If you're a new reader or maybe one who doesn’t make it to the end feel free to take a second to subscribe now. Sources are Argus and Bloomberg unless otherwise noted.

As noted in the weekend update (which is much more in depth than the quick summaries, I encourage you to check it out if you haven’t), as with last week there’s reasons to be bullish this week (technicals, breadth, systematic flows(?)), but also reasons to be bearish (remain mildly overbought conditions, technical resistance), and some wildcards (data, global events, Fedspeak, and earnings).

So, overall, as I noted last week, earnings and data will be the big focus for now, particularly with the Fed on autopilot for the next meeting. Last week I was dubious that we could get through resistance given how overbought the market was (although we still remain overbought just not such extremes). This week I’m a little more optimistic, particularly if we can some systematic flows, but emphasis on a little. Breadth remains pretty good though (and ended the week strong) which is an additional tailwind. The beginning of the week is relatively light on data and with no Fed speakers it’s definitely possible we see a rally over resistance. Thursday and Friday will be more about reactions to the data, and all week earnings will be a moderate factor, so any of those have the potential to push us one way or the other. On the negative side, it’s a weak week seasonally, and, well, we are in a bear market for now, so all else equal the general path is down until that’s been broken. We also are still fairly overbought after not having fully reset the more extreme overbought conditions from last week.

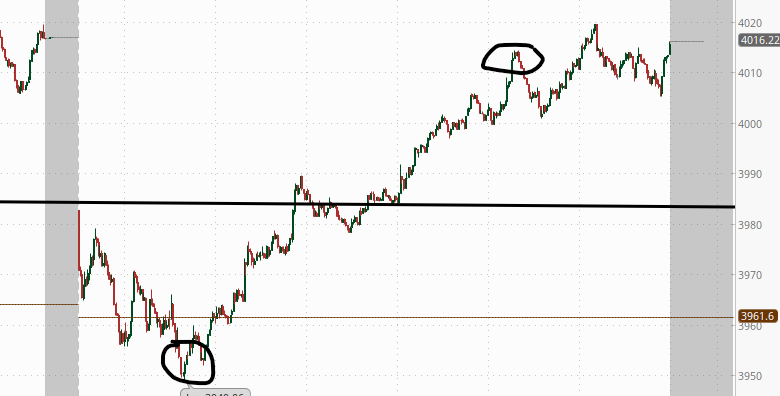

And on Monday we did get the positive start to the week I was hoping for. It definitely took the index back over the 200-DMA, and, depending on where you draw the MOAT (Mother Of All Trendlines), we are above that as well. It’s the first close I have over the line since the start of the bear market. It also took us above the closely watched 4000 level that we haven’t closed over since Dec 13th. So no matter how you look at it, a positive day technically. And I postulated that if they haven’t already, CTA’s will be jumping on this train soon. I ended Monday with

Now is the test. Do we get the follow through buying that keeps us above for more than a day or two or do we fall back into the chop like every other time since the start of the bear market? Answer is above my pay grade, but we’ll know soon enough. We do get flash PMI’s tomorrow. I’d be surprised if they are market moving (but they might be if they come in significantly different from expectations which are for more weakness). Also a relatively big day for earnings (see below) so that potentially could impact things as well.

But on Tuesday in contrast to my thinking that the flash PMIs would be dismissed, it appears they had a sizeable impact on trading, particularly in the dollar and bond markets as both the dollar and yields fell sharply following the release (see charts in Tuesday’s wrap up) which gave a lift to equities that were in danger of breaking down (the SPX notably had fallen beneath 4000 at that point). From there equities continued to grind higher throughout the day to end little changed near their highs. They might have done better but for relatively weak earnings releases. But the recovery kept the SPX above all of those key levels identified above while the Nasdaq and NDX approach those same key levels currently (see chart in the Bloomberg section of Tuesday’s wrap-up), and the RUT is also below a key level (19,000)). I ended Tuesday with:

As noted Monday, after breaking through those well-watched resistance levels, now is the test. As I said, “do we get the follow through buying that keeps us above for more than a day or two or do we fall back into the chop like every other time since the start of the bear market?” Wednesday is free of any major data, so while earnings will be important (which we will get a lot of), the day’s action might give us some indication of which way the markets seem to want to go (and whether we are getting any of that systematic buying) as we head into the data heavy end of the week.

And earnings were in fact “important” today, particularly those from heavyweight Microsoft (easily the second largest stock in the indices) along with Dow component Boeing. Those in addition to other weak reports (see more below) had stocks down early with the SPX at one point -1.5%. But whereas Tuesday the recovery was fueled by a big drop in bond yields on the back of weak PMI’s, today stocks recovered in the face of modestly rising yields (although yields still finished lower on the day). The recovery was also more impressive than Tuesday’s due to the fact that at the lows the SPX had fallen beneath all of those well watched levels (4000, MOAT, 200-DMA), making today’s action notable to me. Still it left the major indices little changed for a second day, an inconclusive result at best ahead of more earnings and some key economic data tomorrow.

Dollar

10-year yield

SPX

Argus:

Today's trade looked a lot different at the open compared to where things ended up. Valuation concerns following Microsoft's (MSFT 240.61, -1.43, -0.6%) disappointing fiscal Q3 outlook and expected growth deceleration for its Azure business fueled a broad retreat to kick off the session. Investors also had a negative reaction initially to results and/or guidance from the likes of Dow component Boeing (BA 212.68, +0.70, +0.3%), Texas Instruments (TXN 175.04, -2.00, -1.1%), Kimberly-Clark (KMB 132.06, -2.57, -1.9%), and Norfolk Southern (NSC 242.97, -12.91, -5.1%). This added to the early weakness and the sense that the market might have gotten ahead of itself with the January rally.

Sentiment started to shift, however, when buyers showed up fairly quickly after the S&P 500 slipped below its 200-day moving average (3,961). Most stocks either narrowed their losses or completely recovered and closed the session with a gain. The Invesco S&P 500 Equal Weight ETF (RSP) was down 1.4% at its low for the day, but managed to close with a 0.2% gain. Notably, the Russell 2000 (+0.3%) and S&P Mid Cap 400 (+0.3%) outpaced the three main indices today to close with a modest gain. Even Microsoft, which had been down as much as 4.6%, briefly tipped into positive territory before settling with a slim loss.

The resilience to early selling efforts became its own upside catalyst and the rebound effort picked up steam in the afternoon trade, likely driven by some short-covering activity and a fear of missing out on a potential breakout move. The main indices ultimately closed near their best levels of the day, which had the S&P 500 above the 4,000 level and the Dow Jones Industrial Average in positive territory.

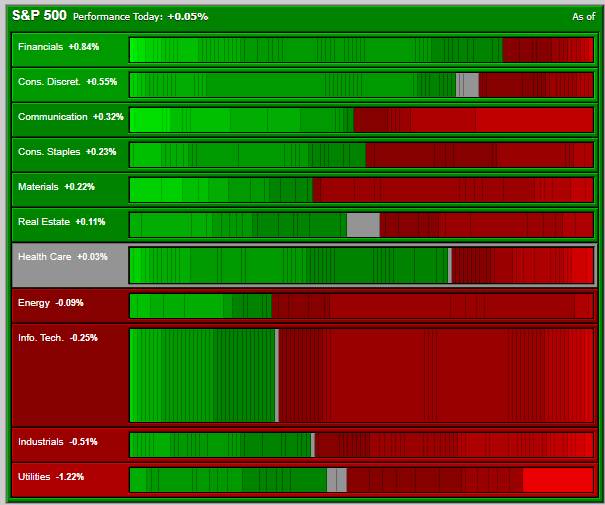

Market internals highlight the strong reversal seen today. Early on, decliners led adv ancers by a 4-to-1 margin at the NYSE and a nearly 3-to-1 margin at the Nasdaq. At the close, advancing issues had the lead over decliners by a slim margin at both the NYSE and the Nasdaq. Roughly half of the 11 S&P 500 sectors closed with a gain led by financials (+0.7%) thanks to an earnings-driven gain in Capital One (COF 116.09, +9.58, +9.0%). The defensive-oriented utilities sector (-1.3%) was the worst performer and the only sector to move more than 1.0%.

Looking ahead to Thursday, market participants will receive the following economic data: 8:30 ET: Advance Q4 GDP (Briefing.com consensus 2.6%; prior 3.2%), advance Q4 Chain Deflator (Briefing.com consensus 3.2%; prior 4.4%) -December Durable Orders (Briefing.com consensus 2.9%; prior -2.1%), Durable Orders ex-transportation (Briefing.com consensus -0.2%; prior 0.2%) -Weekly Initial Claims (Briefing.com consensus 205,000; prior 190,000), Continuing Claims (prior 1.647 mln) - December advance goods trade deficit (prior -$83.30 bln), December advance Retail Inventories (prior -0.3%), and December advance Wholesale Inventories (prior 1.0%) 10:00 ET: December New Home Sales (Briefing.com consensus 614,000; prior 640,000) 10:30 ET: Weekly natural gas inventories (prior -82 bcf)

Bloomberg:

Wall Street shook off most of the losses driven by a dire sales warning from Microsoft Corp., with stock traders shifting their focus to Tesla Inc.’s earnings report after the closing bell. The S&P 500 almost erased a slide that topped 1.5% earlier in the day. “The push-and-pull of bulls and bears continues, with technology earnings the latest data point to energize the bears, though the positive momentum, continued heavy skepticism of the rally and the attractiveness of several areas of the markets could break equities out to the upside,” said Mark Hackett, chief of investment research at Nationwide.

US stocks are headed for their best January since 2019 driven by expectations that the Federal Reserve will moderate its rate hikes. The equity rebound came just as the economy is headed for a downturn — setting the stage for a selloff, JPMorgan Chase & Co.’s Marko Kolanovic told CNBC. Investors should use any rallies to reduce exposure to the equity market, according to Richard Saperstein at Treasury Partners. Slower economic growth caused by the Fed’s tightening and its impact on corporate earnings will likely be priced into stocks over the next several months, he added. “We have not been impressed with the quality of earnings in recent weeks. Looking forward, margins remain at risk as inflation softens and economic growth slows,” Saperstein noted.

In other corporate news, AT&T Inc. rallied after beating analysts’ profit estimates even as the company’s 2023 outlook came up short of Wall Street targets. Boeing Co. reported a surprise loss to end 2022 — its sixth straight money-losing quarter — as higher costs slowed the planemaker’s recovery even though a late flurry of jet deliveries drove a surge in cash. After the close, Elon Musk’s electric-vehicle giant whipsawed as it beat estimates on profit and sales, but missed on cash flow. International Business Machines Corp. delivered an upbeat annual sales forecast while announcing it would eliminate about 1.5% of its global workforce, following similar job cuts by many of its tech peers.

The New York Stock Exchange also disclosed that a manual error caused wild price swings and trading halts for hundreds of company stocks when the market opened on Tuesday. The root cause of the issue, which the exchange operator says has been resolved, was tied to the company’s so-called “disaster recovery configuration” at the start of the day. Over 1,300 trades and some 84 stocks were impacted and marked as “aberrant,” NYSE said in an updated statement on its website.

Elsewhere, the loonie fell as the Bank of Canada raised rates for an eighth consecutive but potentially final time — saying it expects to move to the sidelines and weigh the impact of its rapid tightening.

Traders also kept an eye on the latest geopolitical developments. The US will send Ukraine 31 of its M1 Abrams battle tanks, adding to a German commitment to supply some of its top-line armor and infusing the country with a major new capability as it looks to pry Russian forces from the east.

With a similar index result, not a surprise we got a similar SPX sector flag as yesterday, although we did get one sector down over -1% today (utilities, on the back of a big drop in NEE after earnings (-8.7%) (there were no sectors down that much yesterday). Again though four red sectors. On the upside, again no sector was up more than eight tenths. Growth bounced back after taking a breather from its recent outperformance yesterday, but financials led.

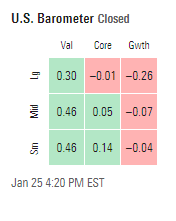

The Morningstarstyle box was even weaker than the last couple of sessions, although like the SPX sectors no style was down more than around six tenths of a percent. But really no style was notably up. Growth underperformed here as well.

Breadth was better today. As a reminder yesterday Nasdaq breadth outperformed, but NYSE was weak. Today 60% of volume was positive on the NYSE (after 40% yesterday), while the Nasdaq had 51% (after 52% yesterday). Issues were 51 and 50% (after 46 and 44%). So NYSE bounced back which is good to see, while Nasdaq was similar. Importantly, both were 50% or higher on all of the metrics despite the down days which means buyers have not given up.

Overseas, major equity indices in the Asia-Pacific region ended the midweek session on a mixed note while markets in China and Hong Kong remained closed for Lunar New Year. Japan's Nikkei: +0.4%, Hong Kong's Hang Seng: CLOSED, China's Shanghai Composite: CLOSED, India's Sensex: -1.3%, South Korea's Kospi: +1.4%, Australia's ASX All Ordinaries: -0.3%.

Australian inflation accelerated to the fastest pace in 32 years in the final three months of 2022, exceeding forecasts and prompting money markets to price in an interest-rate hike at next month’s central bank meeting. Bond yields and the currency gained as the consumer price index advanced 7.8% from a year earlier, exceeding economists’ 7.6% estimate, official data showed Wednesday. The result indicates inflation remains very strong even after 3 percentage points of rate increases between May and December. While the headline number came in slightly below the Reserve Bank’s forecast 8%, it shows Australia is lagging behind its developed-world counterparts where the inflation impulse has begun to ease. Core inflation, a measure preferred by the RBA, accelerated to 6.9% last quarter from a year earlier, exceeding economists’ forecast of 6.5%. That reading of the trimmed-mean measure was the strongest since the series began in 2003. The services component of the CPI recorded its largest annual rise since 2008, the ABS said. “Inflation has probably peaked but remains far too high,” said Su-Lin Ong, head of fixed-income strategy at Royal Bank of Canada. “The data likely seal the case for a 25-basis-point hike in February and the prudent approach would also be a final 25-bps in March to see terminal at 3.6%.” Australian stocks erased gains and fell as much as 0.5%, trailing peers in the region.

Japan cut its view on the overall economy for the first time in 11 months in January, as China's COVID-19 infections and a slowdown in global demand for tech and semiconductors hurt exports, especially to Asia. The government expects the economy, the world's third largest, will pick up going forward but Japan needs to pay full attention to the impact from China's spreading infections after it dropped stringent pandemic curbs, the report said. The authorities slashed its assessment on exports for the first time since November 2021, while it also cut its view on imports for the first time in three months. The January report said both exports and imports are "weakening recently" compared with its previous view of "almost flat" last month.

Bank Of Thailand Raises Key Rate By 25bps To 1.50%; Est. 1.50%

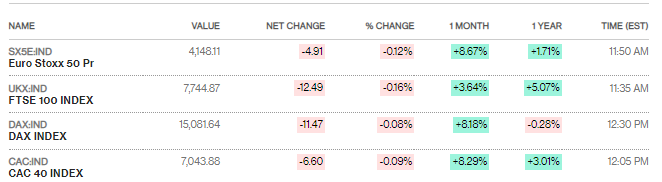

MajorEuropean indices finished mostly just under the flatline. Software firms such as SAP SE and Sage Group Plc fell in sympathy with Microsoft while Dutch chip-tool maker ASML Holding NV fell after posting a profit miss.

UK factories’ fuel and raw material costs are rising at their slowest pace in almost a year, further evidence that pipeline inflationary pressures are easing. Input prices rose 16.5% in December from a year ago, down from a peak of 24.6% in June, Office for National Statistics figures published Wednesday show. That was the slowest pace since February 2022. There were widespread falls in raw material costs, led by imported food, chemicals, parts and equipment, and oil. That suggests some of the supply chain bottlenecks that appeared after the pandemic have started to ease. The figures may fan speculation that the central bank is close to completing its fastest rate-hiking cycle since the 1980s. On a monthly basis, producer input prices fell for a second consecutive time in December, declining 1.1% as the cost of crude oil fell. Output prices, the cost of goods leaving factory gates, fell 0.8% in the month of December and were up 14.7% from a year earlier. That was the slowest annual pace since March. Another promising development was a slowing in the pace of input costs growth for services companies. Services producer price inflation fell from 6.2% to 5.2% between the third and fourth quarters and is now the lowest it has been since the first three months of 2022. There were though still signs of price pressures feeding through in food supply chains as shoppers face accelerating costs on their weekly shop. The cost of food products leaving factories picked up to 17.1% compared to a year earlier, the most since records started in 1997.

In other markets:

The dollar finished mildly lower but once again it was enough to set a new 7-month closing low, continuing to edge towards my target.

The VIX fell again back down to the 19 level.

WTI - WTI was little changed continuing to sit just below the 100-DMA. Daily technicals remain positive, so I continue to think it’s more likely than not it gets through but as I noted Monday there are layers of resistance above that.

On nat gas, as a reminder after breaking my “must hold” level last week I said “it will bounce somewhere, but where is the question.” Since then I have thought if it can just stabilize a few days we could see it move higher, and the first couple of days this week it did that (stabilize), but today it took another leg lower breaking below $3 for the first time since May 2021. At this point, I think the idea that this could turn into a “false breakdown” is now off the table. Unfortunately unless the weather turns much colder, there’s really no catalyst for a bounce until we get a restart date on the Freeport export facility.

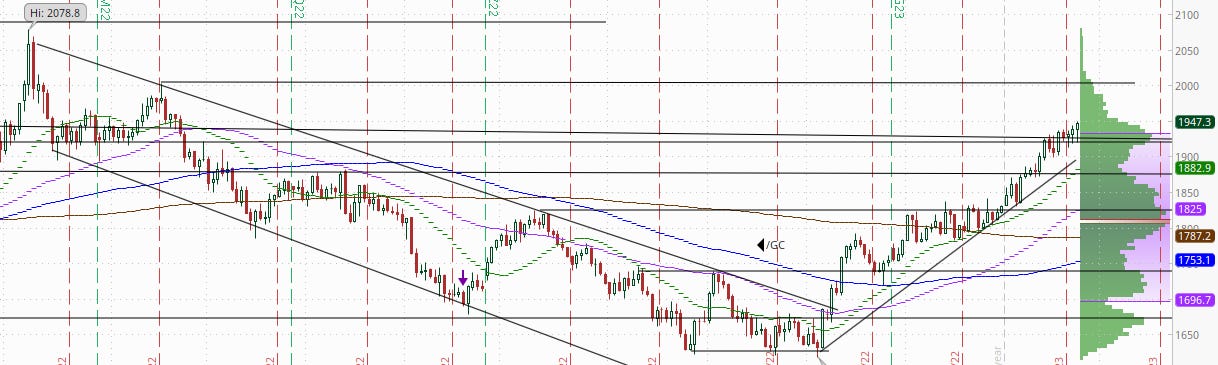

And on gold as a reminder I have been calling for a consolidation for a couple of weeks, but since we turned the calendar into 2023, it has not taken more than a couple of days off in between gains. I noted Monday it had been two days in a row of muted action, and the pattern repeated with gold moving to a new 7-month high yesterday and again today. It’s fairly overbought again, but that hasn’t mattered for a couple of weeks.

So as noted at the top, for a second day stocks recovered from early losses to finish little changed. I’m inclined to take that bullishly (failure to break down), particularly given we broke those noted key levels during the session, breadth outperformed modestly today, and the sideways action has helped to work off some of the overbought condition we started the week with. Tomorrow, though, we get some big data, particularly 4Q GDP. That definitely has the potential to move markets, as do earnings releases once again (particularly the card companies in terms of what they see in consumer spending). So we’ll see how those come out, and if we can make some better headway towards my target of 4100.

No reports today (EIA is coming)

Note: I’ve try to do a quick-take on Twitter on the bigger economic reports when they’re released if you don’t follow me there currently (link is at the bottom of this summary).

To see more content, including summaries of most major U.S. economic reports and my morning and nightly updates go to Neil’s Newsletter Substack for newer posts or https://sethiassociates.blogspot.com for the full history. You can also follow me on Twitter at @NeilKSethi