Markets Update - 2/9/26

Detailed update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with lots of charts!

To subscribe to these summaries, click below!

To invite others to check it out (sharing is caring!),

Link to posts - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog. Also please note that I do often add to or tweak items after first publishing, so it’s always safest to read it from the website where it will have any updates.

Finally, if you see an error (a chart or text wasn’t updated, etc.), PLEASE put a note in the comments section so I can fix it.

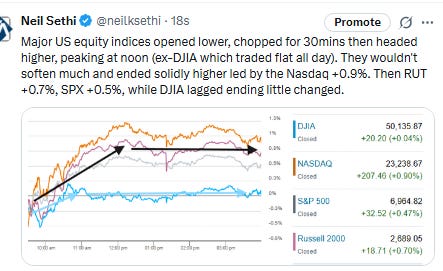

US equity indices opened today’s session modestly lower, not extending on Friday’s rebound on a lighter day for domestic news (as opposed to outside the US where markets were moving on Japan Prime Minister Takaichi’s historic victory (see Asia report) and UK PM Starmer’s crumbling footing (see Europe report).

Indices would chop for the first half-hour then head higher, led again by Tech shares, peaking at noon (other than the DJIA which never made it much past the unchanged mark). Indices wouldn't soften much from the peak and ended solidly higher led by the Nasdaq’s +0.9%. The Russell 2000 followed +0.7%, then SPX +0.5%, and DJIA as noted lagged ending little changed.

Elsewhere, bond yields were slightly lower, but the dollar fell more, its second-worst day since Aug. Natgas was also lower, dropping down towards $3, while gold, crude, copper, and bitcoin all advanced.

The market-cap weighted S&P 500 (SPX) was +0.5%, the equal weighted S&P 500 index (SPXEW) +0.1%, Nasdaq Composite +0.9% (and the top 100 Nasdaq stocks (NDX) +0.8%), the SOXX semiconductor index +1.4% (after +5.7% Friday, the best day since May), and the Russell 2000 (RUT) +0.7% (after +3.6% Friday).

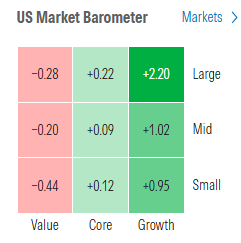

Morningstar style box a neopolitan look with growth outperforming, value lagging.

Market commentary:

“After an eight-day losing streak, buyers finally stepped back into the software space on Friday, underpinning a much-needed relief rally as the tech sector approached key support near the November lows,” said Adam Turnquist, chief technical strategist at LPL Financial. “While this marked a step in the right direction, the broader tech complex remains rangebound until it can decisively break above the December highs.”

“For the broader market to make sustainable progress, renewed tech participation will likely be essential,” he also said, adding that he anticipates the S&P 500 will have some trouble reaching 7,000 without more participation from tech, especially software.

“When markets sell off like certain areas in tech have, there’s often knee-jerk rallies,” said Sameer Samana at Wells Fargo Investment Institute. “Time will tell if we need a retest or if enough value was created.” Wells Fargo Investment Institute is “neutral” on tech and “most favorable” on financials, while also taking a favorable view of industrials and utilities, according to Sameer Samana, the Wall Street firm’s head of global equities and real assets.

“We don’t know who the winners of AI will be, but financials, industrials and utilities can help to support” whichever Big Tech companies take the lead on the buildout of artificial intelligence, Samana said in a phone interview Monday.

“Monday’s equity rally continues to smack of short covering, and that coupled with other risks leaves stocks still on shaky ground near-term. Punters’ animal spirits aren’t quite dead yet, but the absence of long-term buyers in the rally suggests they’re waiting for clarity.” —Alyce Andres, Macro Strategist, Markets Live.

“Expect swings to continue until we have clearer visibility on the AI monetization, as well as the Fed’s rate path,” said Desmond Tjiang, chief investment officer for equities and multi-asset investment at BEA Union Investment.

“These moves also make people say, ‘Let me be a little bit more cautious than I had been” and wait for a better opportunity,” said Keith Lerner, chief investment officer at Truist Advisory Services.

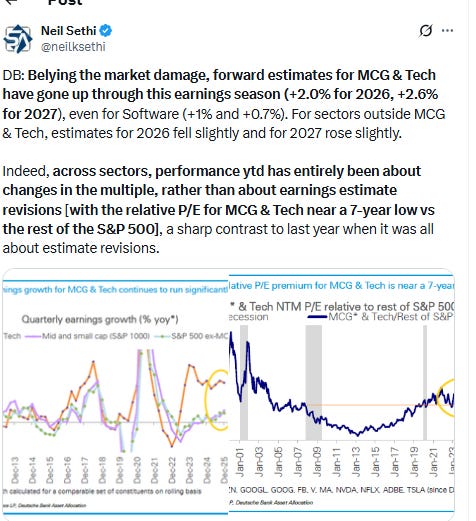

The technology sector reset was a necessary digestion of prior gains, with the industry projected to record earnings-per-share growth of 32% in 2026, followed by an additional 20% in 2027, according to Sam Stovall at CFRA. That compares with the S&P 500’s projected gains of 13% and 16%, respectively.

“Should these EPS growth estimates continue to hold up, investors will be pleased they stayed the course,” he said. “Investors are saying, ‘Okay, we had a tremendous bounce back. Does that have staying power? Is this something that I could get sucked into and only end up getting trounced, or is this really another buying opportunity?’” said Stovall. “We went from a 17% premium to an 8% discount,” the chief investment strategist said about tech’s forward price-to-earnings ratio compared with its average for the past five years. “You could say, ‘Well, gee, that’s pretty good, and so maybe it’s time not to bail out on technology just yet.’

Jed Ellerbroek, portfolio manager at Argent Capital Management, noted that software names were seeing some relief on Monday after a punishing stretch.

“Software isn’t getting wiped out today, it’s not doing great, but it’s not getting wiped out the way it has over the past month,” he told MarketWatch. Ellerbroek also pointed to the big bounce in shares of Nvidia Corp. and Broadcom Inc. “We’re seeing full participation from that AI capex beneficiary group,” he said. More recently, performance in the AI space has favored industrial names like Caterpillar Inc. that were expected to benefit from the ongoing data-center build-out.

There seems to be faith that mega-tech companies know what they are doing in pouring so much money into building out the massive data centers, according to veteran Wall Street strategist Louis Navellier. “There remain doubts as to the timing of the return on the huge investment, as well as the apparent restraint on coming up with the needed power supplies, but we’re already seeing significant job reductions due to the efficiencies of early implementation of AI solutions,” he said.

The S&P 500 is poised for more gains this year as last week’s volatility is likely to remain brief, according to strategists at RBC Capital Markets. The team led by Lori Calvasina says the five models they track still argue for “solid gains” in stocks, while noting that historical data on recent drawdowns suggest “it’s possible that this latest bout of weakness has played out for now.” The strategists maintain their 12-month price target of 7,750 points for the S&P 500.

“We think that the fourth quarter earnings season continues to be supportive for US equities,” said David Lefkowitz at UBS Global Wealth Management. “Solid growth, supportive central banks, and AI should be the key drivers of further upside for US stocks. We maintain our June 2026 and December 2026 S&P 500 price targets of 7,300 and 7,700.”

“Market action during the last week of January felt increasingly toppy to us over the near term,” said Chris Senyek at Wolfe Research. “Last week, this played out in full force with a flat S&P 500 belying the massive churning of the markets underneath the surface with wild price moves across all sectors and factors as forced selling in tech triggered a massive factor unwind.” Senyek expects continued volatility in the days ahead. He noted that an area like consumer staples that has done so well this year is well overbought while non-software tech stocks remain “very crowded” not only with institutional investors but retail as well. “Further systematic selling is likely to continue over the near term,” Senyek said. “Among other things, we’d like to see the HF crowding factor we follow closely revert back to its long-term average.”

While software and the broader tech trade have seen selling to start the year, the percentage of stocks in the S&P 500 making new 52-week highs has been expanding and just hit its highest level in the past year to end last week, according to Bespoke Investment Group strategists. “One of the reasons overall market breadth has been so strong is that consumer staples stocks have caught a huge bid,” they said. “While the S&P 500’s net-new highs breakout is a bullish sign, you don’t really want to see defensives leading a rally.”

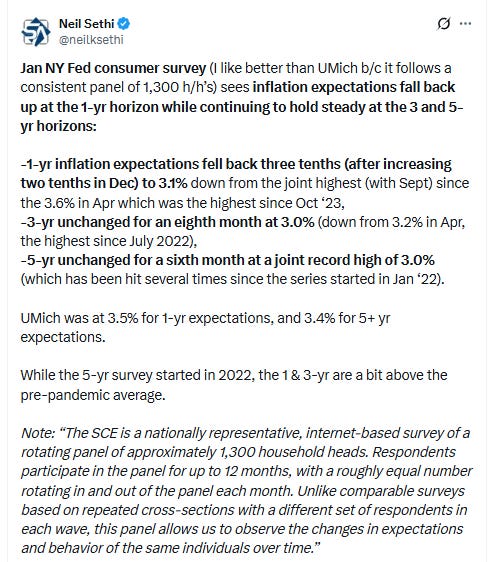

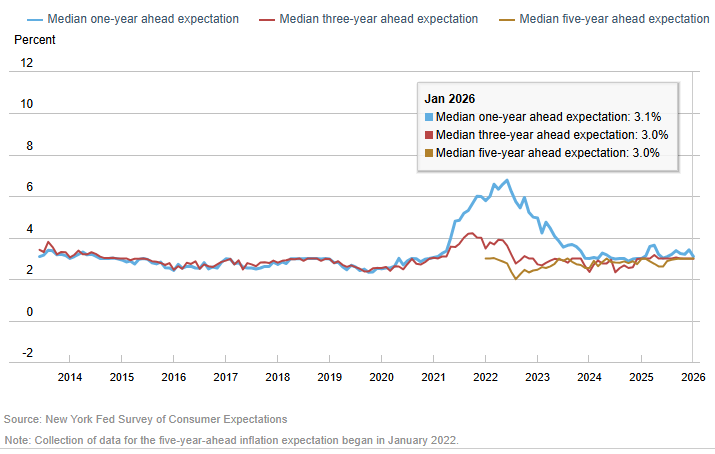

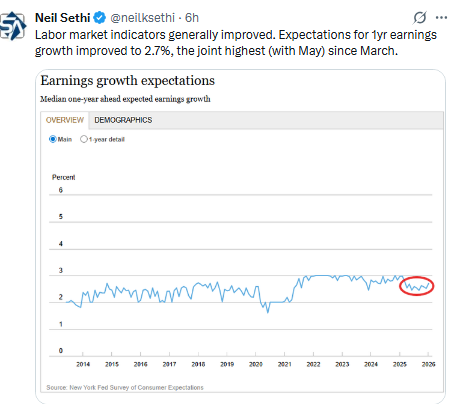

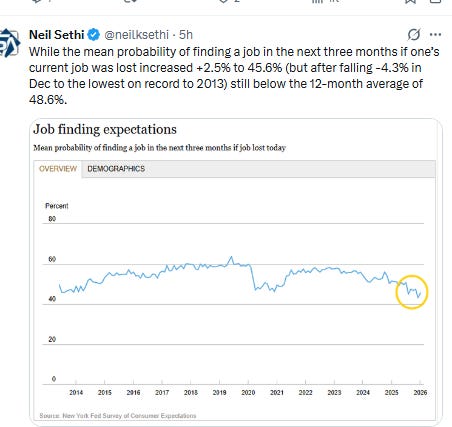

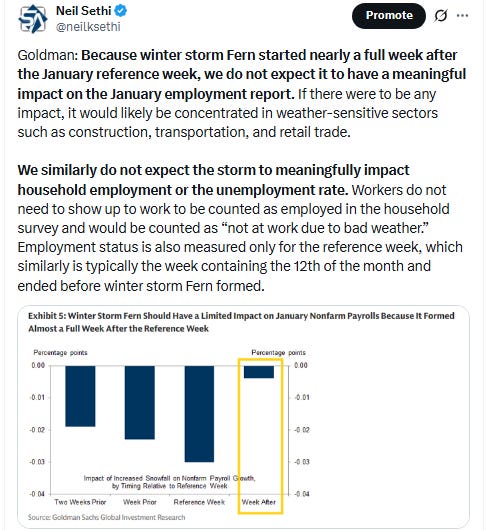

Meantime, this week’s employment data and CPI report may prove pivotal for the Fed as it balances slowing job growth against lingering inflation risks, according to Jason Pride and Michael Reynolds at Glenmede. A meaningful upside surprise in goods or services inflation could narrow the runway for rate cuts in 2026, they added.

“This week brings two of the most important economic data releases in the same calendar week, a rare occurrence due to the brief government shutdown earlier this month,” said Arthur Hogan at B. Riley Wealth. “That means both sides of the Federal Reserve’s dual mandate will be represented with fresh data.”

For each report, a “Goldilocks” outcome that implies solid growth and stable price pressures is the best case for the market, helping support stocks, according to Tom Essaye at The Sevens Report. “Economic data has been almost perfectly Goldilocks since the government re-opened in late November and that needs to continue to help stocks weather rising AI skepticism,” Essaye noted.

“We’re watching whether early-year price pressures will be contained after strong core inflation in January,” said BlackRock Investment Institute strategists. “The jobs report for January will shed light on whether the ‘no hiring, no firing’ stasis in jobs persists. If so, and inflation proves little changed, we see the Fed leaving rates unchanged at its next meeting.”

“A so-so jobs report probably won’t have much of an impact, but traders expecting stocks to bounce on weak numbers have to consider the possibility that a choppy stock market may simply treat good news as good and bad news as bad,” said Chris Larkin at E*Trade from Morgan Stanley.

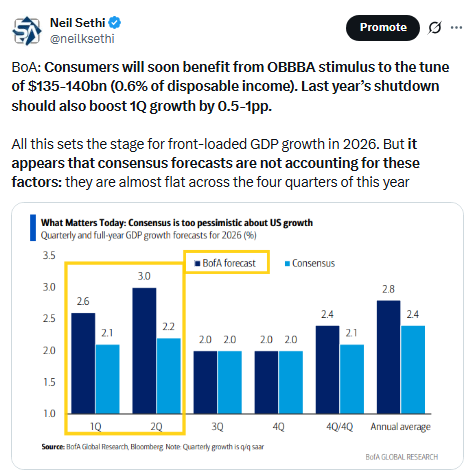

“The underlying US economy is about to take off,” said Torsten Slok at Apollo. “The bottom line is that it is very difficult to be bearish on the US economic outlook.”

“At least two cuts this year, maybe three cuts. Given the easing that we’ve already seen, I think the US economy probably will accelerate this year,” Paul Jackson, global market strategist at Invesco, told Bloomberg TV.

“The 10-year Treasury yield has been well behaved through this recent stock market volatility and in the 4.20% range it remains neutral for markets generally speaking,” Tom Essaye, founder and president of Sevens Report Research, wrote in a note Monday. “That needs to continue, because a sudden plunge below 4.00% would signal growth concerns, while a jump above 4.50% would imply rising inflation risks and both would add incremental headwinds on stocks (and possibly bonds).”

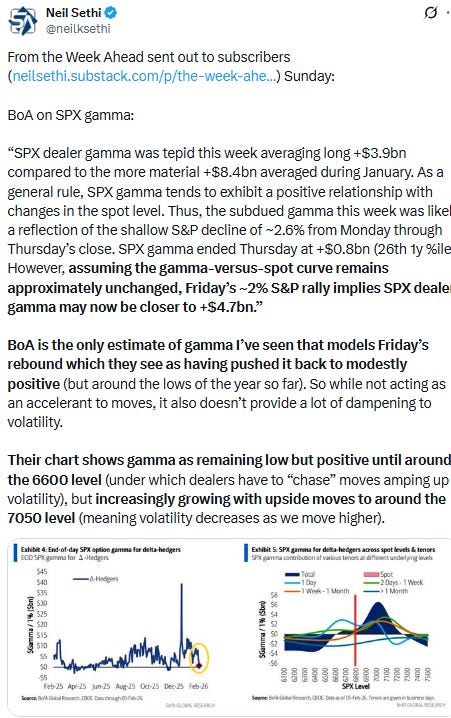

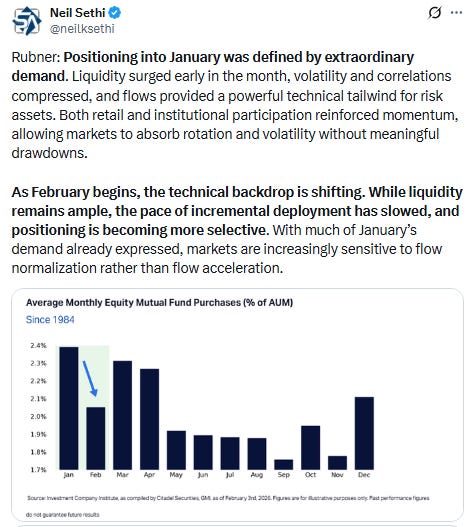

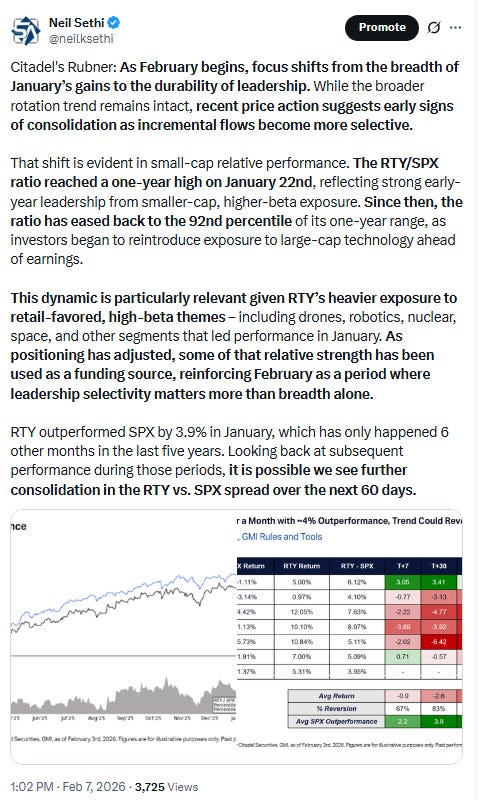

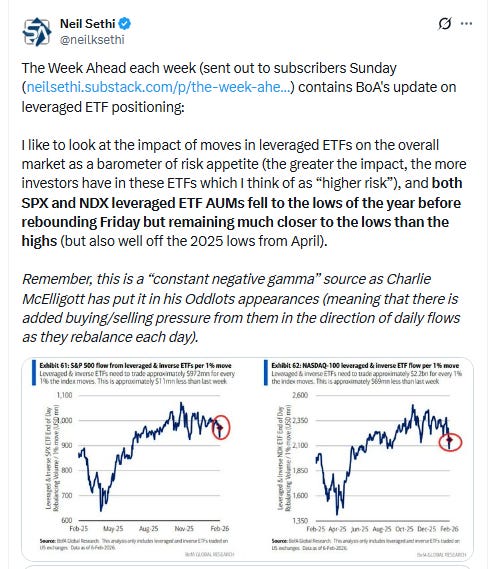

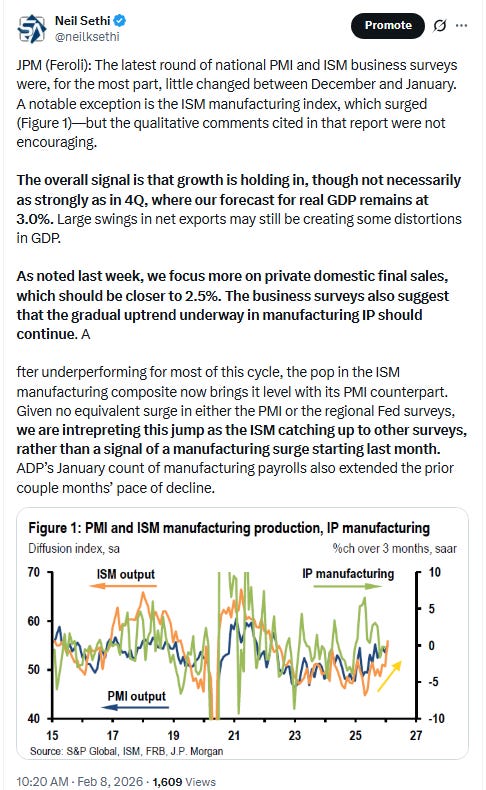

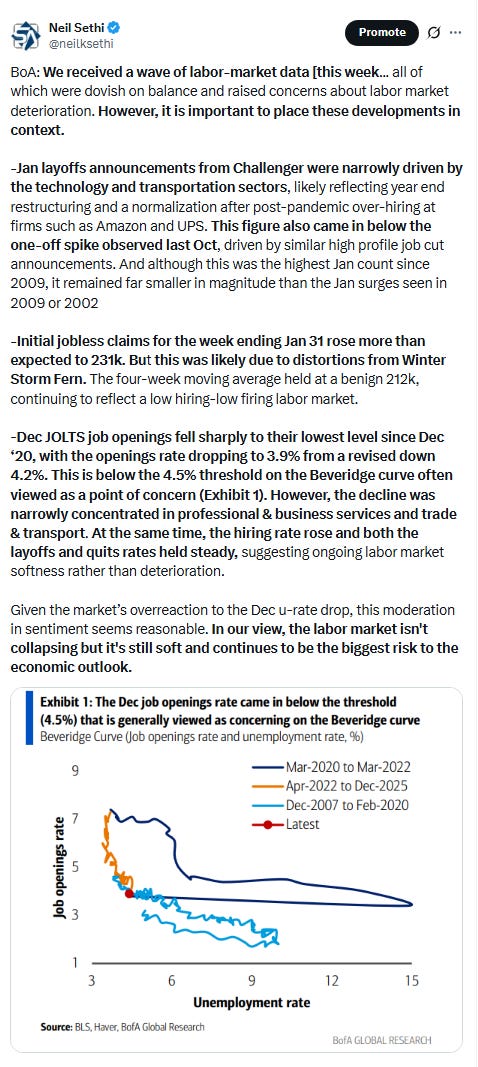

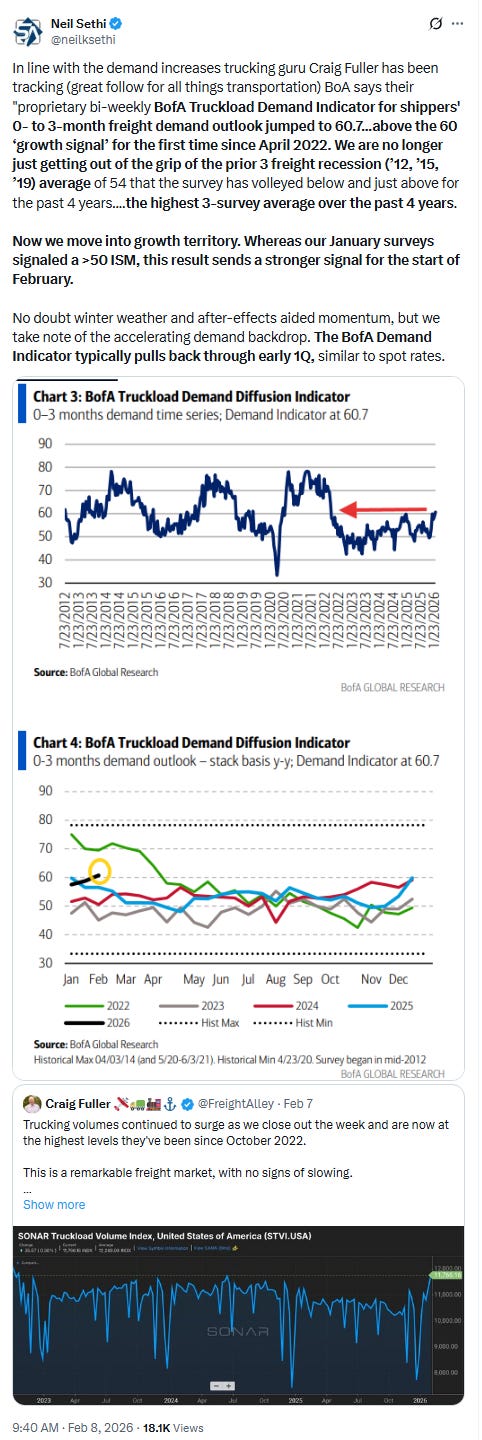

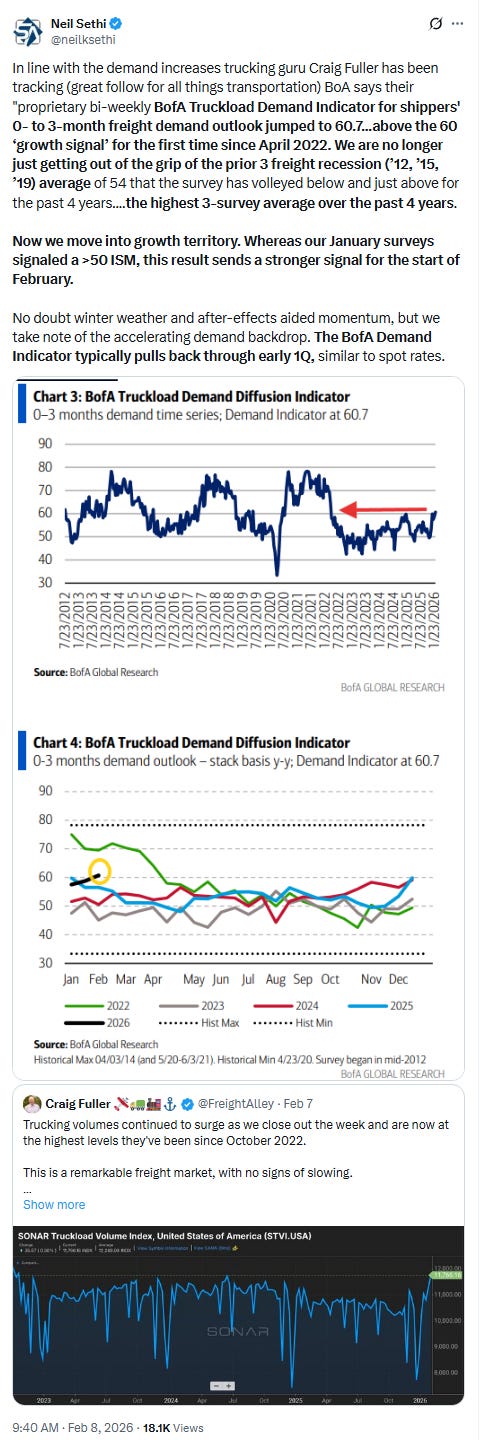

These were all included in last night’s Week Ahead for subscribers:

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

In individual stock action:

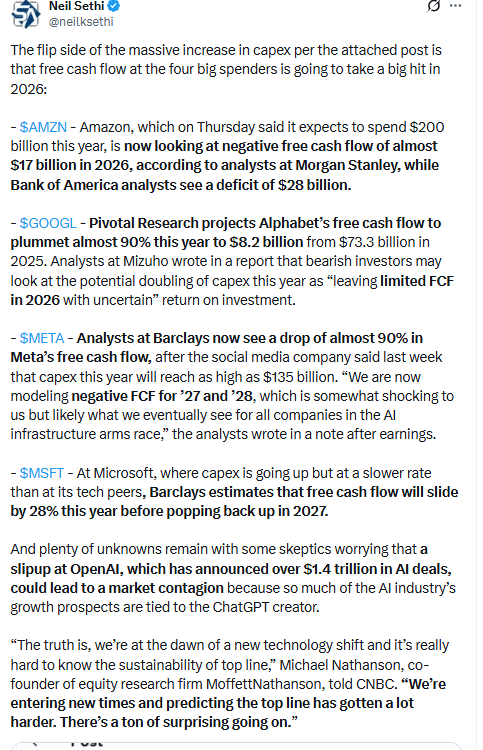

Nvidia and Broadcom were standouts yet again Monday, extending their gains from the previous session with an advance of 2.5% and 3.3%, respectively. Shares of fellow artificial intelligence player Oracle were up 9.6% after receiving an upgrade to buy from neutral at D.A. Davidson due to optimism around OpenAI and its beneficiaries.

A gauge of chipmakers climbed 1.4% while an ETF focused on software names extended a back-to-back advance to almost 7%. Alphabet Inc. embarked on a global bond spree to fund its AI ambitions.

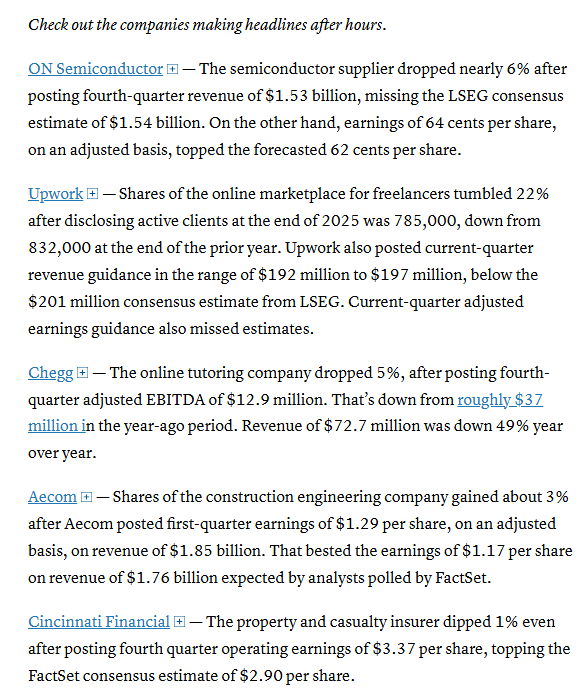

Companies making the biggest moves after-hours from CNBC.

Corporate Highlights from BBG:

Microsoft Corp. shares were downgraded for the second time in less than a week as Wall Street grows increasingly wary about the potential disruption software stocks face from artificial intelligence.

Meta Platforms Inc. was given a European Union warning over policies that block the use of rival Artificial Intelligence assistants on WhatsApp, raising the possibility of further tensions with the Trump administration over the regulation of US tech companies.

While most Americans were transfixed by this year’s Super Bowl proceedings on Sunday night, Elon Musk took to X to proclaim that SpaceX would focus on building out a base on the moon before sending humans to Mars.

Kyndryl Holdings Inc., an International Business Machines Corp. spinoff, plunged after the company announced key leadership exits and a review of its accounting practices.

Eli Lilly & Co. agreed to buy closely held US biotech Orna Therapeutics Inc. for up $2.4 billion in cash, its second deal in as many days as the company expands its pipeline beyond its well-known blockbuster obesity drug Zepbound.

Novo Nordisk A/S said it’s suing Hims & Hers Health Inc. for making knock-offs of its obesity medicines, even as Hims scrapped plans to sell a copycat version of the Wegovy pill.

The US Food and Drug Administration said a TV advertisement for Novo Nordisk A/S’s new weight-loss pill included “false or misleading” claims about the drug’s ability to help users shed pounds, adding to the drugmakers’ recent woes.

Kroger Co. plans to name Greg Foran as the supermarket chain’s next chief executive officer, according to a person familiar with the matter, as the nation’s largest grocer looks to carve a new path after a failed megadeal and an unexpected exit of its former boss.

Converse employees have been instructed to work from home ahead of layoffs and restructuring at the struggling Nike Inc. brand.

Apollo Global Management Inc. set a record in its business of making loans, a crucial plank in the firm’s ambition to become one of the largest underwriters on Wall Street.

Chevron Corp. acquired a ranch in West Texas whose owner had been waging a legal battle accusing the US energy giant of negligently spilling toxic water and crude oil on the 22,000-acre property.

Workday Inc. announced co-founder Aneel Bhusri is returning to head the software company, replacing chief executive officer Carl Eschenbach after the company’s shares have plummeted over the past year.

Activist investor HoldCo Asset Management called a truce with two US regional banks and said it now supports KeyCorp’s chief executive officer after previously calling for his ouster.

Cleveland-Cliffs Inc. plunged after the US steelmaker said it needed more time to land a deal with South Korea’s POSCO.

Deep-water oil rig owner Transocean Ltd. agreed to acquire rival Valaris Ltd. in an all-stock deal valued at $5.8 billion as offshore drilling activity heats up.

Newmont Corp. wants Barrick Mining Corp. to address what it says is underperformance at their joint venture mining operations in Nevada before its partner proceeds with an initial public offering of its North American assets.

Expand Energy Corp. said Domenic “Nick” Dell’Osso, Jr. stepped down as chief executive officer as the largest US natural gas producer plans to relocate its headquarters to Houston from Oklahoma City in mid-2026.

Clothing retailer Eddie Bauer LLC filed for Chapter 11 in what marks the chain’s third trip to bankruptcy court. This time, the plan is to sell as many as possible of its 175 stores — which employ about 2,200 people — and liquidate the rest.

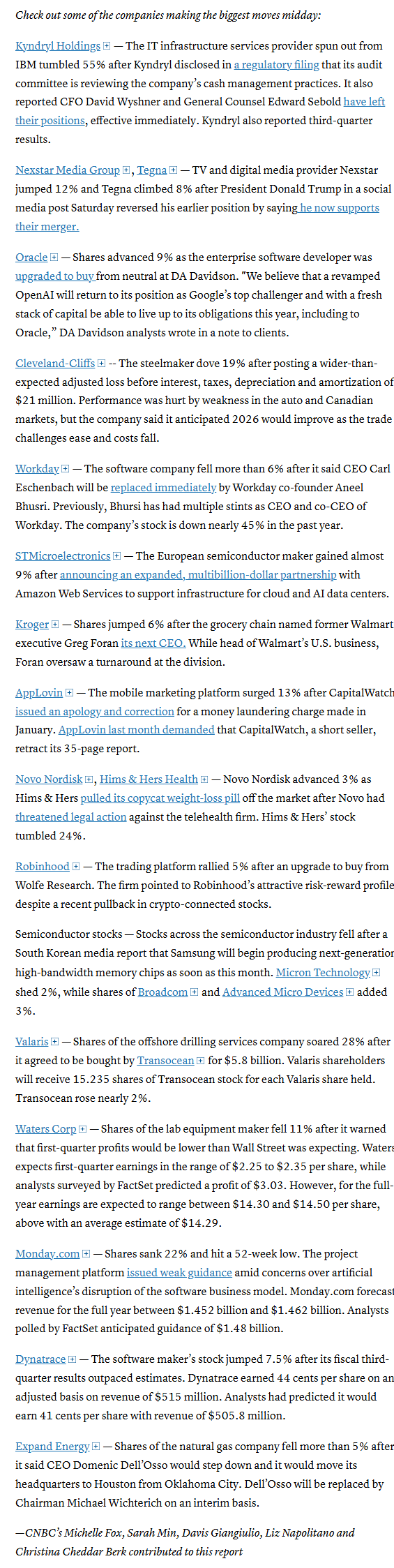

Mid-day movers from CNBC:

In US economic data:

These were all included in last night’s Week Ahead for subscribers:

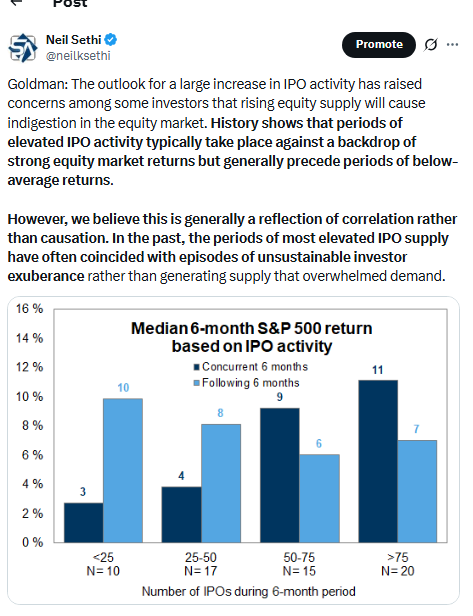

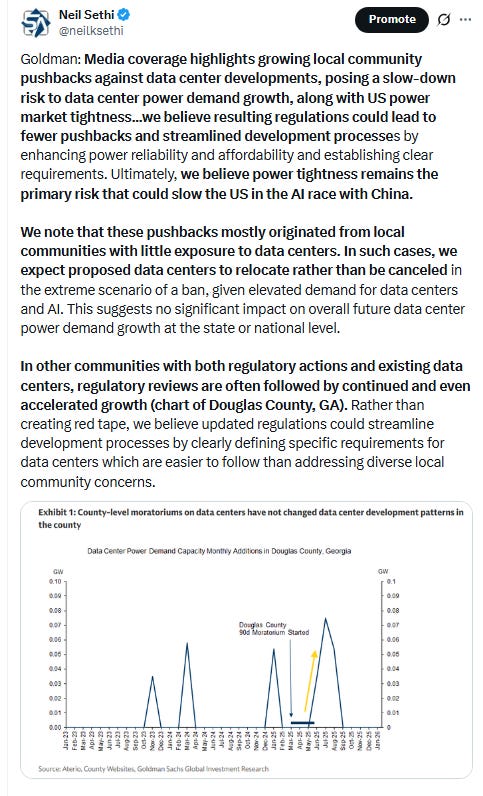

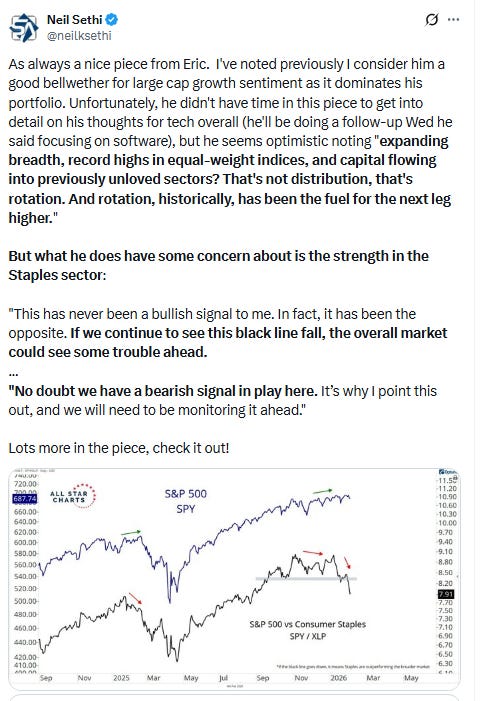

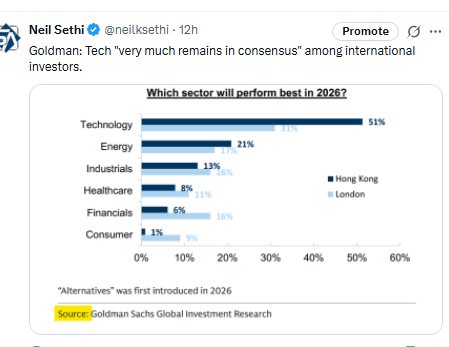

Substack articles:

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X