If you're a new reader or maybe one who doesn’t make it to the end feel free to take a second to subscribe now. Sources are Argus and Bloomberg unless otherwise noted.

As noted in the weekend update (which is much more in depth than the quick summaries, I encourage you to check it out if you haven’t), as with last week there’s reasons to be bullish this week (technicals, breadth, systematic flows(?)), but also reasons to be bearish (remain mildly overbought conditions, technical resistance), and some wildcards (data, global events, Fedspeak, and earnings).

So, overall, as I noted last week, earnings and data will be the big focus for now, particularly with the Fed on autopilot for the next meeting. Last week I was dubious that we could get through resistance given how overbought the market was (although we still remain overbought just not such extremes). This week I’m a little more optimistic, particularly if we can some systematic flows, but emphasis on a little. Breadth remains pretty good though (and ended the week strong) which is an additional tailwind. The beginning of the week is relatively light on data and with no Fed speakers it’s definitely possible we see a rally over resistance. Thursday and Friday will be more about reactions to the data, and all week earnings will be a moderate factor, so any of those have the potential to push us one way or the other. On the negative side, it’s a weak week seasonally, and, well, we are in a bear market for now, so all else equal the general path is down until that’s been broken. We also are still fairly overbought after not having fully reset the more extreme overbought conditions from last week.

And on Monday we did get the positive start to the week I was hoping for. It definitely took the index back over the 200-DMA, and, depending on where you draw the MOAT (Mother Of All Trendlines), we are above that as well. It’s the first close I have over the line since the start of the bear market. It also took us above the closely watched 4000 level that we haven’t closed over since Dec 13th. So no matter how you look at it, a positive day technically. And I postulated that if they haven’t already, CTA’s will be jumping on this train soon. I ended Monday with

Now is the test. Do we get the follow through buying that keeps us above for more than a day or two or do we fall back into the chop like every other time since the start of the bear market? Answer is above my pay grade, but we’ll know soon enough. We do get flash PMI’s tomorrow. I’d be surprised if they are market moving (but they might be if they come in significantly different from expectations which are for more weakness). Also a relatively big day for earnings (see below) so that potentially could impact things as well.

And in contrast to my thinking that the flash PMIs would be dismissed, it appears they had a sizeable impact on trading, particularly in the dollar and bond markets as both the dollar and yields fell sharply following the release (first circles) which gave a lift to equities that were in danger of breaking down (the SPX notably had fallen beneath 4000 at that point). From there equities continued to grind higher throughout the day to end little changed near their highs. They might have done better but for relatively weak earnings releases today. But the recovery kept the SPX above all of those key levels identified above while the Nasdaq and NDX approach those same key levels currently (see chart in the Bloomberg section, and the RUT is also below a key level (19,000)).

Also, if you’re seeing weird stuff on any of your individual stock charts like the ones below (see all the way on the right (bars for today)) there’s more on that below as well.

Dollar

10-year yield

SPX

Argus:

The major indices started today's session in an unexpected manner following a number of aberrations in stock prices for NYSE-listed stocks which led almost instantly to volatility halts with market participants/observers wondering what was happening. The official explanation turned out to be an "exchange-related issue." The issue fortunately was resolved quickly and stocks soon returned to trading in a normal manner. The NYSE will declare a number of trades as “clearly erroneous” from this morning according to a release.

After the early volatility, today's trade was back-and-forth as investors digested a slew of mixed earnings news. Buyers may have also been somewhat reluctant to show strong conviction after the big run recently. Entering today, the Nasdaq Composite was up 8.6% for the year and the S&P 500 was up 4.7%. Considering that and disappointing earnings/guidance from the likes of 3M (MMM 115.00, -7.62, -6.2%), Verizon (VZ 40.42, +0.79, +2.0%), Union Pacific (UNP 203.18, -6.95, -3.3%), and General Electric (GE 80.70, +0.93, +1.2%), the stock market held up fairly well today and showed nice resilience to selling efforts. The S&P 500 was able to maintain its posture above the 4,000 level for most of the session, albeit on very light volume at the NYSE, and the Dow Jones Industrial Average was able to close with a gain of 0.3%.

The Vanguard Mega Cap Growth ETF (MGK) fell 0.3% today versus a 0.1% loss in the S&P 500. Alphabet (GOOG 99.21, -2.00, -2.0%) was among the weakest performers for the mega caps after the U.S. filed an antitrust lawsuit against Google over alleged dominance in digital advertising, according to Bloomberg.

Roughly half of the S&P 500 sectors logged a gain today, but moves were modest in scope in either direction. Industrials (+0.7%) led the outperformers after Lockheed Martin (LMT 449.23, +7.95, +1.8%) and Raytheon Technologies (RTX 99.47, +3.22, +3.4%), which hit a new 52-week high today, reported pleasing quarterly results. To be fair, losses in 3M and Union Pacific weighed on sector gains. The heavily-weighted communication services (-0.7%) and health care (-0.7%) sectors fell to the bottom of the pack, weighing on index level performance. The energy sector (-0.3%) was also among the worst performers amid falling oil prices ($80.23/bbl, -$1.34, -1.6%).

Separately, Treasury yields pulled back today. The 2-yr note yield fell four basis points to 4.19% and the 10-yr note yield fell six basis points to 3.47%.

Ahead of tomorrow's open, Elevance Health (ELV), AT&T (T), Boeing (BA), Progressive (PGR), Abbott Labs (ABT), and Freeport-McMoRan (FCX) are some of the more influential earnings reporters. Looking ahead to Wednesday, market participants will receive the following economic data: 7:00 ET: Weekly MBA Mortgage Index (prior 27.9%) 10:30 ET: Weekly crude oil inventories (prior 8.41 mln)

Bloomberg:

Wall Street saw some buyer fatigue after a solid equity rally, with investors scouring a batch of earnings for clues on the outlook for Corporate America amid mounting fears about a recession. In the run-up to a number of tech earnings after the closing bell, a few other bellwethers reported their numbers. The Dow Jones Transportation Average fell on disappointing results from Union Pacific Corp. 3M Co., the maker of Post-it notes, declined sharply on a profit forecast that trailed estimates and a plan to cut jobs. On the other hand, homebuilder D.R. Horton Inc. beat projections.

A combination of mixed earnings and economic numbers is making investors hesitant to take on more risk particularly after an equity surge that drove the S&P 500 up more than 10% from its mid-October low. US business activity contracted for a seventh month, though at a more moderate pace, while a measure of input prices firmed in a sign of lingering inflationary pressures. “You have to ask: Have investors taken stocks to levels that can’t be supported by what we are about to hear?” wrote Kenny Polcari, senior market strategist at Slatestone Wealth.

In other corporate highlights:

The US Justice Department and eight states sued Alphabet Inc.’s Google, calling for the break up of the search giant’s ad-technology business over alleged illegal monopolization of the digital advertising market.

General Electric Co. continues to grapple with lingering issues in its renewable energy business, even as the slimmed-down manufacturer says strong demand for air travel will help boost overall profits this year.

Johnson & Johnson guided to stronger earnings for 2023 than analysts were expecting after a year in which the pharma division suffered because of waning demand for its unpopular Covid-19 shot.

Halliburton Co. boosted its dividend 33% as the world’s biggest provider of fracking services follows its oil-and-gas clients by expanding shareholder returns amid tight global supplies for crude.

Verizon Communications Inc.’s profit outlook trailed Wall Street estimates in a sign that the consumer wireless business continues to weigh down performance.

After the bell, the $151 billion exchange-traded fund tracking the Nasdaq 100 (QQQ) climbed as Microsoft Corp.’s earnings beat analyst estimates, outweighing Texas Instruments Inc., one of the world’s largest chipmakers, which suffered its first sales decline since 2020 and gave a tepid forecast for the current quarter, hit by an industry slump.

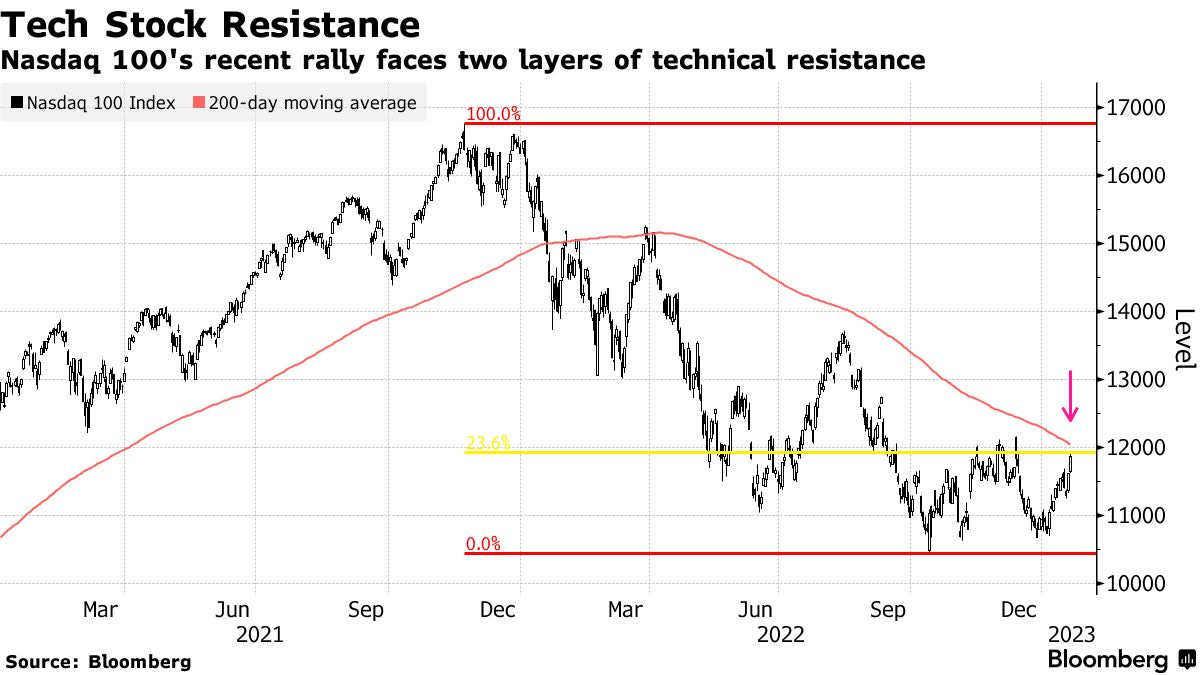

This brings the QQQ to an important technical level. The recent Nasdaq 100 rally has left the gauge just below the 23.6% Fibonacci retracement of its 2021 record high and September low. That level acted as resistance three different times late last year, with rallies fading just above it each time. Even if it does manage a successful break, it will then face a test of its 200-day moving average, a line it hasn’t traded above in nearly a year. [Bloomberg didn’t note it, but there is also a similar MOAT trendline as well].

The popping of the bubble in US stocks is far from over and investors shouldn’t get too excited about a strong start to the year for the market, warns Jeremy Grantham, the co-founder and long-term investment strategist of GMO. “The range of problems is greater than it usually is — maybe as great as I’ve ever seen,” Grantham added.

With the Federal Reserve’s Feb. 1 rate decision about a week away, traders in the options market are contemplating a scenario in which the rate hike it’s expected to deliver ends up being the last one of the tightening cycle. The swap market is pricing around 48 basis points of rate hikes over the next two policy meetings. That implies a small chance — approximately 8% — that if the Fed raises its benchmark rate by a quarter point next week, it could be the central bank’s final move in a tightening cycle that has marked the most aggressive action against inflation in several decades. “It’s almost like people are trying to project forward toward the end the Fed tightening policy and trying to find a bottom here and a new bull-market rally,” said Jerry Braakman, chief investment officer of First American Trust. “But that’s in light of deteriorating economic statistics and I think that’s a little premature.”

‘Null and Void’

The New York Stock Exchange said some trades will be declared “null and void” after determining a “system issue” resulted in a group of securities commencing trading without an opening auction price. A “technical issue” that the exchange didn’t immediately identify resulted in some gyrations that spanned almost 25 percentage points between the high and low in a matter of minutes. Banks, retailers and industrial companies were among those affected, including Wells Fargo & Co., McDonald’s Corp., Walmart Inc. and Morgan Stanley. At least 40 S&P 500 Index stocks were hit with trading halts, according to data compiled by Bloomberg. Walmart and McDonald’s were up and then down as much as 12% before reverting to more normal trading ranges. The exchange said that the trades will be considered as “clearly erroneous” under NYSE rules. It applies to trades in certain securities that did not conduct an opening auction, that occurred after the 9:30 a.m. bell but before certain pricing levels were set, and were executed further from the reference price, NYSE said in an updated statement on its website.

And as might be expected a much weaker SPX sector flag than the last couple of trading sessions, although just had four red sectors and none were down more than around six tenths of a percent. No sector up more than seven tenths though. Growth took a breather from its recent outperformance. Defensives outperformed (consistent with the strength in bonds).

The Morningstarstyle box was even weaker than the last couple of sessions, although like the SPX sectors no style was down more than around six tenths of a percent. But really no style was notably up. Growth underperformed here as well.

Breadth was mixed. 40% of volume was positive on the NYSE, while the Nasdaq had 52%. Issues were 46 and 44%. NYSE volume was weaker than I would have expected, although the RUT being down a quarter percent explains some of that. Nasdaq though outperformed with positive volume despite a negative day, so the breadth in that index continues to be strong, and the NYSE wasn’t really weak although that is the third under 50% day in the past five trading sessions, something to keep an eye on.

Overseas, major equity indices in the Asia-Pacific region ended Tuesday on a higher note while markets in China, Hong Kong, South Korea, and Singapore remained closed for Lunar New Year. Japan's Nikkei: +1.5%, Hong Kong's Hang Seng: CLOSED, China's Shanghai Composite: CLOSED, India's Sensex: +0.1%, South Korea's Kospi: CLOSED, Australia's ASX All Ordinaries: +0.5%. Markets in South Korea and Singapore will reopen tomorrow while Hong Kong will return from holiday on Thursday.

Japan's Manufacturing PMI remained in contraction for the third consecutive month in the flash reading for January, reaching its lowest level since late 2020. But the overall reading returned to growth on a very strong services reading, while Australia saw the fourth monthly contraction in a row, albeit at a shallower level. Commenting on the latest survey results for Japan, Laura Denman, Economist at S&P Global Market Intelligence, said: “Japan’s private sector kicked off 2023 on a more positive note, as signalled by activity returning to growth territory in January. However, similar to trends recorded over much of the past six months, a divergence between the manufacturing and services sectors has remained. While manufacturing firms continued to face muted customer demand, service providers made sustained gains from the travel subsidy programme and recent relaxation of COVID measures. That said, there were some positive developments for manufacturing firms. Rates at which output and new orders declined softened and firms registered a relatively elevated degree of confidence. Input costs and selling prices also increased at the slowest paces in 17- and 16-months, respectively. Conversely, the service sector displayed mixed trends in terms of pricing. While input costs increased at a faster pace, the rate at which firms hiked their prices was the weakest since last August. As such, firms were more cautious about their predictions for the year ahead and registered the lowest level of business sentiment in two years.”

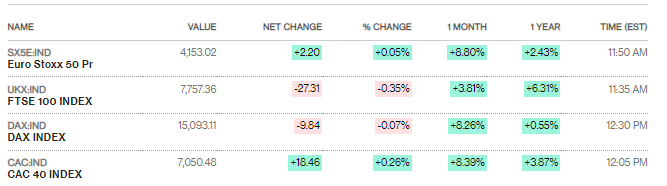

MajorEuropean indices mostly finished little changed recovering from early losses. The UK FTSE 100 underperformed. Yields on 10-year German and British government bonds fell, with the latter weighed down by a particularly poor business activity reading (more below). The European bond gains seeped into Treasury markets, knocking 10-year yields lower. The euro was down against the dollar for the first time in five sessions and the British pound slipping to a one-week low. Traders also pared bets on the peak in the BOE’s key rate, pricing in around 101 basis points of additional hikes by August versus 105 basis points at Monday’s close.

The private-sector economy in the euro area unexpectedly returned to “tentative” and “marginal” growth at the start of 2023 following six months of contraction, offering further signs the region may avoid a recession and comforting the European Central Bank’s focus on underlying inflation risks. S&P Global’s flash Purchasing Managers’ Index rose to 50.2 in January, better than the 49.8 reading predicted in a Bloomberg survey and the first time since June that the gauge was above the 50 threshold that separates expansion from contraction. “The survey suggests a nadir was reached back in October,” Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, remarked. “Since then, fears over the energy market in particular have been alleviated by falling prices, helped by the warmer-than-usual weather and generous government assistance.” While the steadying of the economy does add to evidence the region might escape a recession, “the region is by no means out of the woods yet,” said Chris Williamson, chief business economist at S&P Global Market Intelligence. And readings for the euro area’s two biggest economies remained below 50, though the German services and French manufacturing sectors saw surprise expansions. “Demand continues to fall — merely dropping at a reduced rate — and an upturn in the rate of inflation of selling prices for both goods and services will add encouragement to the hawks to push for further monetary policy tightening,” Williamson said. “The case for higher interest rates is fueled further by the upturn in employment growth recorded during the month and signs of higher wages driving the latest upturn in price pressures,” Williamson said. Still, firms’ outlook improved materially. “Business confidence jumped higher to hint at markedly improving prospects for the year ahead,” the color accompanying the release said. “Employment growth also picked up momentum as firms prepared for a better-than-expected year ahead.”

The above 50 reading in the EU flash composite PMI contrasts with the UK where where companies signaled that output fell at the steepest pace in two years. S&P Global’s reading fell to 47.8 in January from 49 in the previous month, well below the 48.8 estimate in a Bloomberg survey, led by a sharp deterioration in services, which fell to a 2-year low, that had previously propped up the economy. “Service providers experienced a marked loss of momentum since December, with survey respondents citing higher interest rates and low consumer confidence as key factors that held back business activity,” S&P Global said. The pound retreated and gilts rallied. The pace of downturn in manufacturing eased slightly. “Industrial disputes, staff shortages, export losses, the rising cost of living, and higher interest rates all meant the rate of economic decline gathered pace again,” Chris Williamson, chief business economist at S&P Global Market Intelligence, said in a statement Tuesday, “jobs also continued to be lost as firms tightened their belts, though many other firms reported being constrained by an ongoing lack of available labor.” He said the UK is also facing “ongoing damage to the economy from longer-term structural issues such as labor shortages and trade woes linked to Brexit.” In a mixed message for inflation, average prices charged by private sector companies rose “sharply,” and were “driven by historically strong inflationary pressures and efforts to pass on rising staff wages,” although the increase was the slowest in 17 months.

Also, the UK’s budget deficit stood at £27.4 billion ($34 billion), a record for the month of December and almost triple the £10.7 billion shortfall a year earlier, the ONS said today. Economists had forecast a reading of £17.3 billion. “Today’s worse-than-expected public finances figures will only embolden the Chancellor in the budget on 15th March to keep a tight grip on the public finances,” Ruth Gregory at Capital Economics wrote in a note to clients. It means he’ll “waits until closer to the next general election, perhaps in 2024, before announcing any significant tax cuts.” The figures also show that soaring prices and tax rates are bringing more money into the Treasury. The cost of subsidizing gas and electricity is taking a toll, amounting to £7 billion in December alone. Total receipts leaped 11% to £658 billion in the financial year to December. VAT and income tax receipts grew at a double digit pace last month.

Separately, consumer sentiment in the euro area rose to the highest level since last February, a sign of resilience as the region seeks to dodge recession this year. The gauge of confidence increased to -20.9 in January from -22.2 the previous month, according to the European Commission. That’s slightly weaker than the median forecast of economists, who anticipated a pickup to -20.

The German government expects Europe’s biggest economy to grow by 0.2% this year instead of the 0.4% contraction it predicted in October, according to people familiar with new forecasts to be published Wednesday. The government downgraded its growth forecast for next year to 1.8% from 2.3%, according to the people, who asked not to be identified ahead of official publication.

In other markets:

The dollar finished mildly lower but remains in the range of the last week or so, remaining just above my target.

The VIX fell as it continues to churn around the 20 level.

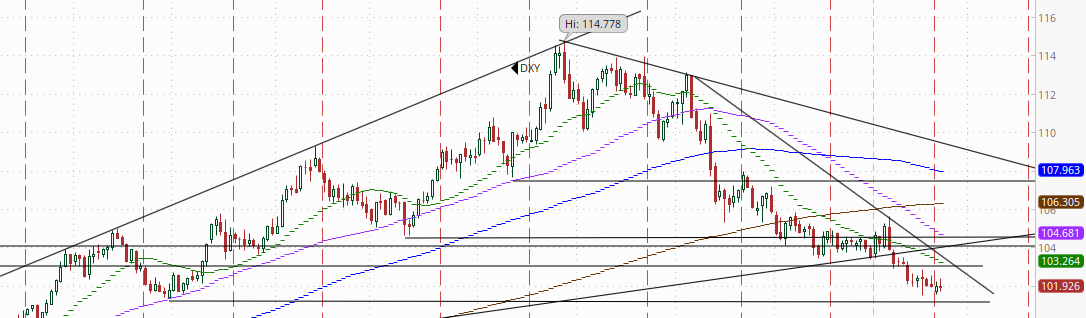

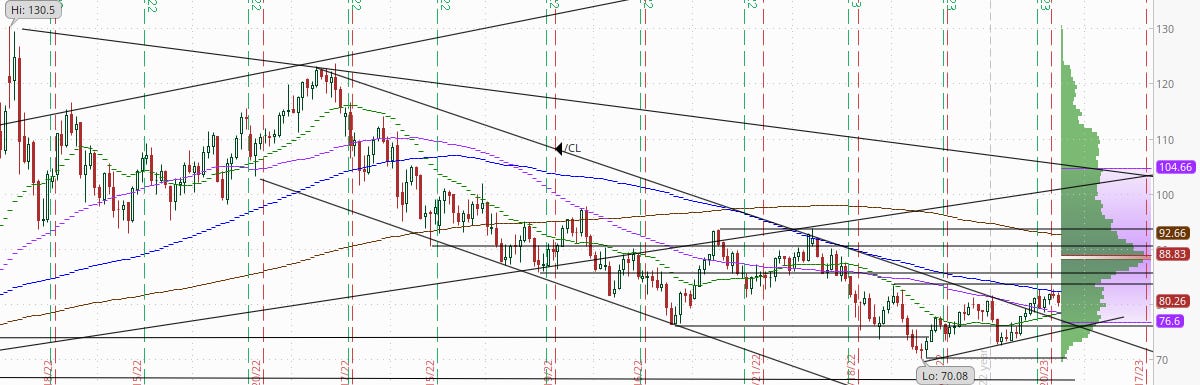

WTI - WTI fell mildly as it continues to struggle with the 100-DMA. Daily technicals remain positive, so I continue to think it’s more likely than not it gets through but as I noted Monday there are layers of resistance above that.

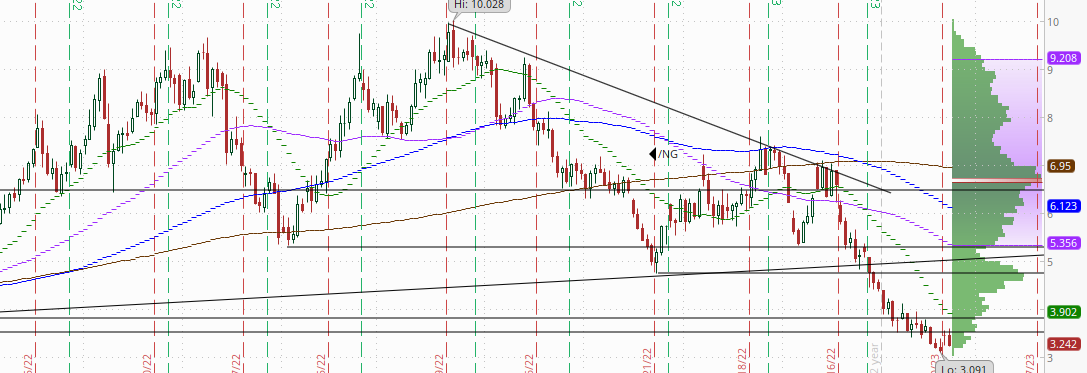

On nat gas, as a reminder after breaking my “must hold” level last week I said “it will bounce somewhere, but where is the question.” Since then I have thought if it can just stabilize a few days we could see it move higher, and it has done that (stabilize) the last couple of days (although it has not been able to really “bounce”. As I noted Monday, if it can get back over the $3.50 level soon, it could turn last week into a “false breakdown” which would be bullish, but it has been rejected the last two days.

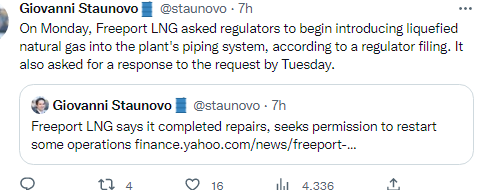

And the weakness was despite some bullish headlines on a potential Freeport restart.

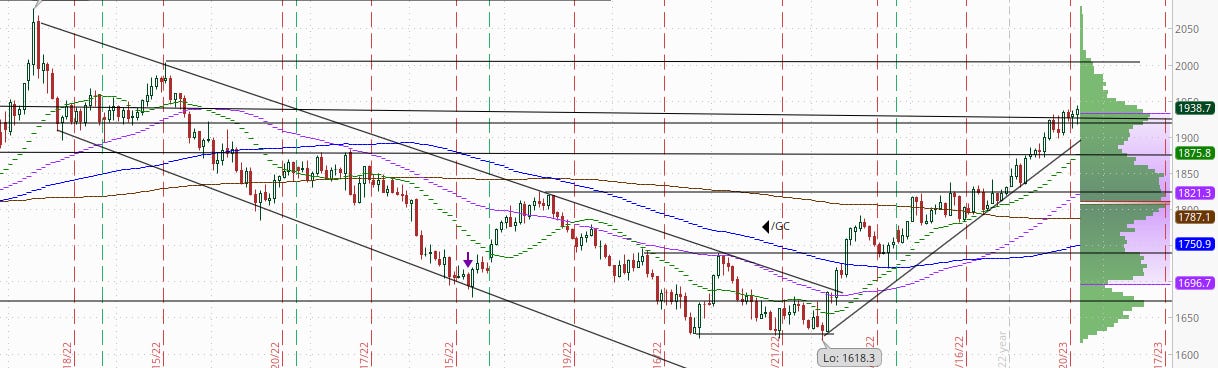

And on gold as a reminder I have been calling for a consolidation for a couple of weeks, but since we turned the calendar into 2023, it has not taken more than a couple of days off in between gains. I noted Monday it had been two days in a row of muted action, and the pattern repeated with gold moving to a new 7-month high (although on a smaller gain than past jumps).

As noted yesterday, after breaking through those well-watched resistance levels, now is the test. As I said, “do we get the follow through buying that keeps us above for more than a day or two or do we fall back into the chop like every other time since the start of the bear market?” Tomorrow is free of any major data, so while earnings will be important (which we will get a lot of), the day’s action might give us some indication of which way the markets seem to want to go (and whether we are getting any of that systematic buying) as we head into the data heavy end of the week.

Note: I’ve try to do a quick-take on Twitter on the bigger economic reports when they’re released if you don’t follow me there currently (link is at the bottom of this summary).

To see more content, including summaries of most major U.S. economic reports and my morning and nightly updates go to Neil’s Newsletter Substack for newer posts or https://sethiassociates.blogspot.com for the full history. You can also follow me on Twitter at @NeilKSethi