If you're a new reader or maybe one who doesn’t make it to the end feel free to take a second to subscribe now. Sources are Argus and Bloomberg unless otherwise noted.

As noted in the weekend update (which is much more in depth than the quick summaries, I encourage you to check it out if you haven’t), as with last week there’s reasons to be bullish this week (technicals, breadth, systematic flows(?)), but also reasons to be bearish (remain mildly overbought conditions, technical resistance), and some wildcards (data, global events, Fedspeak, and earnings).

So, overall, as I noted last week, earnings and data will be the big focus for now, particularly with the Fed on autopilot for the next meeting. Last week I was dubious that we could get through resistance given how overbought the market was (although we still remain overbought just not such extremes). This week I’m a little more optimistic, particularly if we can some systematic flows, but emphasis on a little. Breadth remains pretty good though (and ended the week strong) which is an additional tailwind. The beginning of the week is relatively light on data and with no Fed speakers it’s definitely possible we see a rally over resistance. Thursday and Friday will be more about reactions to the data, and all week earnings will be a moderate factor, so any of those have the potential to push us one way or the other. On the negative side, it’s a weak week seasonally, and, well, we are in a bear market for now, so all else equal the general path is down until that’s been broken. We also are still fairly overbought after not having fully reset the more extreme overbought conditions from last week.

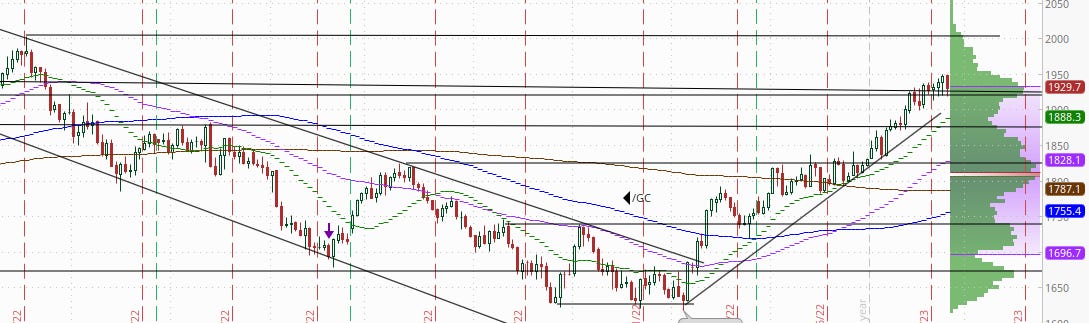

And on Monday we did get the positive start to the week I was hoping for. It definitely took the index back over the 200-DMA, and, depending on where you draw the MOAT (Mother Of All Trendlines), we are above that as well. It’s the first close I have over the line since the start of the bear market. It also took us above the closely watched 4000 level that we haven’t closed over since Dec 13th. So no matter how you look at it, a positive day technically. And I postulated that if they haven’t already, CTA’s will be jumping on this train soon. I ended Monday with

Now is the test. Do we get the follow through buying that keeps us above for more than a day or two or do we fall back into the chop like every other time since the start of the bear market? Answer is above my pay grade, but we’ll know soon enough. We do get flash PMI’s tomorrow. I’d be surprised if they are market moving (but they might be if they come in significantly different from expectations which are for more weakness). Also a relatively big day for earnings (see below) so that potentially could impact things as well.

But on Tuesday in contrast to my thinking that the flash PMIs would be dismissed, it appears they had a sizeable impact on trading, particularly in the dollar and bond markets as both the dollar and yields fell sharply following the release (see charts in Tuesday’s wrap up) which gave a lift to equities that were in danger of breaking down (the SPX notably had fallen beneath 4000 at that point). From there equities continued to grind higher throughout the day to end little changed near their highs. They might have done better but for relatively weak earnings releases. But the recovery kept the SPX above all of those key levels identified above while the Nasdaq and NDX approach those same key levels currently (see chart in the Bloomberg section of Tuesday’s wrap-up), and the RUT is also below a key level (19,000)). I ended Tuesday with:

As noted Monday, after breaking through those well-watched resistance levels, now is the test. As I said, “do we get the follow through buying that keeps us above for more than a day or two or do we fall back into the chop like every other time since the start of the bear market?” Wednesday is free of any major data, so while earnings will be important (which we will get a lot of), the day’s action might give us some indication of which way the markets seem to want to go (and whether we are getting any of that systematic buying) as we head into the data heavy end of the week.

And earnings were in fact “important” on Wednesday, particularly those from heavyweight Microsoft (easily the second largest stock in the indices) along with Dow component Boeing. Those in addition to other weak reports noted in Wednesday’s report had stocks down early with the SPX at one point -1.5%. But whereas Tuesday the recovery was fueled by a big drop in bond yields on the back of weak PMI’s, Wednesday stocks recovered in the face of modestly rising yields (although yields still finished lower on the day). The recovery was also more impressive than Tuesday’s due to the fact that at the lows the SPX had fallen beneath all of those well watched levels (4000, MOAT, 200-DMA), making today’s action notable to me. Still it left the major indices little changed for a second day, an inconclusive result at best ahead of more earnings and some key economic data tomorrow. I ended Wednesday with

So for a second day stocks recovered from early losses to finish little changed. I’m inclined to take that bullishly (failure to break down), particularly given we broke those noted key levels during the session, breadth outperformed modestly today, and the sideways action has helped to work off some of the overbought condition we started the week with. Tomorrow, though, we get some big data, particularly 4Q GDP. That definitely has the potential to move markets, as do earnings releases once again (particularly the card companies in terms of what they see in consumer spending). So we’ll see how those come out, and if we can make some better headway towards my target of 4100.

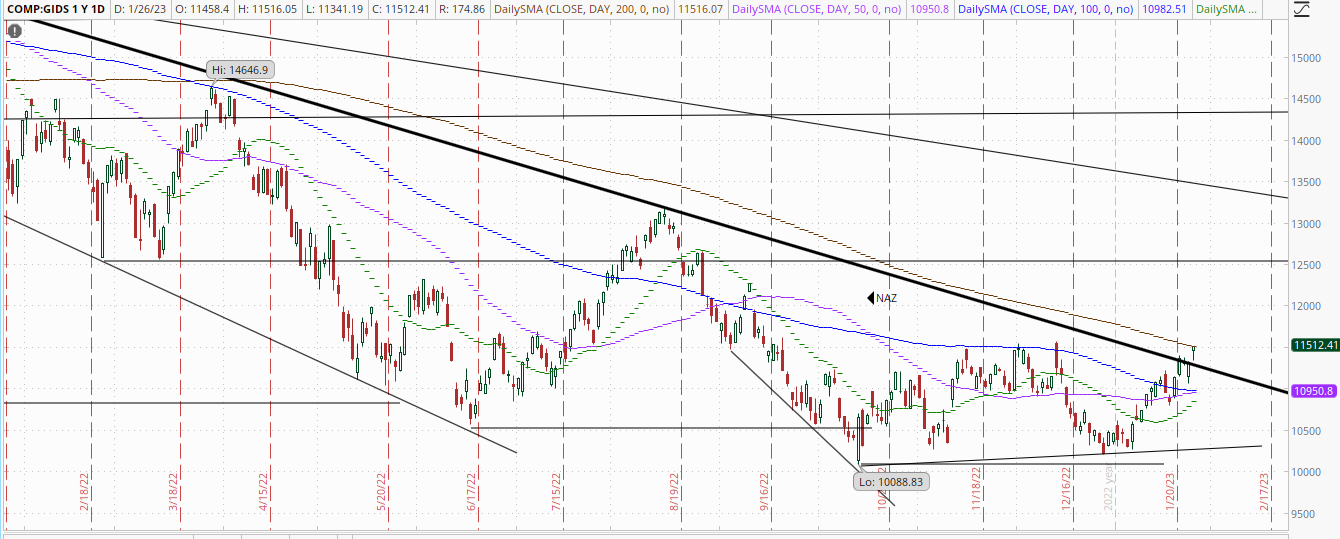

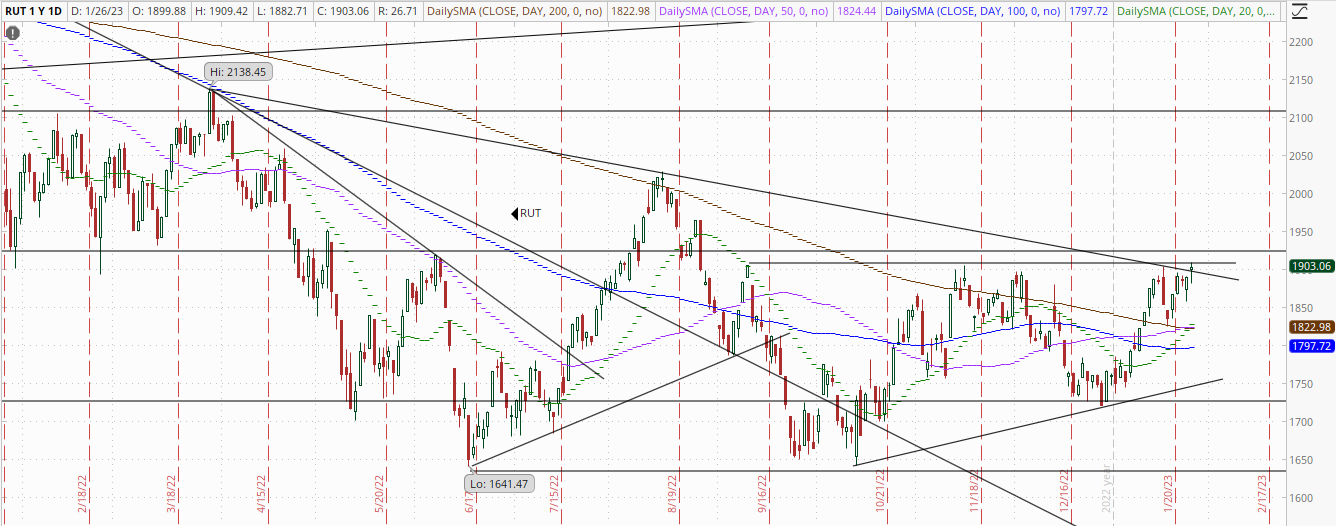

And on Thursday we did “make some better headway towards my target of 4100” getting about halfway there on the back of better corporate news (noted below) and no economic data that the market had a major issue with. While most data came in better than expected, each had caveats, as noted in the linked summaries. Also aiding stocks was declines in yields and the dollar during the session (although both ended higher on the day). And on a technical note while the SPX is now clear of its 200-DMA, the Nasdaq Comp is now testing it’s while the RUT is testing that key 1910 level.

Nasdaq

RUT

Dollar

10-year yield

SPX

Argus:

Today's trade shaped up to be decidedly positive after hitting an air pocket around mid-morning. The main indices moved higher right out of the gate following Tesla's (TSLA 160.27, +15.84, +11.0%) strong quarterly results and outlook, which drove a continued rebound in the mega cap space, and Chevron's (CVX 187.79, +8.71, +4.9%) massive $75 billion stock repurchase program announcement. There was also a slate of pleasing data releases this morning that helped support the positive bias. Namely, the Advance Q4 GDP Report, weekly initial jobless claims, and December durable goods orders all came in better than expected.

Some eventual selling interest kicked in mid-morning, driven presumably by an awareness that this morning's strong data releases could prevent the Fed from pausing its rate hikes in the near future, along with a lingering sense that the market might be getting ahead of itself with the January rally. The Dow Jones Industrial Average, weighed down by IBM's (IBM 134.45, -6.31, -4.5%) earnings-driven weakness, and the S&P 500 slipped into negative territory at their intraday lows.

Nonetheless, equities once again proved to be resilient to selling efforts and the main indices resumed their upside charge. The bounce accelerated in the afternoon trade, likely driven by some short-covering activity and a fear of missing out on further gains, the indices closed at or near their highs for the session. Mega cap leadership was an important support factor in today's turnaround. The Vanguard Mega Cap Growth ETF (MGK) rose 1.7% versus a 0.8% gain in the Invesco S&P 500 Equal Weight ETF (RSP) and a 1.1% gain in the S&P 500.

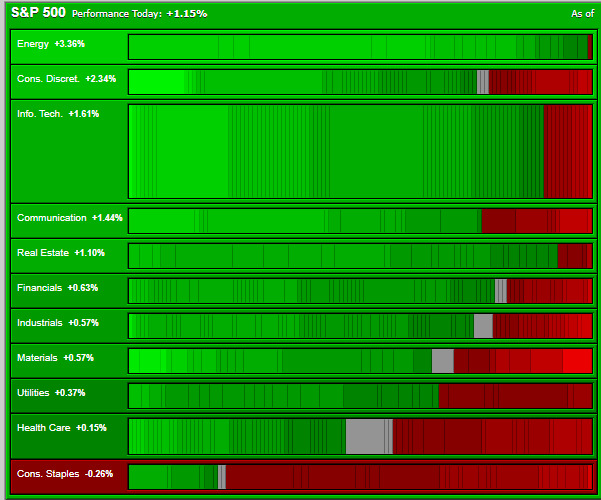

Ten of the 11 S&P 500 sectors logged a gain today led by energy (+3.3%), which was a reflection of Chevron's strong performance. The influential consumer discretionary (+2.0%), communication services (+1.7%), and information technology (+1.6%) sectors were also among the top performers. The consumer staples sector (-0.3%) was the lone the laggard sporting a loss by the close.

Looking ahead to Friday, market participants will receive the following economic data: 8:30 a.m. ET: -December Personal Income (Briefing.com consensus +0.2%; prior +0.4%) and Spending (Briefing.com consensus -0.1%; prior +0.1%), PCE Price Index (Briefing.com consensus 0.0%; prior +0.1%) and core-PCE Price Index (Briefing.com consensus +0.3%; prior +0.2%) 10:00 a.m. ET: -December Pending Homes Sales (Briefing.com consensus -1.0%; prior -4.0%) -January University of Michigan Consumer Sentiment - Final (Briefing.com consensus 64.6; prior 64.6)

Bloomberg:

Tech megacaps powered a stock-market rebound, tempering data suggesting that while the Federal Reserve still has a path to a soft landing, the risk of a recession this year is very much alive. The S&P 500 closed at its highest since early December. Tesla Inc. topped the $500 billion mark, leading gains in the Nasdaq 100 as Elon Musk teased potential for the carmaker to produce 2 million vehicles in 2023.

US gross domestic product expanded at a faster-than-estimated pace into the end of 2022, but there were signs of slowing underlying demand as the steepest rate hikes in decades threaten growth. The Fed is expected to boost rates by 25 basis points next week amid bets the central bank is approaching the end of its tightening cycle. Yet officials are signaling that rates will stay high through the rest of this year. The economy continues to be very resilient in the face of rate increases, but plenty of risks lie ahead, so “we wouldn’t be so quick to blow the all clear,” said Chris Zaccarelli at Independent Advisor Alliance. “That said, this year’s stock-market rally is impressive and shouldn’t be ignored,” the firm’schief investment officer added. “Unfortunately, the Fed is likely to start talking down the market again, as early as next week, so prepare for volatility. We may be in the eye of the hurricane and not completely out of the woods yet.”

To Chris Gaffney, president of world markets at TIAA Bank, the recent data show the Fed is doing a good job, “but there’s more work to be done.”

A team led by Deutsche Bank AG’s Binky Chadha is maintaining its view that the S&P 500 can rise to 4,500 by the end of the first quarter, about 11% above Thursday’s close, before sliding amid an economic contraction. The benchmark is headed for its best January since 2019.

However, it seems like many investors still don’t have the appetite to chase the rally. Some 35% of clients in a recent JPMorgan Chase & Co. survey said they plan to add to stock holdings in the coming weeks. That’s a hair away from a 33% reading in late November that marked an all-time low.

Investors fretting about the prospects for global earnings growth may want to brace for a long slog this year, and stiff headwinds to equities as a result. Analysts’ estimates for 2023 profits continue to fall, with major regions showing negative revision momentum, according to research from Bloomberg Intelligence’s Gina Martin Adams and Gillian Wolff. In the US, for example, sell-side analysts have lowered projections by more than half since September, while the outlook for emerging markets has slumped even more.

Corporate Highlights:

Visa Inc. and Mastercard Inc. saw purchase volumes on their cards climb less than expected in the final three months of the year.

Hasbro Inc., one of the world’s largest toymakers, said it would cut jobs after a disappointing holiday shopping season.

Bed Bath & Beyond Inc. said it received a default notice from JPMorgan Chase & Co. after it failed to prepay an overadvance and satisfy certain creditor protections.

Southwest Airlines Co.’s operations meltdown last month will lead to a first-quarter loss.

Comcast Corp. topped Wall Street profit estimates in the fourth quarter despite continuing to lose customers in its cable and broadband businesses.

In late trading, chipmaker Intel Corp. tumbled on a bleak forecast.

An improved SPX sector flag with only staples declining, and eight of eleven sectors up at least a half percent (and five over 1%). Energy led followed by growth as outperformance there continues.

The Morningstarstyle box also improved with every style up at least a half percent. Growth outperformed here as well.

Breadth was disappointing. The numbers improved from Wednesday, but the improvement was modest compared with the index gains. 64% of volume was positive on the NYSE (after 60% yesterday), while the Nasdaq had 59% (after 51% yesterday). Issues were 66 and 57% (after 51 and 50%). Again, an improvement, so hard to be too negative but would have liked to see these numbers higher.

Overseas, major equity indices in the Asia-Pacific region ended Thursday on a mixed note while markets in China, India, and Australia were closed for holidays. Japan's Nikkei: -0.1%, Hong Kong's Hang Seng: +2.4%, China's Shanghai Composite: CLOSED, India's Sensex: CLOSED, South Korea's Kospi: +1.6%, Australia's ASX All Ordinaries: CLOSED.

On the first trading day following the Lunar New Year break, the benchmark Hang Seng Index jumped 2.4% to close at its highest since March 1. The Hang Seng China Enterprises Index, which tracks mainland companies listed in Hong Kong, rallied almost 3%. The offshore yuan also strengthened against the dollar as onshore markets remain closed for the week. Traders were emboldened by China’s holiday travel and box office data, which showed a strong revival in demand and suggested the nation has emerged from the worst of a Covid Zero exit wave. Investors have been keeping a keen eye on consumption figures from the nation’s most important holiday to gauge the strength of China’s economic recovery. The holiday period also saw tourism rebound in Hong Kong and Macau as cross-border travel revved up. The gaming hub greeted almost 40,000 mainland visitors on the second day of the holiday, the most since the start of the pandemic, while Hong Kong’s daily passenger arrivals also jumped. About 95.9 million trips were made by road, rail, air and waterways during the first four days of the week-long public holiday, which began Saturday, according to Bloomberg calculations from data released by the Ministry of Transport. That’s a daily average of roughly 24 million trips, compared with an average of just 18.6 million over the course of the week in 2022. The global equities backdrop is also supportive. Tech stocks drove US equities higher earlier this week as investors await the release of key earnings, and as comments by Federal Reserve officials dialed back fears of overly aggressive policy moves. And adding to the positive mood music, state-run news agency Xinhua reported that Chinese President Xi Jinping said relations between Australia and China are proceeding in “the right direction,” another sign of thawing relations between the two countries ahead of a meeting of top trade officials expected within months. With Thursday’s gains, the Hang Seng Index as well as the Hang Seng China gauge are set to rally for six straight weeks, boosted by the economic reopening and pro-growth policies. That would be the longest streak of weekly gains since January 2020, just before global markets started to collapse as the pandemic took hold. The CSI 300 benchmark will reopen on Monday.

South Korea's GDP contracted in Q4, but Finance Minister Choo said that growth is likely to return in Q1.

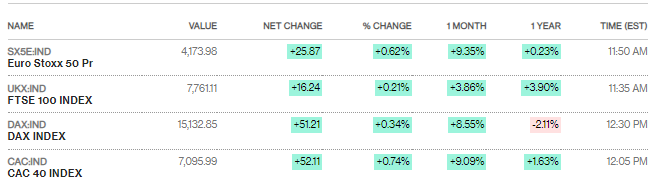

MajorEuropean indices rose following two days of modest losses as investors digested a slew of positive corporate earnings, which signaled that some sectors’ profits and margins can remain resilient despite the economic slowdown.

The Stoxx Europe 600 Index closed up 0.4%, with retail, financial services and banking sectors outperforming. Telecoms group Nokia Oyj surged after better-than-expected quarterly operating profit and chipmaker STMicroelectronics NV jumped amid rising revenue as demand from the auto industry remains strong. Utilities slipped, while Diageo Plc’s biggest drop since August 2020 weighed on beverage companies and the FTSE 100 following disappointing North America earnings for the British firm. Meanwhile, software firm SAP SE retreated as it plans to cut about 3,000 jobs this year while exploring a sale of its remaining stake in Qualtrics International Inc.

Business confidence in Britain has sunk to its lowest level since the global financial crisis, according to a survey of accountants, amid persistently high inflation and fears that the country is already in a recession. The Institute of Chartered Accountants in England and Wales said Thursday that its latest monitor of business sentiment dropped to an index reading of -23.4, the weakest since 2009. The last survey, published in November, stood at -16.9. Companies in the retail, property and manufacturing sectors were particularly downbeat and reported problems accessing capital, the group said. Construction firms had the lowest confidence. The survey included 1,000 chartered accountants and was conducted between Oct. 17 and Dec. 16. Its findings were echoed by a separate survey, also published Thursday, which found morale plummeting among small firms. The Federation of Small Businesses’ confidence index dropped to -46 points in the final quarter of 2022 from -36 in the third quarter. The FSB said it’s now almost as low as during the UK’s second Covid lockdown. Its survey began in 2014. According to the FSB, retail businesses were among the most pessimistic, along with hospitality firms like pubs and restaurants. More than 1,000 small firms were surveyed between Dec. 7 and Dec. 23.

In other markets:

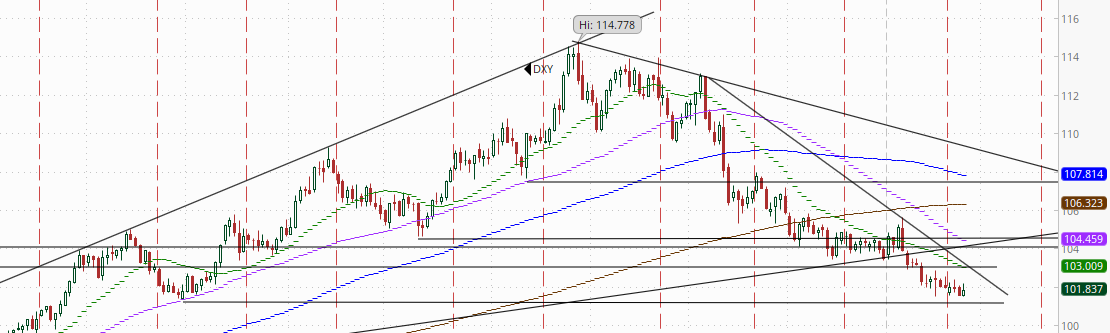

The dollar was up slightly but remains at the bottom of its recent range.

The VIX fell again now with an 18 handle.

WTI - WTI was little changed for a seventh day, continuing to sit just below the 100-DMA. Daily technicals remain positive, so I continue to think it’s more likely than not it gets through but as I noted Monday there are layers of resistance above that, and the 100-DMA is proving very difficult to crack.

On nat gas, as a reminder after breaking my “must hold” level last week I said “it will bounce somewhere, but where is the question.” Since then I have thought if it can just stabilize a few days we could see it move higher, and the first couple of days this week it did that (stabilize), but Wednesday it took another leg lower breaking below $3 for the first time since May 2021. The fact that it couldn’t bounce despite a letter today by the Federal Energy Regulatory Commission authorizing Freeport LNG, the terminal operator, to resume some activities before a full reopening and a larger than expected storage draw speaks volumes, as does the fact that the key March/April spread - essentially a bet on how tight supplies will be at winter’s end — has reversed to a discount.

And on gold as a reminder I have been calling for a consolidation for a couple of weeks, but since we turned the calendar into 2023, it has not taken more than a couple of days off in between gains. I noted Monday it had been two days in a row of muted action, and the pattern repeated with gold moving to a new 7-month high yesterday and again today. It’s fairly overbought again, but that hasn’t mattered for a couple of weeks. It did take another breather today so we’ll see if we get the normal “two days off” pattern.

While we get some earnings and data tomorrow, they are less important than the releases we got today (while the personal income and spending numbers and PCE prices are important, they were incorporated into the 4QGDP number we got today, so we have a very good idea how they’ll come out (weaker consumer spending, weak business investment, in-line prices, solid incomes), and the companies reporting are a lower tier than what we got earlier this week). So there’s really no reason the rally in the SPX can’t continue to that 4100 target area, particularly as I suspect we’re going to see increasing short covering and systematic buying the further we get above the MOAT and 200-DMA. The Nasdaq and RUT are trickier due to the resistance noted at the top, but perhaps this is the time for them as well. We’ll find out soon enough.

Note: I’ve try to do a quick-take on Twitter on the bigger economic reports when they’re released if you don’t follow me there currently (link is at the bottom of this summary).

To see more content, including summaries of most major U.S. economic reports and my morning and nightly updates go to Neil’s Newsletter Substack for newer posts or https://sethiassociates.blogspot.com for the full history. You can also follow me on Twitter at @NeilKSethi