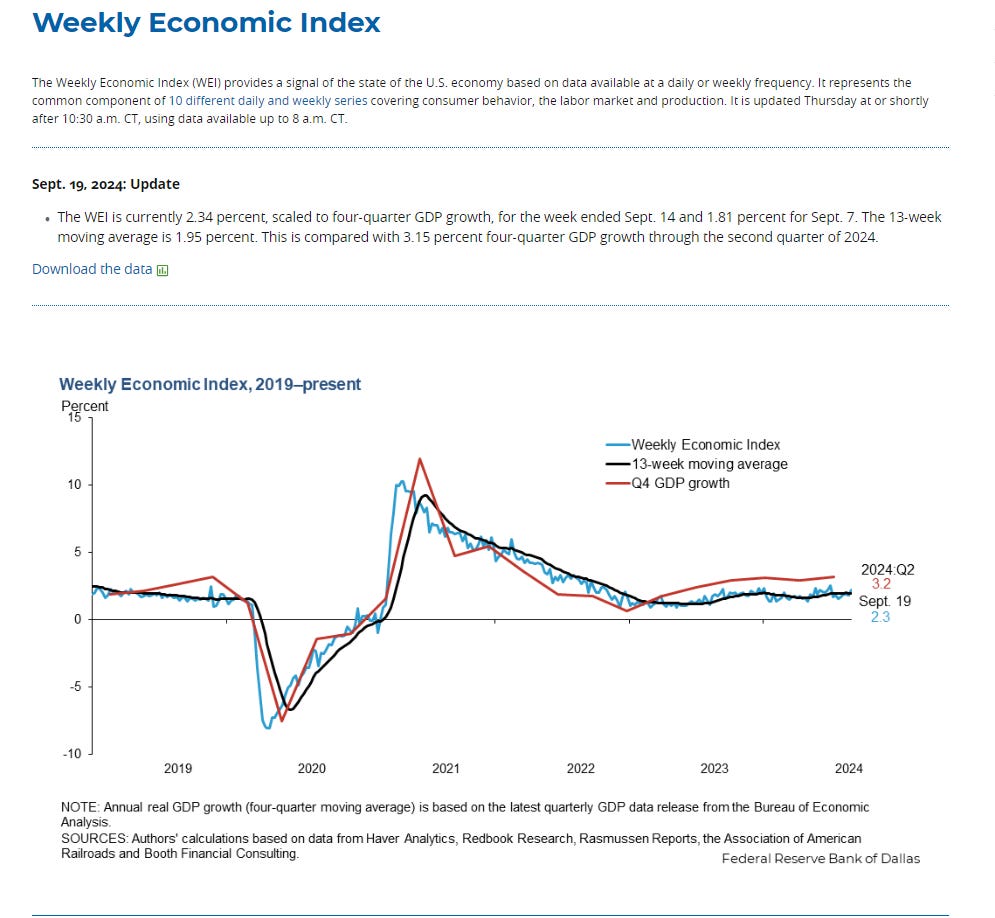

And the Weekly Econ Index from the DallasFed (scaled as y/y rise for GDP), which runs a week behind other GDP trackers, remained the highest this year in the wk through Sep 14th at 2.34% from 1.81% the prior wk (rev’d down from 2.27% (this series is consistently revised lower in the following week)). The 13-wk avg though edged down a tenth for a 2nd wk to +1.95%, evidencing that overall economic momentum remains stable at just under 2% growth.

Here’s the components.

Other economy stuff:

Multiple

Like the other sections, I’ll just post current week items regarding the multiple. For the historical stuff, see the Feb 4th blog post.

With little change in earnings expectations, the stock rally this week pushed forward P/E’s outside of the very largest stocks back near the highs of the year.

The SPX up to 21.2 from 20.9 last wk (& 20.2 the prev Fri), now just below the 21.4 it hit 10 wks ago (which was the highest since Jan '22)).

Mid-caps moved to 15.8, now the highest since the 16.0 it hit early in the year.

Small caps to 15.3 (from 14.5 two weeks ago) just below the highs of the year (15.4 three wks ago).

The “Megacap-8” P/E did jump to 28.3 from 26.4 last wk (which was the least of the yr), still though well below the 31.5 ten wks ago (which was also the highest since Jan ‘22)).

Breadth

Breadth was a little weaker this week but overall was solid for a second week.

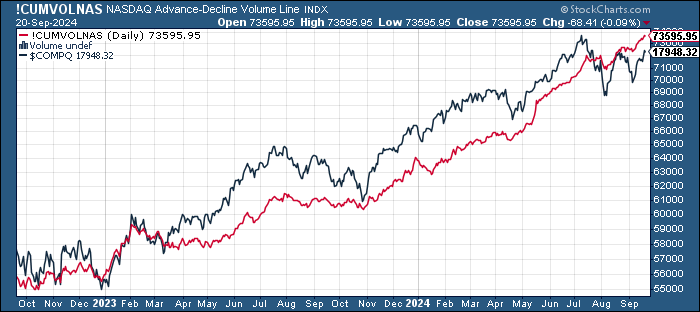

Advance/decline volume lines remain supportive of the rally although the NYSE fell off a bit EOW.

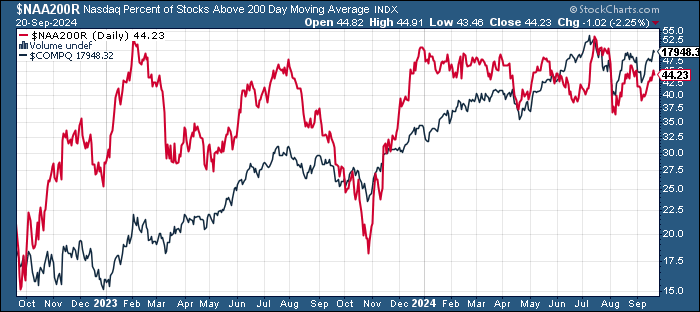

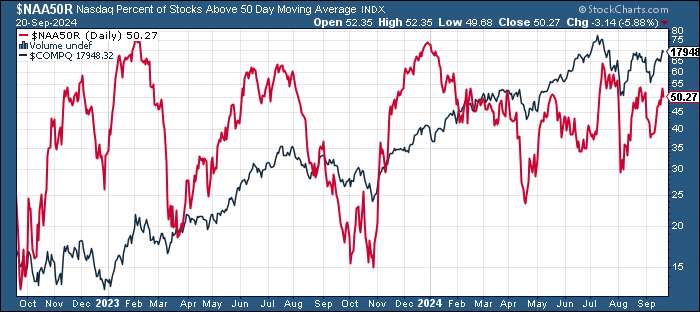

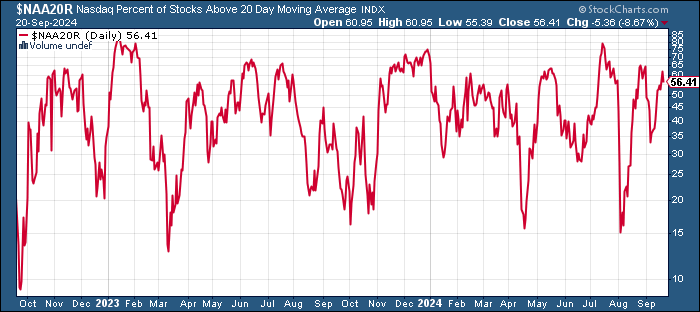

% of stocks over 200-DMAs near the highs for NYSE but lagging for Nasdaq despite the A/D volume line at an ATH.

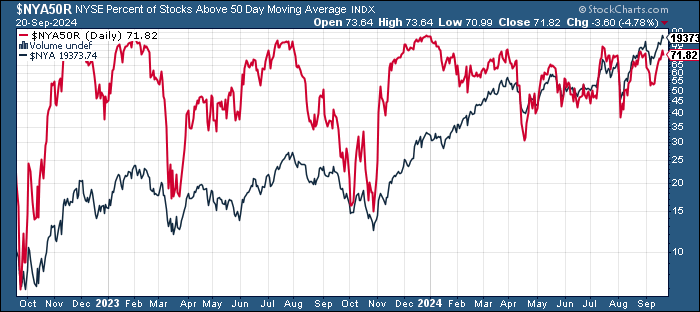

And % of stocks above 50-DMAs a similar story, near the highs for NYSE but lagging somewhat for Nasdaq.

And same for % of stocks above 20-DMAs.

The equal-weighted SPX vs cap weighted ratio remained in the middle of its range since late July.

It continues to me to bear some resemblance to the 2009 pattern where we saw an initial bounce from historic lows, then a big retracement before it embarked on a swift multi-year recovery.

IWM:SPY (small caps to large caps) similarly remains in the middle of its range since mid-July remaining overall not far from the least since 2000.

Equity sector breadth based on CME futures a little weaker than the prior week when every sector ex-energy was up, but still 8 of 11 were in the green, and all of those up at least 1% (down from 9 the prev week) but still very strong w/ no sector down -1%.

Last week's SPX stock-by-stock chart map from Finviz showed the more even gains this week. Every energy SPX component was green this week. Didn’t realize META was up 7% pushing comm services to a nearly +5% week.

Other breadth stuff:

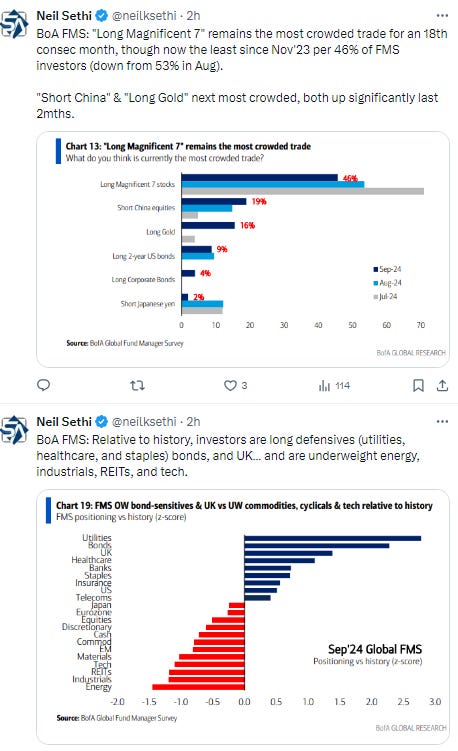

Flows/Positioning

BofA using EPFR data in the week through Sep 18th saw equity flows rebound strongly after falling for the 1st wk in 20 the prev week, +$38.6bn, the 39th inflow in the last 47 weeks, now +$426bn YTD:

US also returned to inflows in a big way after just the 2nd outflow in 11 wks last week (& largest since Apr), +$33.8bn, the 3rd largest this yr, now +$261bn YTD.

EM 16th wk of inflows, longest stretch since at least ‘21, +$1.3bn, now +$110bn YTD, as China saw 17th week of inflows (why is the market down?) (+$0.5bn, +$55bn last 15wks, now +$92.1bn YTD, while India +$0.5bn, now +$20.7bn YTD and easily on pace for record yr. EM took in +$91bn in all of 2023.

Europe continues w/outflows, 4th straight & 75th in 80 wks, -$0.8bn, now -$34.8bn YTD after -$66.9bn in 2023.

Japan returns to inflows, +$1.4bn, now +$15.5bn YTD after +$7.3bn in all of 2023).

US large caps also return to inflows after first outflow in 6 wks the prev week (and just 9th in prev 48 wks) +$26.2bn, now ~+$298bn last 44 wks after +$125bn in all of 2023.

Small caps also see +$3.9bn inflow, one of the largest of the yr (2nd straight), now +$15.9bn last 10 weeks and +$15.6bn YTD.

US value also a big inflow, largest since Dec ‘23, +$4.2bn (still ~-$31.4bn in 2024 after a record -$73bn in 2023).

US growth saw only 2nd inflow 12wks +$1.9bn, still -$30.3bn last 12wks but still ~+$120bn YTD.

Sector specific equity flows were mixed in EPFR data in the week through Sep 18th:

Inflows:

Consumer led inflows for a 2nd week for the first time this year +$0.9bn, largest in 8 mths (+$1.6bn last 2 wks, but still -$24.8bn last 48 weeks).

Materials 1st inflow in 8 wks +$0.4bn.

Healthcare rare (this yr) inflow +$0.3bn (still -$17.2bn last 50 weeks).

Tech returns to inflows for 1st week in 3 (but 9th in 11 wks) but remaining modest at +$0.1bn, +$10.9bn last 8 wks & +$45.9bn last 37 weeks.

Outflows:

Utilities 1st outflow in 3 wks -$0.2bn, most since May (still +$2.7bn last 10 wks).

Real estate 2nd outflow in 8 wks -$0.1bn, still +$1.3bn last 9 wks.

Energy 6th wk of outflows -$0.1bn (-$4.7bn last 7 wks).

Financials led outflows for a 2nd week, -$0.6bn (after largest in 10 mths prev wk), cutting last 15wks to +$2.1bn.

Commercial services -$0.1bn.

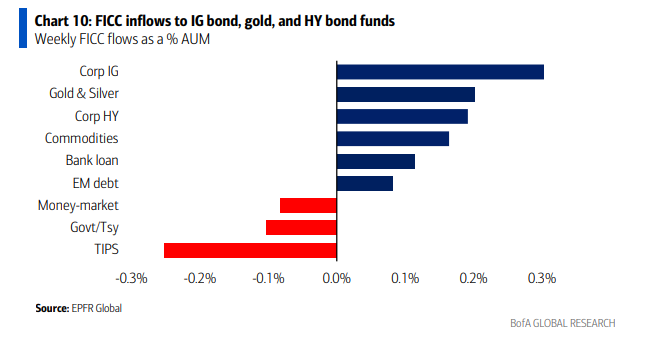

Looking at EPFR data in the week through Sep 18th for fixed income saw a 76th inflow in 77 weeks (and 8th straight) +$15.5bn, now ~+$466bn YTD (annualizing to $652bn):

IG/HG a 47th consec inflow (& 73rd in 75 wks) +$13.9bn, the largest in 4 yrs, now ~+$304bn YTD, on track for a record $425bn in 2024 after +$162bn in 2023.

Munis the 31st inflow in 35 wks (and 11th straight) +$1.8bn.

HY 6th consec inflow, 12th in 13 wks (and 37th in 46) +$1.1bn, now +$47.1bn last 46 wks.

Treasuries back to a rare (this year) outflow, just the 2nd in 21 wks (and 4th in 34 wks) -$1.3bn.

Bank loans back to an inflow, just the 2nd in 9 wks +$0.1bn, still -$3.7bn last 8 wks).

TIPS 6th straight outflow & 10th in 11 wks (& 44th in 55), -$0.4bn. TIPS also saw record outflows of -$33bn in 2023. Doesn’t seem to indicate huge inflation concerns.

EM debt 1st inflow in 8 wks +$0.4bn. EM debt saw -$37.0bn in outflows in 2023.

In week through Sept 18th, EPFR saw cash funds w/the 1st outflow in 7 wks -$7.6bn, still +$592bn YTD (annualizing to more modest but still very healthy +$828bn after a record +$1.3T in 2023 and +$3.3T 2019-2023).

Gold/Silver see 5th consec inflow, the 11th in 13 wks +$0.5bn, now +$9.5bn last 16 wks.

Crypto funds (Bitcoin) return to inflows +$0.5bn, now +$7.2bn last 19 wks.

ICI data on money market flows saw a larger outflow (-$20.0bn) than EPFR’s -$7.6bn in the week through Sep 18th, dropping the YTD flows into money market funds to ~+$408bn and the total MMF assets down to $6.30tn from record highs.

Looking at CTA (trend follower) flows, BoA reminds us that “we noted four weeks ago that differences in long- and short-term trend signals were leading trend followers with varying lookback biases to move in different ways,” with short-term trends negative following the early Aug & then early Sept selloff while longer term trends were more positive not fully incorporating those. That has now reversed with “short term equity trend…significantly improved,” but longer term trends now incorporating those Aug & Sept declines more fully (while the former has exited shorter term lookbacks).

The good news is that leaves CTA positioning “unstretched”. The bad news is that “it could likely take a push to north of 5900 on the S&P 500 to see CTAs continue rebuilding their longs back to levels seen earlier this year.”

Still $SPX (which has by far the strongest trend strength) & $RUT positioning is the longest since July ($NDX is a little off its recent high) but all are very much price dependent (i.e., buying will follow price) BoA est’s. Other markets (Europe/Japan) are more around flat levels.

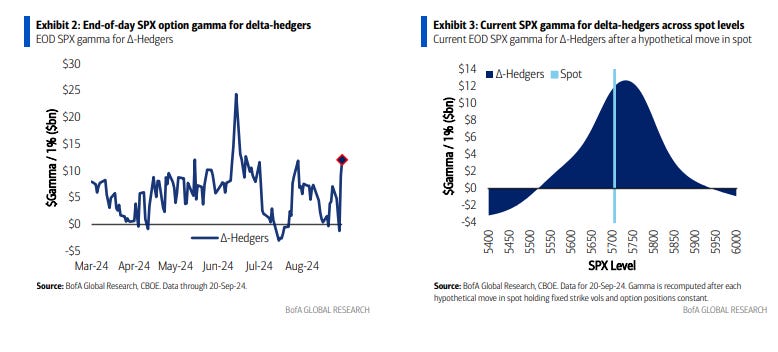

In terms of gamma positioning, BoA notes that a little surprisingly “SPX gamma was short ~$1.2bn” at Wed’s close but “by the end of Thursday gamma had climbed to +$9.1bn for a ~$10bn swing in a single day, among the largest on record. Under the hood, such a rapid rise appears in part due to movement in spot (as the $SPX gained 1.7% on Thurs. to hit new highs) and net new flows supplying dealers with more gamma. Finishing the week, SPX gamma ended Friday long $12.1bn (97th %ile year-to-date).”

The takeaway is that we’re now back to very high levels of gamma which act as a market stabilizer dampening volatility in both directions. As I noted last week, this should reduce some of the normal end of September volatility. It would take a rapid move to sub-5525 (-3%) to see gamma potentially flip negative, a good amount of breathing room.

And Nomura’s Charlie McElligott (described as the “OG” of this sort of analysis on a podcast I listened to this weekend) put Thursday’s action like this (from Heisenberg Report):

“[The FOMC’s] 50bps ‘lift-off cut’ blasted the market-implied probability distribution away from ‘hard landing’ and back into ‘soft landing’ mode [which] in turn [sent] a defensively-positioned, de-risked, netted-down equities set across mutual funds, long/short hedge funds and systematics… into ‘grab and chase’ upside FOMO.”

[With dealers short long upside optionality (from customers who bought calls for “stock replacement” purposes) above SPX 5640, as spot prices moved through that region], dealer hedging “creat[ed] a huge positive delta impact as market makers grabb[ed] S&P futures the higher they [went]” McElligott said.

“As I’ve made a career of discussing, it’s the second-order flow impacts of these macro shifts which then create the market ripples,” noting that Nomura’s pre-market September 19 projections tipped nearly $11 billion of EOD leveraged ETF-buying across the products the bank tracks, alongside $8 billion of projected Nasdaq 100 futures buying from the large, well-known big-tech overwrite ETF, whose short calls were, as Charlie noted, “deep ITM.”

In other words: Thursday’s early gains on Wall Street set the stage for as much as $20 billion of buy flows on the end-of-day rebalance, and that was on top of any simultaneous FOMO-buying from discretionary investors desperate to jump aboard a moving train.

Like CTA’s, volatility targeters (vol control), who were sellers the past 2 wks given the increased volatility (which doesn’t have to be negative), also pushed their positioning to the highest since July with solid buying last week. As I noted last week “if we can get volatility to calm down these will reengage (i.e., daily market moves <1%),” and that seems to be happening.

While buybacks picked up last week.

But now we’re deep into the buyback blackout period with over 80% of companies in the blackout which lasts until Oct 25th.

Sentiment

Sentiment (which I treat separately from positioning) is one of those things that really only matters at the extremes (and even then, like positioning, it really is typically helpful more at extreme lows vs extreme highs (“it takes bulls to have a bull market”, etc.)). With the rally in equities the past two weeks we’ve seen sentiment improve as would be expected in most metrics, many quite sharply, but not yet to what I would consider “extreme”. In fact it might be considered more of a tailwind as it supports further buying at this point.

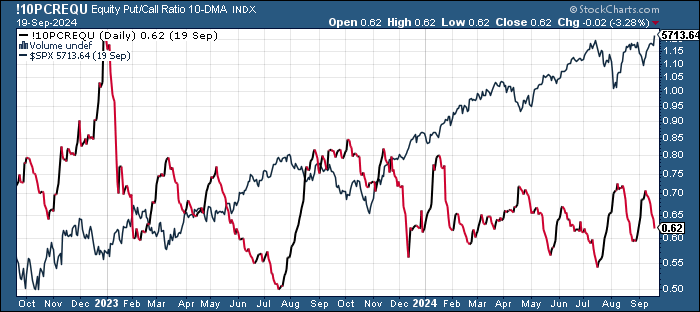

The 10-DMA of the equity put/call ratio (black/red line) has continued to fall but just basically to the middle of the range this year, far from “extreme” levels of bullishness.

On the sentiment front, it will be no surprise that the Investors Intelligence bulls notched up to 49% but what I find very curious is that the bears were up fractionally as well and believe it or not that puts the bears at the highest level (22.9%) since we were at 26% one year ago. In the big picture, bears at 23% is not high—there are still more than two bulls for every bear—but it’s certainly not what I expected with the S&P making new highs.

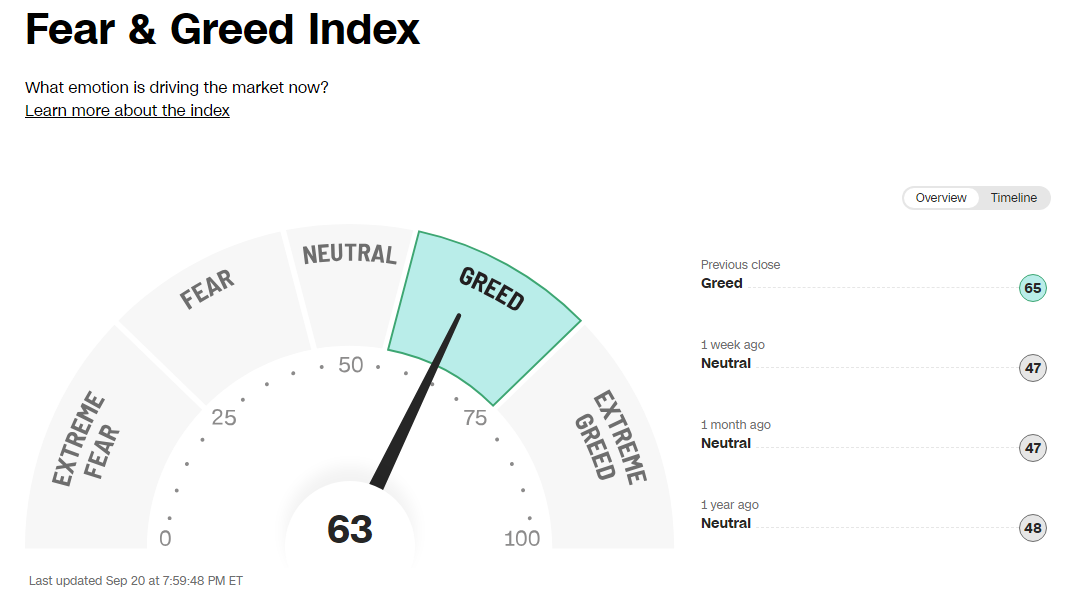

CNN Fear & Greed Index continued its sharp improvement, on Thurs hitting 65, the highest since April, up from 39 two wks ago, firmly into Greed territory, but not yet into Extreme Greed.

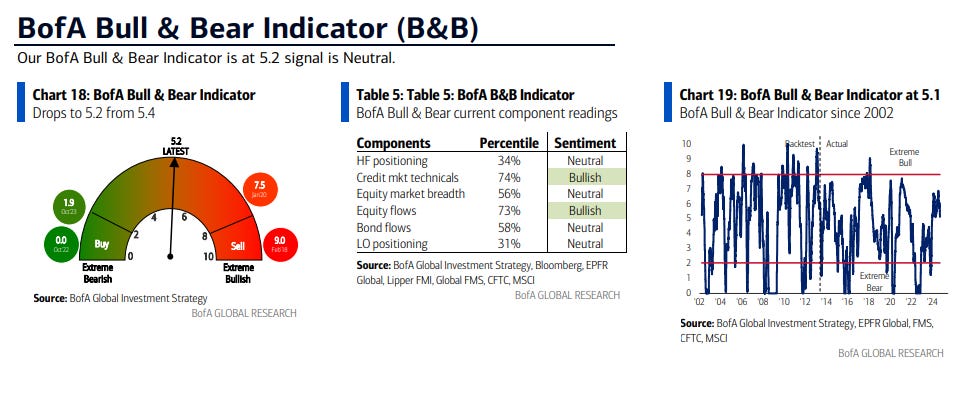

BofA’s Bull & Bear Indicator though falls back for the 7th wk in 8 after hitting the highest since May ‘21 in late Aug (6.9), now at 5.2 from 5.4 last wk, still well above the “Extreme Bear” buy level. The decrease was due to “global equity fund outflows, big hedging activity against lower SPX & oil; positioning neutral…consensus long credit & stocks with big downside hedges; note hedge funds least bullish on 2-year Treasury contracts since May'23, most bullish on Japan yen since Feb'21..”

While Helene's followers remain bullish for the 9th wk in 10 (and 11th in 13), meaning they remained mostly bullish throughout the entire roller coaster since mid-July.

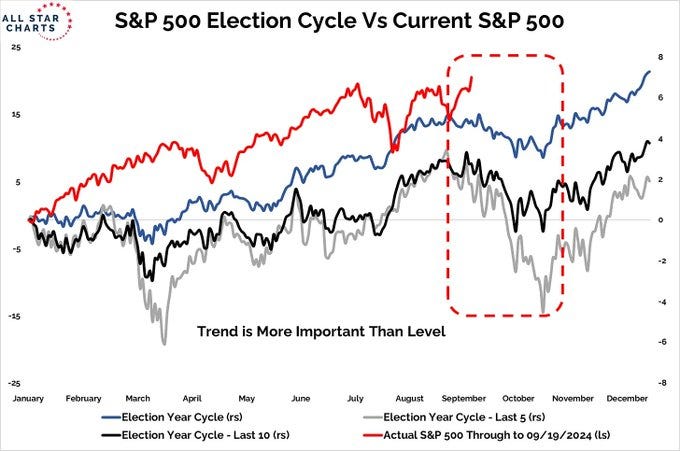

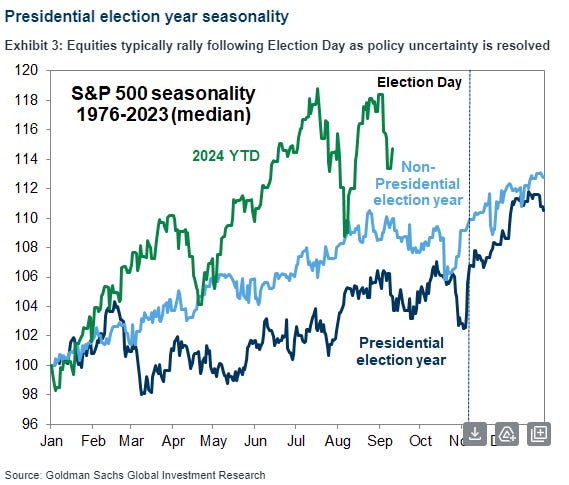

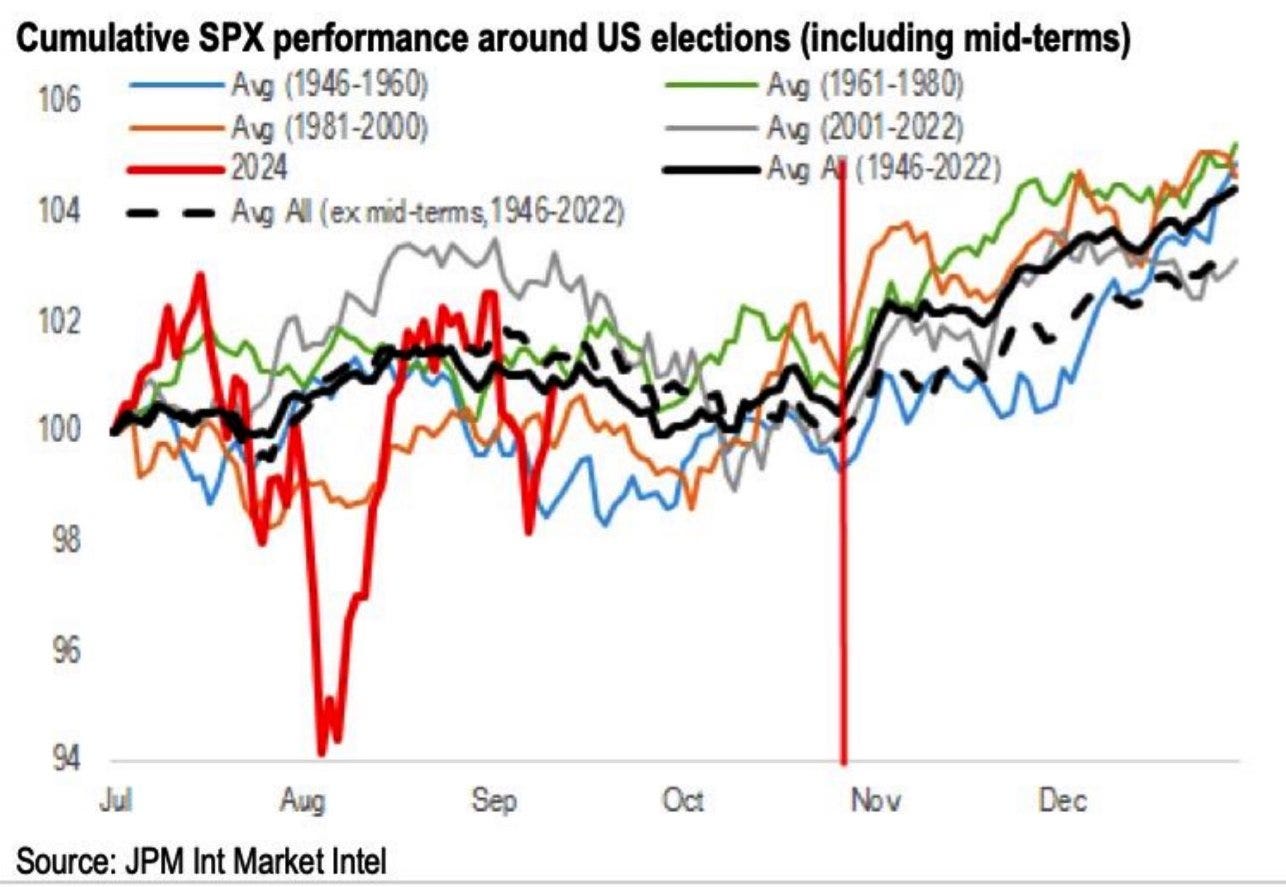

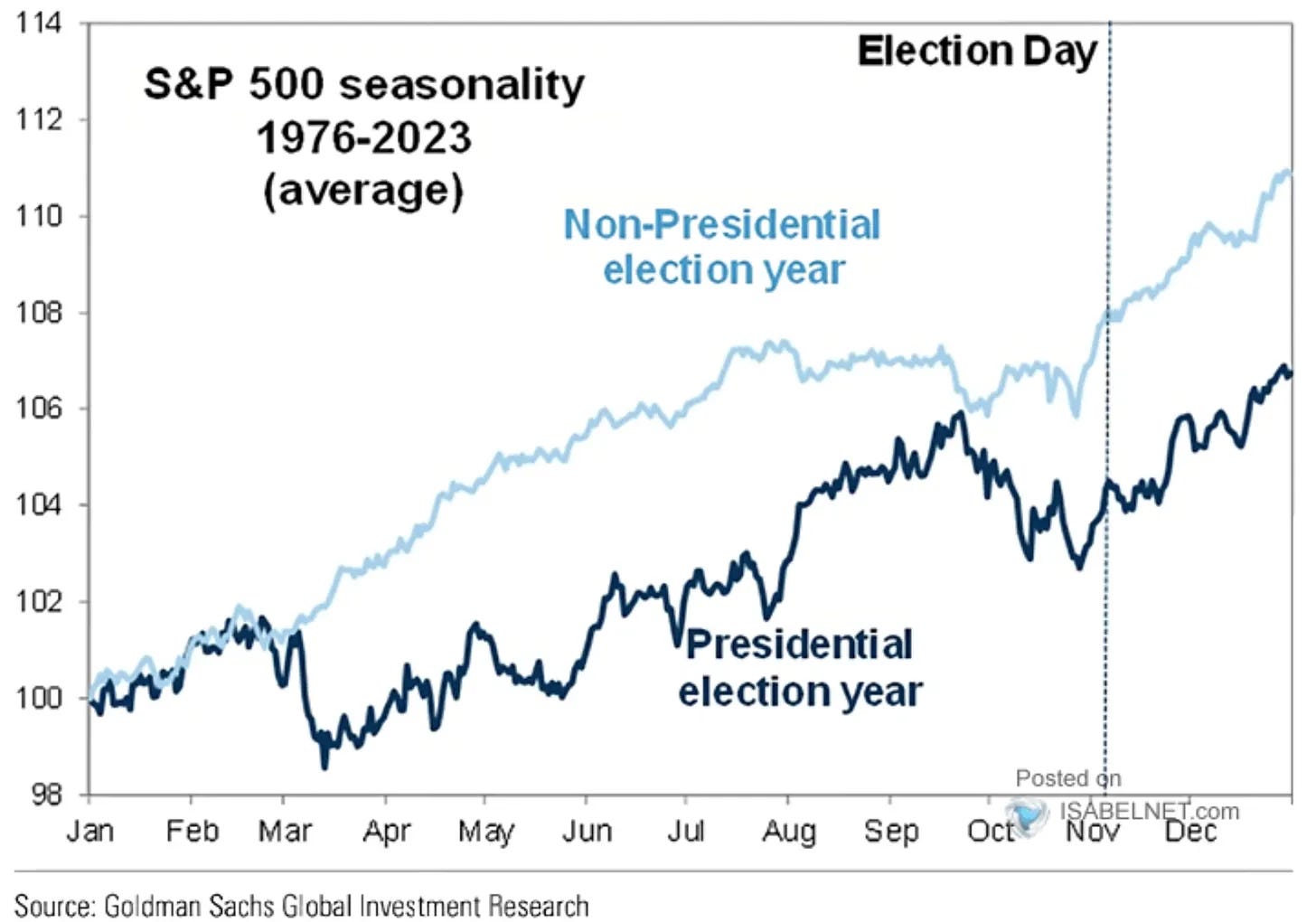

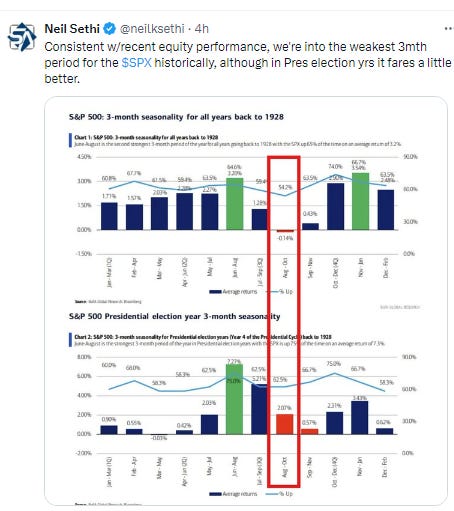

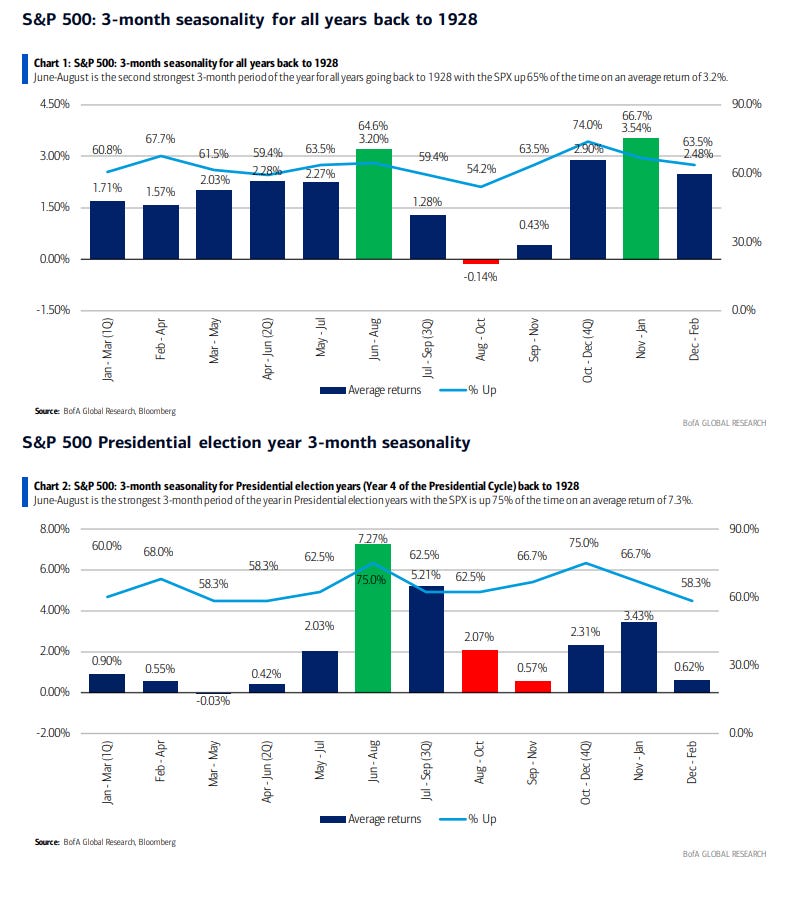

Seasonality

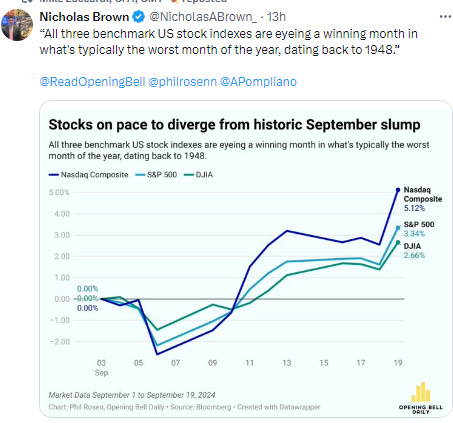

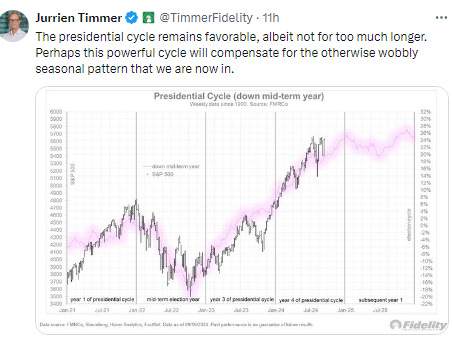

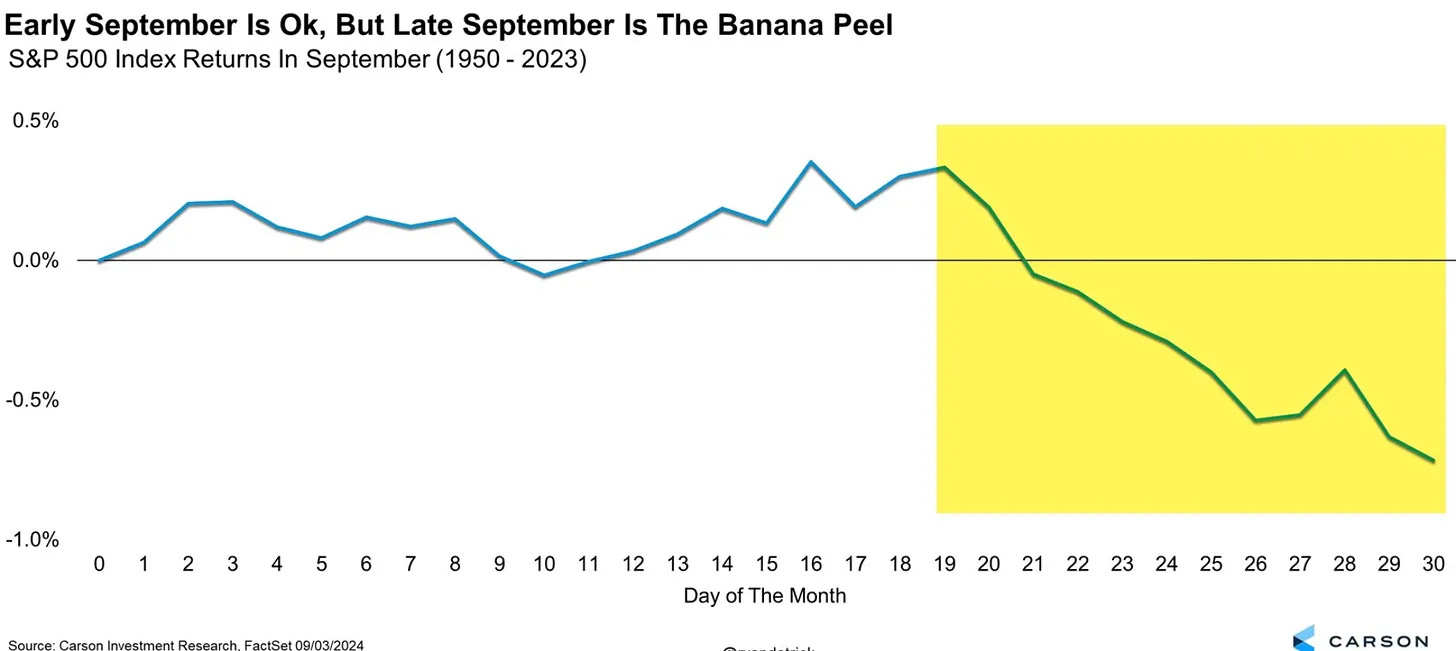

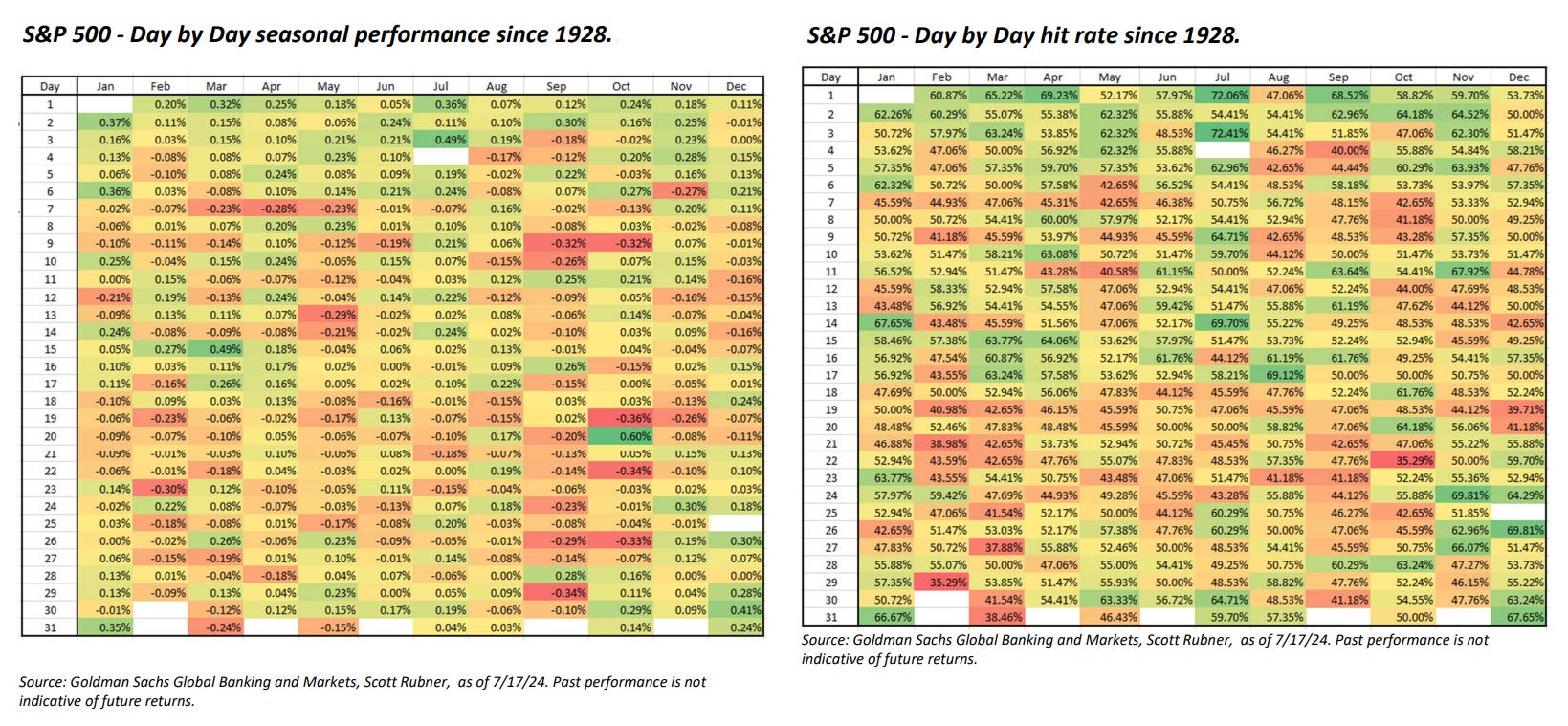

As noted in previous weeks while the May-Nov period is commonly thought of as seasonally weak ("Sell in May” and all that), in reality on average it sees positive returns and also is normally stronger in an election year. However it does have its stronger and weaker periods, and as noted last week, we crossed over into what is historically the weakest 2 weeks seasonally of the year. BUT, Goldman’s Scott Rubner posited that perhaps we might have pulled that forward into the first week of the month on front running. That seems like it might be proving true. That said, as noted below the week after the Sept options expiration is notably week, and we’re moving deeper into the buyback blackout period. Typically things don’t materially improve on the seasonality front until closer to the election when we get a very strong tailwind, but so far we seem to be bucking the seasonality trend in September.

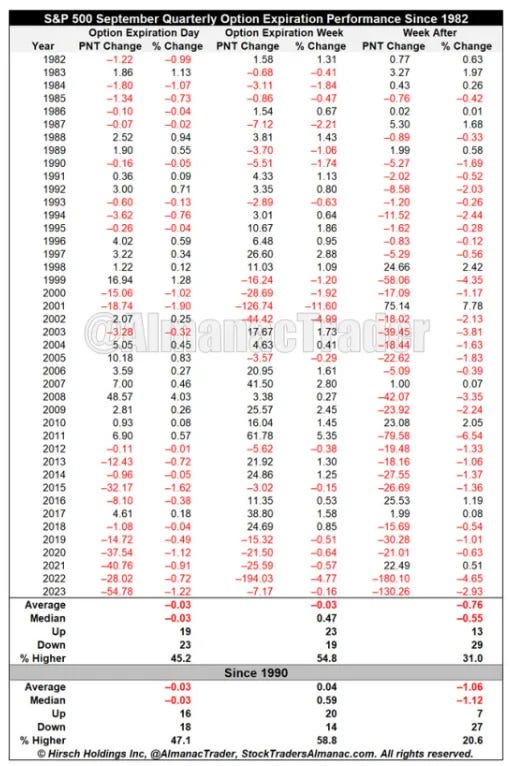

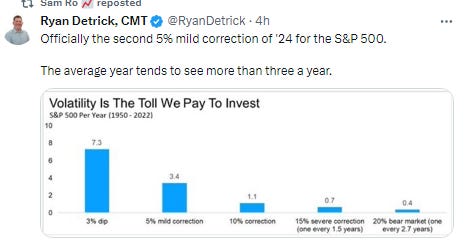

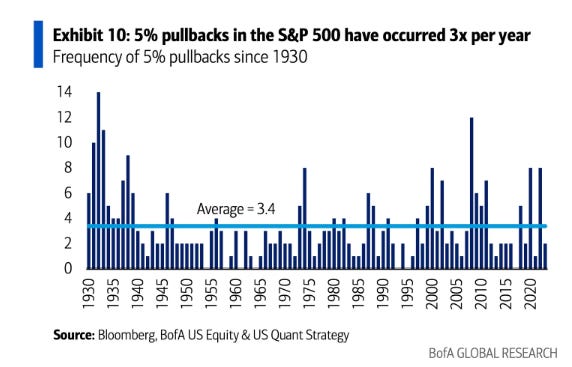

In addition to the normal seasonality issues, we had a “triple-witching” options expiration on Friday. Since 1990 the SPX has fallen -1.1% on avg the week after options expiration w/2021 the only yr in the past 6 that saw a positive week.

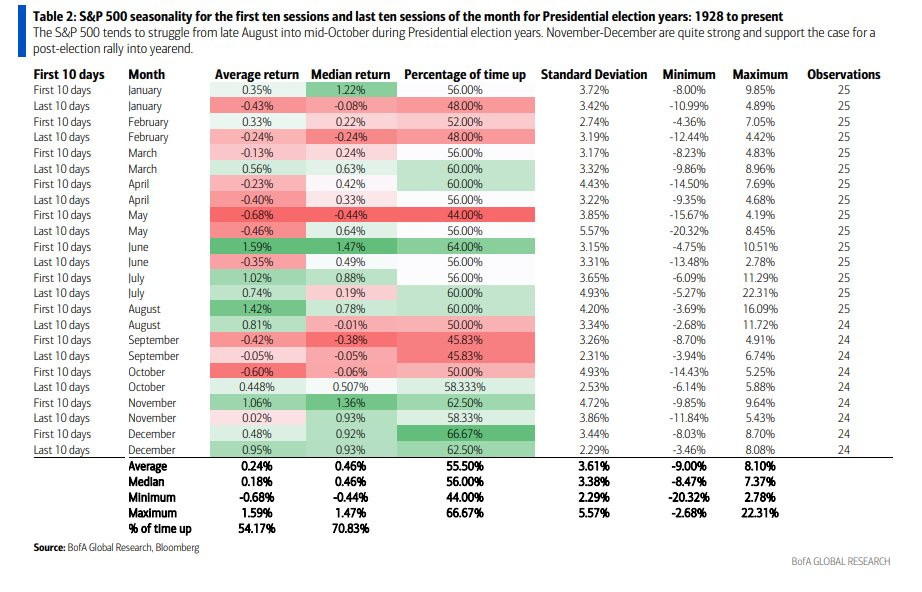

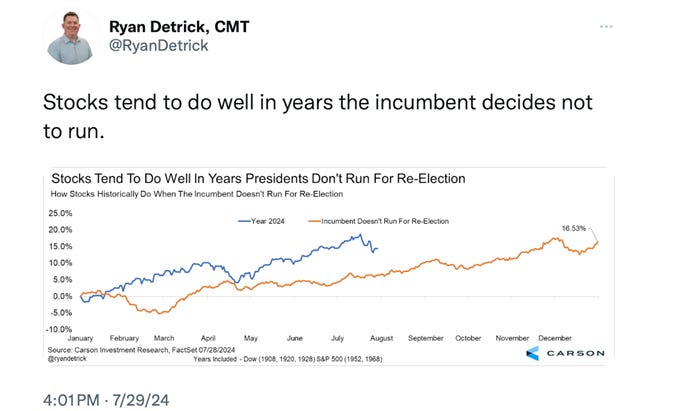

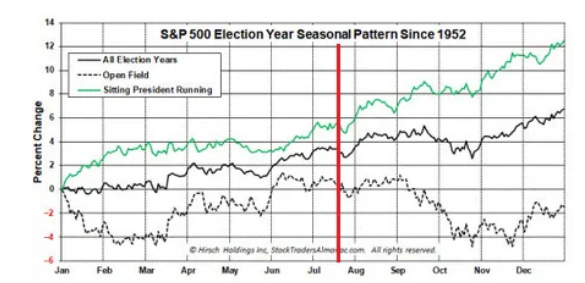

And now we have a new seasonality pattern to consider, an “open field” presidential contest, it's probably no surprise that returns are not nearly as healthy as when a sitting president running (as the incumbent doesn’t have as much interest in a buoyant stock market), but in this case given the very compressed timeframe and the incumbent “choosing” his successor, I think it would be a mistake to follow the open field historical pattern.

And as we consider seasonality, a really nice post from Callie Cox about how you need to take historical analogies w/a grain of salt (unless you've dug into the history). Her chart on Presidential election yr performance w/ & w/o 2008 (when the SPX was -17% in Oct) is a wonderful example.

https://www.optimisticallie.com/p/a-history-lesson

For references to all of the “up YTD through Feb” see the March 3rd post. For all the very positive stats through March (strong 1Q, strong two consec quarters, etc.) see the April 14h post.

For the “as January goes so goes the year”, see the February 4th Week Ahead.

Final Thoughts

As noted last week,

And it appears that whatever it was that catalyzed the selling to start the month did, in fact, “run its course” … Of course, we’re now embarking on the worst two weeks of the year historically as noted in the seasonality section, but as also noted there some think we may have “pulled forward” some of the normal selling. In the argument for more gains we have relatively low positioning, relatively bearish sentiment, a Fed about to embark on a cutting cycle, supportive earnings expectations, not terrible (but not great) valuations, much improved techincials, and expanding breadth. On the other side we have the weak seasonality supported by the entering of the buyback window, the start of tax loss selling season, lofty expectations for Fed rate cuts, and the potential for a reemergence of the carry trade issues. To me there’s a bias for the upside, but it would be easy for any of the multiple catalysts this week (economic data, central banks, etc.) to upset the cart. So I’m steering clear of any predictions for now.

And my thinking of a “bias for upside” turned out to be the right way to go last week. None of the factors noted above have really changed, and on net have turned more favorable (particularly gamma positioning which as noted in the Flows section is back to providing a strong dampener on volatility which will allow systematic strategies to continue to reengage). We do have the issue of the options expiration, which often sees a trend reverse, and we’re now deep into the buyback blackout, so the coast is definitely not all clear, and we’re relatively short term overbought, so some consolidative action is not out of the question. But as BoA noted, weeks that are light on catalysts have generally seen gains, and I don’t see anything this week that should shake up markets (but that said, I should reiterate that flow dynamics are tricky (as are Fed speakers), and between options expiration and the buyback blackout it’s best to stay on your toes this week).

But as I’ve said all year:

Overall this feels like a bull market (the economy is growing, earnings are growing, the Fed is much more likely to be cutting than hiking as its next move, the technical picture and seasonality are strong overall for this year, balance sheets are solid, there’s lots of liquidity, and there’s lots of stocks other than the biggest ones that are performing well (the equal weight SPX hit a new ATH in March, etc.) [this last part has taken a step back with the heightened recession fears - to the extent those soften these will start to perform well]. So if/when we do get that sharp pullback I would think it will likely be an opportunity to buy (like most sharp pullbacks are), not a reason to run for the hills.

And as always just remember pullbacks/corrections are just part of the plan.

Portfolio Notes

Sold out of TD, and trimmed SWN, BANX, BABA, YUMC, CSCO, EEMV, WPP, VFC, CAL, LAZ, BXMT. No adds.

Cash = 12% (held mostly in SGOV, MINT & BOXX (BOXX mimics SGOV but no dividend, all capital appreciation so get long term capital gains if you hold for a year) but also some non-TBill (>1yr duration) Treasury ETF’s (if you exclude those longer duration TBill ETF’s, cash is around 8%)).

Positions (after around the top 20 I don’t keep track of their order on a frequent basis as they’re all less than 0.5% of my portfolio).

Core positions (each 5% or more of portfolio total around 20%) Note the core of my portfolio is energy infrastructure, specifically petroleum focused pipelines (weighted towards MLP’s due to the tax advantages). If you want to know more about reasons to own pipeline companies here are a couple of starter articles, but I’m happy to answer questions or steer you in the right direction. https://finance.yahoo.com/news/pipeline-stocks-101-investor-guide-000940473.html; https://www.globalxetfs.com/energy-mlp-insights-u-s-midstream-pipelines-are-still-attractive-and-can-benefit-from-global-catalysts/)

EPD, ET, PAA

Secondary core positions (each at least 1% of portfolio)

ENB, XOM

For the rest I’ll split based on how I think about them (these are all less than 1% of the portfolio each)

High quality, high conviction (long term), roughly in order of sizing

DIS, SHEL, CVS, CTRA, KHC, GOOGL, ADNT, T, PFE, TRP, BWA, SCHW, APA, ADNT, O, GSK, EQNR, BMY, CMCSA, GILD, TLH, TPR, MTB, DVN, OXY, RHHBY, STLA, NEM, NTR, E, ING, VZ, DAL, KMI, CI, AM, JWN, VSS, ARCC, CVX, AES, SQM, BAC, VNOM, PFF, TFC, MPLX, VOD, FSK, DAL, BAYRY, ING, HBAN, CCJ, BTI, FSK, RRC, FRT, VICI, DGS, WES, INDA, CURLF, MPLX, VWAPY, BMWYY, DDAIF, BUD, KEY, CVE, URNM, URA, SWN, SOFI, BEP, BIIB, SAN, OWL, TEF, SPG, KVUE, KT, ALB, F, VNM, WCC, MT, MFC, GPN, LVMUY, SEE, LYG, NKE, AAPL, ADBE, ORCC, EMN, ZS, ON, NVDA, BCE, MDT, BAX, SNOW, SLB, RTX, LAZ, HAS, DELL, NOC, CHDRY, OCSL, MSM, PHM, TAP, EL, ABNB

High quality, less conviction due to valuation

Higher risk due to business or sector issues; own due to depressed valuation or long term growth potential (secular tailwinds), but at this point I am looking to scale out of these names on strength. These are generally much smaller positions outside of the top few.

ILMN, AGNC, PARA, PYPL, URNM, URA, YUMC, STWD, CFG, FXI, ORAN, KSS, CHWY, TIGO, WBA, ACCO, KVUE, KLG RMD, CLB, HBI, IBIT, UNG, TCNNF, TCEHY, EEMV, PK, VNM, SABR, NSANY, VNQI, VALE, SBH, ST, WBD, LADR, BNS, EWS, , IJS, NOK, SIL, WVFC, VTRS, NYCB, ABEV, TPIC, PEAK, SEE, LBTYK, RBGLY, LAC, CMP, CZR, BBWI, LAC, CAL, EWZ, CPER, MBUU, TLRY, HRTX, MSOS, SIRI, SOYB, DG, CORN

Note: CQP, EPD, ET, MMP, MPLX, PAA, WES all issue K-1s (PAGP is the same as PAA but with a 1099).

Reminder: I am generally a long term investor (12+ month horizon) but about 20% of my portfolio is more short term oriented (just looking for a retracement of a big move for example). This is probably a little more given the current environment. I do like to get paid while I wait though so I am a sucker for a good well supported dividend. I also supplement that with selling calls and puts. When I sell a stock, I almost always use a 1-2% trailstop. If you don’t know what that is, you can look it up on investopedia. But that allows me to continue to participate in a move if it just keeps going. Sometimes those don’t sell for days. When I sell calls or puts I go out 30-60 days and look to buy back at half price. Rather than monitor them I just put in a GTC order at the half price mark.

To subscribe to these summaries, click below (it’s free).

To invite others to check it out,