The Week Ahead - 2/1/26

A comprehensive look at the upcoming week for US economics, equities and fixed income

If you're a new reader or maybe one who doesn’t make it to the end feel free to take a second to subscribe now. It’s free!

Or please take a moment to invite others who might be interested to check it out.

Please note that I do often add to or tweak items after first publishing, so it’s always safest to read it from the website where it will have any updates.

As a reminder, some things I leave in from prior weeks for reference purposes, because it’s in-between updates, it provides background information, etc.. Anything not updated this week is in italics. As always apologize for typos, errors, etc., as there’s a lot here, and I don’t really have time to do a thorough double-check.

For new subscribers, this is a relatively long post. The intent is to cover the same areas each week. Sometimes the various areas are more interesting, sometimes less, but it’s easier just to go through them all, so you can expect this format (with things in the same places) each week.

The main sections are intended to cover 1) what’s upcoming next week, 2) what the Fed and rates markets are up to, 3) what’s going on with earnings (which along with valuations and positioning are the determinants to stock prices over the long term), 4) what’s going on with the economy (both because of its impact on our daily lives (I am a business investor in my “real” job) but also because it impacts earnings), 5) valuations, 6) breadth (which gets into sector/style performance), 7) positioning/flows (this is the most important determinant to asset price changes in the short term), 8) sentiment (really only matters at extremes but interesting to track), 9) seasonality (gives you an idea of what normally happens), 10) “Final Thoughts” (remember you get what you pay for there, and it’s the last thing I do, so it often is a bit rushed), and 11) my portfolio (to be transparent about where my money is in the market (but note first it is most definitely not intended as financial advice, and second as I mentioned earlier my main job (and investing assets) are in private industries (RE & venture capital)) so my portfolio is built with that in mind (i.e., it’s not how I pay the day-to-day bills) plus see note about MLP’s in that section).

Note: Per my earlier mentions, Monday I am starting the subscription model (which has been set at $9/month if you commit to a year). At year end, all proceeds from subscriptions will be donated to the top-10 charities chosen by subscribers (the only caveat is they have to be 4-star rated by Charity Navigator (which has no political leanings with both right and left-leaning organizations receiving 4-star ratings)).

Also, to update you on the poll results, it turns out that most of you actually like the Week Ahead all at once and all of what I’m putting out (flattered) ao I won’t be making any major changes but just working to improve on what I’m already doing.

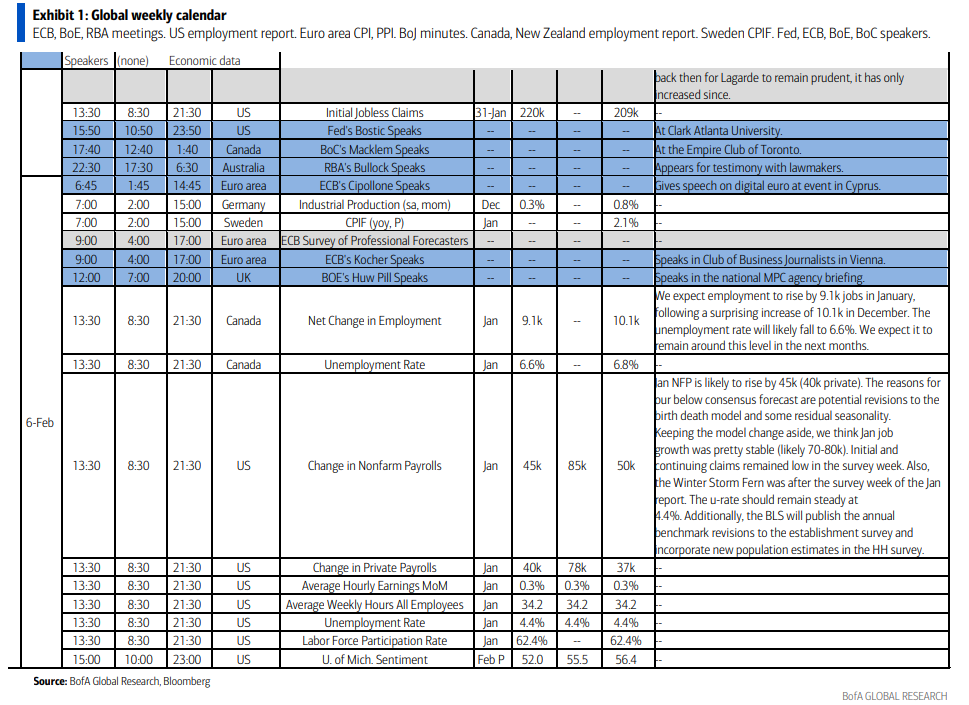

The Week Ahead

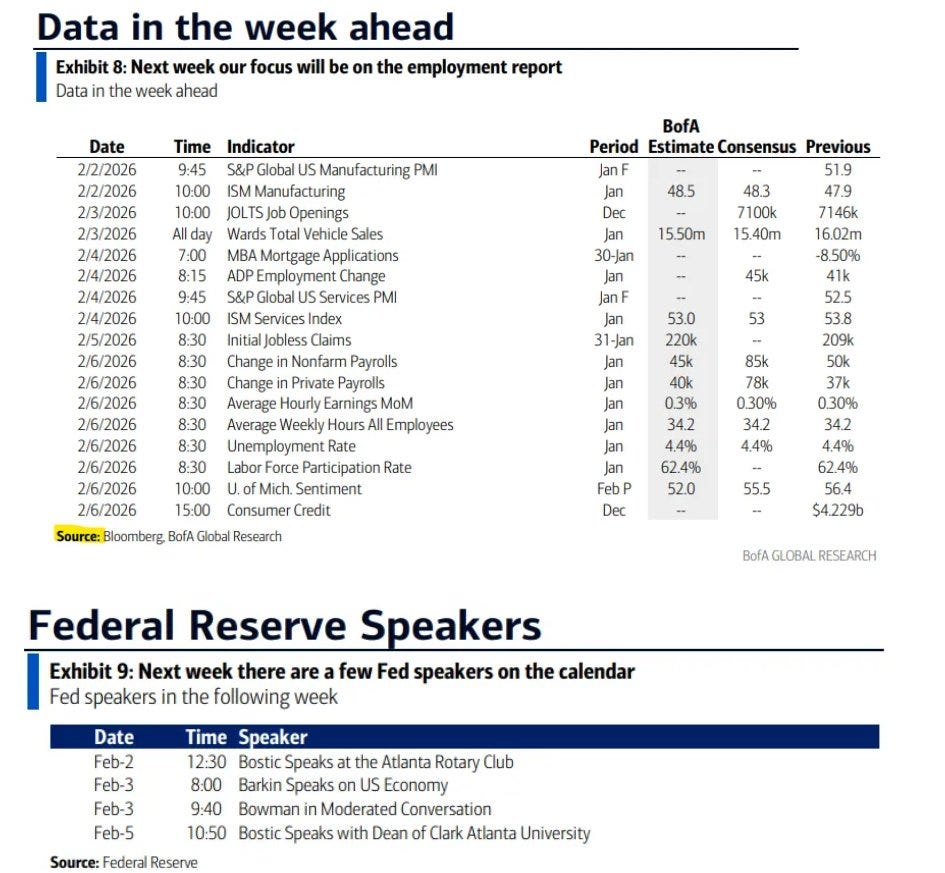

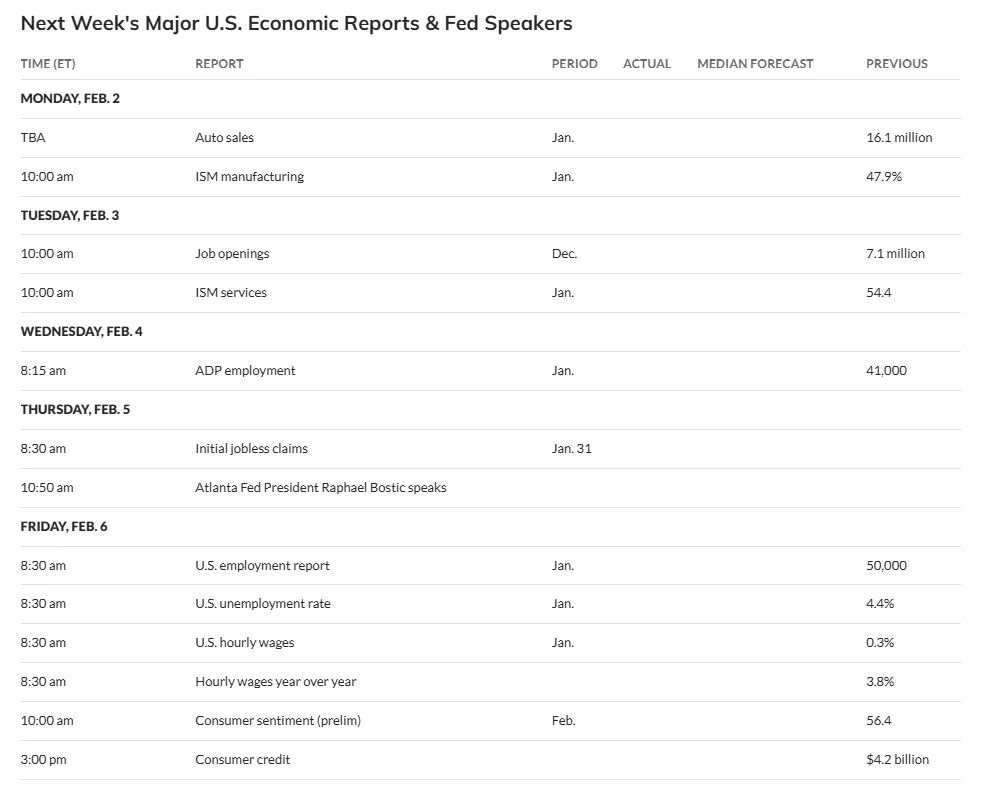

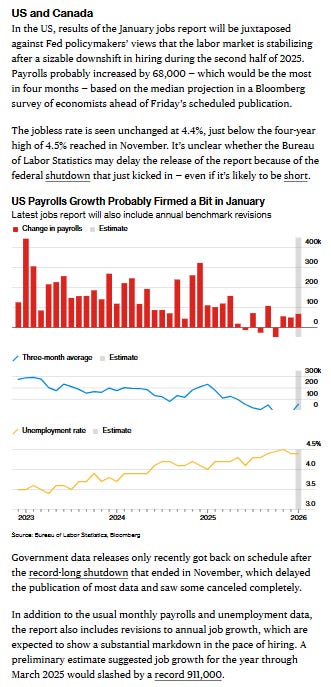

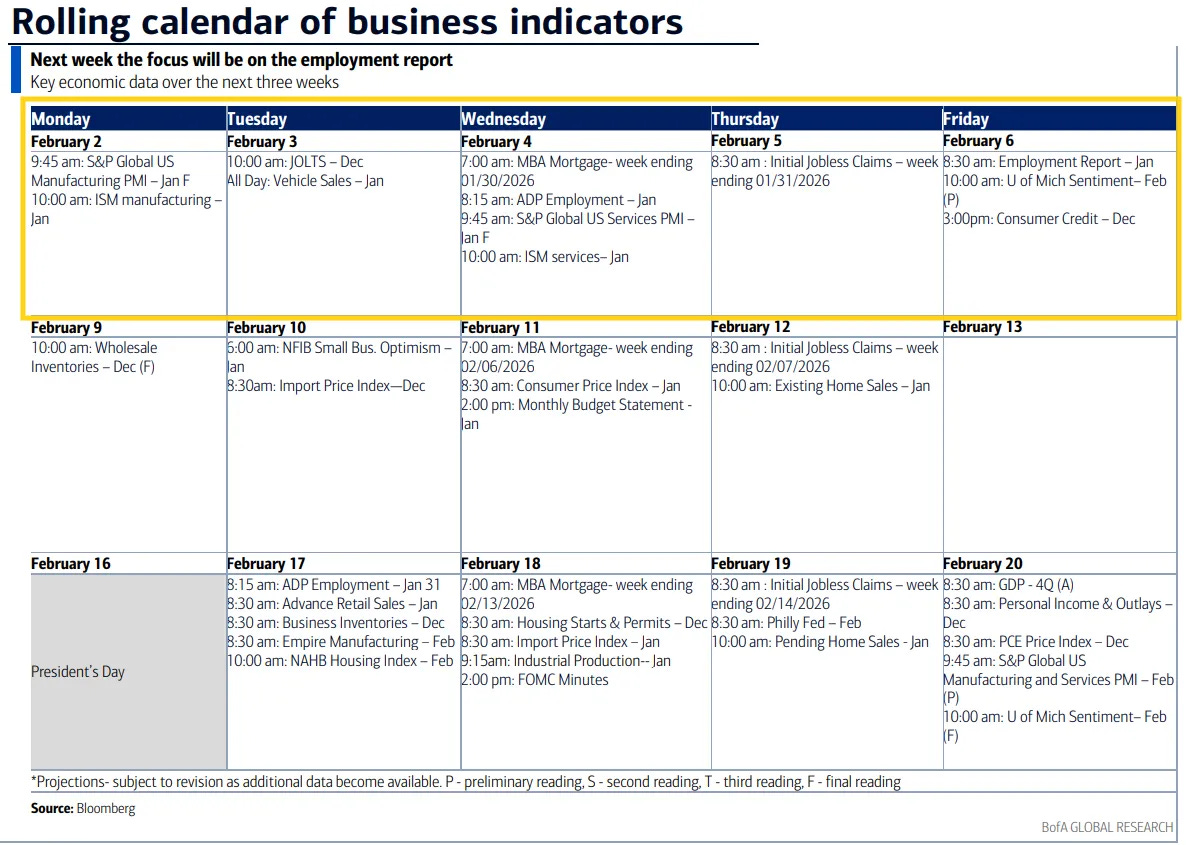

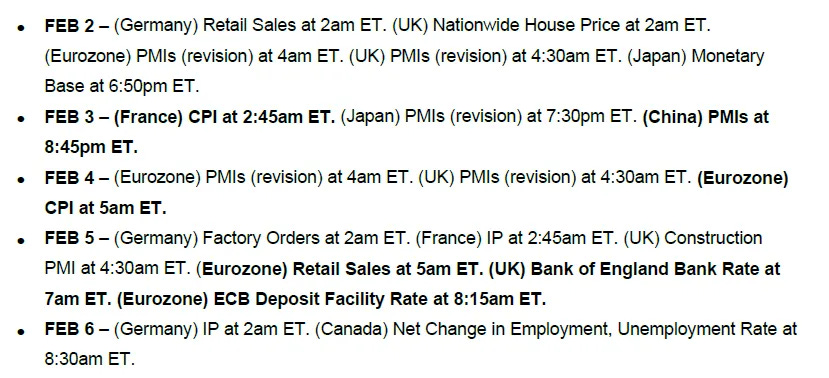

Next week is the first week of the month, and we’ll get most of our normal first week of the month US economic reports with a focus on the labor market leading up to “jobs Friday” (all assuming no shutdown). But as usual, before we make it to Friday, we’ll receive Jan ADP and Challenger job layoff/hiring announcements, Dec JOLTS, and weekly jobless claims. And, as usual, we’ll have the Jan ISM and final S&P PMIs, auto sales, and as we sometimes do, Dec consumer credit and the preliminary Feb UMich consumer survey. There’s also the Senior Loan Officer’s Survey (Mon) and the weekly mortgage applications and EIA petroleum/natgas inventories.

Note though the January jobs report is a little different in that it contains the “second half” of the QCEW revisions (which adjusts estimated employer payrolls to the actual best estimate we have - state unemployment insurance fund contributions). We got the first half (through March 2025) of that last year. This will revise the rest of 2025 (Apr-Dec). Last year that resulted in a more than 900k revision downward to 2025 job growth. While that large of an adjustment is not expected, if it’s anything close it will garner plenty of headlines (Jerome Powell for what it’s worth insinuated at one point he’s expecting something like -700k (-60k a month)).

Fed monetary policy speaking blackout is over, and it will be back to the circuit for Fed members, although formally there’s just a few speaking next week, and one is outgoing Atlanta Fed Pres Bostic (twice). Another is Richmond Fed Pres Barkin who speaks quite a bit (and is not a voter), and the last is Gov Bowman who we heard from on Friday. I’m quite sure there will be more.

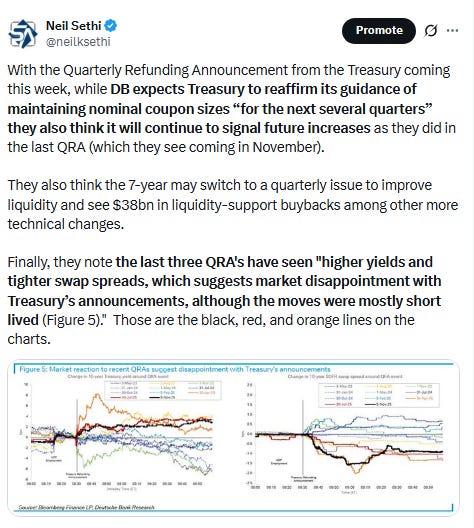

No non-Bill Treasury auctions (>1yr in duration) until they pick back up the following week, but we will get the Treasury refunding announcement. While no changes are expected to auction sizes at the upcoming quarter, there are expectations that they will need to change (increase) as we get into the second half of the year, which would mean the key language about stable auction sizes for upcoming quarters will need to change at some point. Such a change in language will likely see some disruption in markets.

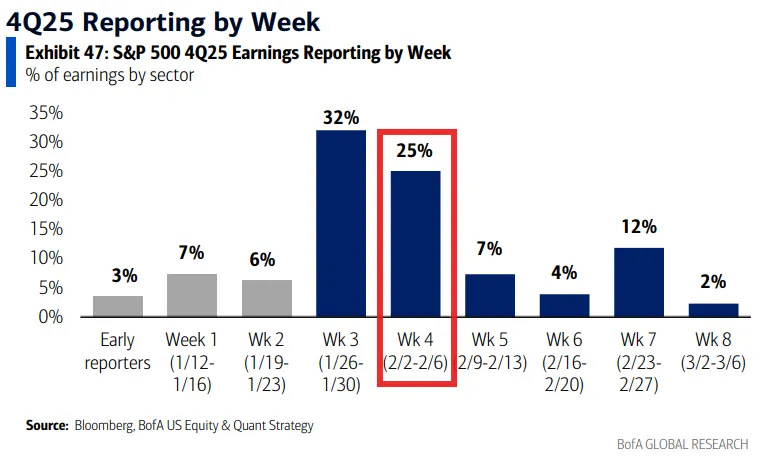

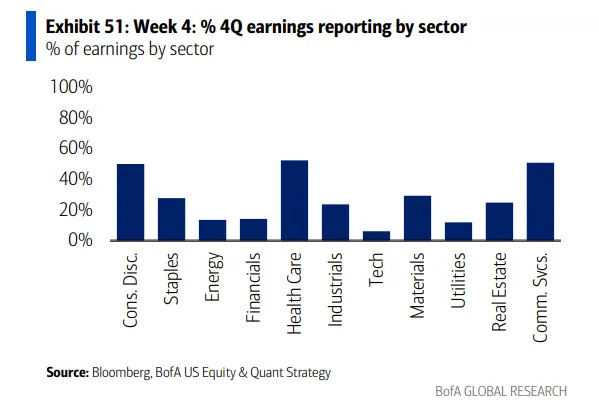

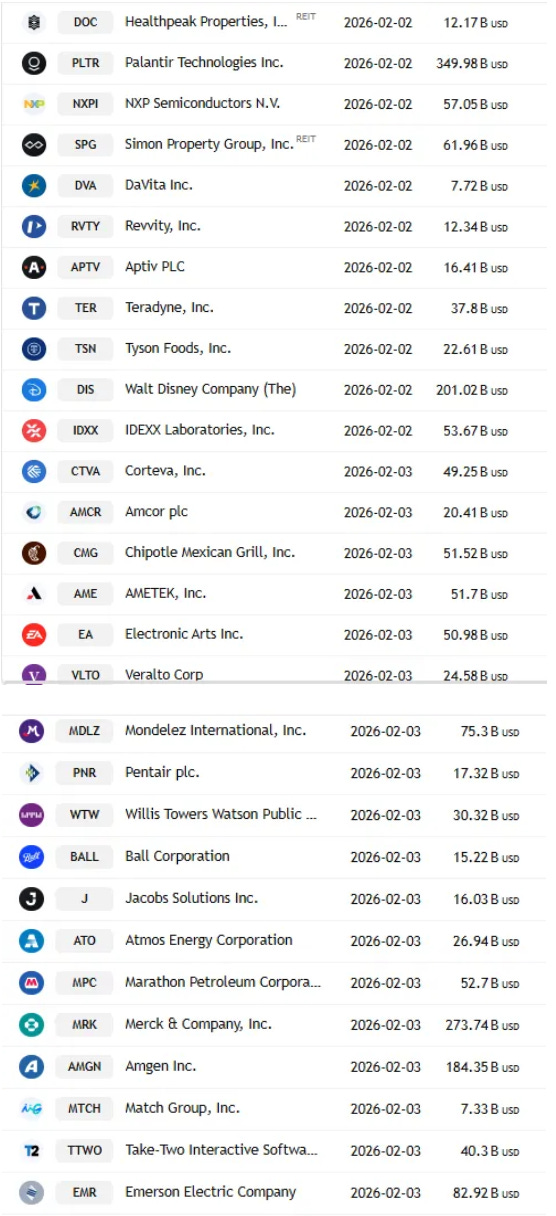

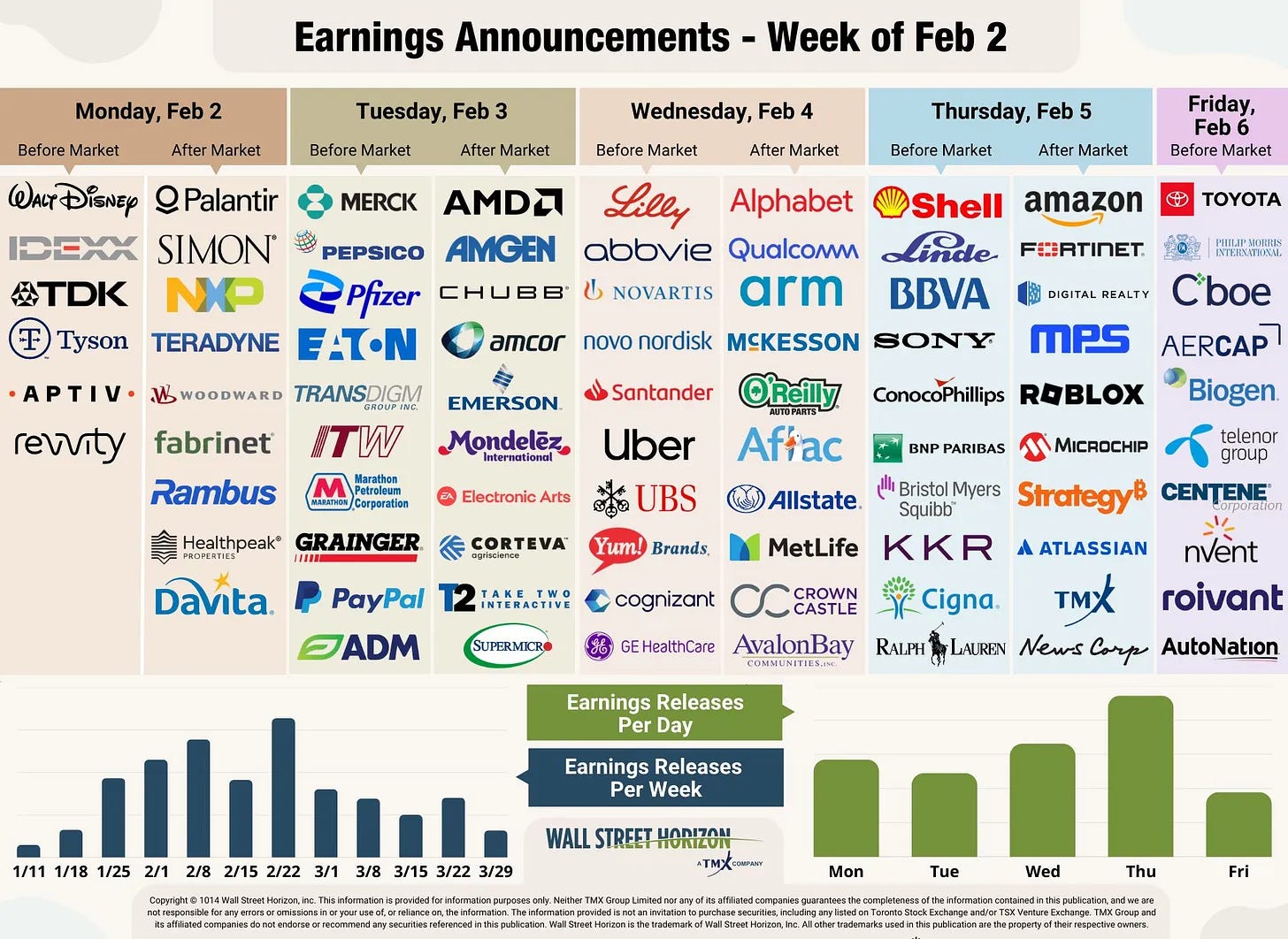

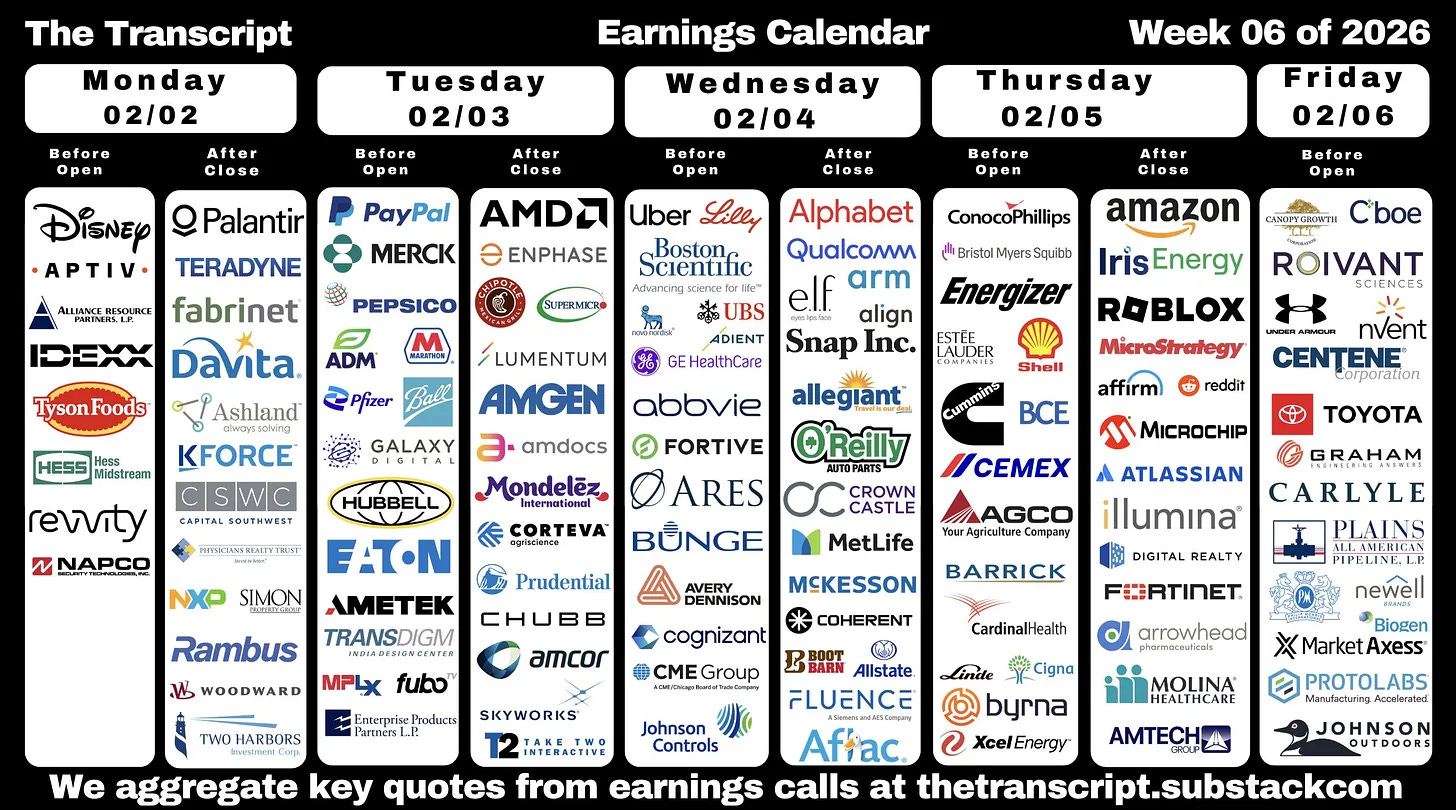

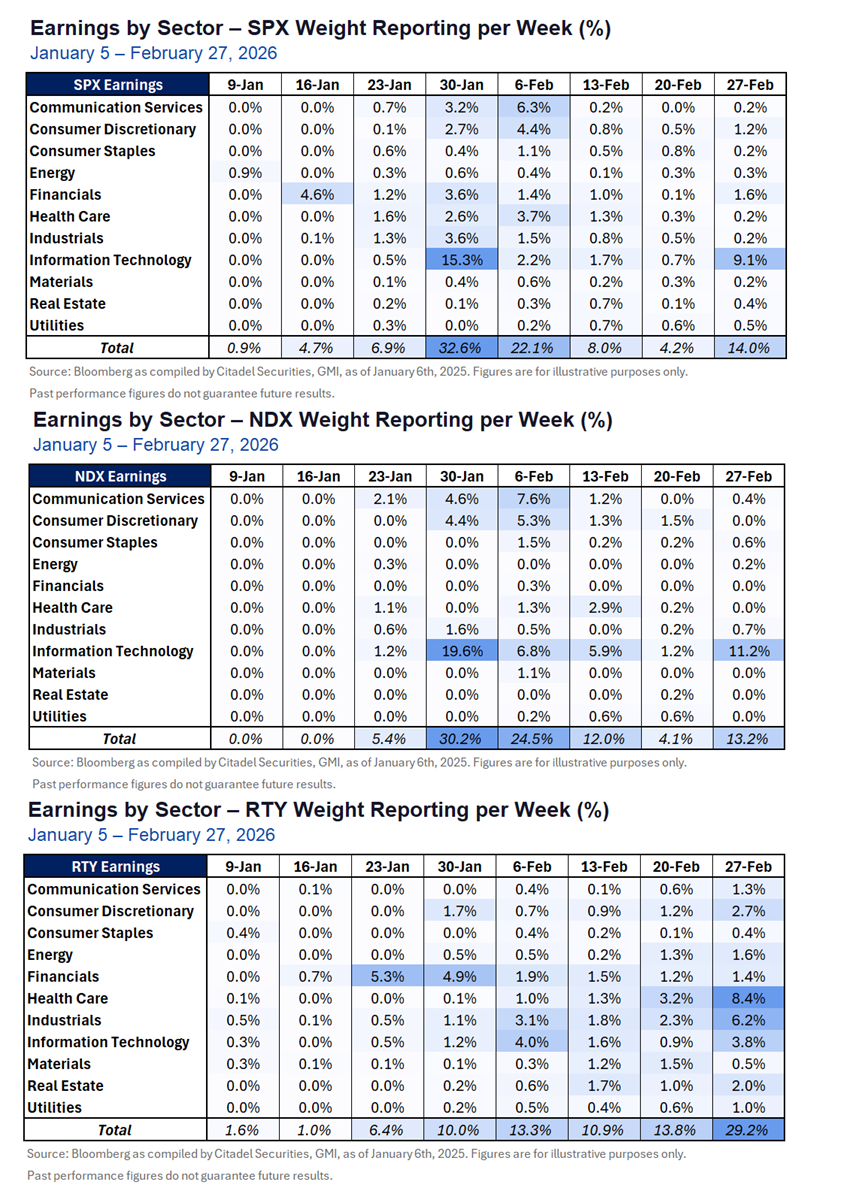

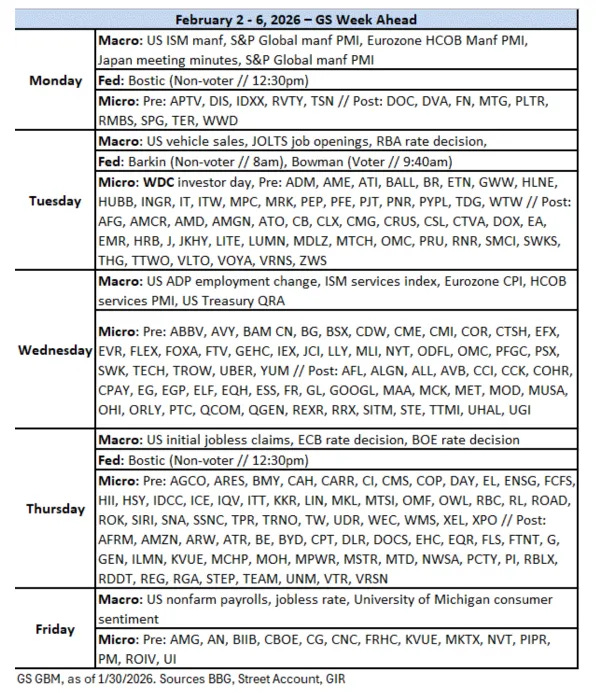

While we’re past the peak of SPX earnings, it’s still a huge week with 25% of the SPX by earnings weight reporting consisting of around 155 SPX components, with two more Mag-7s in GOOG & AMZN and another ~20 >$100bn in market cap in DIS, PLTR, AMGN, AMD, MRK, CB, PEP, ETN, PFE, BSX, CME, MCK, QCOM, ABBV, UBER, BMY, LIN, COP, KKR, PM (by reporting date). Full list below from TradingView.

And of course we still for now have a partial government shutdown. All indications are that the House will pass the Senate bill, but there’s something about counting chickens before they hatch that comes to mind.

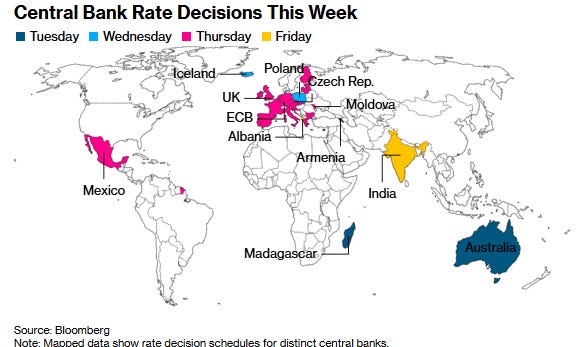

Ex-US highlights include a number of global rate decisions from the BoE, ECB, RBA, RBI, and Banxico (England, EU, Australia, India, and Mexico) among many others as well as BoJ (Japan) and BCB (Brazil) minutes, global PMIs, EU CPI (along with individual countries) and retail sales, Germany retail sales, factory orders, and IP, Canada employment, and Japan household spending in addition to many other global data releases.

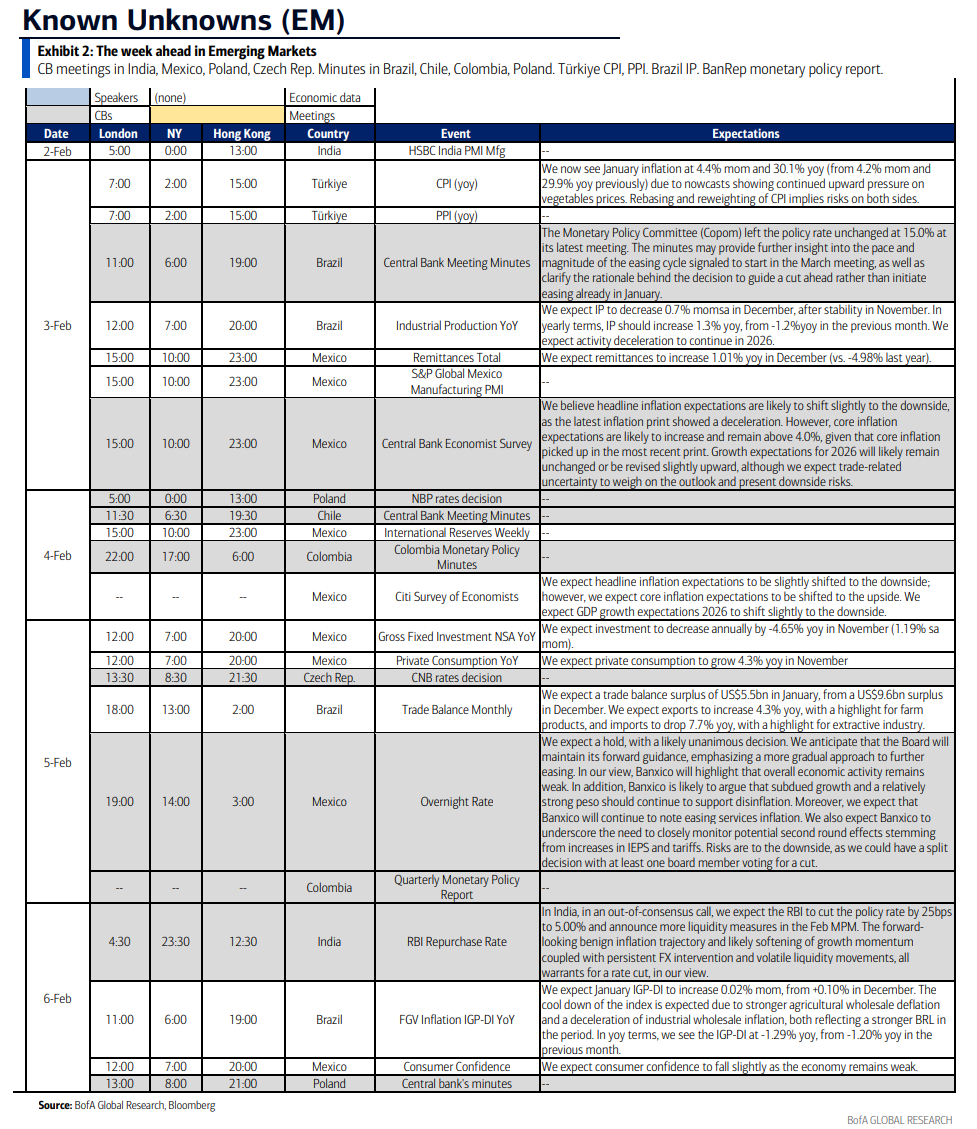

Canada

Canada’s January jobs report is likely to underscore ongoing labor-market weakness, despite stronger-than-expected hiring in late 2025. Unemployment has climbed back to 6.8%, and the Bank of Canada says youth joblessness remains elevated while firms’ hiring intentions are soft. Governor Tiff Macklem — fresh off declaring that rules-based trade with the US is “over” — will outline the forces reshaping Canada’s economy during a speech in Toronto on Thursday.

Asia

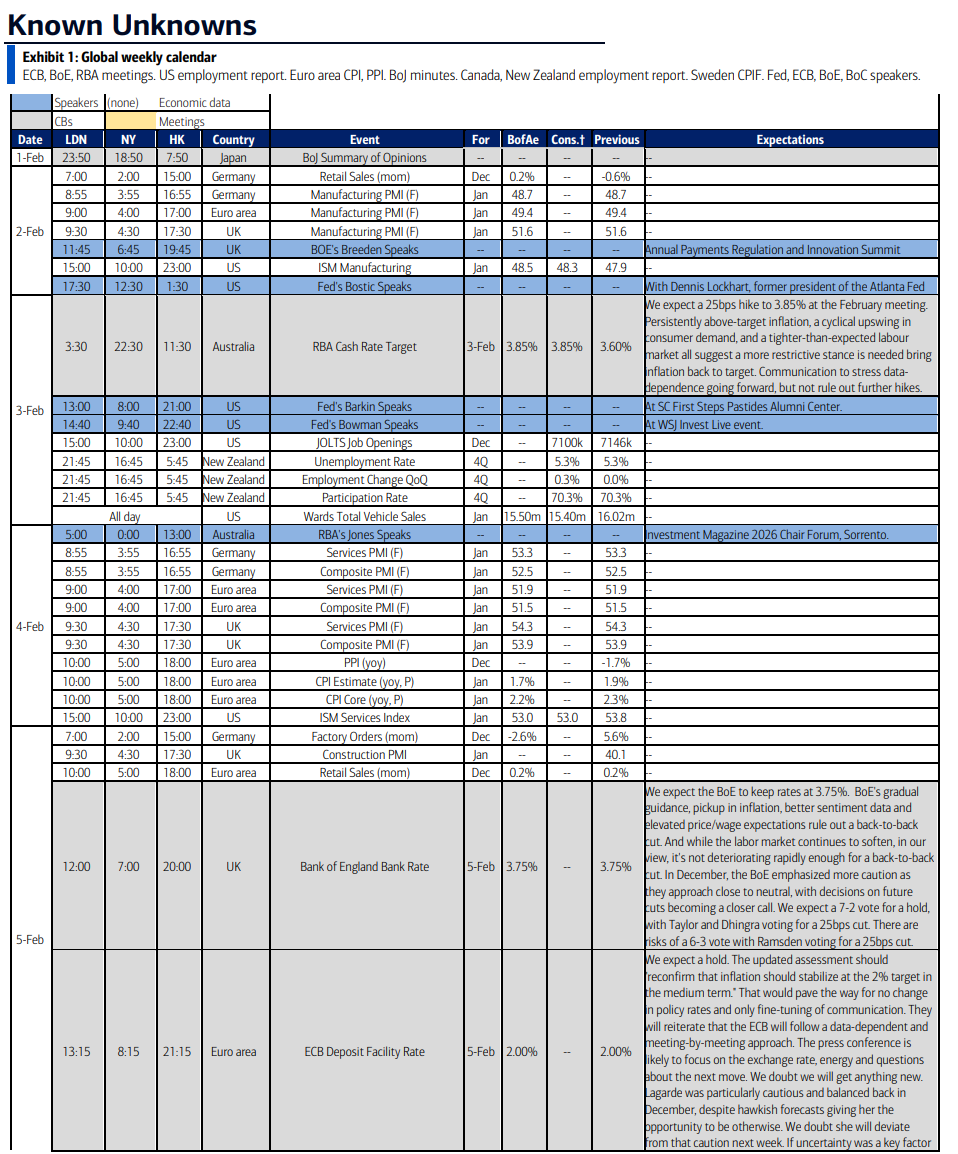

The week kicked off with India’s budget presentation, with Finance Minister Nirmala Sitharaman on Sunday outlining several new programs to boost manufacturing and infrastructure to support an economy grappling with global risks and steep US tariffs. In central banking, Asia may see a pair of institutions adjusting policy in opposite directions. Traders have increased bets that the Reserve Bank of Australia will raise its cash rate target to 3.85% on Tuesday after a key inflation gauge registered 3.4% year-on-year growth in the fourth quarter, above the RBA’s 2-3% range. There’s at least a chance India’s Reserve Bank will trim its repurchase rate on Friday after consumer price gains stayed below the midpoint of the RBI’s inflation target for an 11th straight month in December — although not all agree. A strong autumn harvest suggests food prices will stay deflationary for some time, according to Bloomberg Economics. The Bank of Japan’s summary of opinions from its January meeting, due on Monday, may shed light on how soon Japan will see its next rate increase.

On the data front, the week gets underway with a Monday round of January manufacturing PMI reports. China’s gauge is expected to hold steady at 50, the dividing line between contraction and expansion. Also publishing PMI figures that day are Indonesia, South Korea, Malaysia, the Philippines, Thailand, Taiwan and Vietnam. China’s services and composite PMI indexes follow on Wednesday. The same day, New Zealand releases fourth-quarter labor statistics, with a focus on the jobless rate after it rose to 5.3%, the highest in nine years, in the previous quarter. Consumer inflation updates are due during the week from Thailand, Taiwan, Vietnam and South Korea.

In Japan, household spending data on Friday will provide a glimpse into the willingness of the nation’s consumers to spend before voters deliver a verdict on Prime Minister Sanae Takaichi on Sunday. One focus will be food, as recent data have shown the proportion of food spending within overall consumption at a record high. A weak yen has compounded the pressure by driving up costs of groceries, energy and other imports. While Japan managed to secure breathing space for its currency without intervening in markets last month, any comments by policymakers are in focus. That pushed Prime Minister Sanae Takaichi clarify earlier comments on Sunday. Trade numbers are also due from Indonesia, Pakistan and Australia. Data for South Korea published Sunday showed exports extended their growth streak in January, underpinned by robust semiconductor demand and an increase in the number of working days from a year earlier because of the effects of a favorable calendar.

Europe, Middle East, Africa

The Bank of England is likely to leave rates on hold at 3.75% on Thursday, as UK officials debate how much further to go in their cutting cycle. The rate-setters are weighing a faster-than-expected cooling in inflation against surveys pointing to stubbornly high wage growth and a strengthening economy. It will unveil new forecasts that are expected to show inflation falling close to the BOE’s 2% target over the spring, following measures in the Labour government’s recent budget to ease cost-of-living pressures. The same day, policymakers in Prague are likely to hold rates at 3.5% as they await evidence that inflationary pressures are easing.

A day earlier, Polish officials could resume cuts, while Iceland’s central bank is seen holding off on further reductions until the second quarter. Rate decisions are also scheduled in Albania, Armenia, Madagascar and Moldova. Beyond monetary policy, Saudi data on Sunday showed that the economy expanded at the fastest pace in three years in 2025, with the oil sector emerging as a stronger engine of growth under new OPEC+ supply policy. Turkish numbers on Tuesday are expected to reveal annual inflation easing to about 30% in January from 30.9% a month earlier. The central bank recently slowed the pace of rate cuts amid concerns about a surge in food prices. Germany’s factory order, industrial production and trade data on Thursday and Friday will be scoured for signs of recovery in the region’s largest economy.

Friday also sees the publication of Swedish inflation, with data predicted to show a slight downtick. Even so, after holding rates on Thursday, Bloomberg Economics expects Riksbank policymakers to stick with that stance, as much of the slowdown reflects temporary tax effects and medium-term risks remain tilted to the upside. That day also sees Russia’s gross domestic product data for 2025. The Economy Ministry’s September forecast predicted 1% growth, a sharp slowdown from 2024, when heavy state spending on the war effort drove an expansion of 4.3%.

Latin America

Banco Central do Brasil’s January meeting minutes get the week rolling. Keeping the Selic unchanged yet again didn’t surprise, but the overtly explicit guidance — to expect a cut in March — was a bit of an eye-opener. At the same time, Brazil watchers hoping for more on BCB’s potential rate path may be disappointed. Industrial production and monthly trade data are also due out from Brazil. In Chile, December GDP-proxy results should show the economy bouncing back from November’s weak results on the back of rising copper prices, while the peso’s gains help curb inflationary pressures.

As if on cue, Chile’s January consumer prices report may see inflation actually drop below the 3% target while the minutes of the central bank’s dovish rate hold in December may help pin down the timing of the next cut. In LatAm’s No. 2 economy, Mexico’s central bank has done a fairly thorough job of telegraphing clear intent to pause a 12-meeting, 400 basis-point easing cycle at Thursday’s rate decision. Slack in the economy is a concern, though potentially volatile US trade policies and an upcoming review of Mexico’s free trade accord with the US and Canada argue for some caution.

The central theme of three separate reports from Colombia will be inflation — which looks to be a major headache for policymakers now and for the foreseeable future. Colombia’s BanRep posts minutes on Wednesday of its shock move to deliver a full-point rate hike, to 10.25%, as a double-digit minimum wage increase is set to heat up the economy. It will also issue its quarterly monetary policy report. The nation’s January consumer prices report on Friday should underscore those concerns: the early consensus sees monthly headline and core prints of better than 1%, with the annual headline rate pushing up over 5.4% from 5.1%.

.

GS one-pager:

DB one pager:

BoA’s cheat sheets:

Market Drivers

So let’s go through the list of items that I think are most important to the direction of equity markets:

Fed/Bonds

As noted previously this was one of the sections that had grown unwieldy, so I’ve really pared it down (I know, it’s still really long). Given I provide daily updates on Fed expectations, Fedspeak, and analyst thoughts on the Fed, it’s duplicative (and time consuming) to regather it all, so, again, I encourage you to look at those (the daily posts) for updates. I will just give more of a quick summary.

I’ve taken out the background information from how we got to where we were from the start of the year through the end of March, but if you’re interested you can find that in this section from the March 23rd update. And I had left in the background from March to August fora while as I had said it was “still relevant in terms of ‘how we got here,’ and it reflected the continued slow evolution of the Fed away from worries about tariff impacts on inflation towards the need for rate cuts (remembering that absent those tariff worries the Fed would already be cutting at this point),” and we got that with Powell’s pivot at Jackson Hole, so if you’d like that background, you can find it at the August 17th update. I then took out the “next phase” in the Fed’s evolution (from Jackson Hole leading up to the October meeting). You can find that material at the October 19th update.

And now I think it’s officially time to take our next step as we now clearly have a Fed which for the most part feels that it has taken out sufficient “insurance” against labor market declines, and, as Powell said at the press conference, feels that while there are still risks to both sides of the mandate (inflation and employment) they both “have diminished” but “there is still some tension” which leads the bulk of the committee to feel that “policy is in a good place,” and “well positioned to let the data speak.” That message was repeated in one form or another several times by Powell, and is consistent with the messaging from most of the Fed outside of the three doves (Gov’s Miran, Waller, and Bowman (the Trump appointees other than Powell)).

If you want the background on “how we got here” since October you can find that in the Jan 25th update.

Given all of the “forward guidance” from the Fed speakers ahead of time, this messaging from Powell was pretty much expected, and rate cut bets didn’t change much, still expecting just one more cut (in June) with the a better than 50/50 chance of another cut before the end of the year following the meeting.

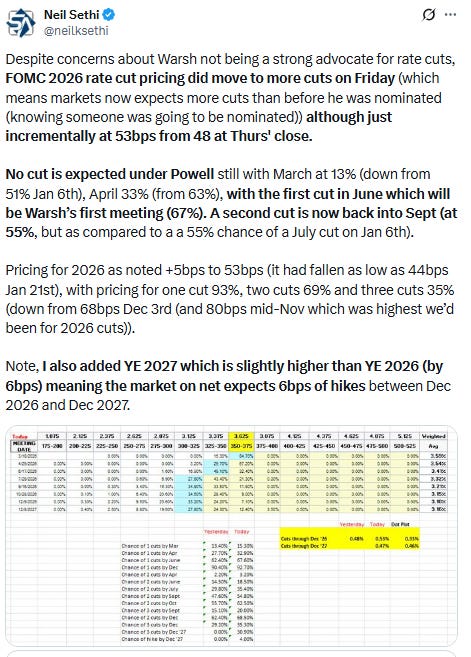

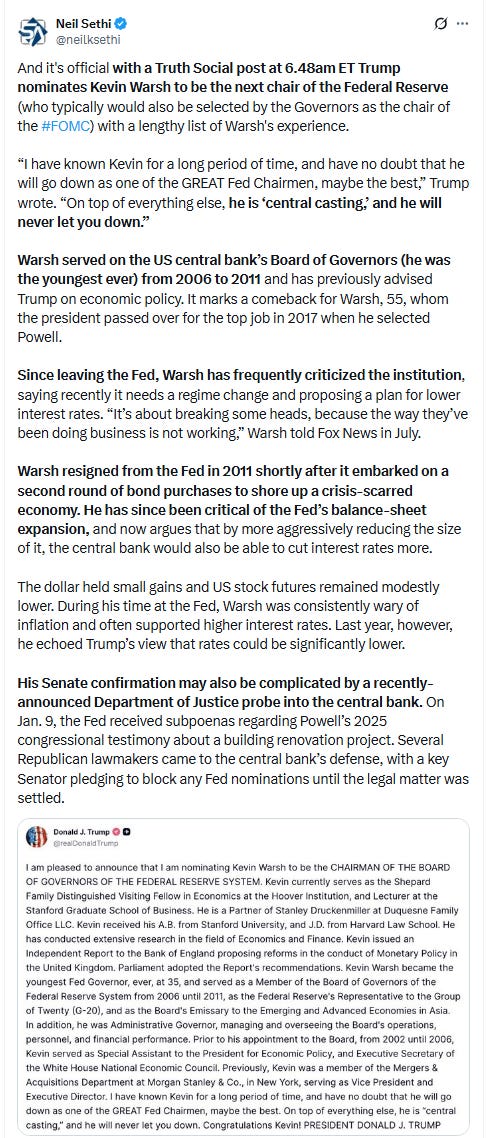

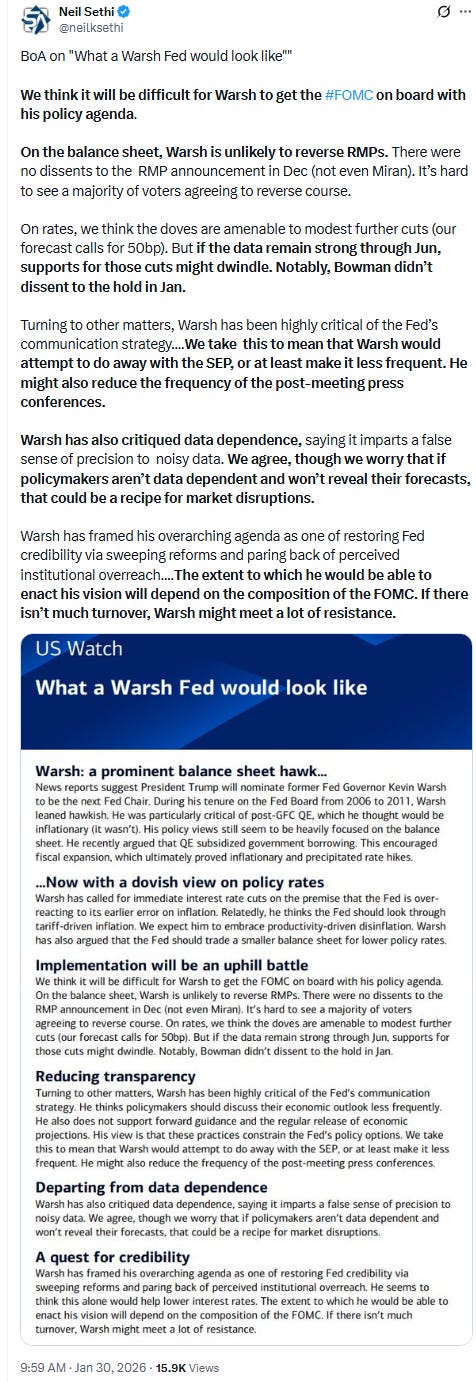

But all of that is now set to change to some extent with the introduction of a new character to the script in Fed Chair nominee Warsh. I’ll have more to say about Warsh as we get closer to him actually becoming a Governor (which doesn’t look to to be anytime soon given the standoff between Trump and key Senator Tom Tillis. With Trump not wanting to drop the criminal investigation into the Fed, and Tillis adamant he won’t advance Warsh’s nomination absent the investigation being “cleared up”, unless a Democratic Senator in the Banking Committee is willing to cross the aisle, this will drag on until one one gives in.

I did put in my posts about Warsh during the week which gives you some background, but given his time at the Fed was nearly two decades ago, there are some questions as to how useful that will be as a roadmap. But what we do know is that as recently as a couple of months ago Warsh was saying what was need was to “break some heads” and “regime change” at the Fed. Some of his proposals include:

Less “data dependence” which he calls backward‑looking and overly focused on high‑frequency releases, calling that “false precision and analytic complacency. Instead he wants policy more firmly anchored in simple rules and clearer frameworks. This is something that I think might find some support.

He has been a consistent critic of the Fed’s “bloated balance sheet” and thinks it can be reduced significantly which would allow it to lower rates. This is something that I think will run into resistance as the last time the Fed tried to shrink its balance sheet beyond where the market was comfortable (which is basically where we are now), it caused severe disruption in short-term funding markets which spilled over into equities.

Warsh has also called for a new “Treasury–Fed accord”, where the Treasury and Fed will work in concert on the size and composition of the balance sheet (and perhaps is one reason Treas Sec Bessent likes Warsh). While theoretically this makes a lot of sense, it is a little dangerous in opening the door to the Fed becoming enmeshed in the realm of fiscal policy (i.e. Executive Branch policy) which brings it into the realm of politics.

But between now and when Warsh is confirmed (which is highly likely once this roadblock with Tillis is cleared) unless Trump changes his mind, we’ll need to see either inflation or the labor market move significantly lower before we can expect any further rate cuts. For now, hikes are not even being considered. “They are nobody’s base case,” Powell said meaning even the most hawkish don’t expect rates to move higher over the next year at least.

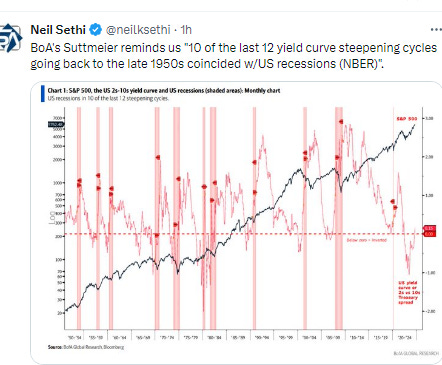

The 2/10 Treasury edged back up to just under the +0.72% three weeks ago, which was the highest since Jan ‘22.

As a reminder, historically when the 2/10 curve uninverts following a long period of inversion the economy is either in a recession or within a few months of one. It uninverted in Sept 2024, so I had said this looks officially like a “this time is different” situation as we’re now over a year. Anything that has a lead time that long is not really useful.

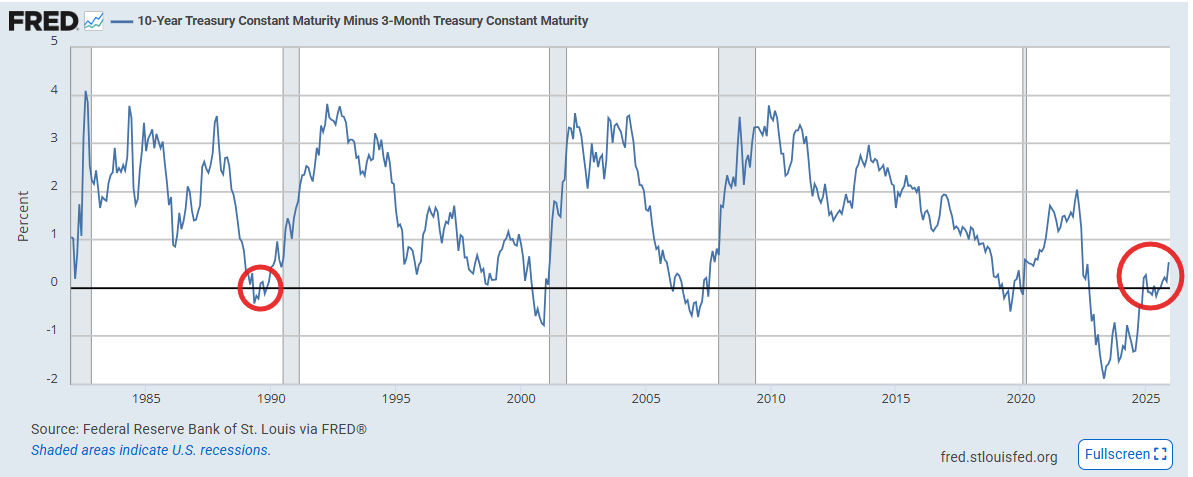

The 3mos/10yr yield moved to +0.66%, not far from the +0.72% Jan 20th which was the highest since Oct ‘22 still though calling for more rate cuts or a move higher in 10yr yields (this is historically around +1.25%).

Note this curve is considered a better recession signal than 2/10’s w/the last four recessions on average coming a few months after the curve uninverted (prior to that it generally uninverted after a recession had already started)). This though is starting to run past its due date as well.

It had spent nearly a year within a quarter point of 0%. The only other comparable period (inversion followed by a long stretch around 0%) was 1989 when it spent the year within a slightly larger band (but after a much smaller inversion). When it finally lifted after that instance a recession followed six months later. This is NOT to say I think we’ll see recession in 6 months (quite the opposite).

Also, as noted back in February, reinverting is something that it did prior to (or just after) the last two recessions and it also dipped (but didn’t reinvert) in the two recessions prior to that, although this one was much more mild than previous. Regardless, the longest it went in those previous four instances before recession after reinverting is 6 months (2007).

Also note that in 1989 and 2007 we saw similar periods of a recovery from inversion that stalled at the zero line for long periods of time which turned into recessions after they finally started to steepen again (but in 1989 it took six months (we’re beyond that now)), but see the note above about the length it spent around the zero line.

Similarly the 10yr Treasury yield remains the furthest above the Fed Funds midpoint (and the EFFR) since Oct ‘22, at +60bps (+1bps this week) still though well under the typical non-recessionaly spread of around 1-1.25%, so calling for another ~50bps of rate cuts (or perhaps if one thinks the 10yr is mispriced, a higher 10yr yield (or some combination)).

The 2yr yield though remains below the Fed Funds midpoint (and EFFR) by -12bps (-8bps w/w). It is also under the typical non-recession spread of ~+50bps so also calling for more rate cuts (or a higher 2-year yield).

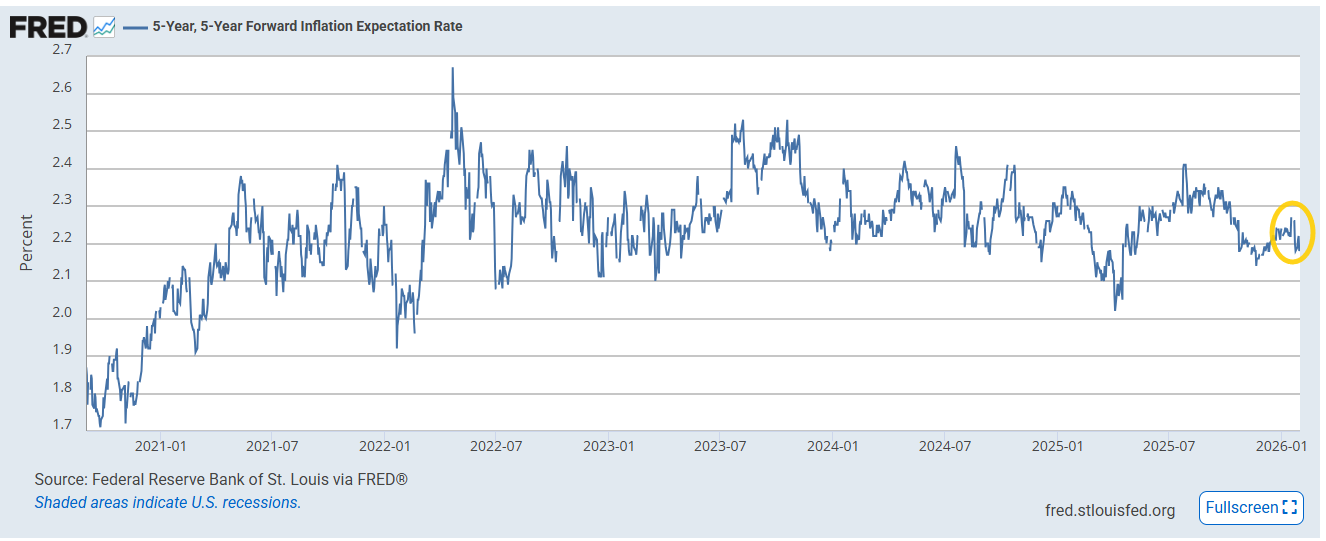

Long term inflation expectations as measured by the 5-yr, 5-yr forward rate (expected inflation starting in 5 yrs over the following 5 yrs) which had pushed up to 3-month highs at 2.27% two weeks were little changed at 2.19%. These remain in the middle of the range since 2022. They’re a touch below their 20-yr average (2.25%).

The peak in 2025 was 2.41% July 28th which was the joint highest (with October) in a year) and 2.67% was the post-pandemic peak in Apr ‘22. The 2025 low was around Liberation Day at 2.02%

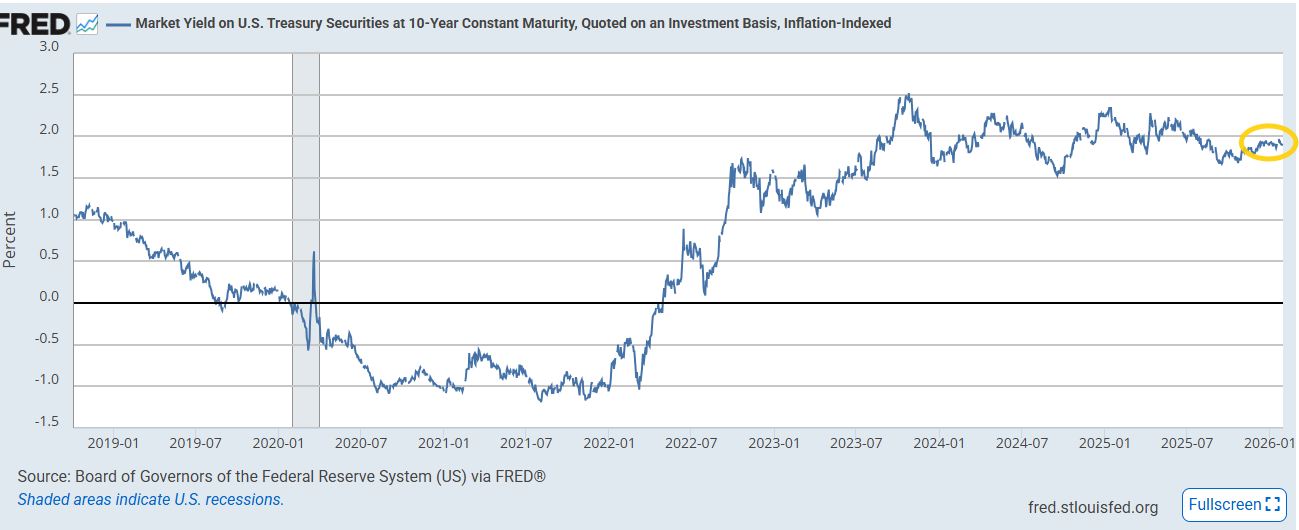

Interestingly though the 10-yr breakeven inflation rate moved to the highest since Sept at 2.36%, but remaining in its post-2022 range.

10yr rate real rates though fell back to 1.89% from 1.95% as of Thursday. They overall remain in their range since Aug 2023.

They are well below the 2.34% in mid-Jan (which was the highest since Oct ‘23 (and before that 2007)), but also still well above the 2012-2020 peak of 1.12%.

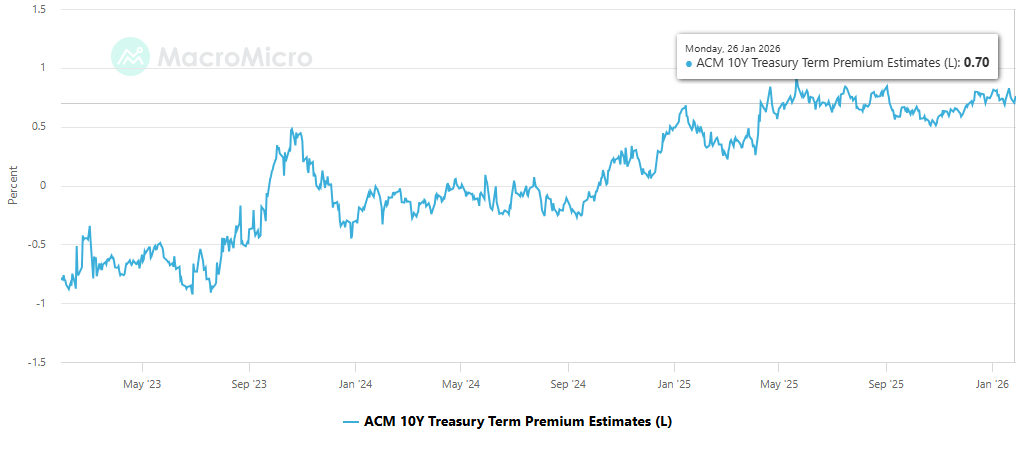

The ACM model of the 10yr Treasury term premium (which is solely based on interest rates so has no “external anchor” to help explain why short-term rates may be moving (such as Fed policy expectations)), fell back as of Wed for a second week to +0.70%, in the middle of the range since April.

The high of 2025 was +0.91% on May 21st (which was the highest since July 2014).

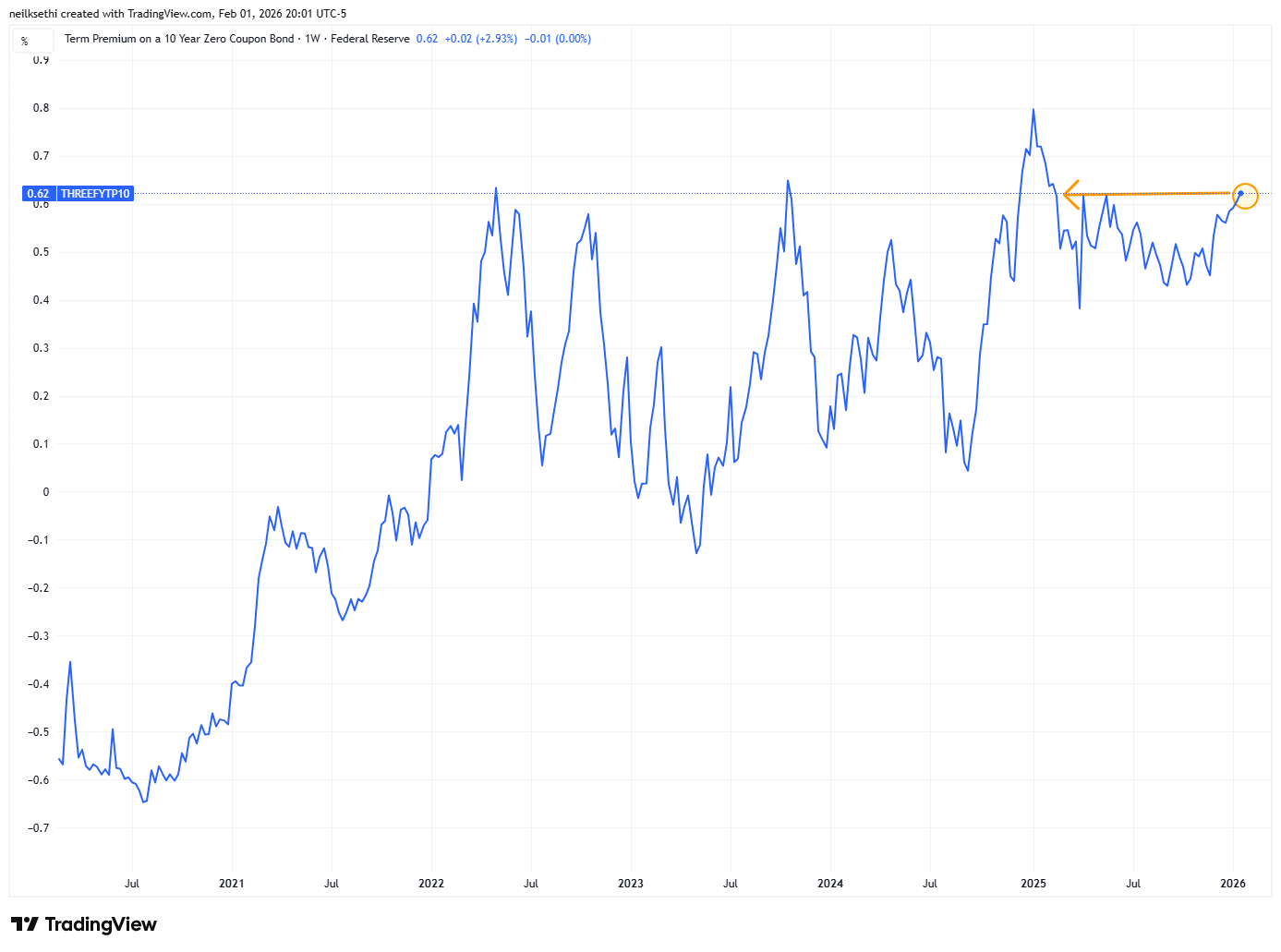

As mentioned above, the ACM model has a weakness in that it looks only at rates with no “anchor” to the external environment. The Kim-Wright model addresses that by adding in an expectations layer (from Blue Chip forecasters) of the expected path of short-term rates. That is just updated through Jan 19th, but that rose to the joint highest since Feb at +0.62%.

Unlike the ACM model, the post-pandemic peak was in Jan at 0.80%. The overall message is similar though in that pre-pandemic you have to go back to 2013 to find comparable levels.

The extended discussion on term premium (what it is, why it’s important, etc.), can be found in this section in the Feb 4th Week Ahead.

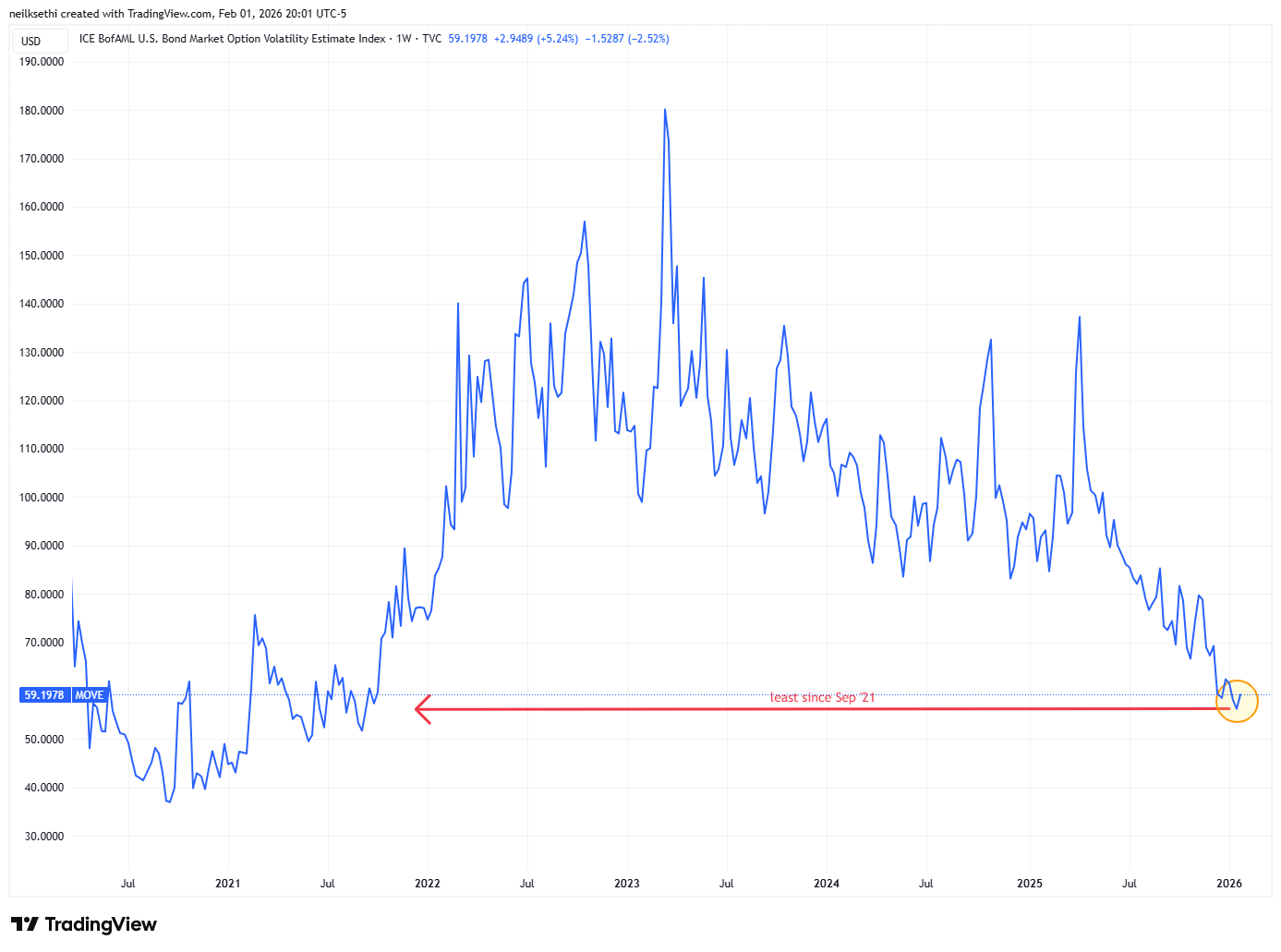

The MOVE index of expected 30-day Treasury note/bond volatility edged up to 59.2 after Tues hitting the least since Sept ‘21.

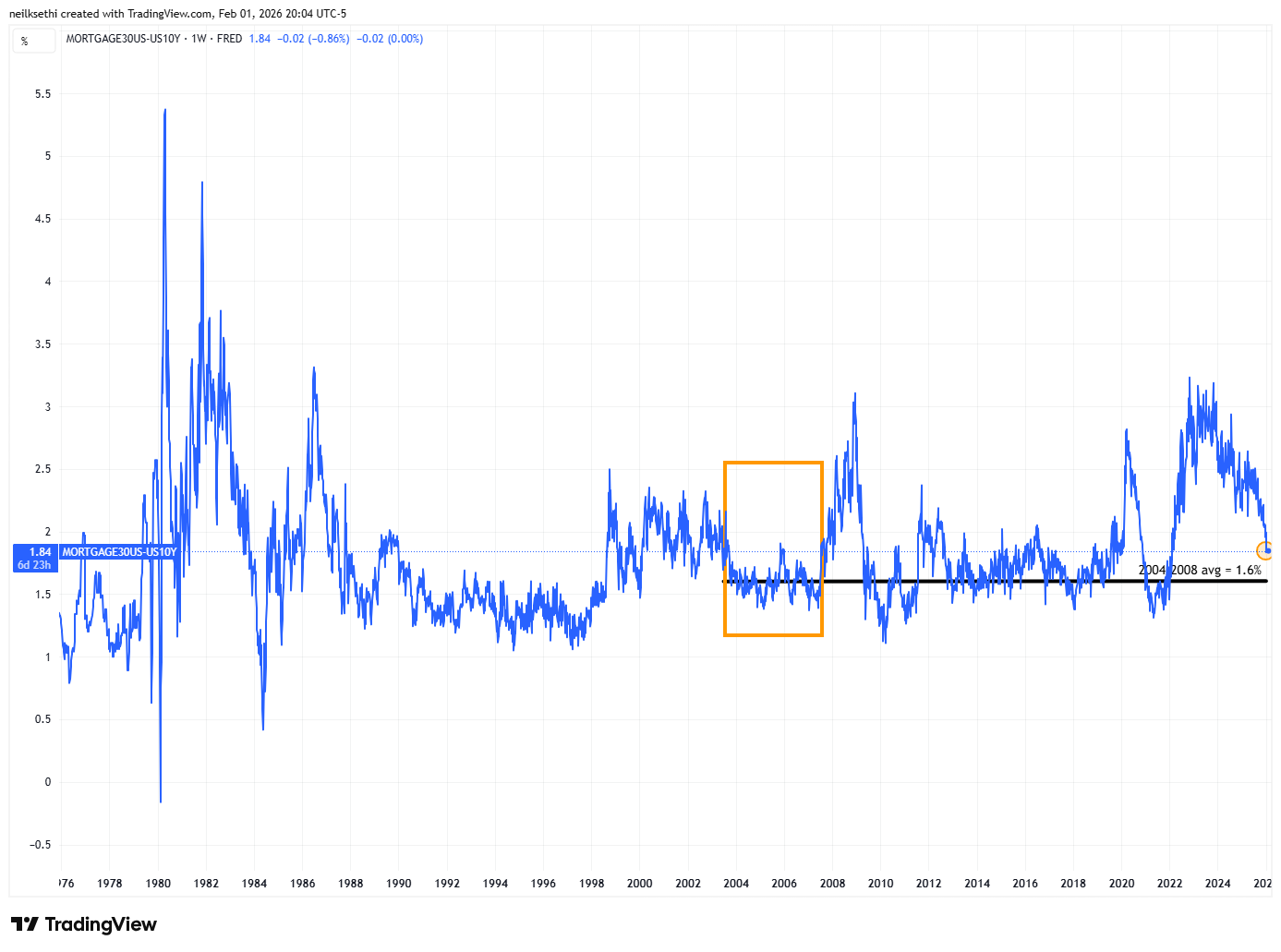

Mortgage spreads (based on the Freddie Mac 30-yr rate) edged lower despite the increase in the MOVE index now at 1.84% the least since Feb 2022 (when they were surging higher from 1.45% in Jan 2022 to the 3.1% peak in June 2023 as the Fed tightened rates).

Still, they remain well under the peaks from the 2010-2019 period but still have some room (~24bps) for them to fall to get to the 2004-2008 avg level of ~1.6% (I use that period as it was like now a period of higher yields than post-GFC and also a period when the Fed wasn’t buying MBS and we had a more robust private market pre-2004 although with Fannie/Freddie maxing out their MBS purchases we very well might fall right through that). It also happens to coincide with the pre-pandemic 10-year average as well despite the distortions from Fed purchases, etc.

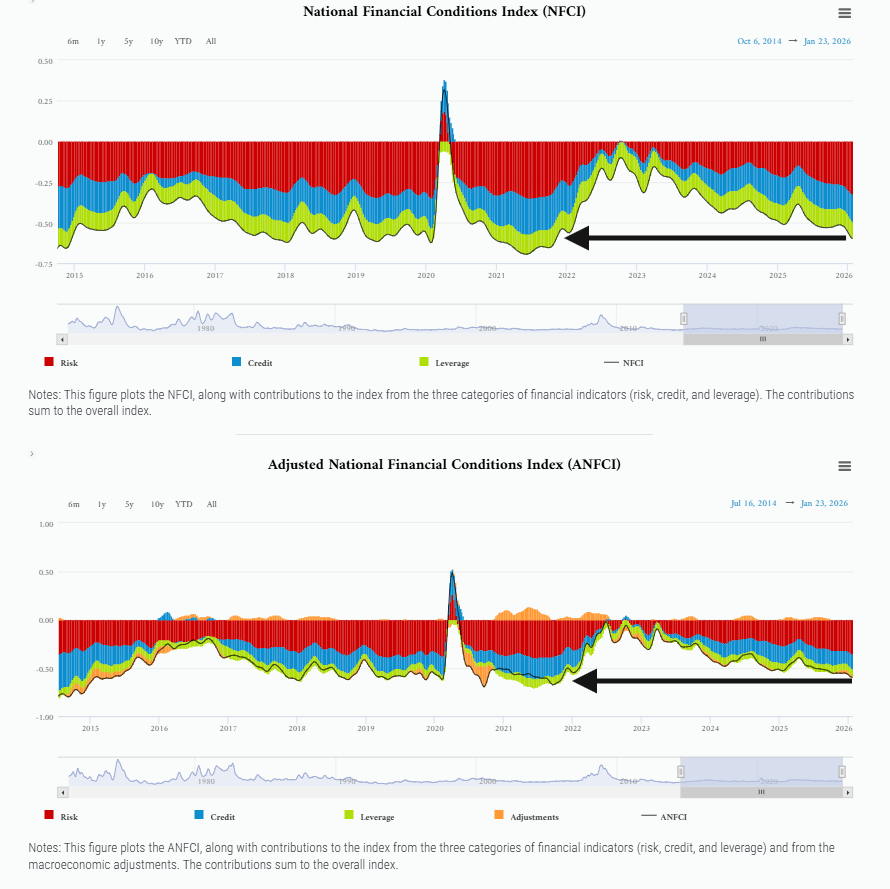

The Chicago Fed National Financial Conditions Index and its adjusted counterpart* each took another step down (looser) to the least (loosest) since Nov ‘21 in the week through Jan 23rd.

*Both of these indexes are very comprehensive, each w/105 indicators. The “adjusted” version attempts to remove the correlation between the various indicators due to broad changes in economic conditions which also impact other areas (so as to not double count them).

https://www.chicagofed.org/research/data/nfci/current-data

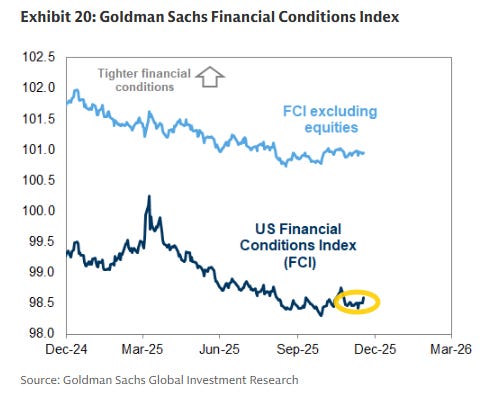

Goldman’s US Financial Conditions Index moved higher after last week falling to the least (loosest) since October (which in turn was the least since April 2022). Still remaining very loose historically.

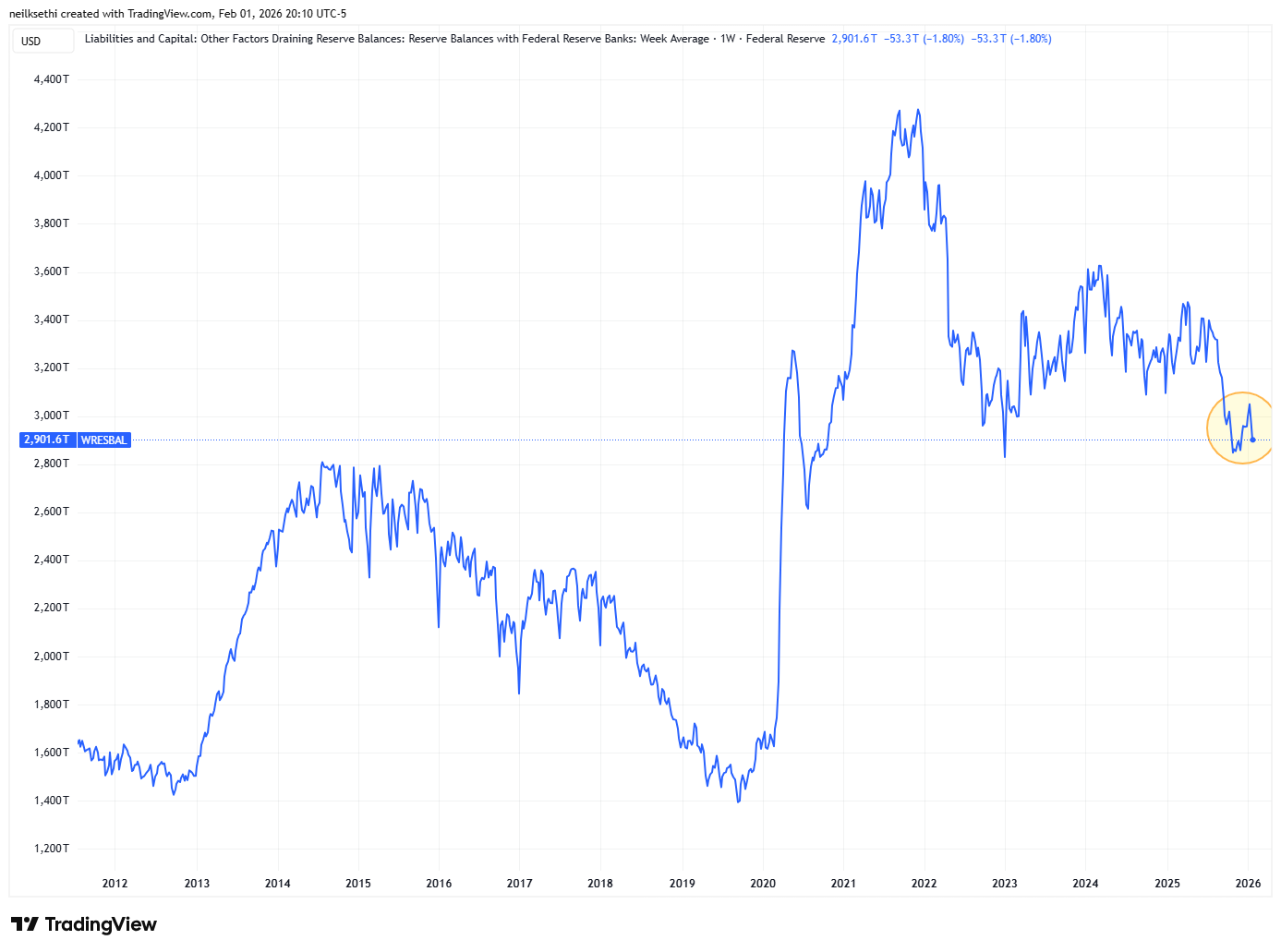

Bank reserves, which fell as low as $2.83tn as of the end of October, which was the least since Oct 2020 and down from $3.6tn Apr 10th (the highs of the year) under my “danger zone” level of sub-$2.9tn, fell back to $2.9tn, but likely just as a function of month end (as banks shed risk-weighted assets for their “snapshot” for regulators).

Given the FOMC reserve management purchases of $40bn a month (for the time being) added to the end of QT (as of Dec 1st), I would expect them to bounce back next week. Even at current levels though it is a level Fed members have generally indicated they are comfortable with.

Getting back to rates,

I said back in April 2024 that 2-year Treasuries were a good buy at 5%, and as I noted once the Fed started its cutting cycle thereafter the ship has likely sailed on seeing those yields anytime soon (meaning years). I still have some 2yr’s left but have sold over half the position , not really getting a chance to reload as they never seem to be at a level that makes sense, although most analysts think they’re going lower from here.

In terms of 10yr’s I had advised then grabbing some at 4.7% (which I subsequently sold on the drop under 3.75% as posted here in September). At the time 4.7% seemed like something we wouldn’t see anytime soon, but we got back there in January of last year (and I added some as posted here), and it seemed like we might be headed much higher until Treas Sec Bessent noted the administration’s focus on keeping the 10yr yield low (and perhaps more importantly committing to the auction schedule set up by Sec Yellen for the foreseeable future (and perhaps even reducing longer term supply as he has noted in subsequent interviews and through the increase to the Fed’s buyback program), which has exerted downward pressure on 10yr yields). I sold that new, small position on the dip under 4% in April, and I had been waiting on us revisiting that 4.7 - 5% area to reload. But as I said in late Sept, it is looking less and less likely that I will get that trip back up to the 4.7% area to add to my 10yr holdings any time soon. I had been thinking that 4.3-4.5% is potentially in the cards, and we finally got that there for a hot second, but they have fallen back (in line with my statement that week that “there is very strong resistance there”). I bought a small amount but would prefer something closer to 4.5% to really wade in.

In 2025 the 10yr yield for the most part held the bottom of of my 2025 likely trading range of between 4 and 5%. As I said coming into the year, my 2026 range is 3.5 to 4.5% (with risk to the downside if the labor market continues to weaken). There is now some moderate risk to the upside if Kevin Warsh becomes the Fed chair, but allowing higher 10-year rates would be inconsistent with Pres Trump’s goal of lower mortgage rates. So we’ll see.

For all the old “final hike” and “first cut” materials, you can reference the Feb 4th blog post.

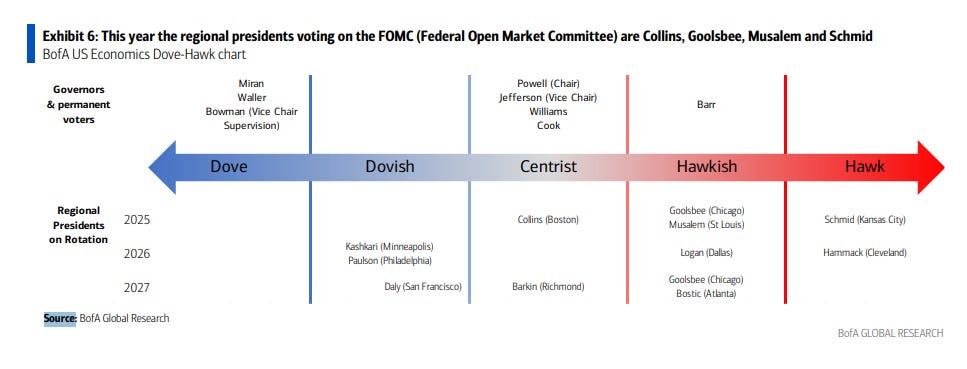

BoA finally updated their Dove-Hawk chart. Logan I think is as hawkish as Schmid, and I’m not sure I’d characterize Goolsbee as Hawkish, more Centrist, but otherwise seems about right.

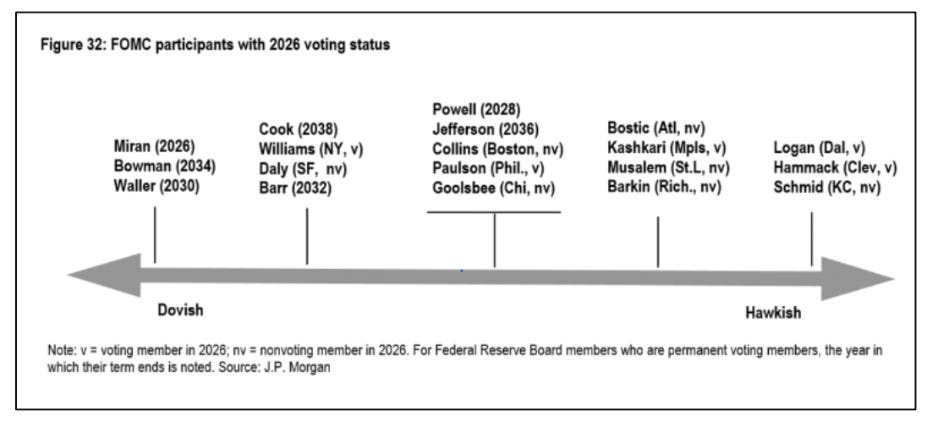

And JPM has one that gives you 2026 voters. I have some quibbles. The ends are fair but there really should be a distinction b/w Miran and the rest. No way is Barr dovish (and he proved that with a speech not long after I first wrote that). He’s now proven himself to be with the Bostic/Kashkari Fed Presidents. Also, not sure about Cook (she seems to vote with Powell). I think Paulson though should be with Williams and Daly (and she proved that with a speech on Dec 12th. Collins was fairly hawkish in her last appearance as has been Goolsbee (although he’s tricky, dissenting from the Dec cut but also saying “I’m one of the most optimistic folks about how rates can go down in the coming year.”). Otherwise hard to argue much with the slotting.

And here’s one that goes over current term expirations. Note that all of the regional Fed presidents had their terms renewed for another five years (so now expire Feb 28, 2030)

Earnings

As a reminder, I have removed most of the background material, which you can get in the Feb 4th blog post. You can reference this post from 12/1/24 for stats on 3Q, this post from 3/9/25 for stats on 4Q, and this post from 6/1/25 for stats on 1Q 25. And the 9/1/25 post for 2Q 25.

While Q3 earnings will continue to trickle in, they won’t move the needle, so if you want to reference the stats for Q3 you can find them at this posta from 11/23/25.

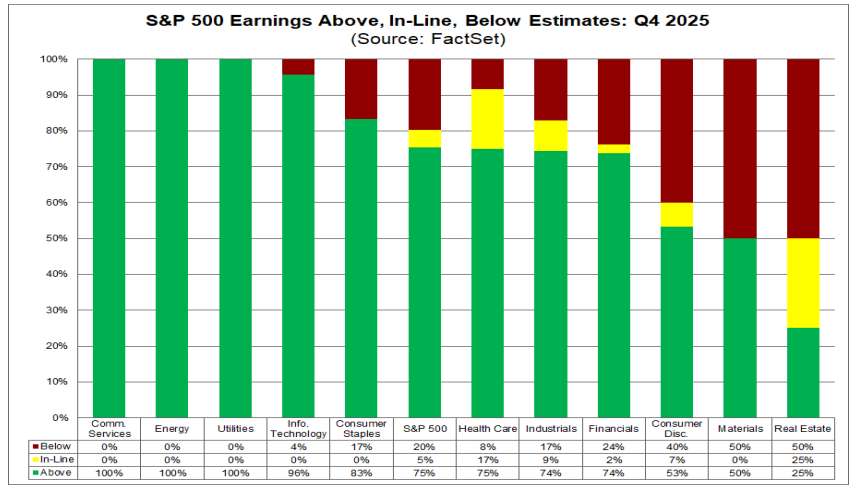

With 33% of the SPX by earnings weight having reported (so still on the early side) through Thursday, 75% have beaten (unch w/w and down from 83% in Q3, which though was the best since Q2 ‘21), below the 5yr average of 78% and the 10yr average of 76%.

While the % of companies beating has remained the same, what saw a big change last week is the magnitude of the beats which are now +9.1% y/y (up +3.6% w/w), well above the +6.6% in Q3, and also above the 5yr average of 7.7% and the 10yr average of 7.0%.

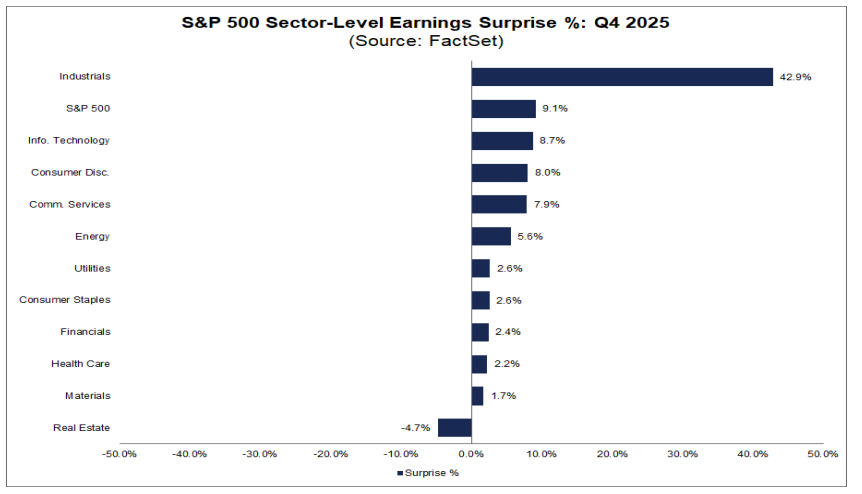

Leading the change is a massive 42.9% beat amount for the Industrials sector (the only sector above the SPX’s +9.1%), but note this is more due to accounting than performance: “Boeing ($9.92 vs. -$0.44) and GE Vernova ($13.48 vs. $2.93) have reported the largest positive EPS surprises. The actual EPS for Boeing included a $9.6 billion dollar gain on a sale connected with closing of the Digital Aviation Solutions transaction, while the actual EPS for GE Vernova included a $2.9 billion tax benefit due to a U.S. valuation allowance release.”

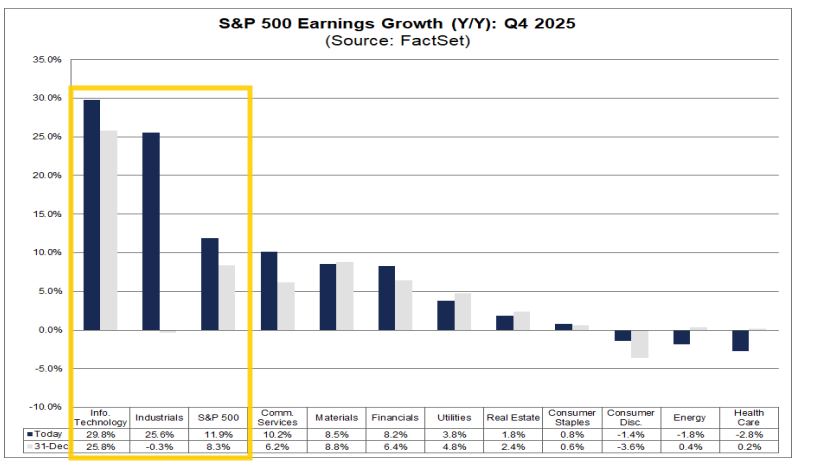

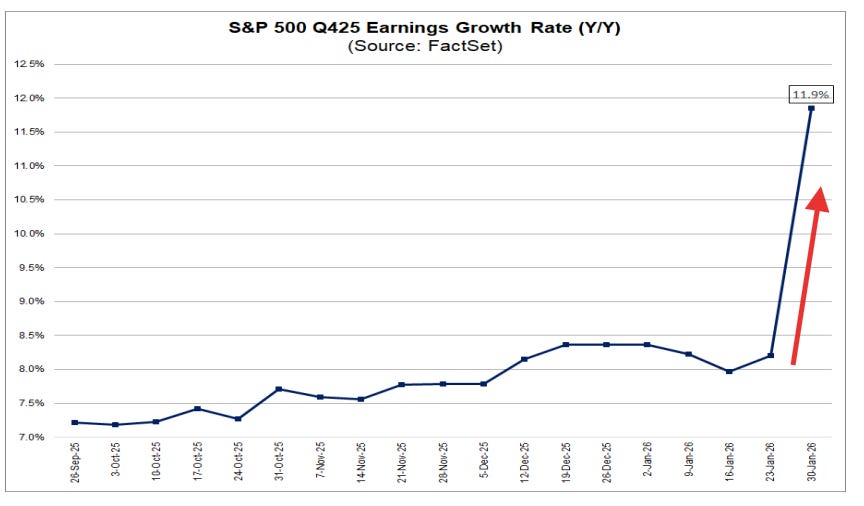

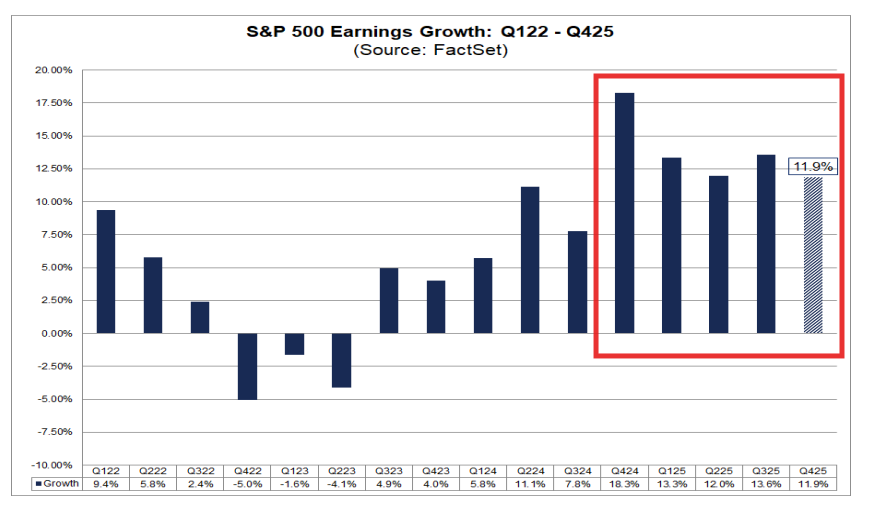

With the stronger beat amounts,, expectations for Q4 y/y earnings growth jumped to +11.9% (from +8.2% the prior week) according to Factset, which now represents a +4.1% increase from Sept 30th (and up +3.6% since the start of the year). The last time the S&P 500 reported 5 consecutive quarters of double-digit earnings growth was Q4 2017 through Q4 2018.

The 8.2% in expected earnings growth continues to be largely driven by Tech which is expected to see a huge +29.8% y/y increase (+3.6% w/w).

The only other above 11.9% is Industrials at an almost equally big +25.6% (up from -0.3% at the start of the year (largely though due to those accounting gains noted earlier)). In contrast Cons Discretionary, Health Care, and Energy, are expected to see negative y/y growth.

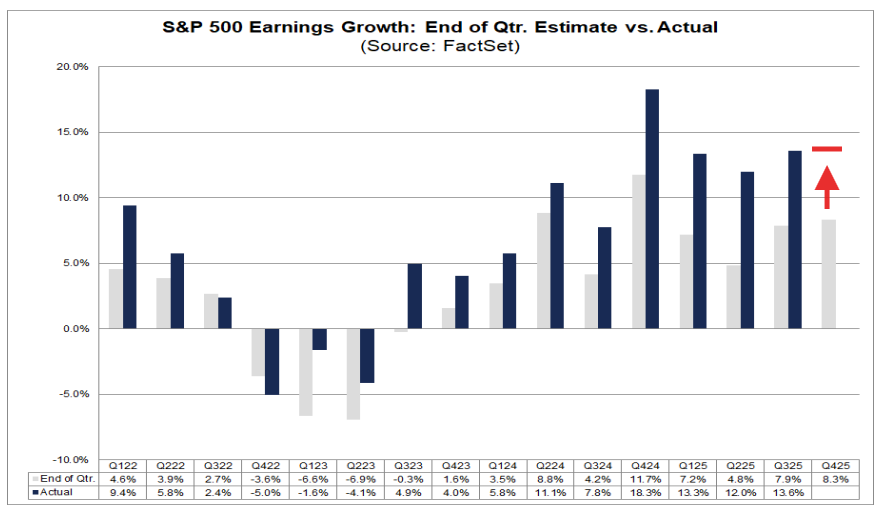

And I noted two weeks ago if past is any guide the earnings growth for Q4 can be expected to come in at +14.0% or higher as Factset says over the past 1, 5 & 10 yrs companies have beaten earnings expectations by 7.4%, 7.7% & 7.0% respectively resulting in “inflation” to the earnings estimates on average over the quarter by 6.4%, 7.4% & 5.7% respectively over where they stood as of the start of the quarter (in this case Sept 30th which was 8.2%).

So using those averages would mean Q4 earnings will come in at +14.7%, 15.7%, or 14.0% respectively.

Actual earnings by the end of the quarter have not surpassed expectations at the start of the quarter in only 3 of the past 43 quarters (Q1 ‘20, Q3 ‘22, and Q4 ‘22 are the only exceptions according to Factset).

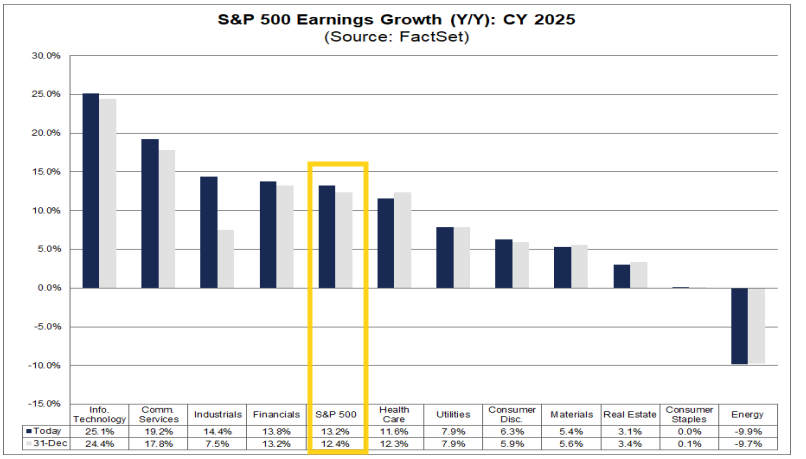

2025 earnings growth expectations as a result moved to +13.2% from +12.4%, the prior week (and where it started the year), and up from +10.6% Sept 30th.

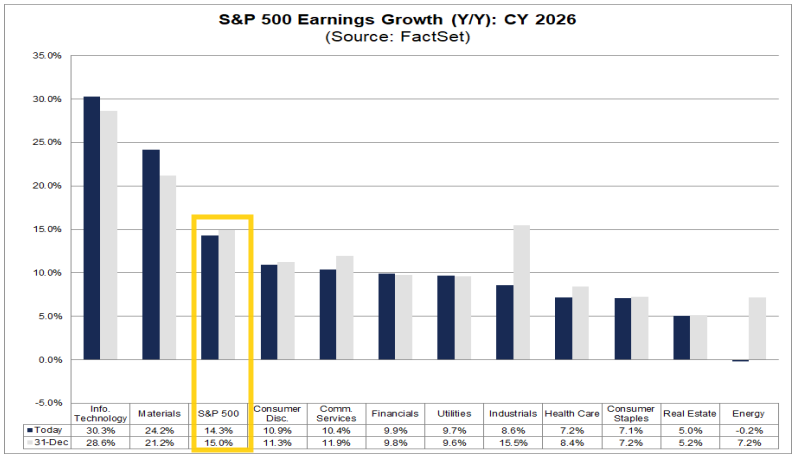

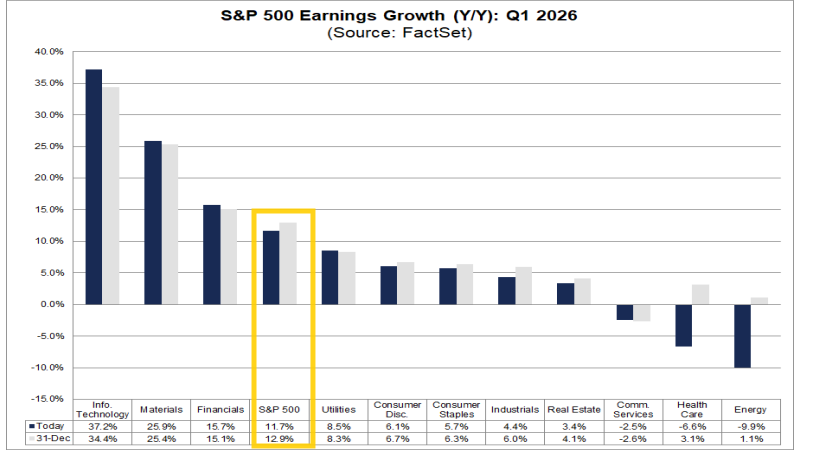

2026 earnings growth expectations remain at a very robust +14.3% although edging back -0.4% as the “base” (2025 earnings) moved notably higher this week). 2026 is again expected to be led by Tech at +30.3% (which is up +1% w/w despite the higher base). That would be the third year of double-digit growth earnings growth.

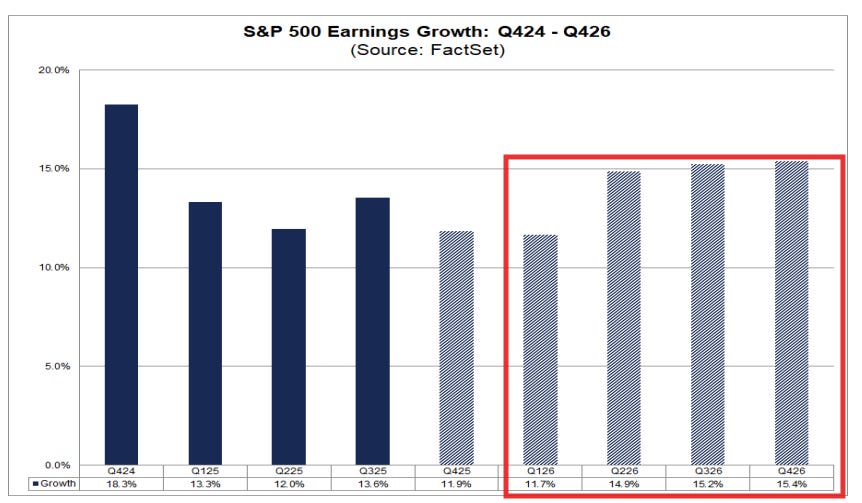

And that double digit y/y earnings growth is expected to continue throughout 2026 with Q1 at +11.7% (+0.5% w/w although still down from 12.9% at the start of the year), while Q2 is +14.9% (+0.4% w/w), Q3 +15.2% (+0.4% w/w) and Q4 +15.4%(-3.0% w/w, dropping due to the big increase in Q4 ‘25 earnings).

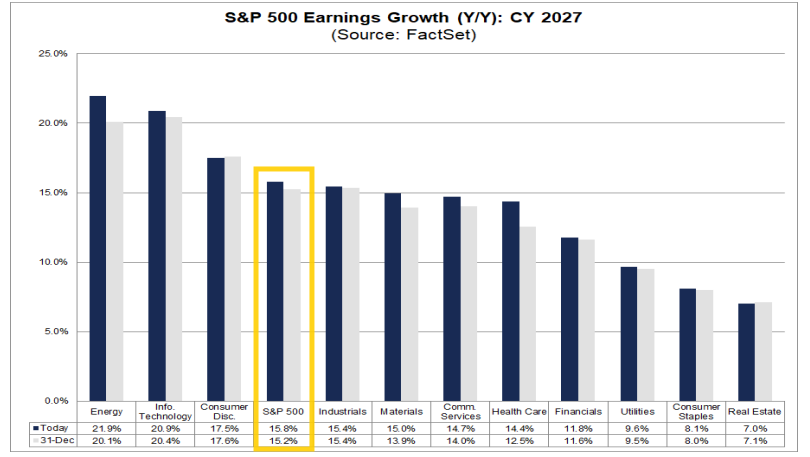

And 2027 earnings are expected to grow another +15.8% (+0.1% w/w), which would be a fourth year of double-digit growth. Interestingly Energy is expected to take the lead +21.9% (-0.9% w/w but +1.7% since the start of the year) followed by Tech +20.9% (-0.1% and +0.5%).

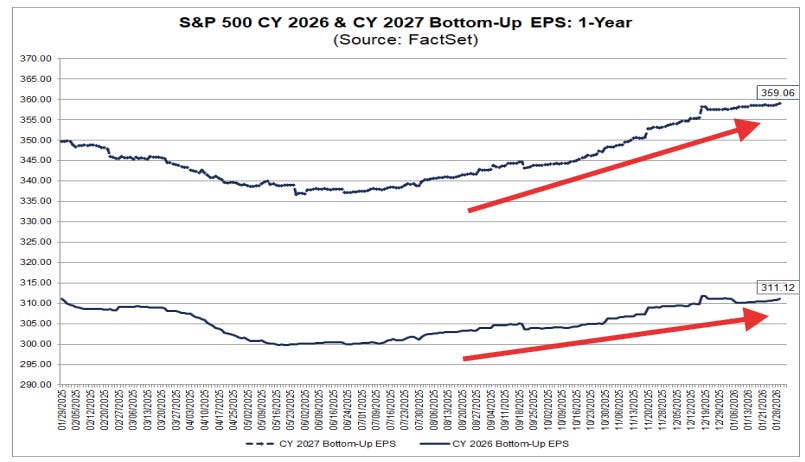

In terms of the earnings growth expected for 2026 Factset notes it will be a record. On average over the past 25 yrs there is a -6.3% deterioration from where it starts the year ($311) which would equate to $292.34 based on the average deterioration. But Factset pulls out 4 outlier years (2001, 2008, 2009 & 2020) where the overestimation was between 27-43% due to recessions. Excluding those, and assuming no recession, the difference is just -1.1% (which would equate to $307.58.

Looking at 2026/2027 earnings expectations on a numeric basis both pushed higher this week to with the former to $311.12 little below the peak while 2027 earnings expectations are at $359.06, a record high

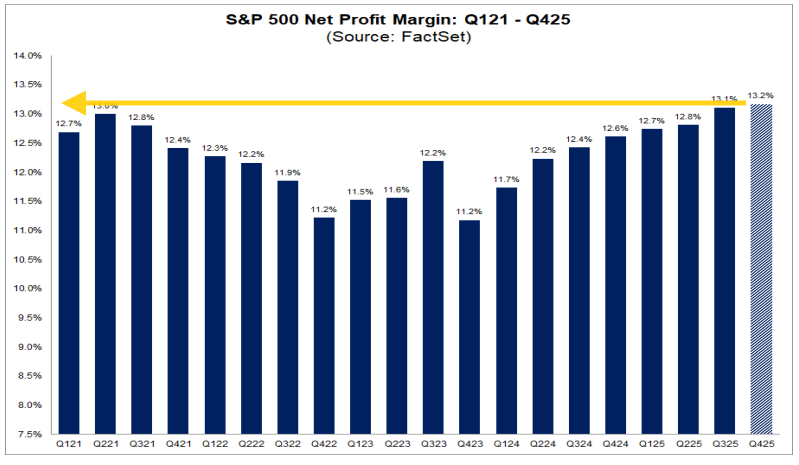

Q4 profit margin expectations jumped along with earnings to +13.2%, the highest since Factset tracking started in 2009. It is vs 12.7% in Q4 ‘24 and the 5-year average of 12.1%.

And analysts expect it to continue to set new records in 2026 according to Factset. “As of today, the estimated net profit margins for Q1 2026 through Q4 2026 are 13.2%, 13.8%, 14.2%, and 14.2%, respectively.”

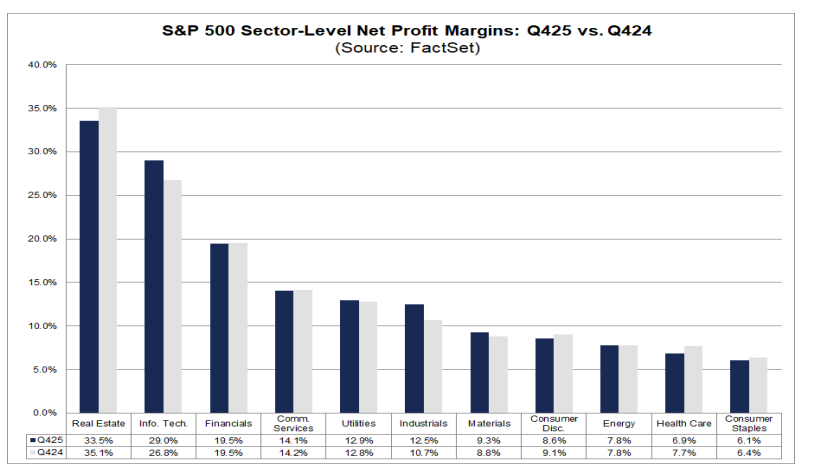

Four sectors are reporting a year-over-year increase in their net profit margins in Q4 2025 compared to Q4 2024, led by the Information Technology (29.0% vs. 26.8%) and Industrials (12.5% vs. 10.7%) sectors

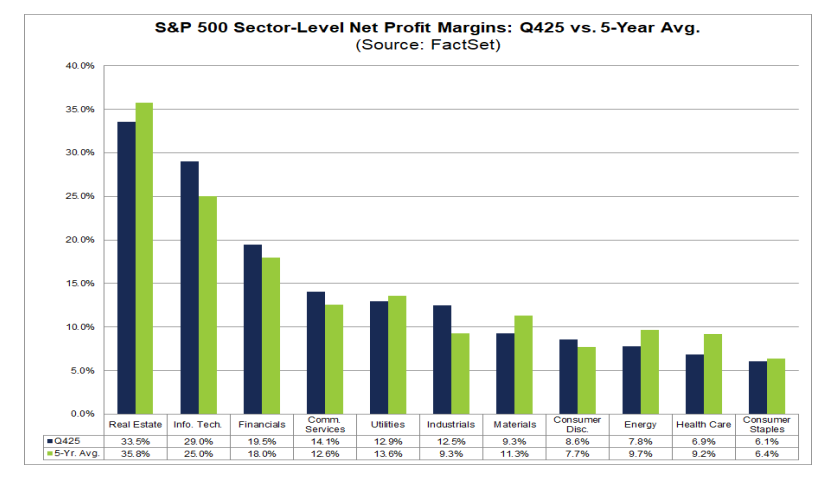

Five sectors are reporting net profit margins in Q4 2025 that are above their 5-year averages, led by the Information Technology (29.0% vs. 25.0%) and Industrials (12.5% vs. 9.3%) sectors

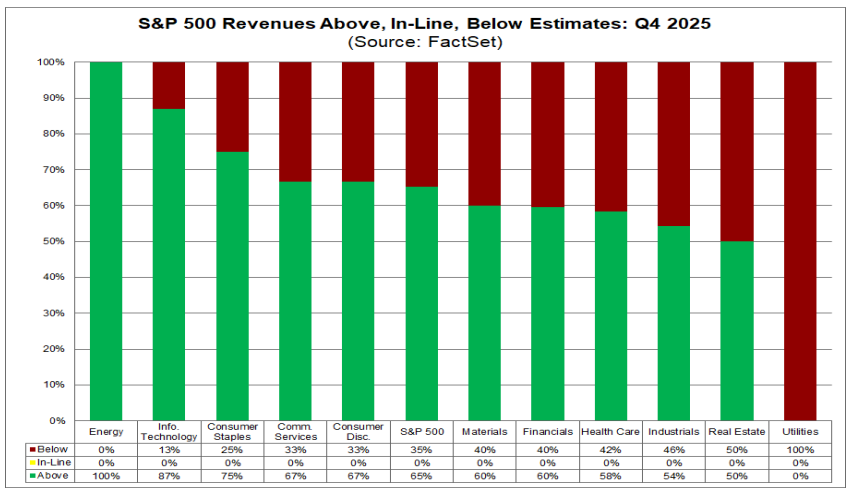

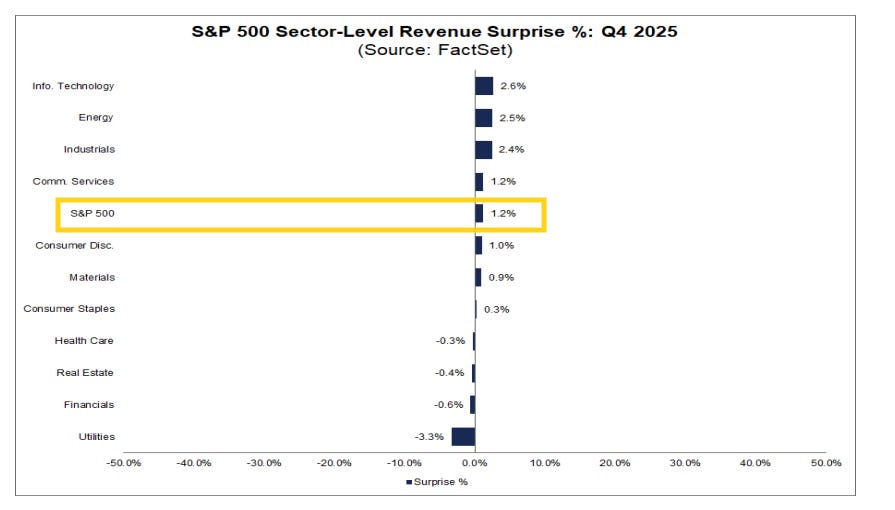

In terms of revenues for Q4, 65% of S&P 500 companies have reported revenues above estimates according to Factset, down -4pp from the prior week below the 5yr average of 70% and the 10yr average of 66%.

And like earnings the beat amounts have jumped higher to +1.2% still though well below the 5-year average of 2.1% and also below the 10-year average of 1.4%.

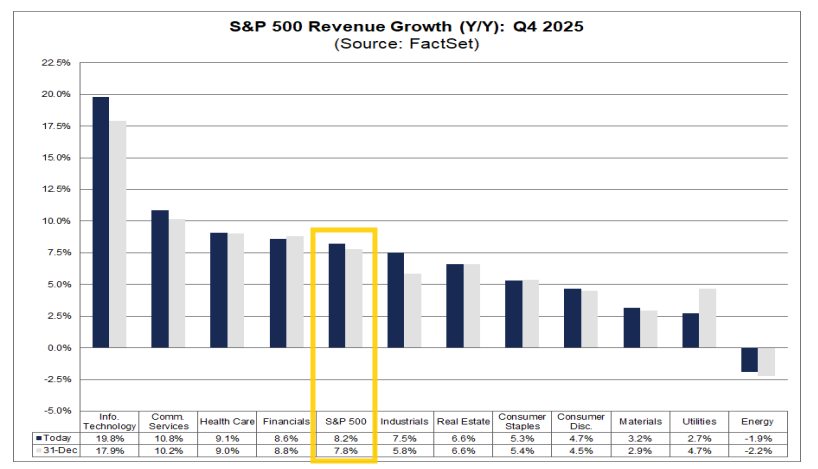

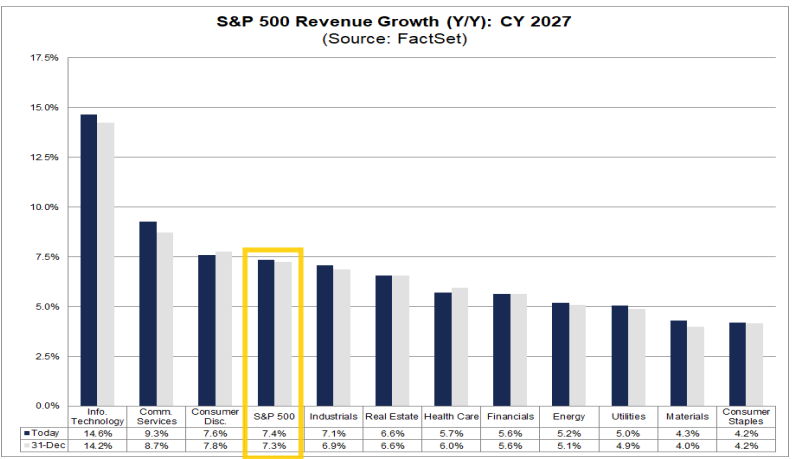

SPX revenues are now expected to grow +8.2% y/y according to Factset (+0.4% w/w). Those have also grown from +6.4% on Sept 30th.

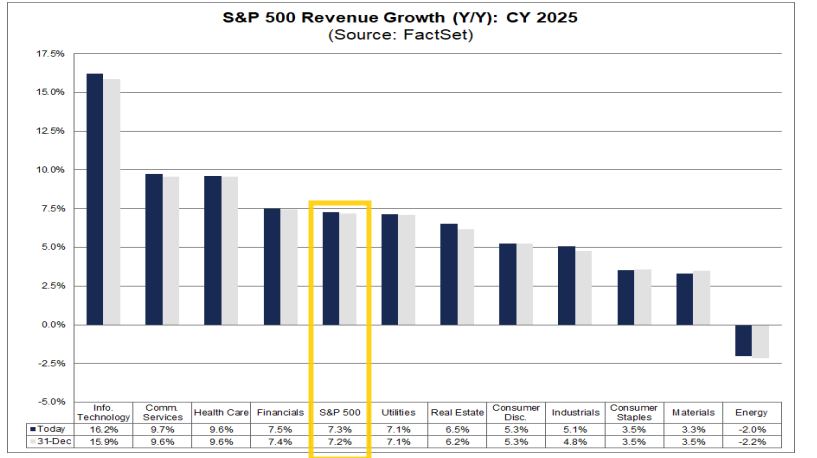

Factset: 2025 revenues are now expected to grow +7.3%, +0.1% w/w and +1.7% since the start of 2025 (which is an unusually high increase). Just energy is expected to have negative revenue growth (but much less than expected even June 30th).

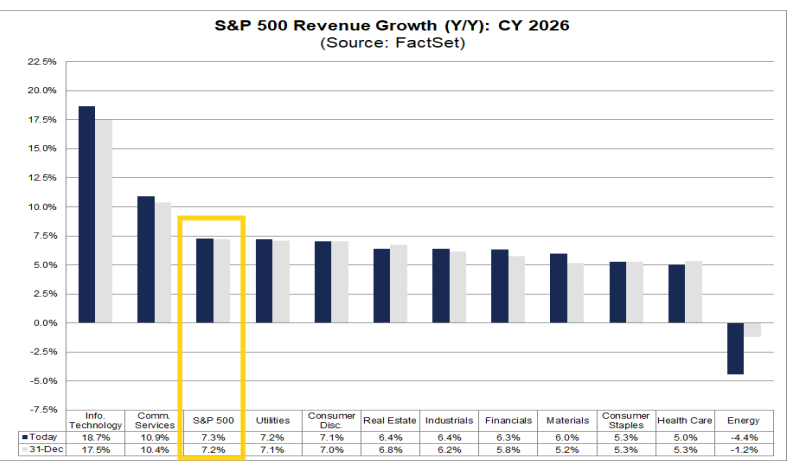

2026 SPX revenue growth is expected at +7.3% (unch w/w despite the higher base), with Tech +18.7% (+0.5% w/w) and Comm Services +10.9% (+0.4% w/w) carrying the load (the only two sectors expected to be above the SPX).

2027 SPX revenue growth is expected at an equally strong +7.4% (+0.1% w/w) with again Tech +14.6% and Comm Services +9.3% leading (up +0.1% and +0.4% respectively w/w).

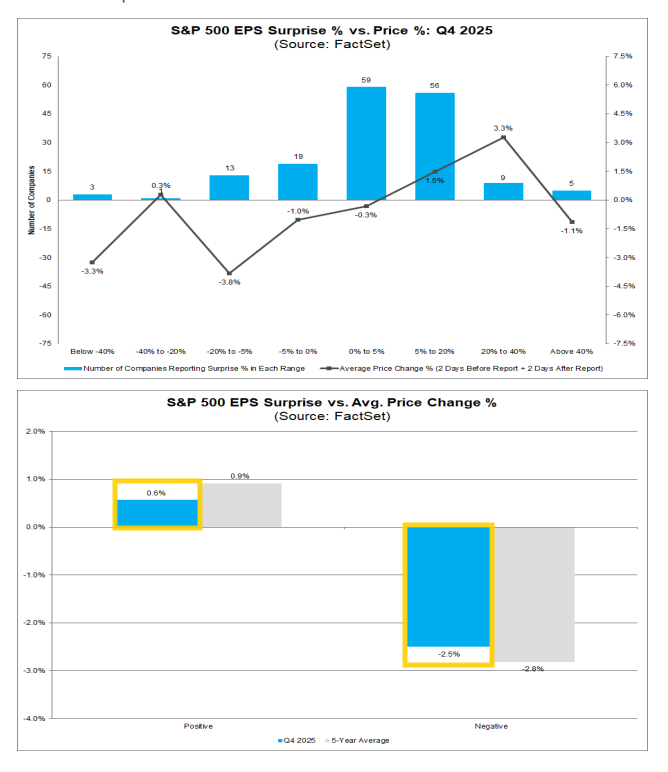

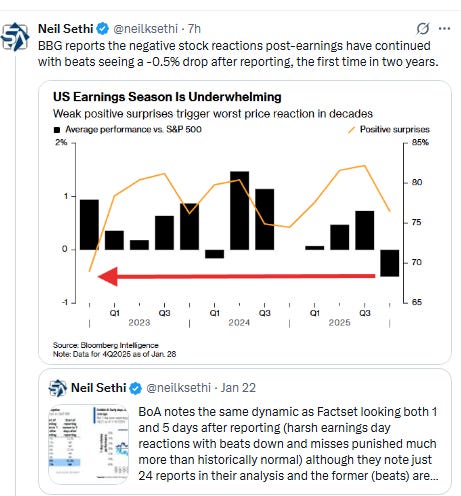

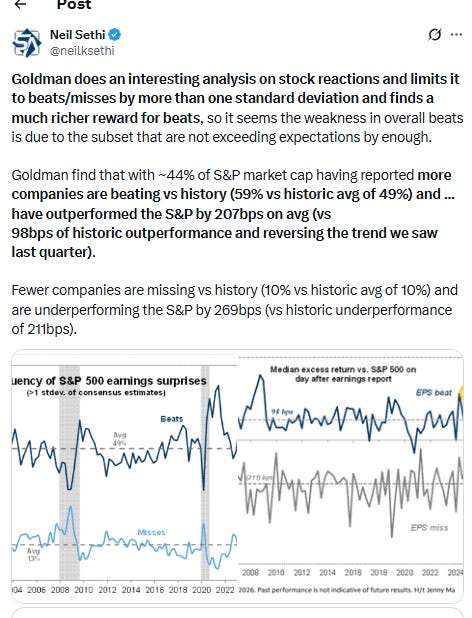

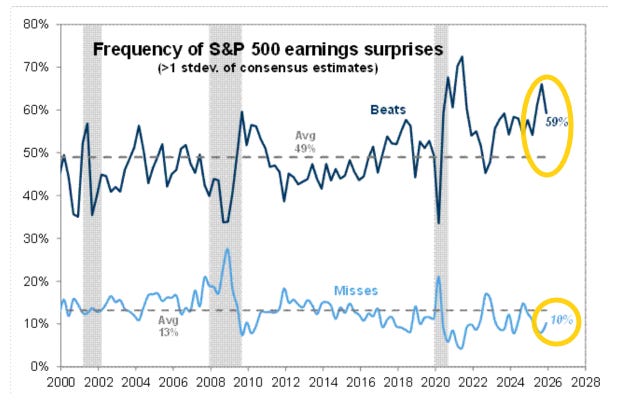

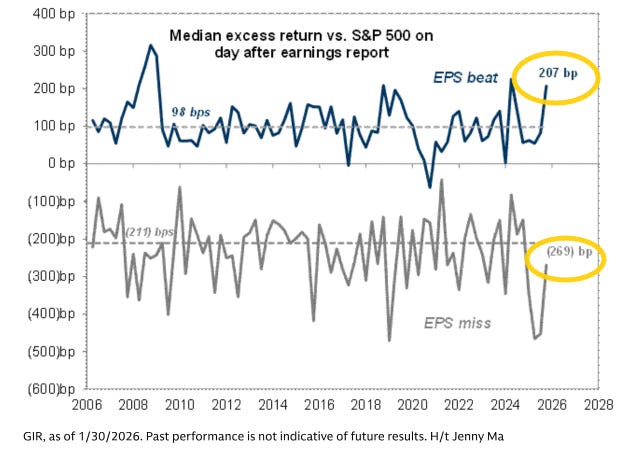

In terms of how markets are handling earnings beats & misses for 4Q, looking at the two days before to two days after a report Factset finds we are for a third quarter seeing beats rewarded less than typical but just modestly so at +0.6% (from -0.4% two weeks ago). That’s now above the +0.4% in 3Q and 2Q but below the 5-yr average of +0.9%.

Meanwhile misses are now longer being punished more than average at -2.5% from -4.0% two weeks ago and vs the -5.0% in 3Q and -5.5% in 2Q (the latter of which BoA said was the worst negative reaction since 2000), now basically in line with the 5-yr avg of -2.8%.

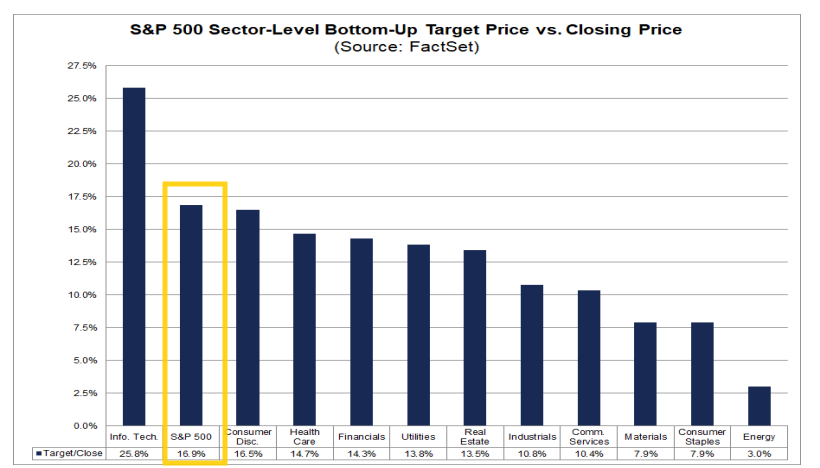

Factset’s compilation of analyst bottom-up SPX price targets for the next 12 months as of Thursday continued to increase for a 31st week to 8,145 which would be +16.9% from Thursday’s close. That’s an ATH +35pts w/w (+614pts the past 11 weeks and +1,512pts the past 31 weeks).

Tech (+25.8% down from +27.4% the prior week) easily remains the sector seen by analysts with the largest upside (the only sector above the SPX), followed Cons Discr (+16.5% up from +15.3%), while Energy remains the sector expected to see the smallest price increase (+3.0% down from +5.7% and +7.5% the week before that) followed by Staples (+7.9% unch but down from +13.5% two weeks ago).

As Factset reminded us in December, the last 20 yrs (through 2024) analysts have been on avg +5.9% too high from where they start the year (which was 6,755 coming into 2025, 8,000 for 2026) but note they underestimated it five of the past six years (including 2024). They ended ~100pts too low.)

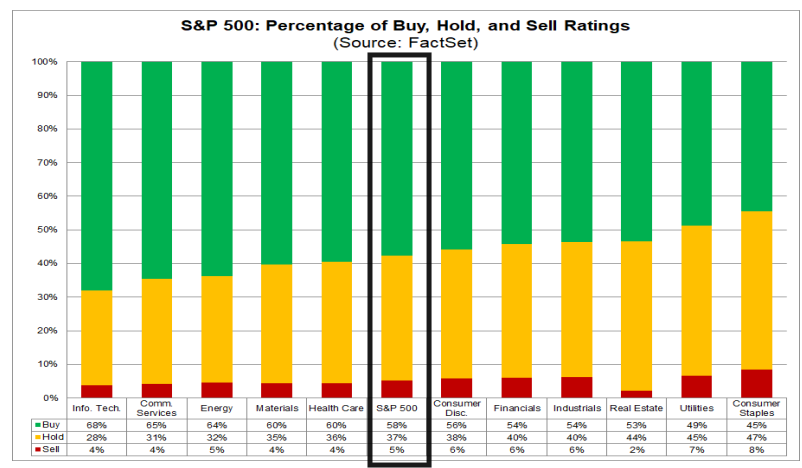

Factset: In terms of analyst ratings, buy and hold ratings continue to dominate with buy ratings at 57.7%, the highest on record (to 2010) at month-end according to Factset. Hold ratings are at 37.2%, with sell ratings at 5.1%.

The Information Technology (68%), Energy (65% unch despite the rally), and Communication Services (64%) sectors have the highest percentages of Buy ratings, while Consumer Staples (45%) has the lowest percentage.

Consumer staples also has the most sell ratings at 8% (down a tenth w/w) and Hold ratings at 47% (down from 50% six weeks ago, next closest on Hold ratings is Utilities at 45%.

The percentage of Buy ratings is above its 5-year (month-end) average of 55.1%. The percentage Hold ratings is below its 5-year (month-end) average of 39.0%. The percentage of Sell ratings is below its 5-year (month-end) average of 5.9%.

Factset also notes that two of the three sectors that have recorded the largest price increases since December 31st are also two of the three sectors that had the highest percentages of Buy ratings on December 31st: Communication Services and Information Technology. The other though, Energy, saw the second smallest price gain since then.

Just one of the three sectors that have recorded the smallest price increases since December 31 are also one of the three sectors that had the lowest percentages of Buy ratings on December 31st: Consumer Staples. The others were Utilities and Materials/Industrials.

And some other earnings stuff:

Economy

Over the past 2+ years part of my earnings optimism has been due to the economy holding up better than expected. While earnings only track the economy loosely (and markets look forward 6-12 months), there is a clear positive correlation between the economy and earnings (particularly a weak economy and weak earnings), and there is a very strong correlation between earnings and stock prices (although stock prices (being as noted forward looking) generally fall in advance of a recession and bottom 6-9 months before the end of one). So if you can see a recession coming it is quite helpful, although very difficult (especially ahead of the market). You can reference this Week Ahead (see the Economy section) for a lot of material on how every recession is preceded by talk of a “slowdown” or “soft landing” as close as a month before the start. That report also has the notes about how small caps have shorter debt maturity profiles and more of it (debt).

As long time readers know the beginning of this section hadn’t changed much since I switched to the Week Ahead format in mid-2022, with the indicators to me during that period consistent with solid (which at times has been robust) economic growth, and I have been a broken record that I “certainly do not think we’re on the verge of a recession (although as noted above every recession starts out looking like just some economic softening).”

Since the end of March, though, we’d seen the data soften (it actually stretched back pre-March with 1Q services spending getting a notable markdown in the GDP revisions (as did services exports (tourism, etc.) and construction spending)) with reports since then more mixed, although remaining consistent with an economy running around trend levels (if not a bit above).

While we were deprived of the official data, what we saw during the shutdown “seemed to offer little change in the picture with estimates of layoffs and hires remaining generally low, consumer sentiment remaining weak, but private estimates of spending healthy, reinforced by earnings reports which also indicate a fairly healthy business environment (even if top-heavy) with solid balance sheets and low delinquencies (again though with some cracks in the subprime or leveraged areas and what seems like perhaps some slowing in certain pockets of discretionary spending like restaurants).”

And as noted in mid-December “we continue to see an economy with some softening in hiring but spending remaining very solid along with good business investment spending, strong government spending (concentrated in defense and other administration priorities), offset somewhat by weak spending on structures outside of data centers and subdued exports.”

But as I noted last week, the data“to me is starting to show some evidence of reacceleration in the economy and even some green shoots for the labor market (although that is still more mixed).” This past week saw more potential evidence of that with Nov durable goods and core capital goods orders coming in much better than expected as did overall factory orders, 3Q GDP productivity remained unchanged at its very strong initial read, and jobless claims remaining historically low. We did see exports fall back, consumer confidence fall to the least since 2014, and Nov producer prices come in hot, but I would say on balance the data was consistent with my reacceleration theme.

As I said two weeks ago,

I have said the past several months “the data continues to show an economy remaining in ‘ok’ shape (although a 3Q GDP print over 4% is definitely more than ‘ok’ and now 4Q is looking to be better than anyone had expected coming in), with continuing ‘tiny cracks’ as I put it in mid-June,” but if the data continues to inflect higher, particularly with the tax refunds that are upcoming (and it appears more fiscal stimulus coming down the pike), continued expansion in AI spending, government spending having troughed, the Fed more inclined to cut than raise rates, etc., I will soon have to upgrade that to “an economy that has reaccelerated to “solid” shape”.

I think at this point it’s hard not to describe the economy as being “in solid shape”.

And as I said at the start of September 2024:

without question, the evidence is building that the days of >3% real GDP growth are behind us. That though is far from a disaster, and we should be happy to settle into something more around trend (1-3% real (infl adjusted) growth). The important thing will be to see the softening level out (L-shape) rather than continue to fall turning the “soft landing” into a recession.

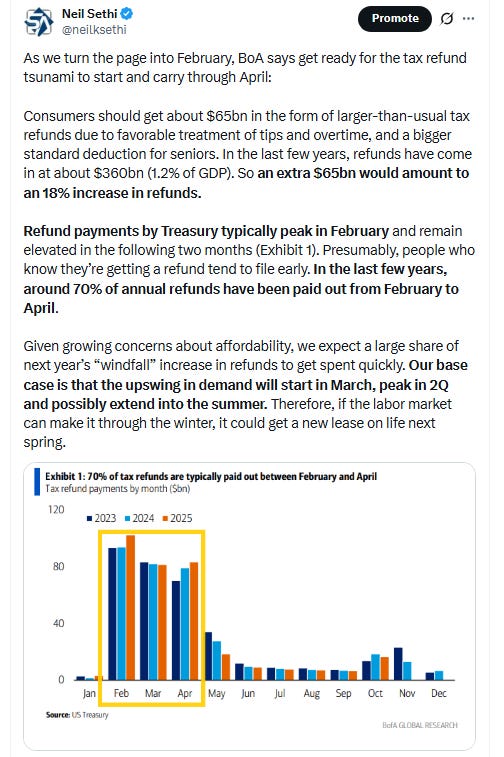

Finally, as mentioned, as we turn the page into 2026 we’ll be getting more economic boost from deregulation and the OBBB which should at the very least offset the drag we’re getting from the tariffs, restart of student loan payments, and in the short-term loss of the health insurance subsidies (although I expect those last to be replaced at some point) and perhaps provide a bigger tailwind than many are expecting.

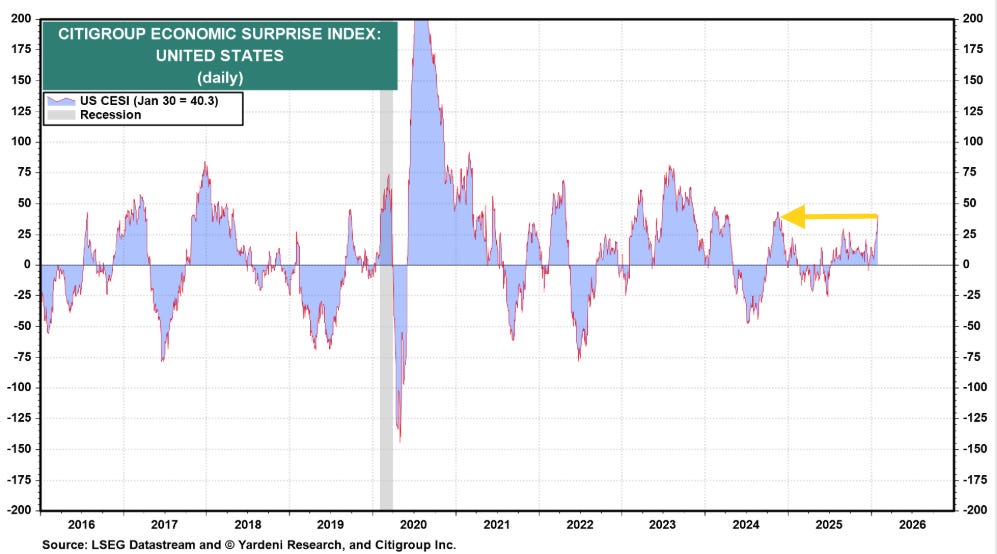

The Citi Economic Surprise Index jumped to +40.3 as of Friday, the highest since Nov ‘24 from +25.2 the prior week. The 2024 high was 47.7 (in Feb). The only caveat is that inflation reports (PPI) coming in above expectations are a “beat” so helped push it higher even if a market negative.

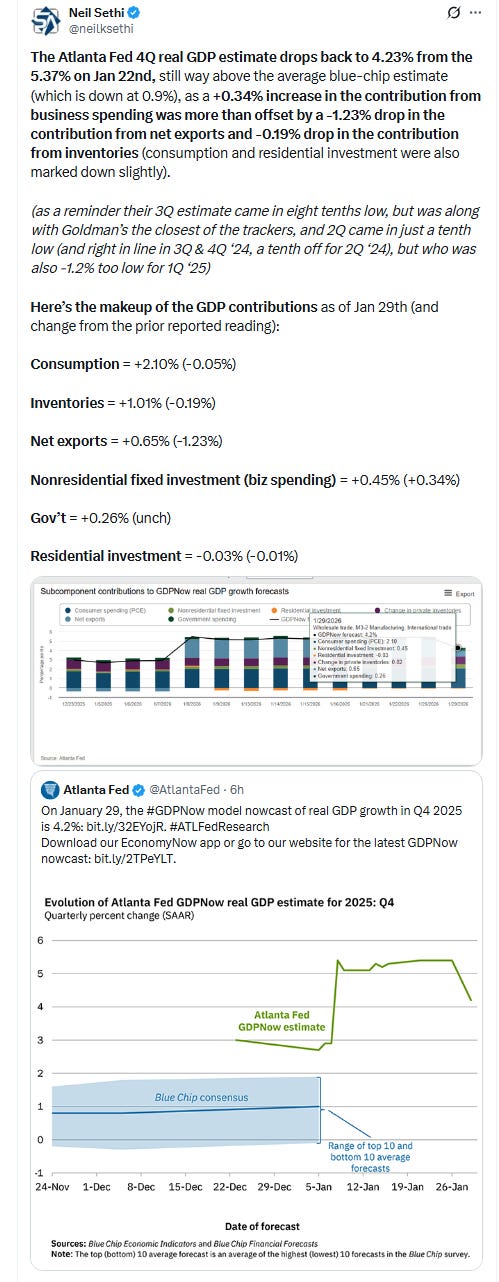

And GDP estimates are for now consistent with a no recession call (again though remembering GDP going into recessions generally doesn’t look like one is coming (it was up around 2% in Q2 & Q3 2008 well after the recession had started)). After a very strong read in Q3, estimates outside of the Atlanta Fed are for some slowing in Q4 due to the shutdown drag (which will be “paid back” to us in the current quarter), but estimates for the most part have been rising quickly with a 2% or higher quarter now expected by almost all the trackers (and several closer to three with Atlanta Fed over 4%) much better than the 1% the ‘“blue chip consensus” expected coming into the quarter.

Atlanta Fed saw their 4Q GDP tracker fall back to 4.23% after having come in the closest (along with Goldman) for 3Q at +3.48% vs the actual 4.3%.

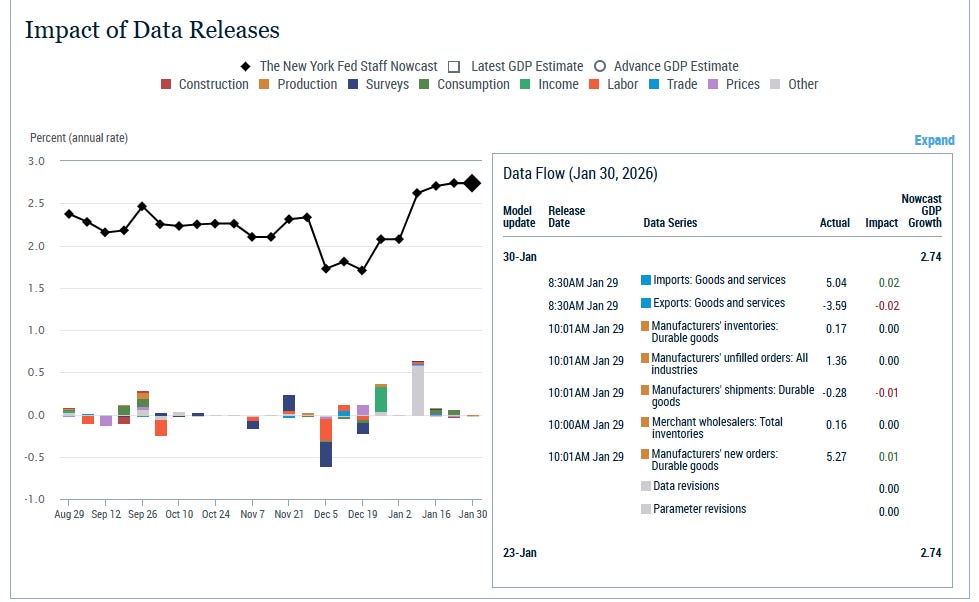

Surprisingly the NY Fed’s 4Q GDP tracker remained just off the highest since it initiated tracking in August at 2.73% (the peak was 2.75% Jan 16th) not seeing any net changes from the very unexpected trade balance report (which saw cuts to other GDP trackers).

As a reminder, they were well under for 3Q at +2.31% vs the +4.3% actual first estimate and 2Q at +1.68% vs +3.0% after being too high for 1Q at +2.6% vs -0.3% (although they have been closer in most quarters prior to 2025)).

And another reminder, the model is “dynamic” and constantly updating itself (how it weights inputs, etc.) to become more accurate which result in “parameter revisions” (which are normally small, but Jan 9th saw an increase of +0.60%). This week no change.

Their Q1 2026 tracker was also unchanged at +2.74%, the highest since they started tracking in late November.

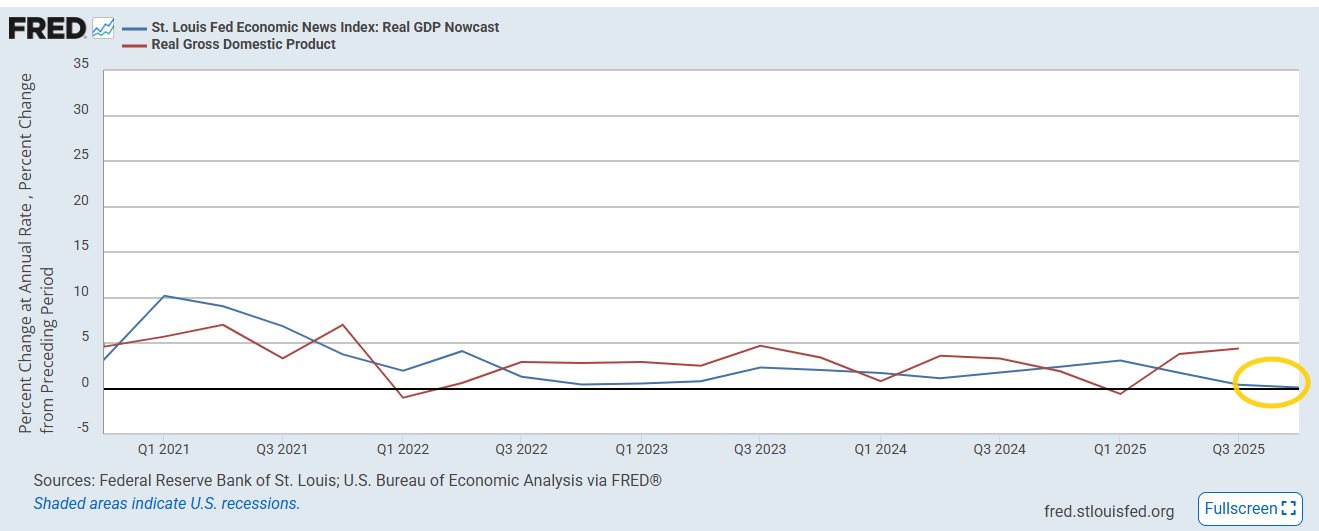

The St. Louis Fed 4Q GDP tracker continues to confound, and while other GDP trackers were stable or fell, it improved but to only +0.10% as of Friday from -0.04% the prior week but -1.46% three weeks ago. Unhelpfully they do not give a breakdown of the inputs.

The St. Louis Fed was a pretty good tracker pre-pandemic, but since Q2 ‘20 it has been much less so. For the just completed 3 Q they were by far the lowest of the trackers at +0.42%, nowhere in the vicinity of the 4.3% actual first estimate.

That dismal 3Q performance comes after undershooting 2Q ‘25 by -1.2% and overshooting Q1 ‘25 by +3.7%. It did though do well Q4 (and Q1) ‘24 but otherwise has been at least 1.5% off every quarter since Q2 ‘20, often by much more than that.

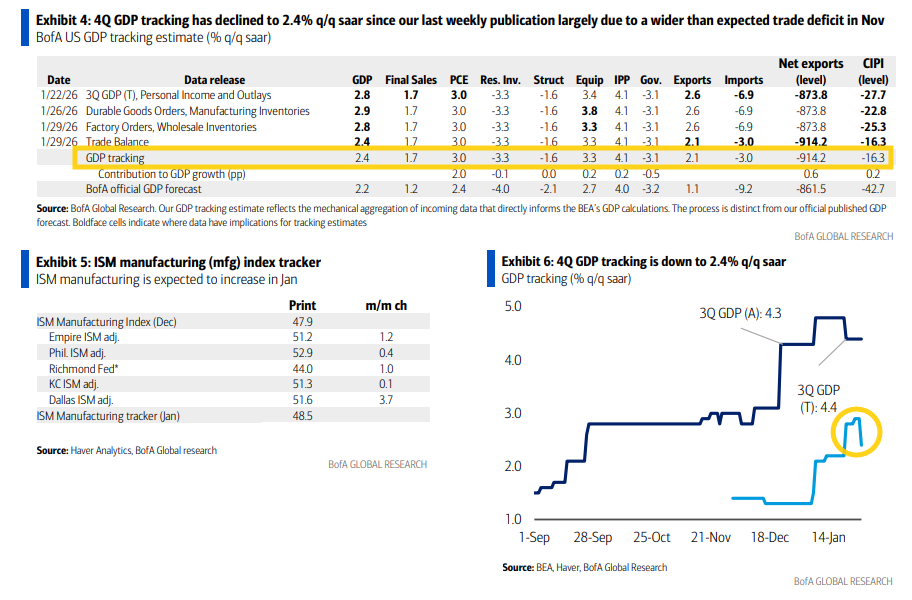

BoA sees their 4Q GDP tracker give back two-thirds of the prior week’s +0.6% jump (still up +1.0% the last month) to 2.4% as of Thursday. They see real final sales to domestic purchasers coming in at +1.7% (unch).

Here were the details behind the change if you’re interested in the granular detail:

“In the preliminary durable goods report for Nov, core capital goods orders and shipments came in higher than expected but along with some downward revisions to Oct core capital goods orders. Also, manufacturing inventories printed stronger than expected. On net, this increased our equipment investment and inventory accumulation tracking. In the Nov factory orders print, final core capital goods orders and shipments were revised down along with weaker than expected wholesale inventories. This led to a decline in our equipment investment and inventory accumulation tracking. Nov trade deficit widened more than expected, largely due to an increase in imports. Also, exports fell a little. On net, this decreased our net exports tracking estimate.”

As a reminder their tracker was 1.2% low for 3Q vs the first estimate and 0.8% low for 2Q ‘25 GDP, a tenth high for 1Q, right on for 4Q ‘24 GDP & two tenths high for 3Q ‘24.

Their official forecast was 2.7% for 3Q GDP (vs 4.3% first estimate) and is 1.4% for 4Q.

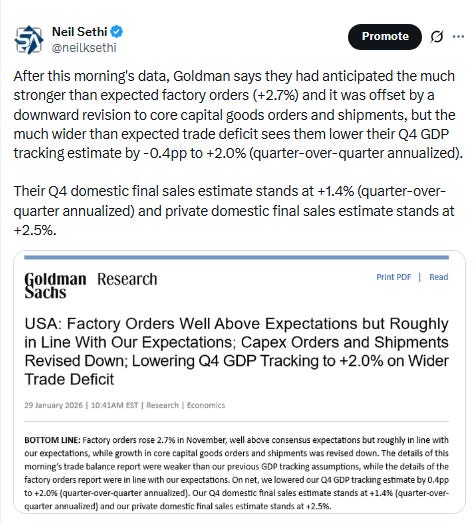

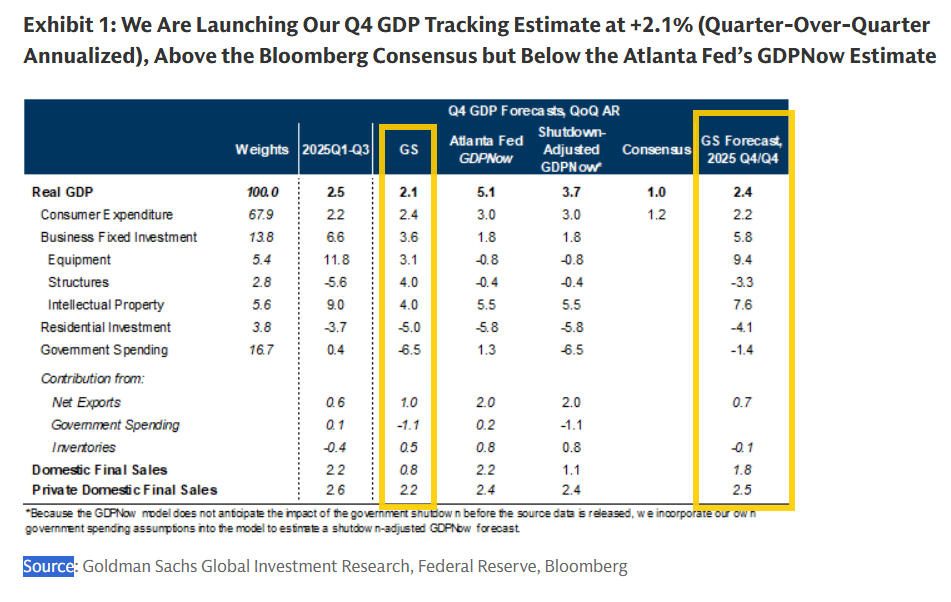

Goldman as of Thursday had also dropped their 4Q GDP tracker four tenths to +2.0% (Q/Q SAAR) with private domestic final sales growth though increasing a tenth to +2.5%.

Goldman’s official “house forecast” is for +2.4% GDP with +2.5% private domestic final sales growth (last column).

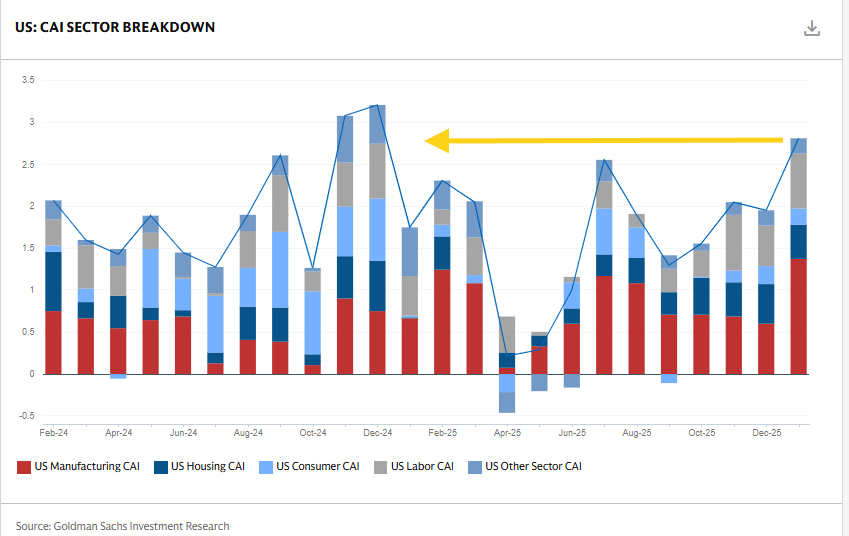

Goldman’s Dec US Current Activity Indicator* remained at +2.8% the highest since Dec ‘24.

*The CAI is their “real-time measure of inflation-adjusted economic momentum using 37 inputs.”

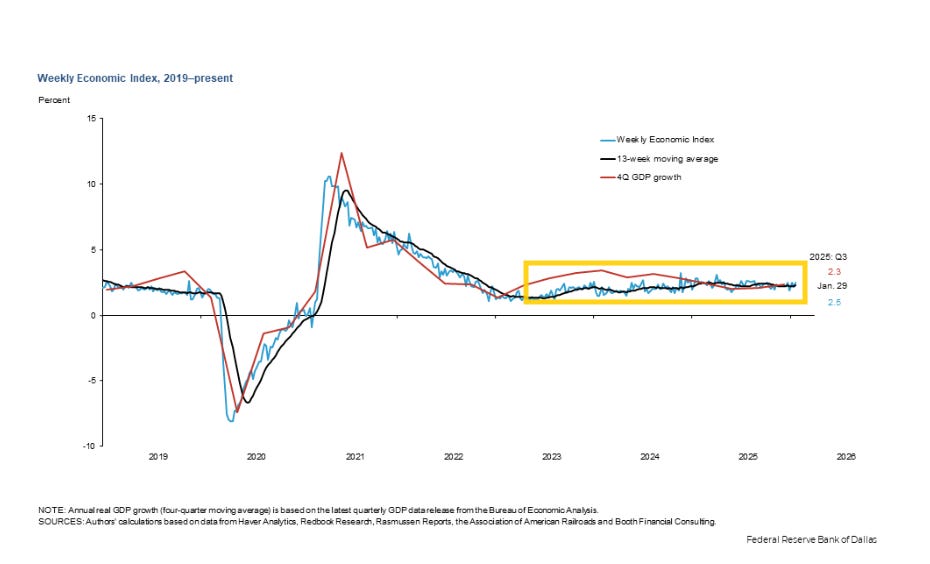

The Weekly Economic Index from the Dallas Fed* in the week through Jan 24th jumped +0.33% to 2.49% (after the prior week was revised -0.18% lower), remaining in the 1.49 - 2.79% range it has occupied since 2022 only poking above a couple times (most recently Apr 5th).

This series has become one of my favorites as it has a high correlation with actual GDP (see chart and note the recently released Q3 GDP report showed y/y GDP at 2.33%, right in line with this index) and has consistently indicated no recession and relatively healthy growth since the pandemic (which is what we’ve seen). It was referenced in November by Dallas Fed Pres Laurie Logan as support for her contention that the economy “remains solid”.

Importantly, the 13-wk avg is at 2.26% (down a bit from the 2.53% reading May 3rd, which was the best since 2022, but still a very healthy reading), continuing to evidence economic momentum that is slightly above trend.

*The WEI is scaled as a y/y rise for real GDP (so different than most GDP trackers which are Q/Q SAAR) and uses 10 daily and weekly economic series but runs a week behind other GDP trackers.

https://www.dallasfed.org/research/wei

Other economy stuff:

Valuations

Like the other sections, I’ll just post current week items regarding the multiple. For the historical stuff, see the Feb 4th blog post.

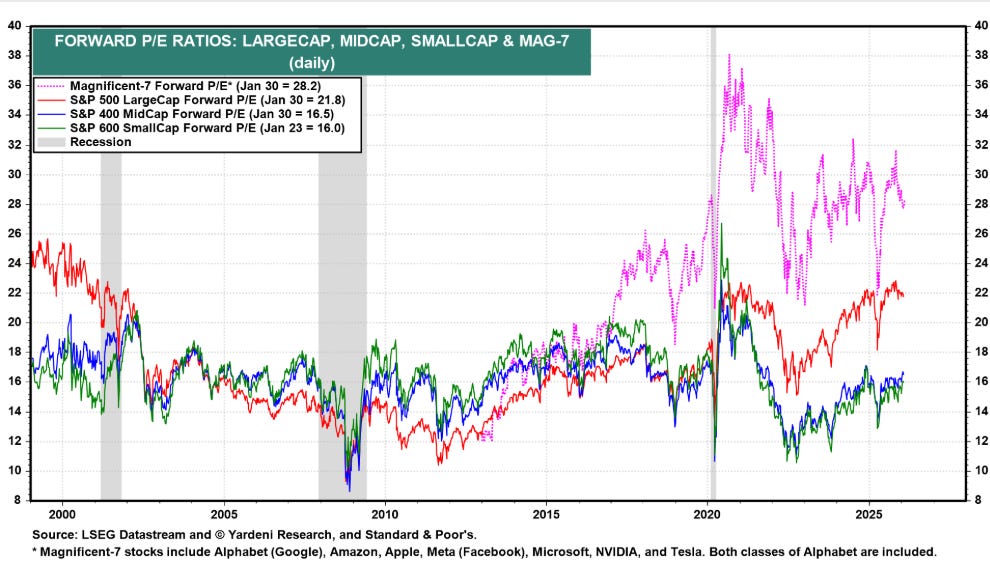

I would have thought P/E’s would have fallen w/w with the improvement in earnings expectations and flat to down weeks in the indices, but all four that Yardeni tracks were unch w/w other than the Mag-7 which edged higher:

-The SPX forward P/E (red line) remained at 21.8 (-1.8pts from the highest since 2001 on Yardeni’s model (which is a bit lower than most others (presumably due to the forward earnings calculation and earnings data source))).

-Mid-caps’ (blue, S&P 400) at 16.5 (-0.2pts from the highest since 2024 and -0.6pts from the highest since early-’21 (17.1)).

-Small caps’ (green, S&P 600 so higher quality than the Russell 2000) at 16.0 (the highest since early 2025 and -1.0pts from the highest since early-’21 (17.1)).

-Mag-7 (purple) though +0.4pts to 28.2, now up +0.5pts from the least since 1H ‘25 (but -2.8pts from the highest since 2024 (30.9)).

https://yardeni.com/charts/stock-market-p-e-ratios/

Other valuation stuff:

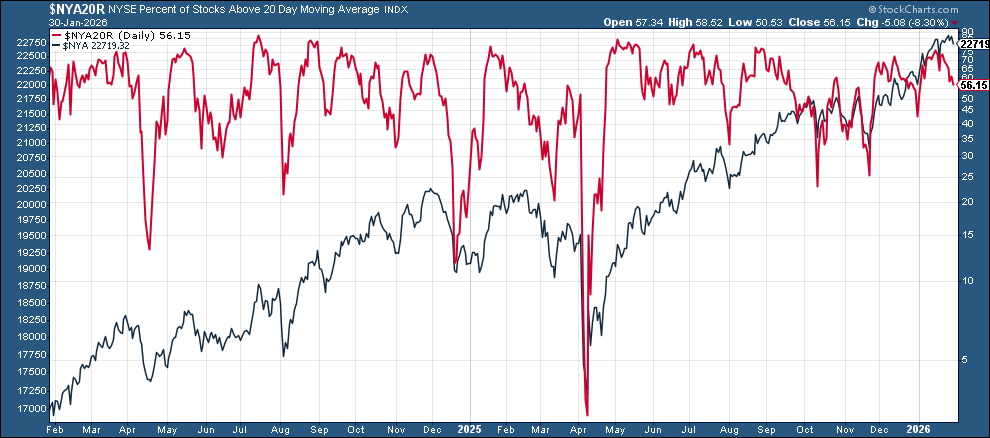

Breadth

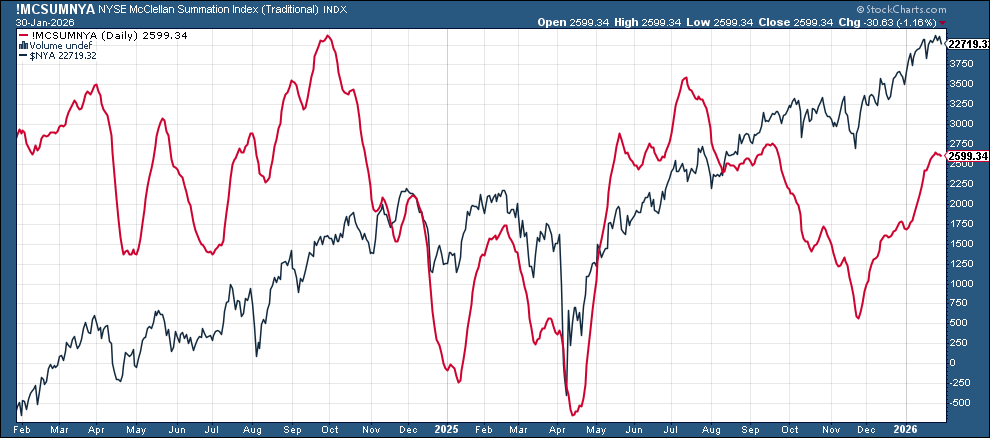

The McClellan Summation Index (“what the average stock is doing”) has started to roll over after getting to the highest since late Sept.

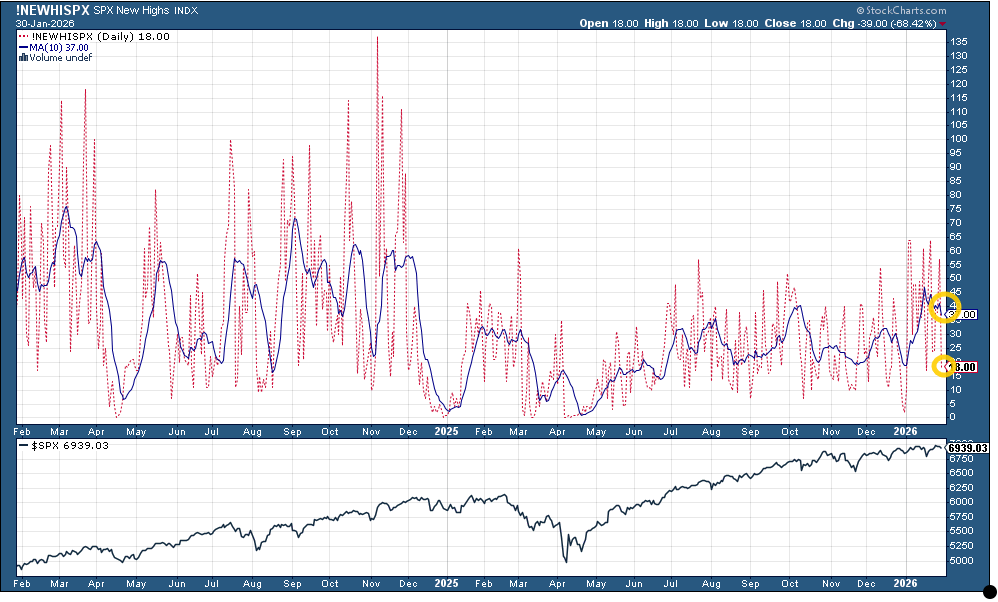

SPX new 52-wk highs (red dotted line) fell to 18 on Friday, the second least of the year down from 64, the joint highest since Nov ‘24, hit in the previous week.

Evidencing the overall weakness, the 10-DMA (blue line) has fallen back further from the 47 hit two weeks ago (the best since Dec ‘24) to 37, still though well above the 19 hit four weeks ago, which was the least since June.

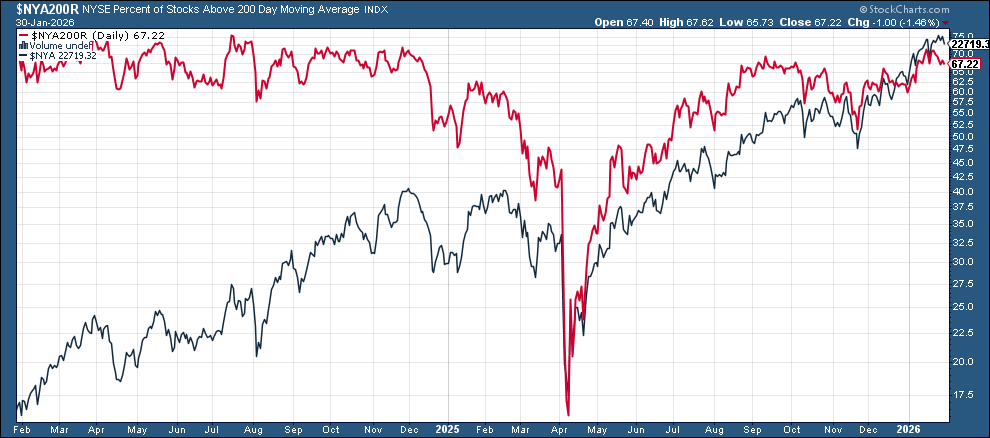

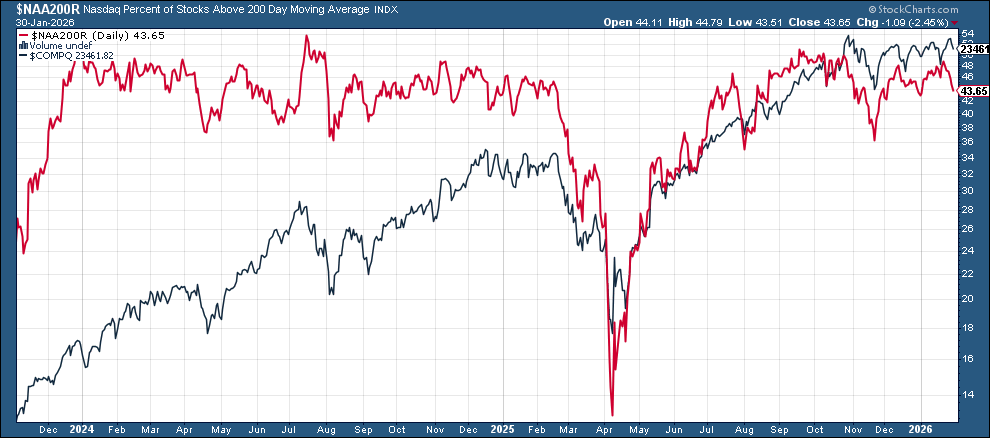

% of stocks over 200-DMAs (red lines), a gauge of stocks in longer term uptrends, after improving to over 70% for the NYSE for the first time since Dec ‘24 last week fell back under to 67%. The Nasdaq meanwhile saw a larger deterioration.

SPX though weaker than both.

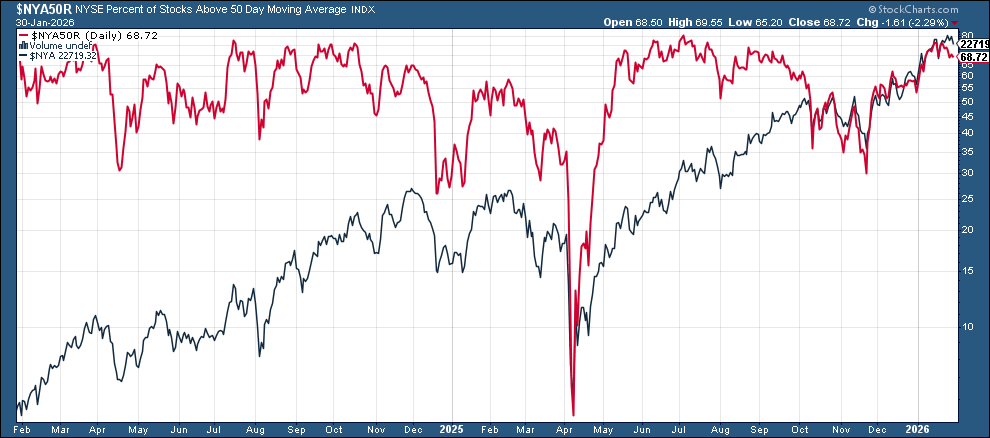

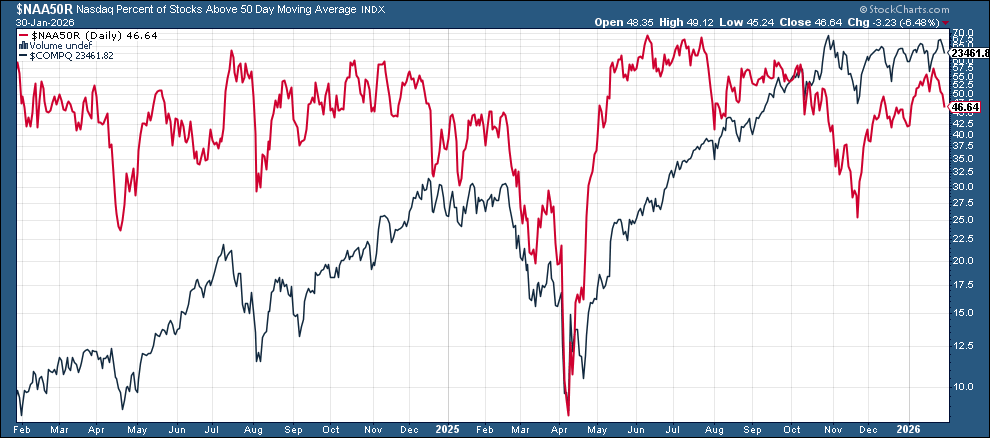

% of stocks above 50-DMAs (red lines), a gauge of stocks in medium-term uptrends, a similar story.

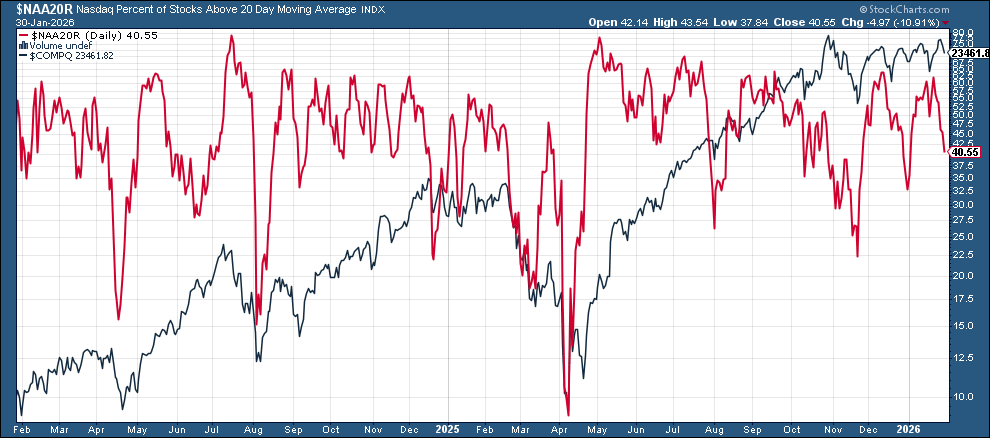

Shortening the lookback to % of stocks above 20-DMAs (red lines, indicative of equities in shorter-term uptrends) saw larger deterioration.

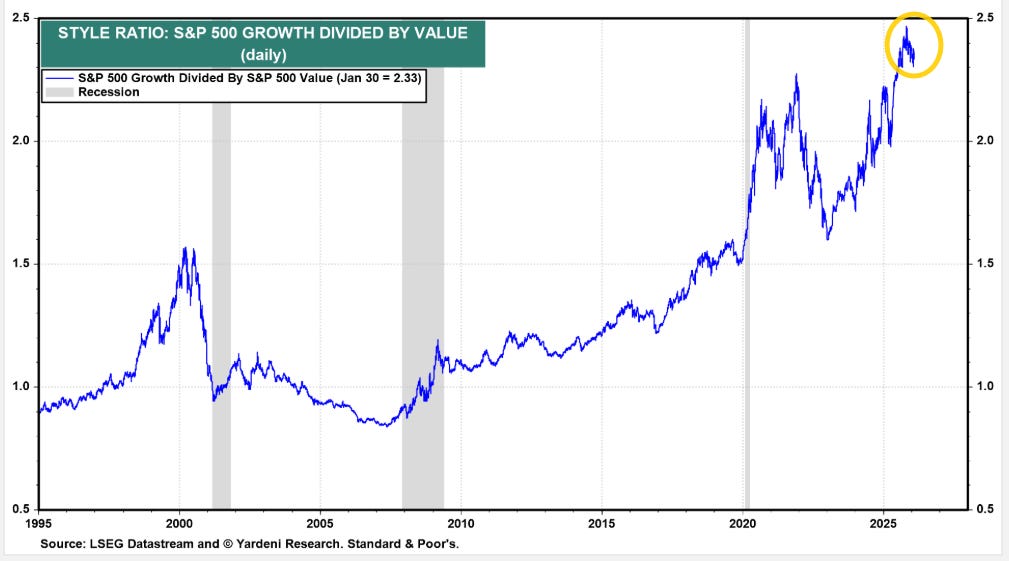

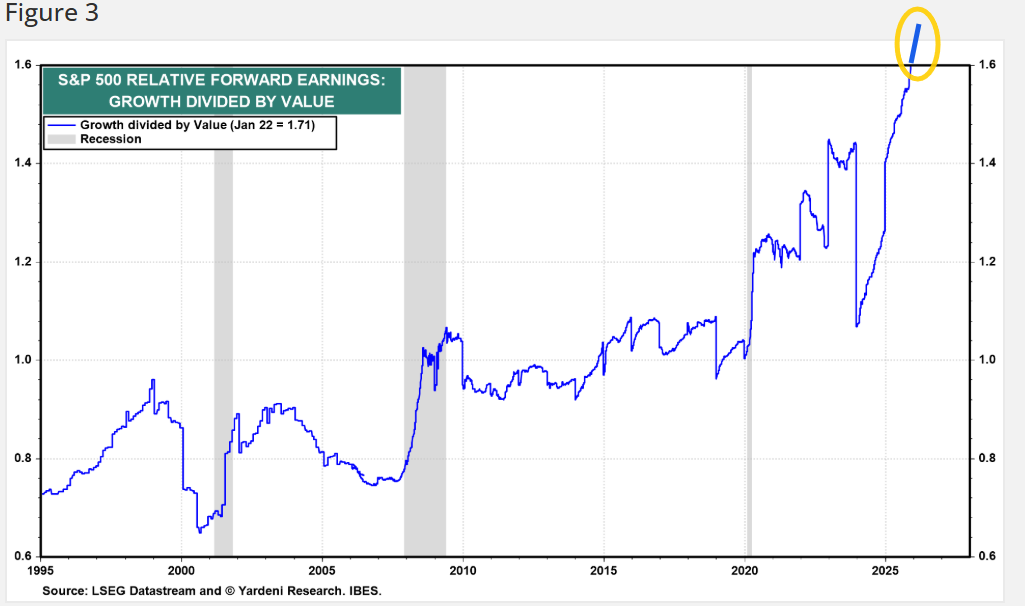

SPX growth/value fell back to the 5-mth low of 2.33 as of Friday, down from the highest since 1995 (2.44) the first week in Nov, but still up from around 2.0 to start 2025.

https://yardeni.com/charts/growth-vs-value/

The softening in the growth/value SPX ratio comes even as the relative forward earnings of growth vs value pushed to a new record high (1.71 as of Jan 22nd), further off the chart. That is up from 1.0 Jan 2020.

Equal-weighted SPX vs cap weighted ratio remained under its downtrend line from the start of its drop from the Jan ‘23 peak (which was a 3-year high (the all-time high was in 2015)).

IWM:SPY (small caps to large caps) have fallen back after breaking the downtrend line from the local peak in 2021 and making it to the highest since Dec ‘24 two weeks ago.

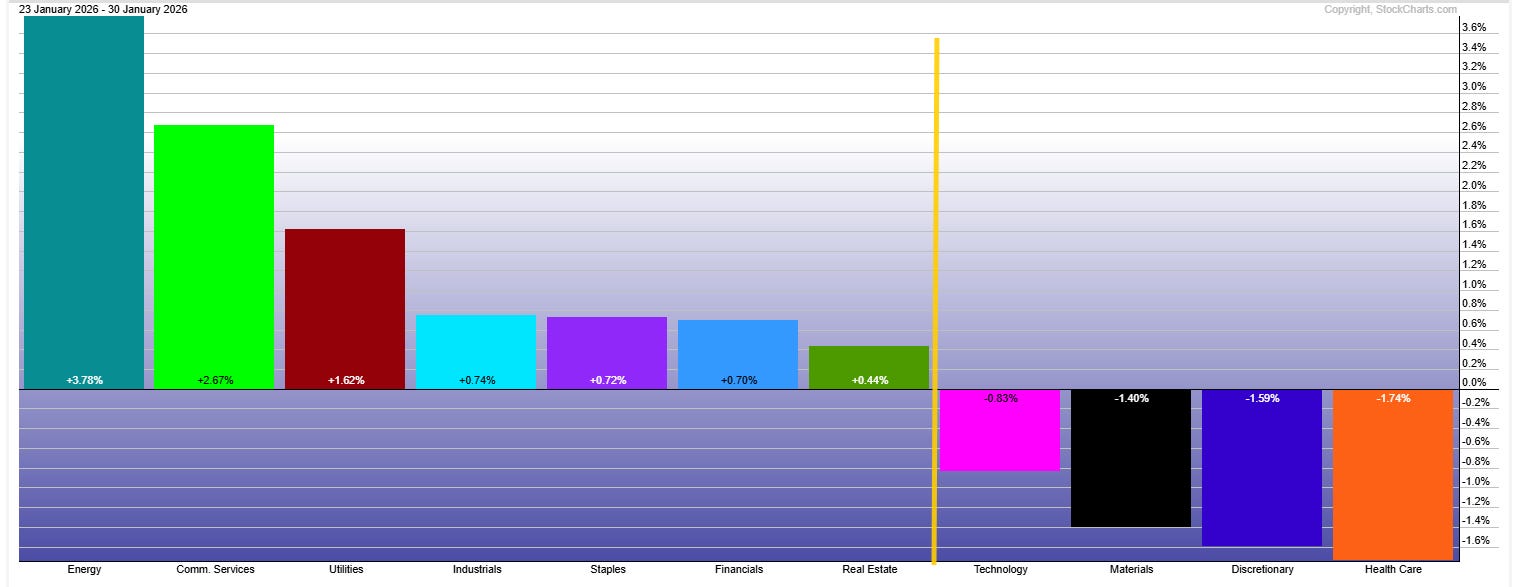

SPX sector breadth improved in terms of the number of positive sectors, but the average moves last week were a little less. Still just five sectors moved less than 1% after two the prior two weeks.

On the positive side, 7 of 11 sectors higher (up from 6 the prior two weeks but down from 10 the week prior to that which was the most since Nov), with again two up over 2% (after five the two weeks before last week but none the week before that), and again one up at least +3% (down from three and two the prior two weeks).

Energy remained in first place +3.8% (after +3.2% the prior week) which took it to an ATH for the first time since 2014. Comm Services +2.7% was second after third the prior week +1.6%.

On the negative side, three sectors were down at least -1% (from four the prior week but one the week before that), although none down at least -2% (after two the prior two weeks). Three though down -1% or more (vs four the prior week) led by Health Care -1.7%.

Weekly stock-by-stock chart from @FINVIZ_com looks much like a reverse image of the prior week with the exception of Energy remaining quite green.

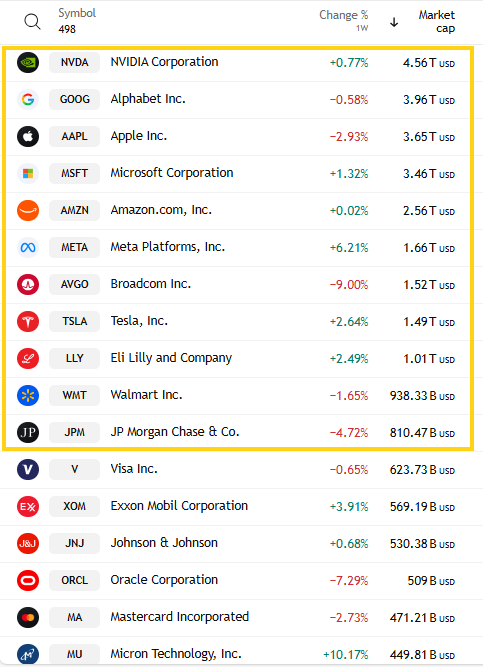

Looking at the top 11 stocks by market cap, eight were higher (up from six the prior week) led by META for a second week +8.8% (after +6.2% the prior week but -5.0% the week before that). Leading to the downside was MSFT -7.7%.

2026 winner SanDisk SNDK leads for a second time this year (and it was second the prior week) +21.6%, now up +173%(!) this year. It was one of twelve stocks up at least +10% (up from four and 11 the prior two weeks but 22 the week before that).

~50 SPX components were up over +4%, about the same as the prior week down from ~120 the the week before that, which was the most since Nov. Over a third of those were >$100bn in market cap (up from the prior week but matching the week before that) in VZ, TXN, T, GEV, META (again), LMT, PEP, CVX, ETN, TMUS, CSCO, CAT, IBM, XOM, GILD, GE, SUK, WFC (in descending order of percentage gains),

On the other side Humana HUM, led decliners -26.8%, one of 17 SPX components down over -10% (up from two the prior week and 11 the week before that).

~100 SPX components were down -4% or more (up from 50 the prior week and 70 the week before that), with 18 >$100bn in market cap (after 14, 4, 11, 0 the previous four weeks) in UNH, PLTR, NOW, INTU, APP (for a third week), NEM, AMD, TMO, BA, ORCL, CRM, ACN, SBUX, KKR, KLAC, BX, APH, COST (in order of percentage losses).

Other breadth stuff:

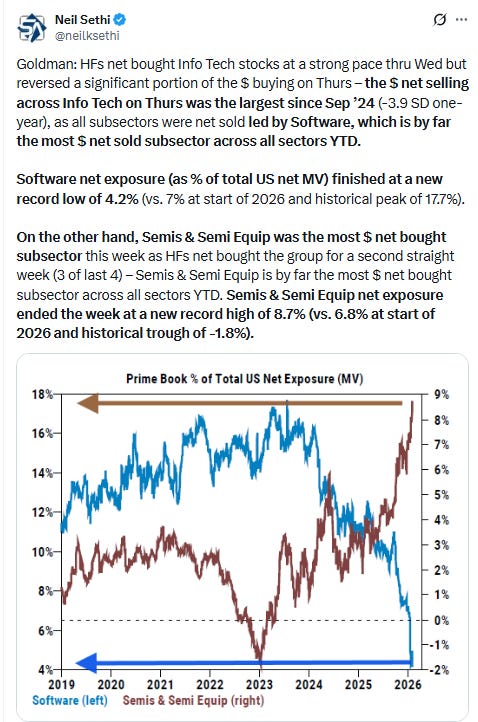

Flows/Positioning

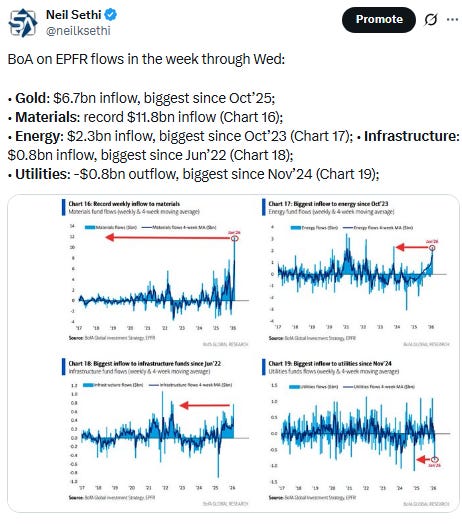

EPFR from the Flow Show:

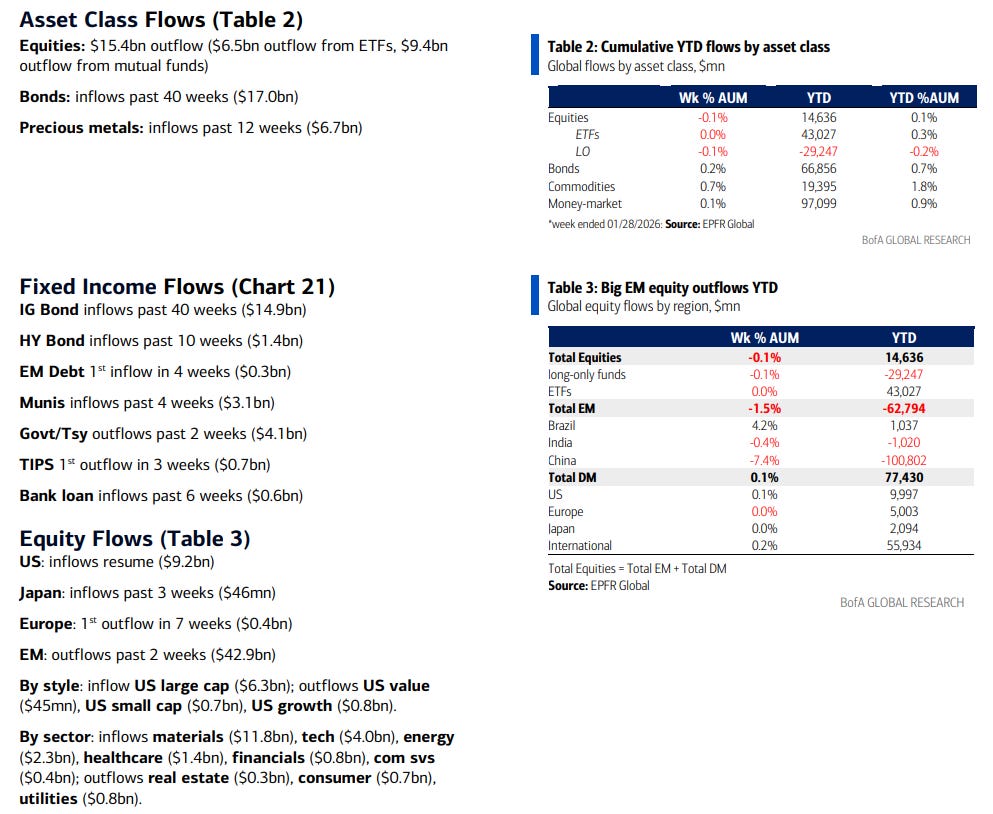

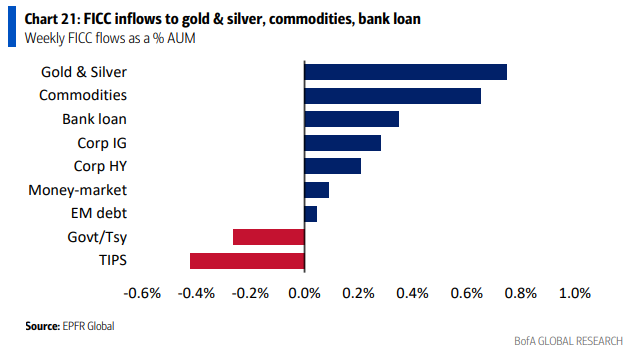

EPFR FICC flows in the week through Wed saw Gold/Silver and Commodities remain in the top three spots (where they’ve been almost every week for the last couple of months) at first and second with +0.8% & +0.7% of AUM.

Bank loans fell back one spot to third but remained in the top 3 for a third week although falling back to +0.4%.

Rounding out the inflows were Corp IG, then Corp HY, MMFs (those three in the same order as the prior week) and EM debt (which had finished in the bottom two with outflows the prior three weeks).

Seeing outflows were Treasuries and TIPS (the latter after two stronger weeks of inflows).

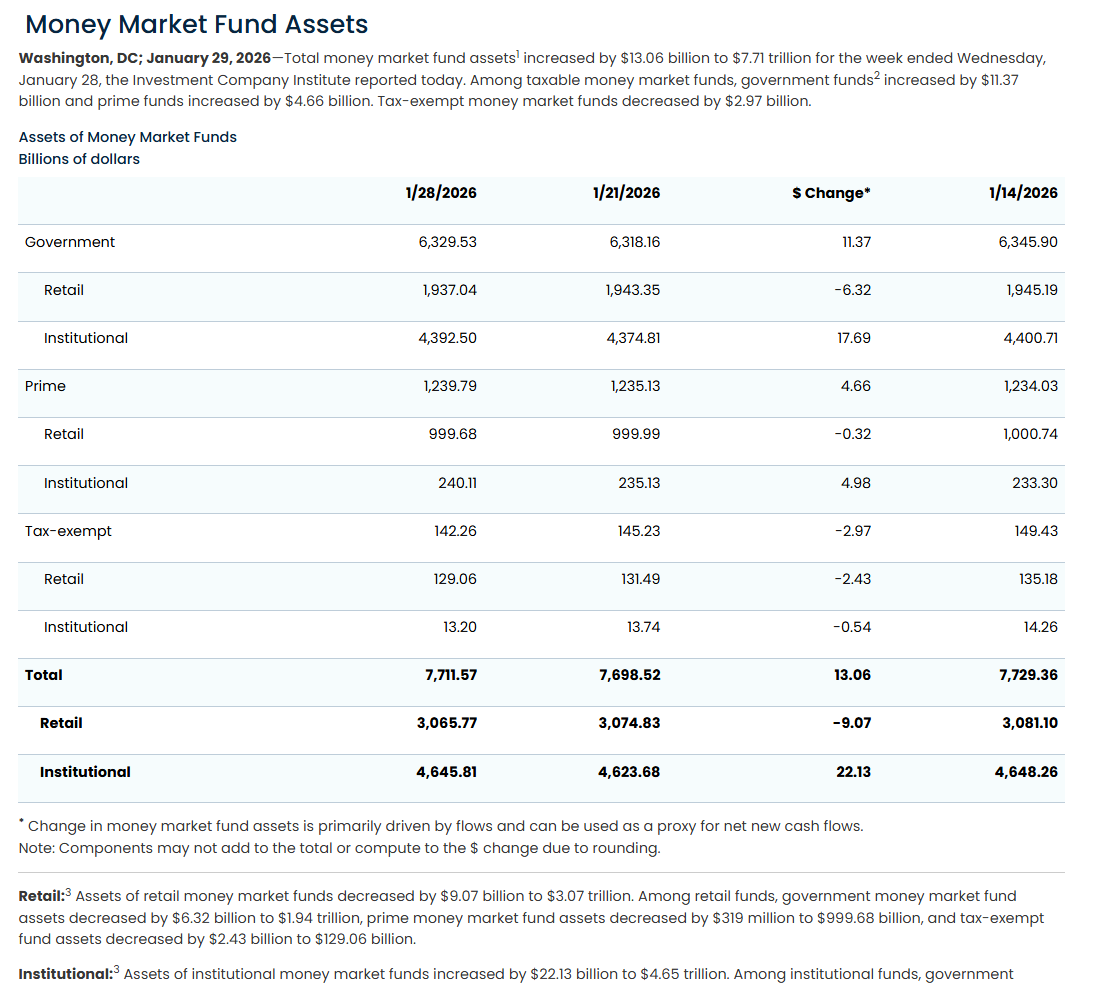

ICI data on money market flows in the week through Jan 28th like EPFR saw a modest (+$13.1bn) inflow into MMFs, but still the largest since the start of the year after -$105.5bn the prior two weeks (the largest outflows in at least 20 weeks (I haven’t been keeping a record of this that long), which left the YTD total at -$21.7bn.

Institutions (who hold ~60% of MMF assets), saw all of the inflow this week (after having led outflows the prior two weeks but inflows for 7 of the 8 weeks prior to that), at +$22.1bn now -$9.9bn YTD (but +$437.8bn last 20 weeks).

Retail though saw outflows for a third week -$9.1bn taking three-week outflows to -$34.4bn, now -$11.8bn YTD but +$99.0bn the past 20 weeks).

Total MMF assets are now $7.71tn down from a record $7.80tn Jan 7th.

https://www.ici.org/research/stats/mmf

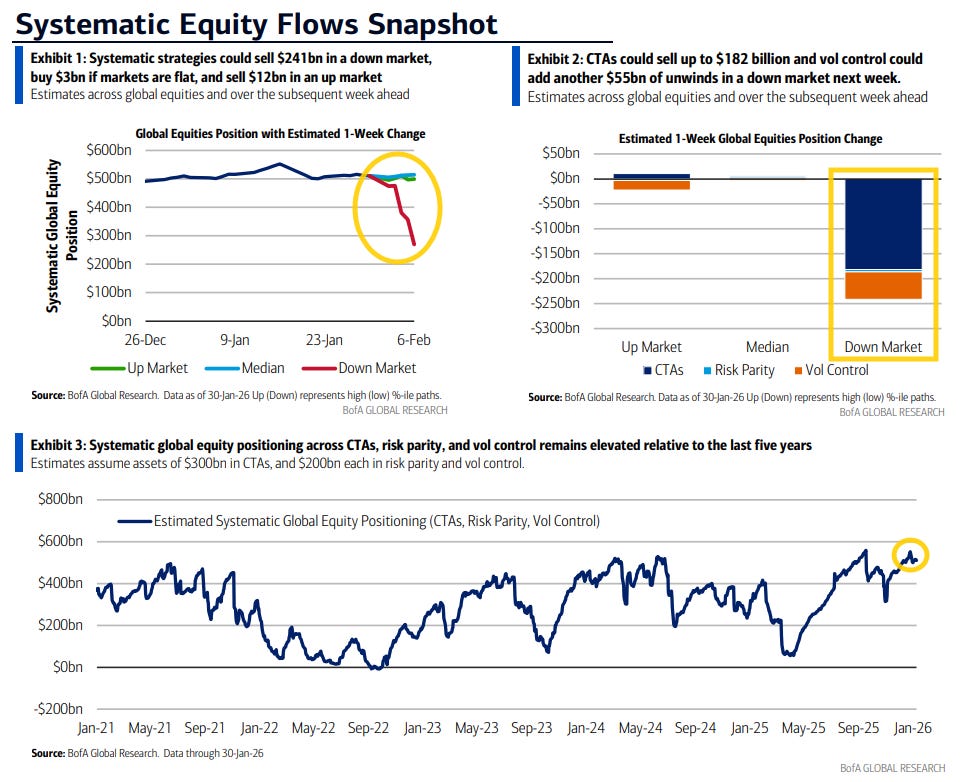

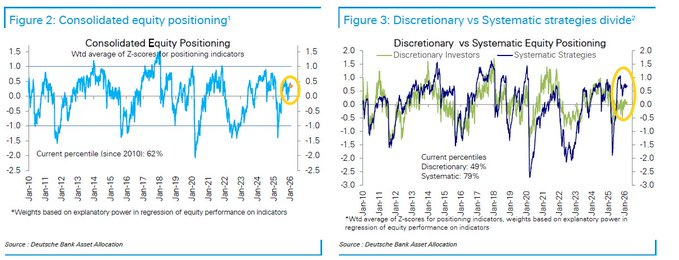

On combined systematic strategy positioning, BoA doesn’t comment directly on their charts, but as a reminder last week I said volatility increased, and as one might expect given that set-up, systematic positioning was dialed back, although remaining for now not far from those 5-year highs. That remained the case this week with not much change in systematic positioning.

But as I said “that also increases the sensitivity to further volatility, particularly to the downside, leading to the most asymmetric modeling since late October before that pullback.” That actually increased this week.

In that regard, BoA estimates just +$3bn of buying in a flat market (down from +$19bn two weeks ago), and

-$12bn of selling in an “up” market due to the volatility increase (”up market” defined as 97.5 %ile price path or ~+3.5% similar to Goldman)), and

-$241bn selling in a “down” market, up from -$169bn two weeks ago (”down market” defined as the 2.5 %ile price path or ~-2.9% (different than Goldman who uses --4.5%)).

CTAs still dominate the selling in a down market (due to both increased volatility but more importantly breaking sell triggers) representing -$182bn of the -$241bn in combined estimated selling, but as noted two weeks ago vol control has become a larger piece and would add -$55bn, the most since they switched to this new format, with risk parity the rest.

DB on positioning:

Our measure of aggregate equity positioning was trimmed this week, but remained modestly overweight (0.33sd, 62nd percentile).

Discretionary investor positioning (0.05sd, 49th percentile) declined slightly towards neutral but continued to be in the cautious range it has been in over the last 11 months.

Systematic strategies positioning (0.67sd, 79th percentile) was also pared slightly but remained overweight.

Tier1Alpha says overall systematic positioning remains just above the average level since 2011 with no major changes expected absent a change in volatility:

Systematic Funds, including Vol Control, CTA, and Risk Parity strategies, are maintaining their current exposure to equities. In a stable volatility environment, these strategies are unlikely to make significant adjustments to positioning. However, if volatility rises, some modest deleveraging may occur, while contained volatility would limit additional buying.

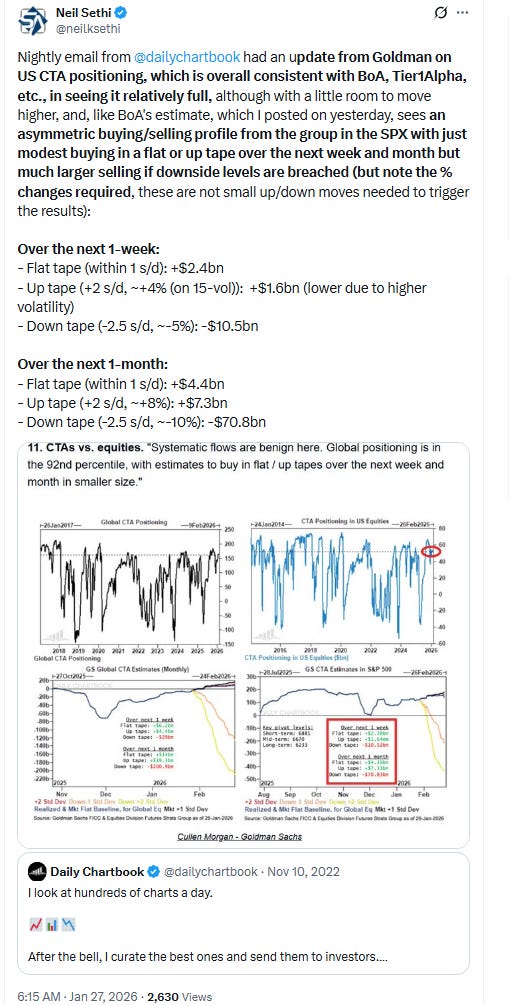

Looking more specifically at CTA (systematic trend follower) positioning in the US indices, BoA says:

“With the capitulation of CTA gold longs, the beta of trend following frameworks to global equities will rise given the elevated longs across regions, especially among medium- to long-term trend followers. CTA equity position sizes were little changed this week, but declines did bring stop loss triggers closer. Short-term frameworks could sell equities on weakness next week, but longer-term trend followers will maintain a greater focus on changes in volatility as price trends remain elevated.”

As a reminder, BoA now looks at bullish, flat, and bearish price paths (which are based on price trend vs moving averages), but also in short, medium, and long term price trends.

So interestingly, BoA seems to be saying with the recent losses on gold longs and yen shorts, CTAs will be “tightening up” their stop losses across markets which mean it will take less of a decline to hit stop loss triggers This means they see a -2% or so decline as getting to the first level of sell triggers on US indices vs -3% or more previously. As a side note, we continue (as we have since early December) to see only the shortest price trend CTAs not yet having brought their positioning back up to the levels from early Nov (ex-RUT which is back to those levels) which leaves less room for CTAs to add per the systematic positioning summary (and BoA notes could even be sellers on any sustained equity weakness).

They don’t therefore provide buy levels (as buying is more dependent on lower volatility than higher prices) but they see the first layer of sell triggers at 6792, 25203, and 2557 on the SPX, NDX, and RUT respectively.

DB sees CTA equity positioning at the 82nd %ile to 2010 up from the 73rd %ile three weeks ago. In terms of the US though, long positioning remained at the 64th %ile for a third week (up though from 54th three weeks ago) with the SPX at the 63rd (from 55th three weeks ago), RUT at the 63rd (53rd), and NDX the 55th (46th), so seeing more room to expand than BoA models.

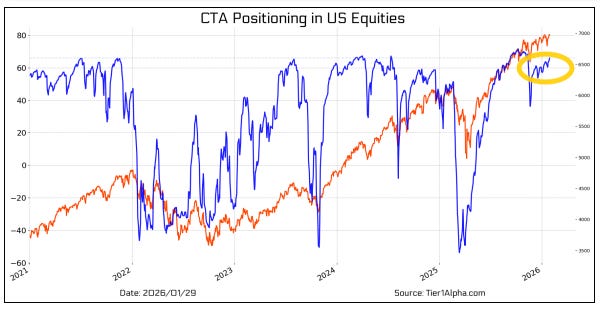

Tier1Alpha sees CTA positioning in US equities more in the mode of BoA closer to full positioning.

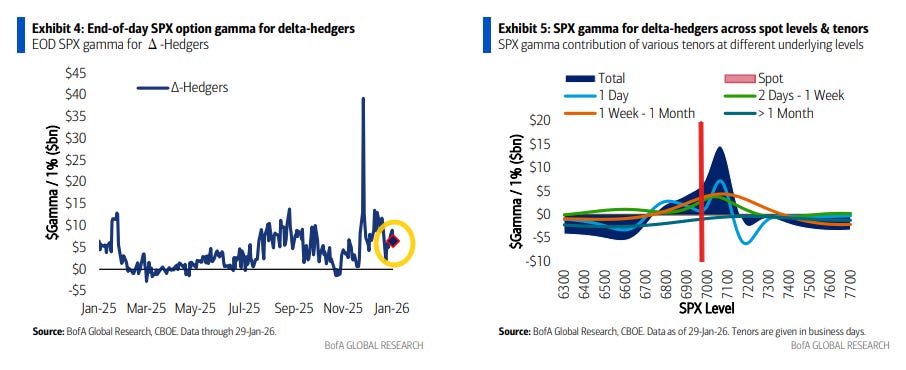

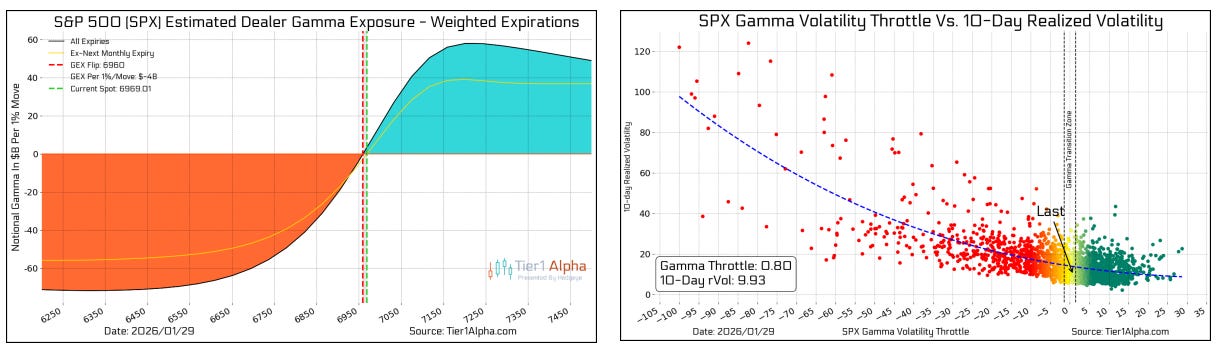

BoA on SPX gamma:

“SPX dealer gamma was supported this week with an average level of +$7.9bn continuing the trend of notably higher gamma, so far, in 2026 (avg. of +$8.6bn YTD) compared to 2025 (avg. of +$3.6bn). As of Thursday’s close, SPX gamma was moderately long at +$6.5bn (76th 1y %ile). The current gamma curve suggests there is material room for gamma to grow if equities climb to new all-time-highs near term. Though, as is the norm, if the S&P falls next week then gamma is likely to decline as well and would flip negative roughly 3% lower from here (at a level of ~6740).”

So like Goldman BoA sees gamma as ending the week at a relatively high level (at least as compared with the past year which has been relatively low), which should provide some cushion to volatility, although as they note it falls off relatively quickly to the downside, turning negative at the 6740 level (where dealers have to “chase” moves), so seeing volatility growing with downside moves and increasingly softening with upside moves to around the 7100 level.

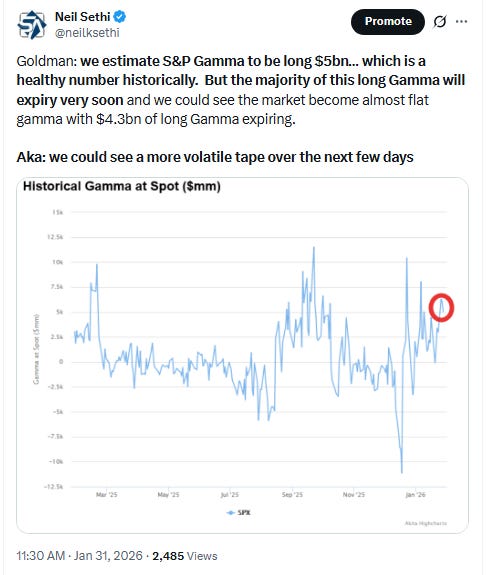

Tier1Alpha though sees gamma a little differently:

SPX has drifted back into a neutral gamma regime, which means dealer hedging flows are likely to be less supportive.

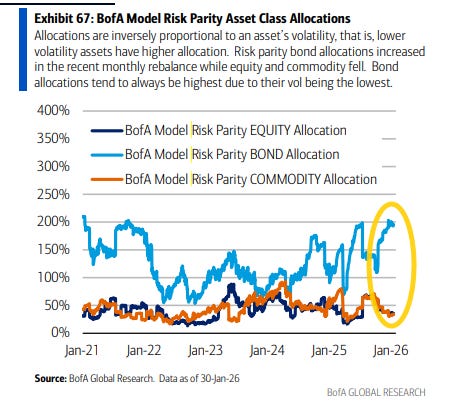

BoA’s estimate of risk parity positioning (which they estimate at around $200bn of AUM at max exposure) continues to see the leveraged exposure to bonds at around the highest since 2021, while the stock and commodity exposure remains around average levels since then.

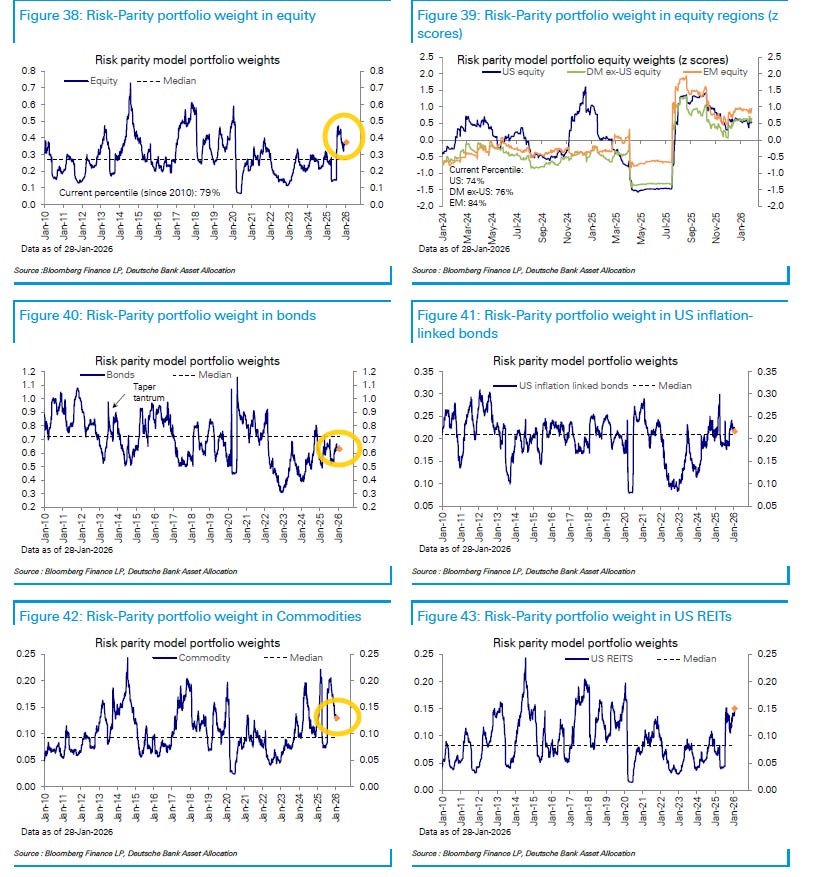

DB models risk parity funds (est ~$250bn in max AUM) much differently than BoA with the equity allocation at the 79th %ile (from 76th the prior week) and commodities the 77th (from 75th) but bonds at just the 35th (from 41st) (although the charts don’t look quite in line with that):

Risk-parity funds’ overall equity allocation increased this week (79th percentile), driven by increased allocation to the US (74th percentile), other developed markets (74th percentile), and EM (84th percentile). Their allocation to bonds (35th percentile) and inflation-protected notes (58th percentile) was trimmed, while allocation to commodities (77th percentile) rose modestly.

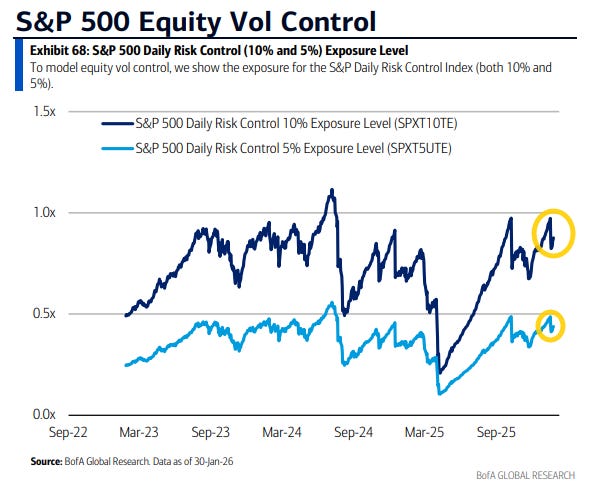

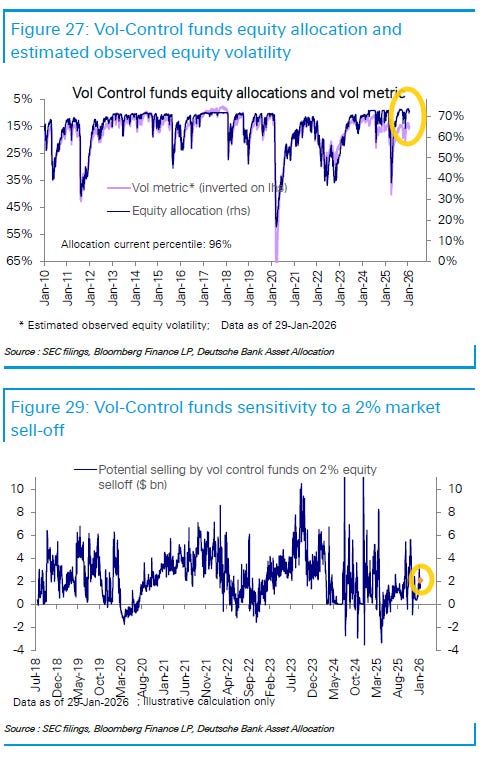

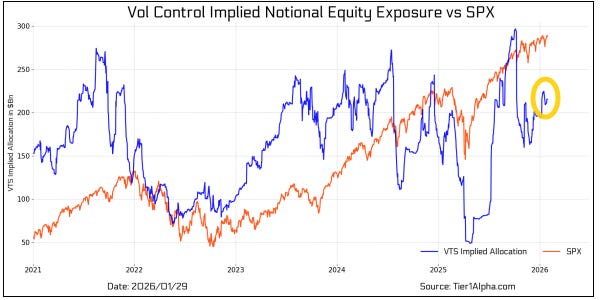

BoA models some buying last week by vol control funds (which they estimate at around $200bn of AUM) which saw their positioning edge up overall though not far from the 2025 peak.

DB sees vol control funds “slightly below their historical maximum allocation (96th percentile)”, and their sensitivity to market selloffs “relatively low.”

While Tier1Alpha models less buying from vol control funds last week but also had seen less selling the prior week.

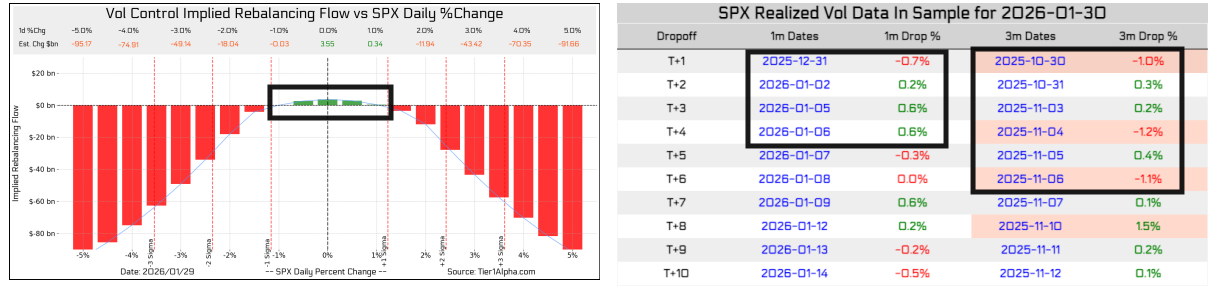

And there is some scope for buying expansion from vol control funds as we drop 1.2%, 1.1%, and 1.0% days (the last was Friday) out of the the 3-month lookback (which is “the new rebalancing toggle,” as it has moved over the 1-month). There is nothing greater than a 0.7% day though falling out of the 1-month.

For example, this resulted in around $5bn of buying on Friday when the 1% day dropped off. 2% or greater moves continue to see large selling modeled.

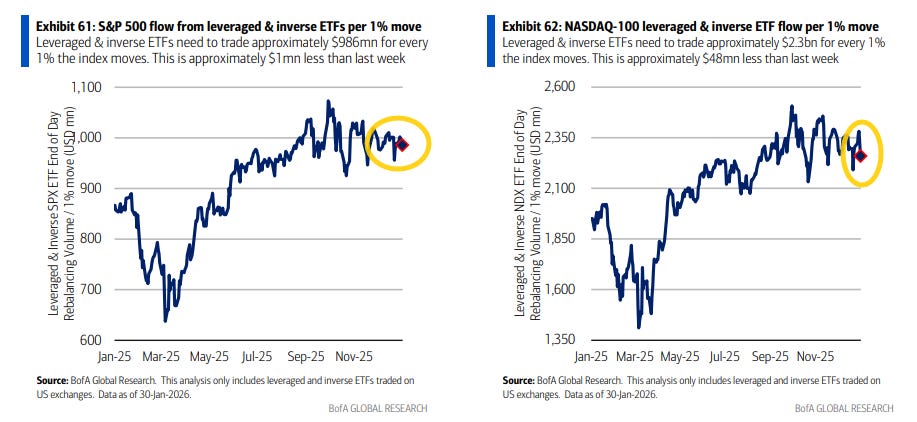

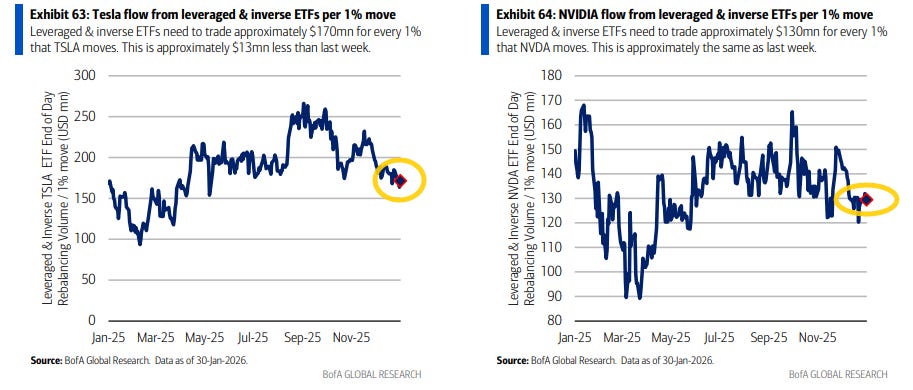

I like to look at the impact of moves in leveraged ETFs on the overall market as a barometer of risk appetite (the greater the impact, the more investors have in these ETFs which I think of as “higher risk”), and both SPX and NDX leveraged ETF AUMs fell back last week although remaining in their recent ranges and overall much closer to the highs of 2025 than the lows.

Remember, this is a “constant negative gamma” source as Charlie McElligott put it in a Oddlots appearance (meaning that there is double/triple buying pressure from them as they rebalance each day).

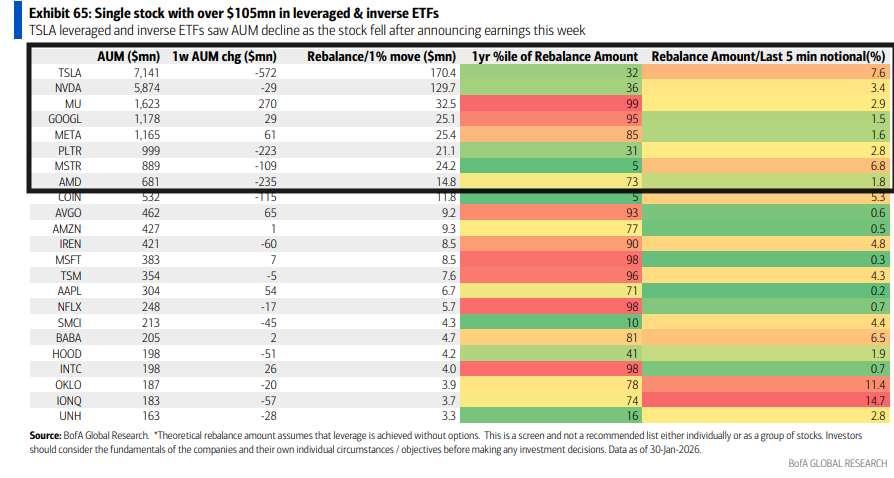

Looking at the two largest single stock ETFs, TSLA and NVDA, after bouncing some the previous week, both fell back last week with their AUM’s remaining around the least since May and June respectively. TSLA ETFs shed -$0.6bn in AUM to $7.1bn (32nd %ile over the past year), while NVDA leveraged ETFs dropped -$29mn to $5.9bn (36th %ile over the past year).

MU remained in 3rd (after jumping from 7th the previous week) adding +$0.3bn to take it to $1.6bn (100th %ile over the last year), but PLTR dropped back to 6th place from 4th the prior week as it dropped -$0.2bn (31st %ile) to +$1.0bn putting GOOG back in 4th +$29mn (95th 1yr %ile as the funds are relatively new).

META improved to 5th adding $61mn to $1.2bn (85th %ile) and MSTR (-$109mn) remained in 7th at $0.9bn (but just the 5th 1yr %ile). I noted last week you can now add AMD to the mix but that fell back dropping -$235mn to $681mn in AUM.

And after buybacks ended 2024 at record levels and started 2025 even better, they had by and large remained below seasonal averages from April until October when they seemed to have picked back up (depending on who you ask), but according to BoA and Goldman they accelerated into year-end and have continued to run at record levels on a nominal basis in 2026, although that is still just in line with the average since 2010 on a market cap weighted basis We are now starting to exit the buyback blackout window which will allow discretionary buybacks (~30% of all buybacks) to recommence.

And some other notes on positioning:

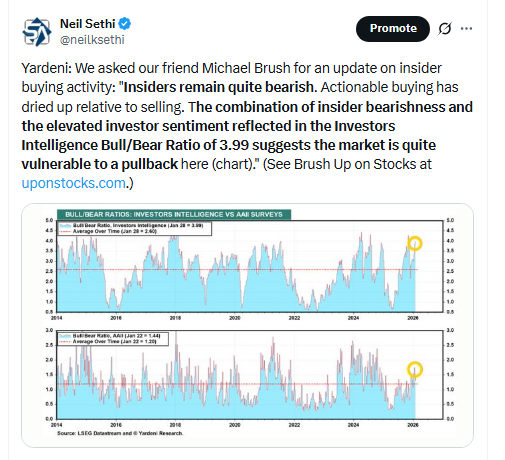

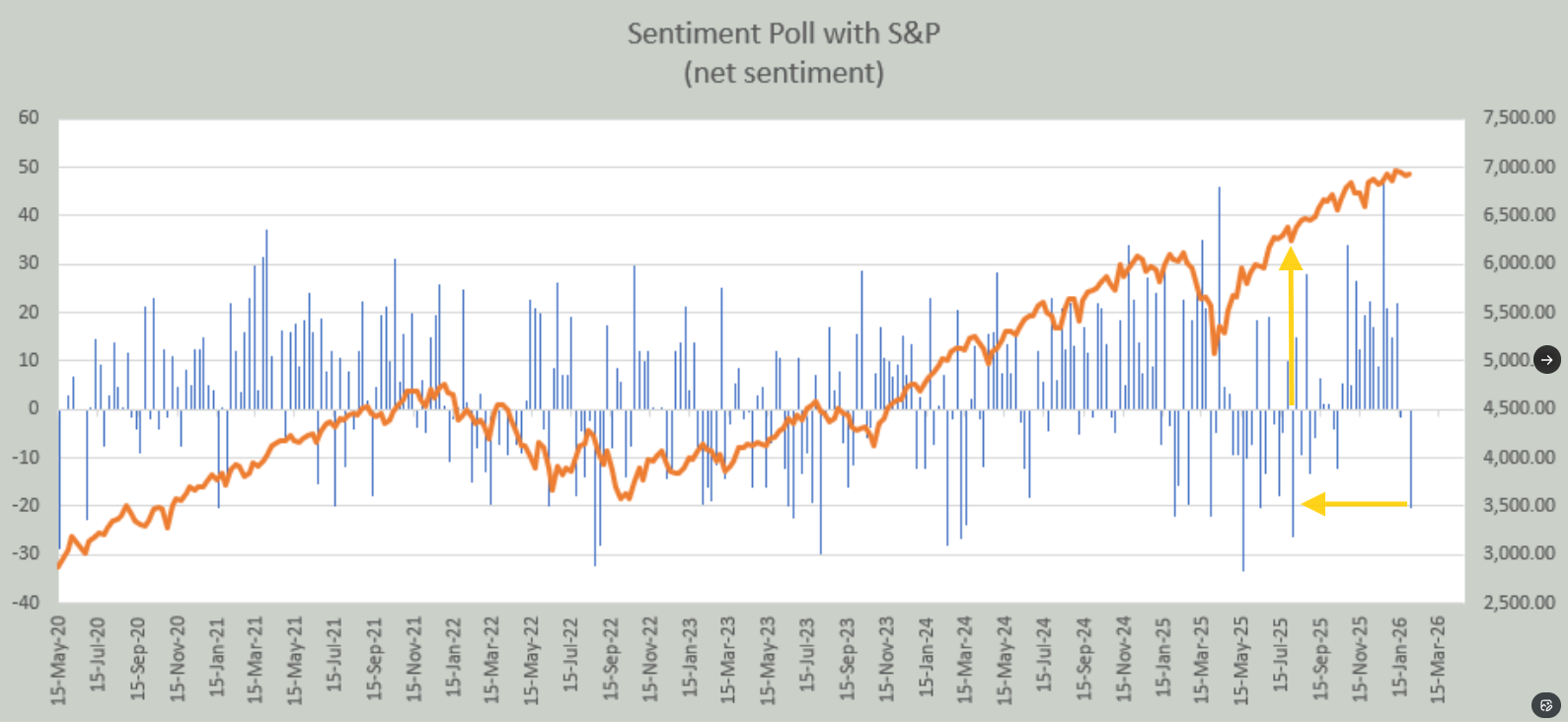

Sentiment

Sentiment (which I treat separately from positioning) is one of those things that is generally positive for equities when its above average but not extreme (“it takes bulls to have a bull market”, etc.), although it can stay at extreme levels for longer than people think, so really it’s most helpful when it’s at extreme lows (“washed out”).

After moving towards extreme bullish readings in later October before falling back along with the equity drawdown in November, with a couple hitting at or near extreme lows for the year at the end of November, as noted since then “like clockwork they have rebounded along with the equity recovery although only a couple are really anywhere near extreme levels.” This week we saw some of those that had softened move back to or nearer extremes (BoA’s new Bull/Bear indicator which hit the joint highest since 2021, the II Bull/Bear spread (see post below), and the put/call ratio which made a big move down (more bullish)). Otherwise things are mostly in that “above average but not extreme” area..

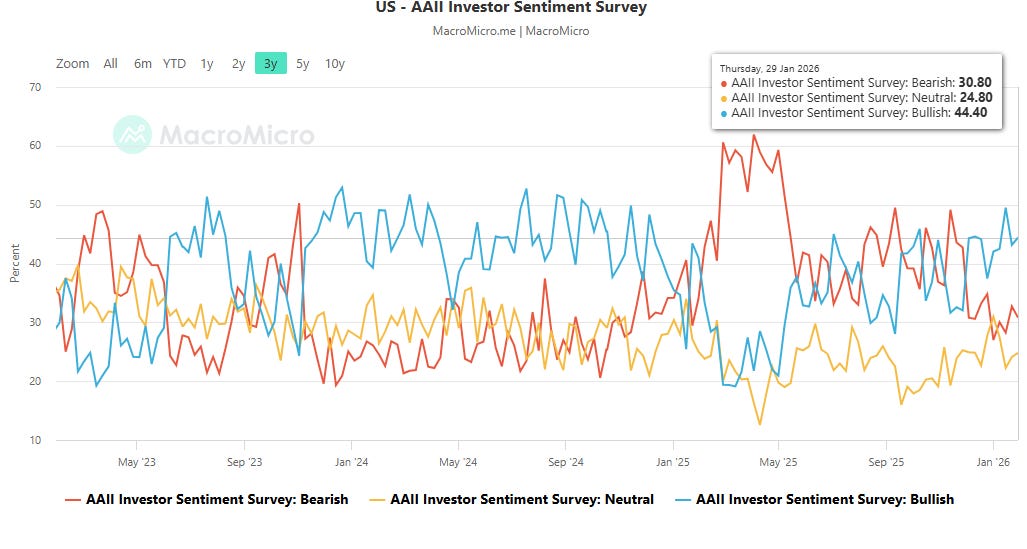

AAII a little more bullish but still below the widest bull-bear spread since Nov ‘24 seen two weeks ago:

AAII bulls (those who see higher stock prices in 6 mths, blue line) edged to 44.4% from 43.2% still down from 49.5% the week before that, which was the highest since Nov ‘24, remaining above the long-term historic average of 37.5% for a 5th week (and the 8th week in 9 (with the other week 37.44).

Bulls also remained above the level of the bears (who see lower stock prices in 6 mths, red line) for a 9th week, the longest streak since 2024, who edged down to 30.8% from 32.7%, which was a 4-week high, still above the 27.0% four weeks ago, which was the least since Oct ‘24. Bears also just back under the long-term average of 31.0% for the fourth time in five weeks (only though the 8th week since Dec 12, 2024).

The Neutral camp (yellow line) edged up to 24.8% from 24.1% and remaining under the long-run average of 31.5% for the 79th week in 81 (since July ‘24).

https://aaii.com/sentimentsurvey

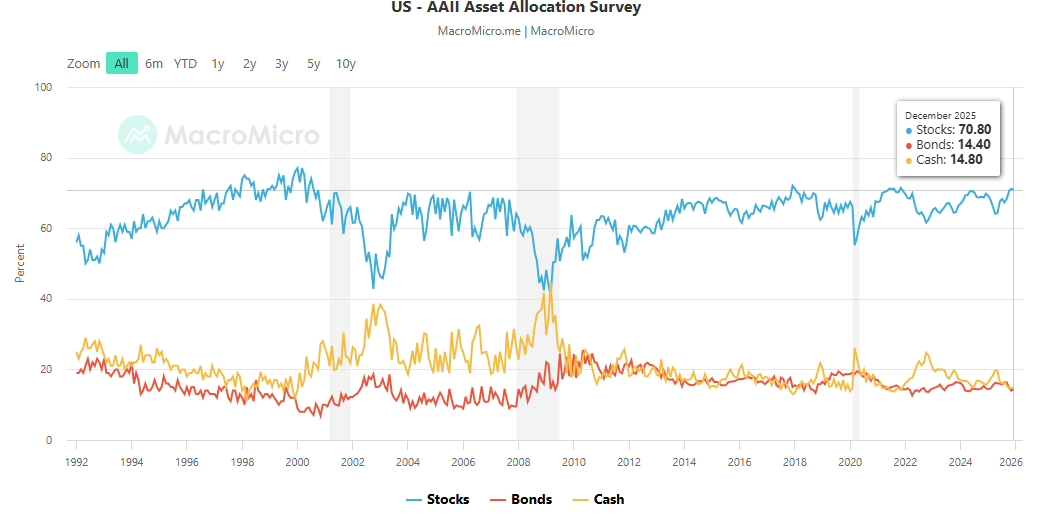

The AAII asset allocation survey saw the allocation to stocks edge down to 70.8% in December from 71.2% in Nov, which was the highest since Nov ‘21, moving into bonds which edged up to 14.4% from 14.0%, which was the least since May ‘24, while cash remained at 14.8%, a tenth off the 14.7% in Oct which was the least since Nov ‘21.

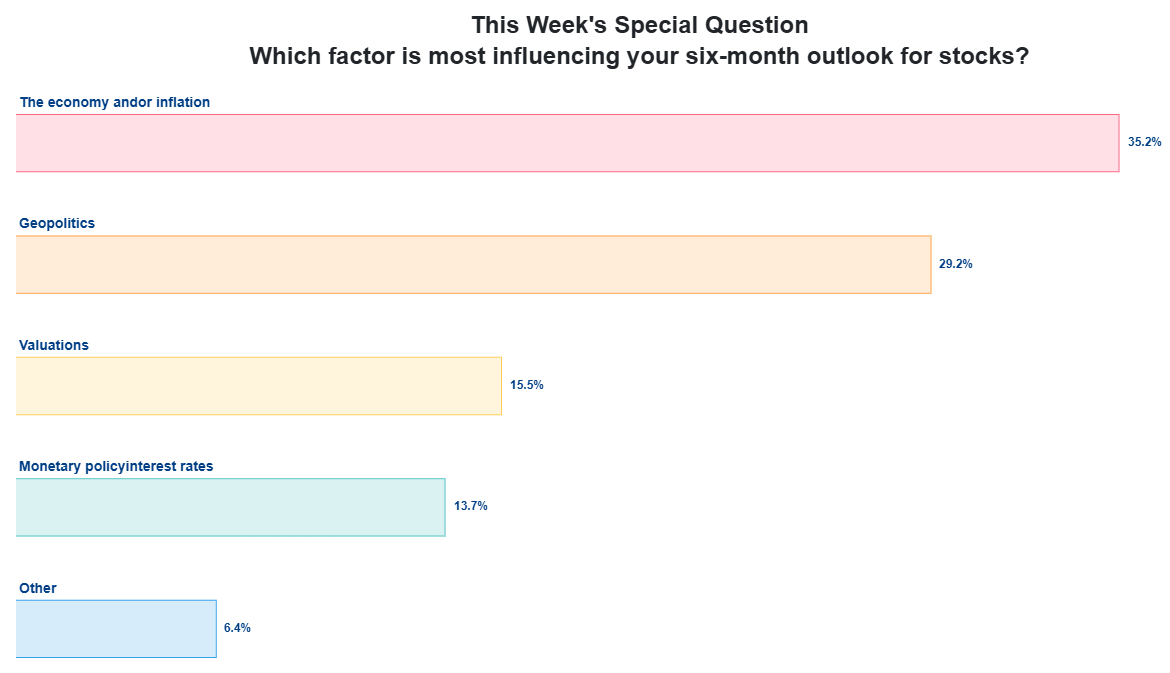

In the special question this week AAII asked “Which factor is most influencing your six-month outlook for stocks?”

The answers were relatively diverse with the economy/inflation leading at 35.2%.

Geopolitics was second at 29.2%, valuations were selected by 15.5%, and monetary policy/interest rates by 13.7%.

6.4% said it was something else.

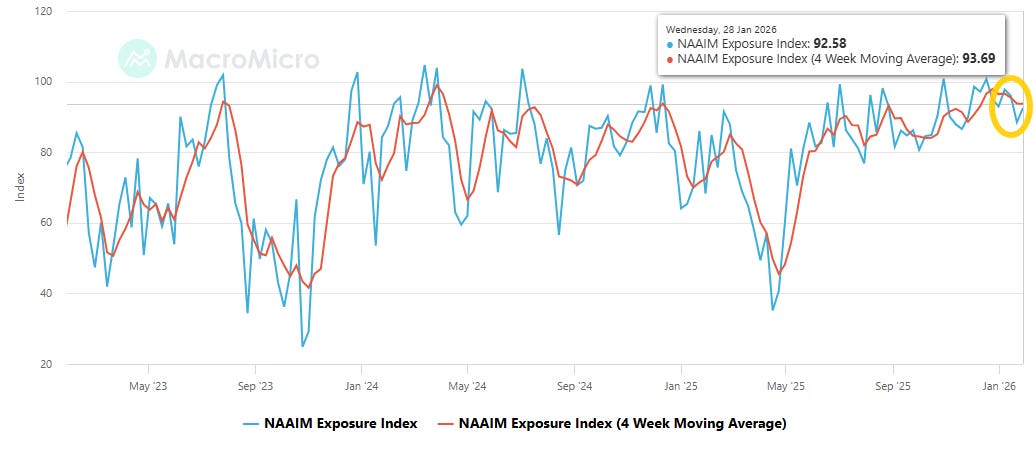

NAAIM (investment managers) exposure index (blue line) edged higher to 92.58% after falling back for two weeks to 88.46% the least since Nov 19th, remaining in its range since late May when it crossed above 80. Since then it has ranged between a low of 76.85 (July 30th) and high of 100.83 (Oct 29th) (over 100 means that the average respondent (investment manager) was levered long equities).

The 4-wk avg (reddish line) edged down to 93.69% from 93.78% continuing its softening from the 97.9% Dec 24th, which was the highest since Mar ‘24 (99.0%).

As a reminder, the index “represents the average exposure to US Equity markets reported by our members” and which ranges from -200% (2x short) to +200% (2x long).

https://naaim.org/programs/naaim-exposure-index/

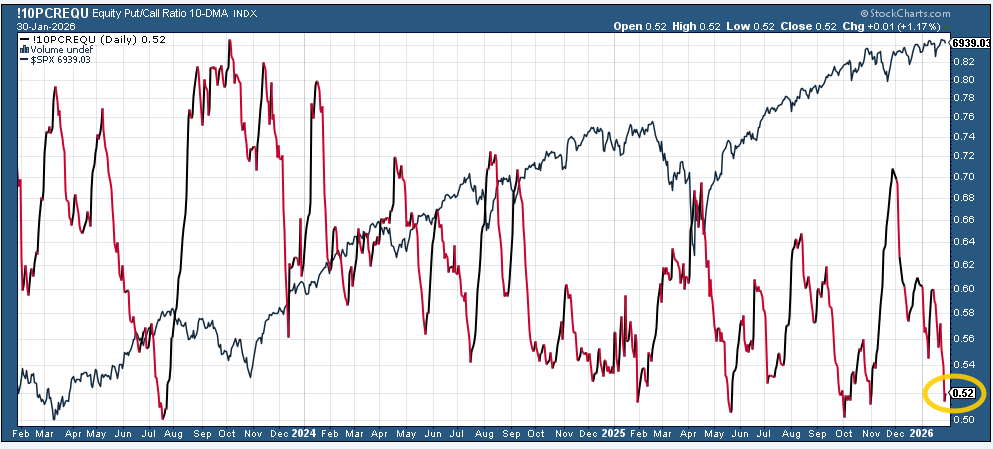

The 10-DMA of the equity put/call ratio (black/red line) fell to the lows of the year at 0.52, not far from the 3-year lows in October of 0.50, meaning much more upside protection (calls) is being bought than downside protection.

That’s down from the highs of the year (0.60) and the 0.71 in late Nov (which was the highest in a year).

When it’s increasing it normally correlates to a consolidation in equities and increase in volatility and vice versa.

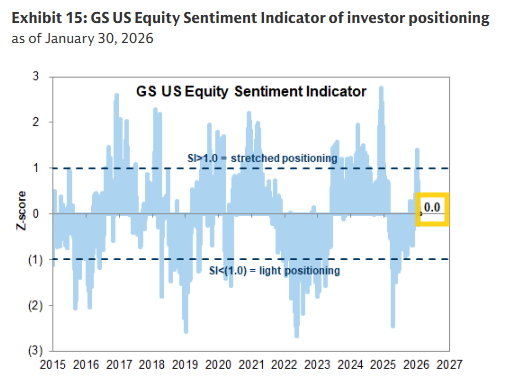

Goldman’s US Equity Sentiment Indicator* after moving into “stretched positioning” (over 1.0) four weeks ago for the first time in nearly a year but fell back the following week to -0.2 (the first negative read in six weeks) spent a third week near the 0 mark, this week right on it (0.0).

*The indicator combines “six weekly and three monthly indicators that span [across the more than 80% of the US equity market that is owned by institutional, retail and foreign investors]. Readings of +1.0 or higher have historically signaled stretched equity positioning. Readings of -1.0 or lower have signaled very light positioning and have historically been a statistically significant signal for subsequent S&P 500 performance”.

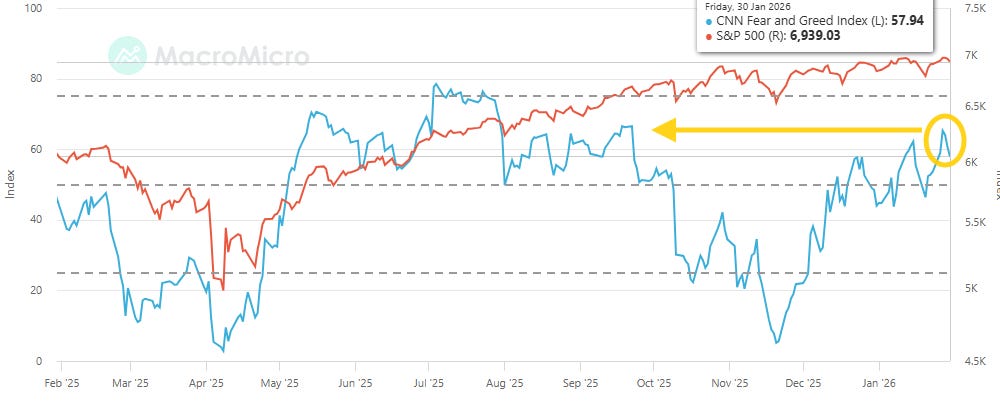

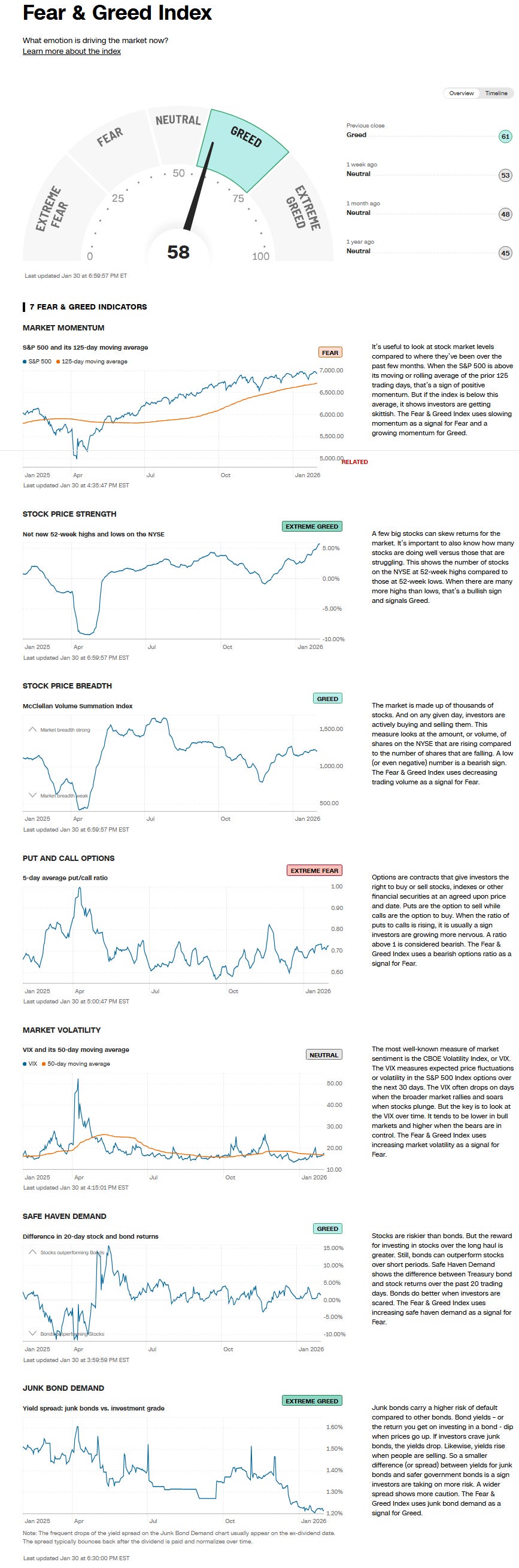

The CNN Fear & Greed Index (blue line) rose to 65.27 Tuesday, the highest since Sept 22nd before falling back the rest of the week ending at 57.94, still in “Greed” territory.

Interestingly just one indicator changed w/w (safe haven demand went from Extreme Fear to Greed). That broke up the “perfect split” the previous week with now the index tipping to the Greed side with four indicators on that side, two on the Fear side:

Extreme Greed = junk bond demand (vs investment grade); stock price strength (net new 52-week highs)

Greed = stock price breadth (McClellan Volume Summation Index); safe haven demand (20-day difference in stock/bond returns) (from Extreme Fear)

Neutral = market volatility (VIX & its 50-DMA)

Fear = market momentum (SPX vs 125-DMA)

Extreme Fear =put/call options (5-day put/call options)

https://www.cnn.com/markets/fear-and-greed

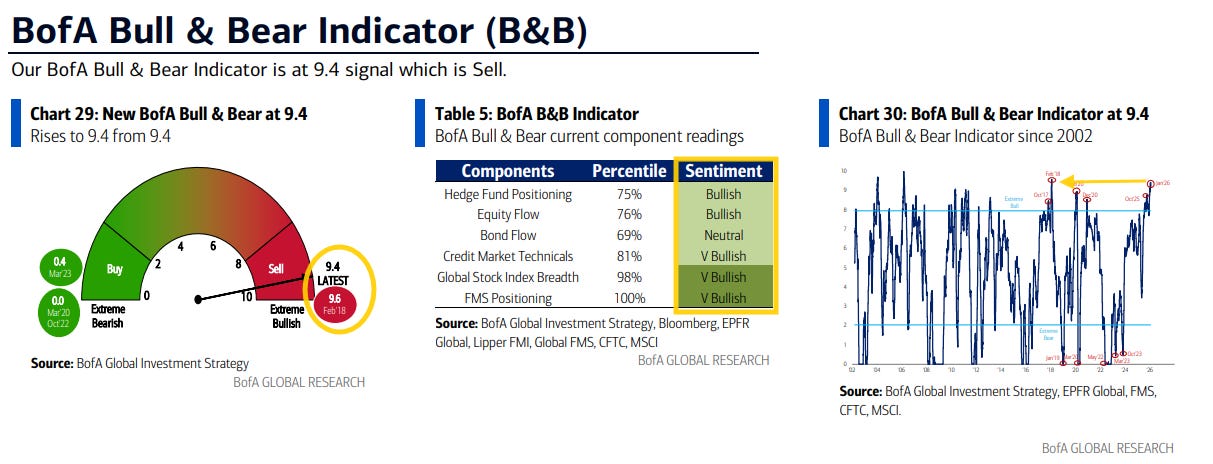

The revamped BofA Bull & Bear Indicator back up to 9.4 for the second time in three weeks, the highest since Feb ‘18, “an extreme bullish level,” back over the “contrarian sell signal” level which “is “still in operation”.

The move was “on strong global stock index breadth, long-only bull positioning (e.g., record low 3.2% FMS cash level), and robust credit market technicals, which offset global equity outflows”.

As a reminder Hartnett noted three weeks ago that “past 24 years average 3-month return when B&B Indicator >9.3… ACWI flat, S&P500 - 1%”. All six of the components remain either “Bullish or “V Bullish”.

Hartnett notes the “old” BofA Bull & Bear indicator though fell for a second week to 6.4 from 7.0 the prior week and 7.5 the week before that (the highest since Feb’21, but still never hitting a sell signal (the old indicator didn’t hit a sell signal post-pandemic (why they changed it))).

Two weeks after the record streak of bullishness in Helene Meisler’s weekly poll ended at 13 weeks, and a week after Helene’s poll respondents were exactly split 50/50, they took a bigger step back into the bearish camp with only 39.9% seeing the next 100pts on the SPX higher, the least since Aug 1st.

Notably, that day (Aug 1st) marked a low that would not be seen again (at least so far) as seen in the second chart. Fingers crossed we get that again! (Better than the 8-10% pullback which followed the last two 50/50 splits!).

The record high was 73.3% Dec 20th, the record low was 33.2% on May 17th.

I noted when that 13 week streak ended it resumed soon thereafter with another 6 weeks of bullish readings (and the SPX chopped for a bit but also continued on its way for another six months). Looks like we’re not going to see that but perhaps we’ll get the rally?

Looking in more detail at when the previous longest streak (10 weeks) of bullishness in Helene’s poll ended in Apr 2021 (second chart), the next week was higher but then we fell back for two weeks, chopped for a month, then resumed climbing into the Dec ‘21 peak of that cyclical bull.

And the link to Helene Meisler’s always excellent Weekly Chart Fest.

Her message this week:

Sure we had a big whack in some groups last week (looking at you metals and software) but nothing broke. Most of what I see is what I have been looking for for 2 weeks now: the 493 were overbought and over-extended and needed to correct. The buck is the most interesting chart: was that a fake break? And the SPY/Naz ratio chart.

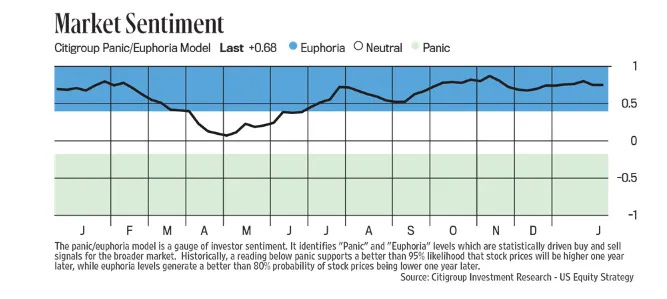

It normally includes Citi’s Panic/Euphoria Index which fell almost to the zero line at the end of April, moved higher, softened again in August but never left Euphoria before hitting new 52-week highs six weeks ago before again softening mid-Nov to mid-Dec but again climbed back towards the highs before softening a touch this week remaining well into Euphoria.

While the fine print says “[h]istorically...euphoria levels generate a better than 80% probability of stock prices being lower one year later,” it has seen a mixed track since the start of 2024:

-It entered euphoria in late March 2024 (when the SPX was around 5200). We didn’t get to 5200 by late March of this year, but we got closer than I would have thought at 5500 (and we did fall under for one day in April).

-The next entry into Euphoria was in late October 2024 w/the SPX around 5800. The closest we’ve been since the start of October was 6550.

This most recent entry was in July w/SPX at 6200. We’ll see how it does this time (so would need to be under 6200 July 2026).

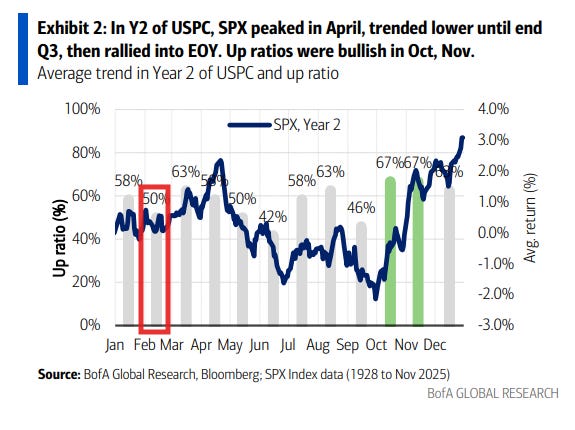

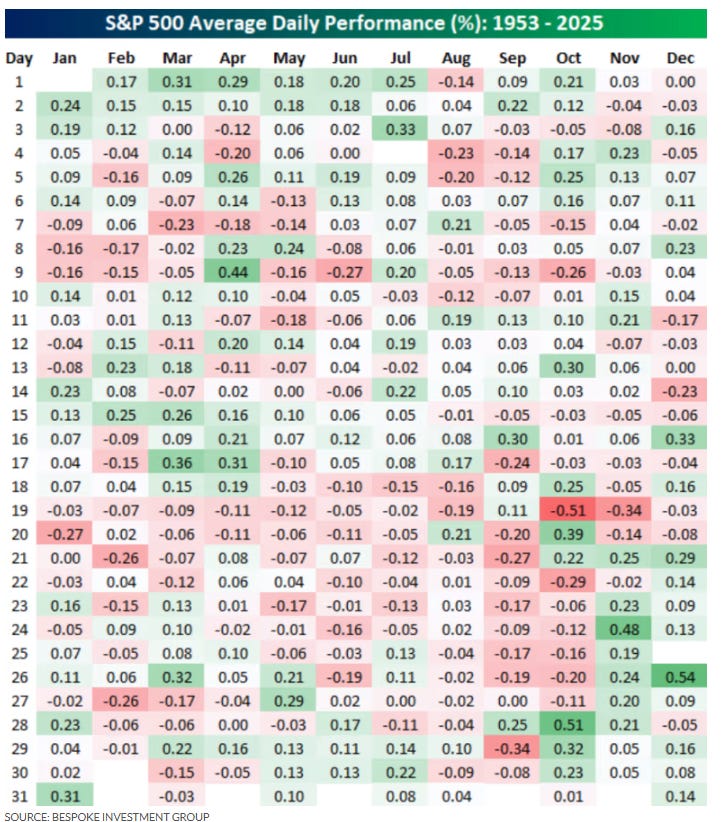

Seasonality

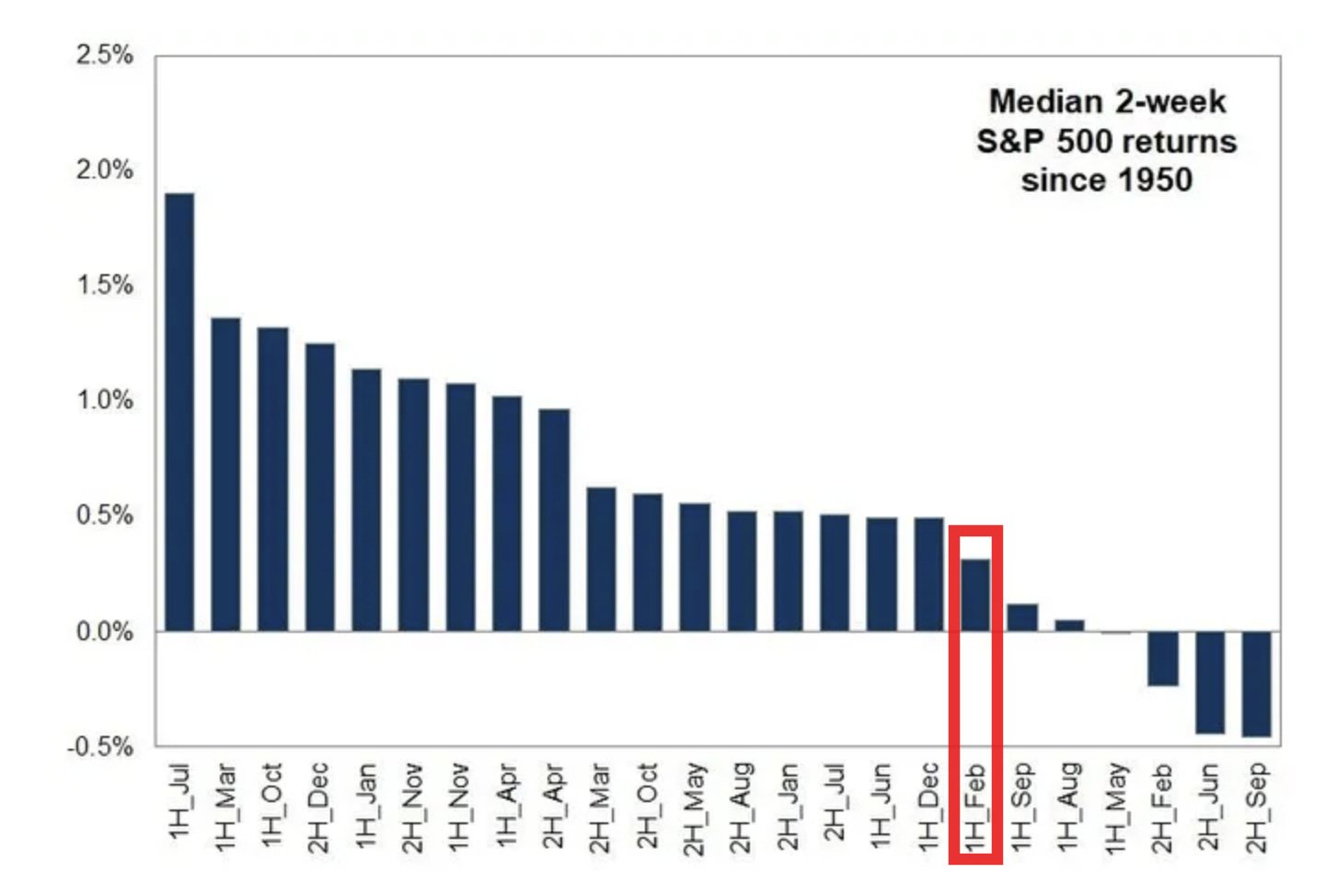

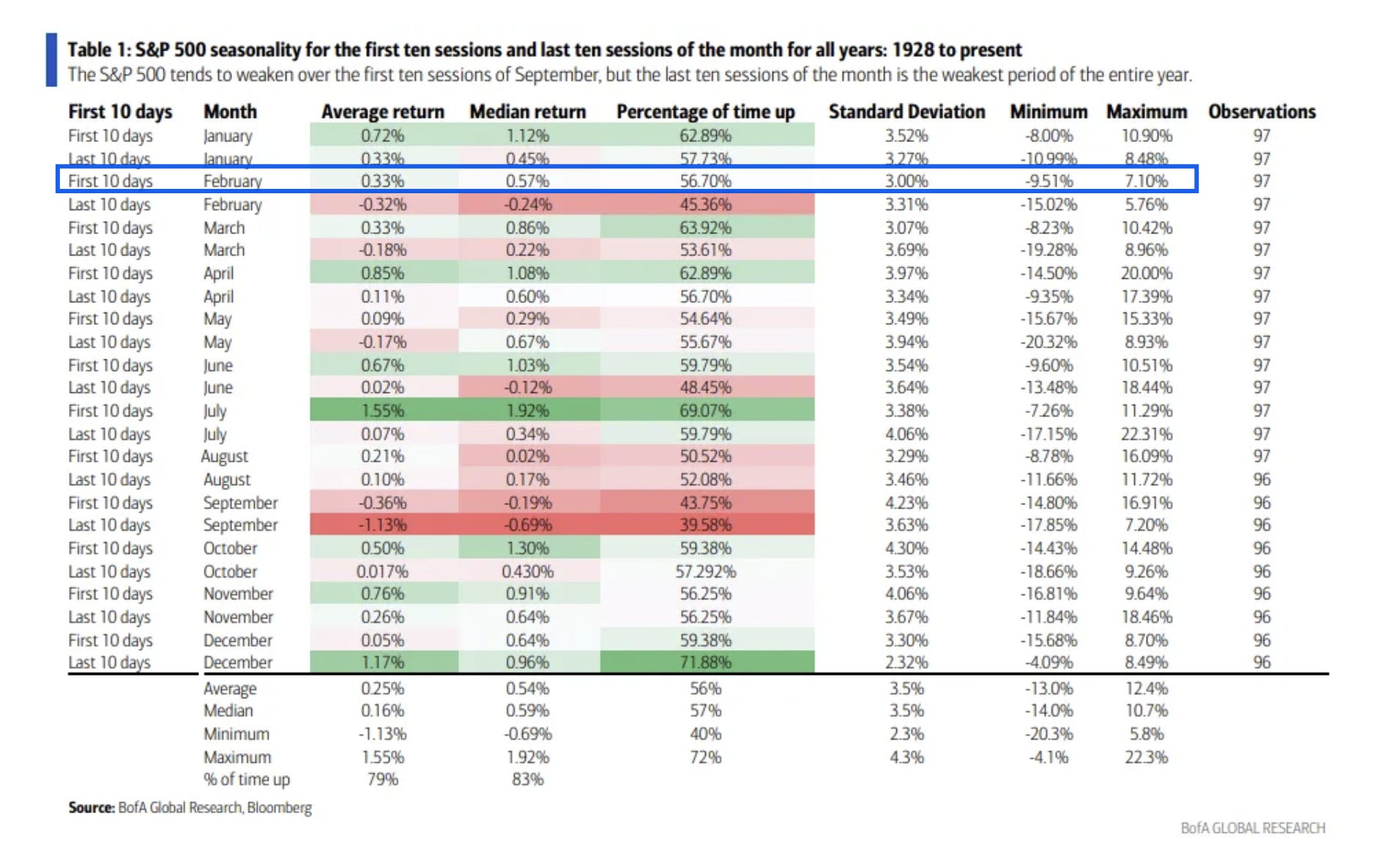

As we move into the first half of February, seasonality for all years since 1950 turns again less supportive but still positive with a median return of +0.3%, but that’s the 7th worst among all half months.

Looking since 1929 though the first half of Feb actually has the same average gain as the second half of Jan at +0.33%, right in the middle of all half-months, a little above the all-halves average of +0.25%, and the median a little better at +0.57% which is similarly around the middle of all half-months and a little below the all-halves median of +0.59%.

The first half of Feb has been positive 56.7% of the time, a touch above the 56% average and in-line with the 57% median for all halves, while the standard deviation (volatility of returns) drops to 3.00% the second least of the year (after the last half of Dec) well below the all-halves avg/median of 3.5%.

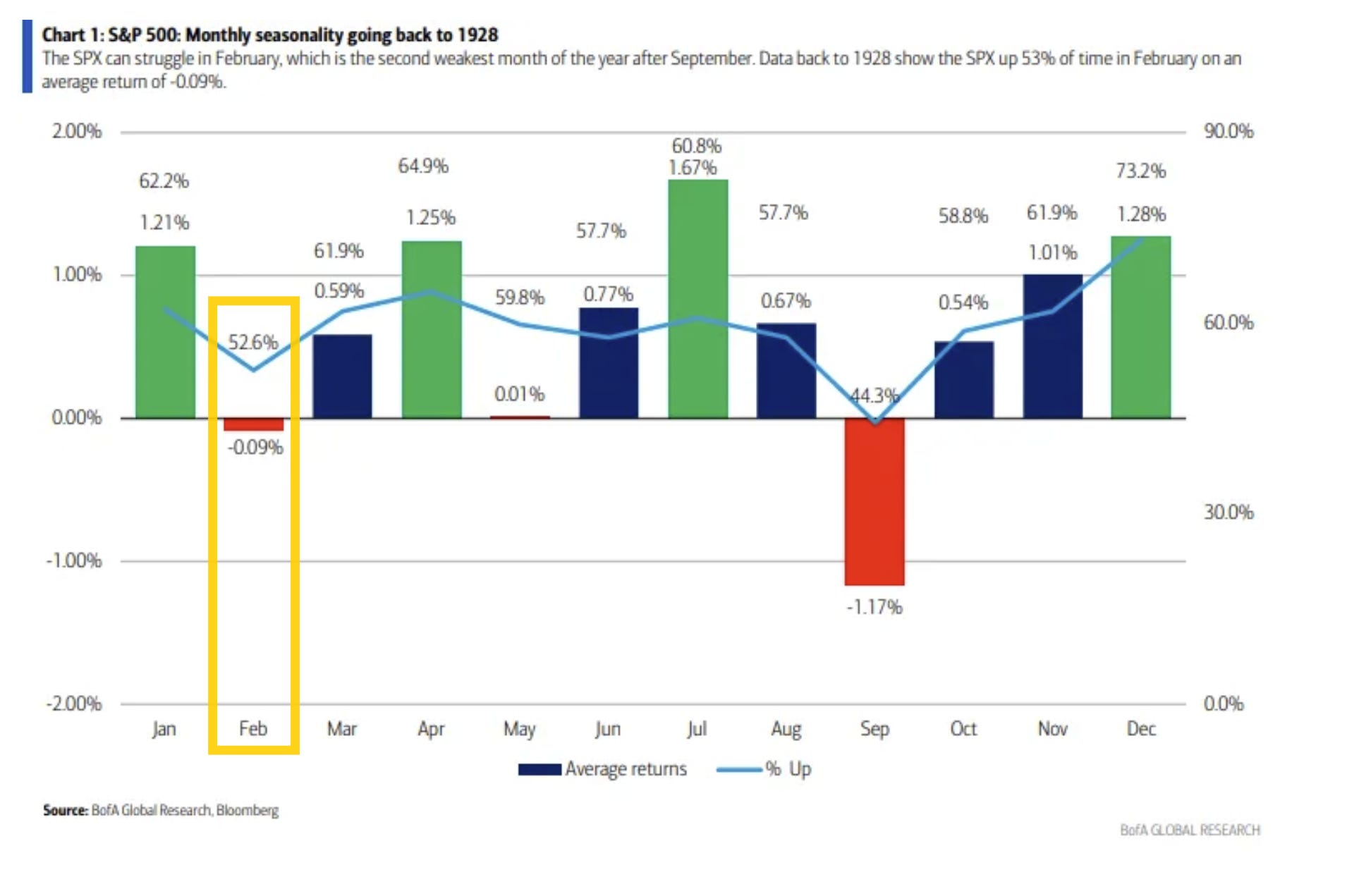

For the month as a whole though, since 1928 February is 2nd wors month with an avg return of -0.09%, up just 52.6% of the time.

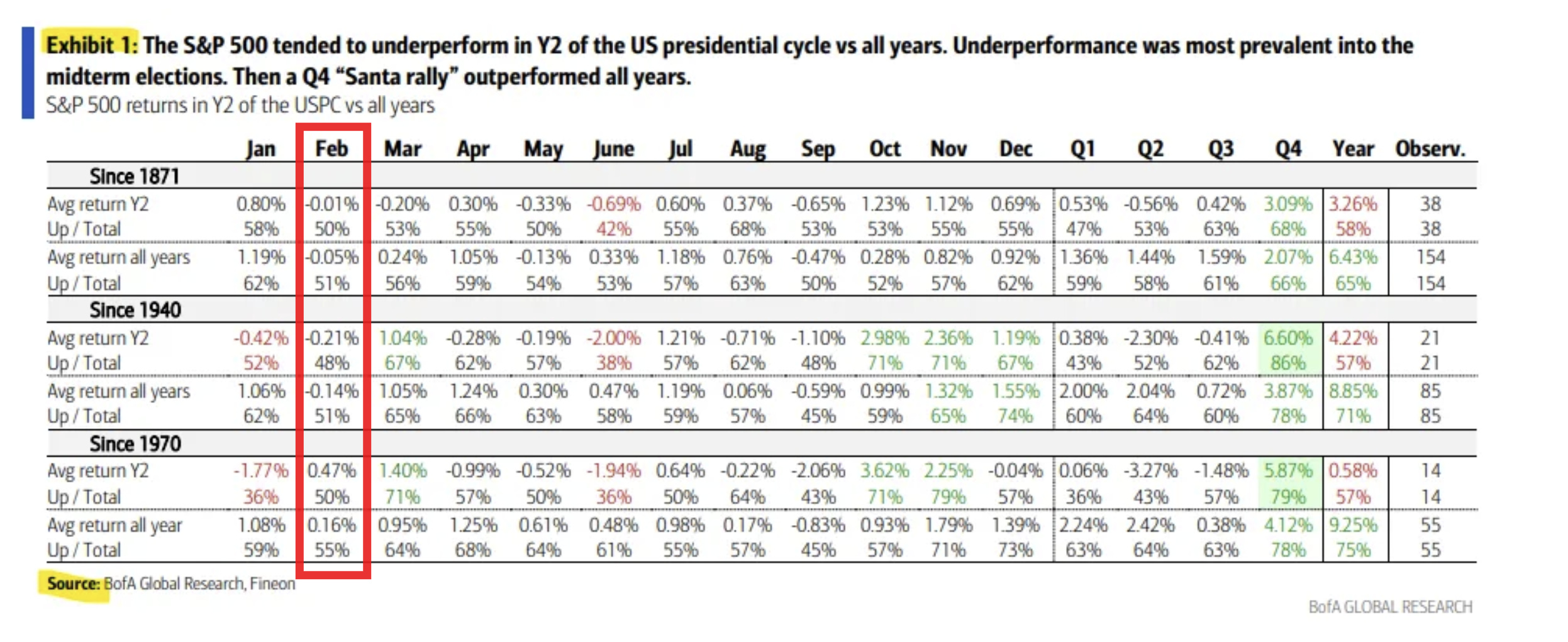

And looking specifically at Year 2 of the Presidential cycle, since 1940 February has been up 48% of the time with an average gain of -0.21% (vs 51% and -0.14% for all year), but if we zoom in on since 1970, it’s been up 50% of the time with an average gain of +0.47% (vs 55% and +0.16% for all years).

Final Thoughts

If you want the summary as to “how we got here” in 2025 you can see the Dec 21st Week Ahead in this section.

As I said last week,

despite a start to the year that I think few envisioned (outside of the President’s inner circle perhaps) from the geopolitical (Maduro removal, potential Iran strikes, potential NATO tariffs, etc.) to the domestic (Fed rate cut bets slashed, a flurry of executive proposals from capping credit card rates to homebuyer assistance to attempts to limit certain buybacks and executive compensation, renewed government shutdown threats, etc.) markets have not only hung in remarkably well but have seen a dramatic broadening to the more sensitive areas of the market (cyclicals, small caps, etc.).

Holding things back at the big-cap index level has been the weakness in the heavyweights (Mag-7 is flat not only for the year but since Sept 22nd) along with selling from systematic strategies last week with the increased volatility. But nevertheless, the index remains in its upwards channel since June, supported by previous Fed rate cuts (and a very high bar for hikes), solid if not spectacular earnings (even if they’re not being rewarded as they historically have for a third consecutive quarter), a solid economy that is showing tentative signs of reaccelerating (see Economy section), a continued strong retail bid with hedge funds also now participating, systematic strategies that have maintained high levels of exposure even if trimming at the margins, and buybacks reaccelerating to record levels (even if just average on a % of market cap basis) and sentiment while positive is not frothy (the “sweet spot”), while valuations, while high, are off their most extreme levels.