A ton of information from last week, and it just keeps going this upcoming week. I’ll continue to get through as much as I can. As usual, it was a scramble to get this out, with no time to do a full edit. Apologize for any typos, etc.

If you're a new reader or maybe one who doesn’t make it to the end feel free to take a second to subscribe now. Subscriptions help validate spending the time to create these (and I’ll have a note on pledges at the end in the Overall section).

Also please note that I do often add to or tweak this after first publishing it, so it’s always best not to go off the emailed version but to read it from the website where it will have any updates.

Recap

Here was my recap from Friday’s report:

As noted in the weekend update (which is much more in depth than the quick summaries, I encourage you to check it out if you haven’t), as with last week there’s reasons to be bullish this week (technicals, breadth, systematic flows(?)), but also reasons to be bearish (remain mildly overbought conditions, technical resistance), and some wildcards (data, global events, Fedspeak, and earnings).

So, overall, as I noted last week, earnings and data will be the big focus for now, particularly with the Fed on autopilot for the next meeting. Last week I was dubious that we could get through resistance given how overbought the market was (although we still remain overbought just not such extremes). This week I’m a little more optimistic, particularly if we can some systematic flows, but emphasis on a little. Breadth remains pretty good though (and ended the week strong) which is an additional tailwind. The beginning of the week is relatively light on data and with no Fed speakers it’s definitely possible we see a rally over resistance. Thursday and Friday will be more about reactions to the data, and all week earnings will be a moderate factor, so any of those have the potential to push us one way or the other. On the negative side, it’s a weak week seasonally, and, well, we are in a bear market for now, so all else equal the general path is down until that’s been broken. We also are still fairly overbought after not having fully reset the more extreme overbought conditions from last week.

And on Monday we did get the positive start to the week I was hoping for. It definitely took the index back over the 200-DMA, and, depending on where you draw the MOAT (Mother Of All Trendlines), we are above that as well. It’s the first close I have over the line since the start of the bear market. It also took us above the closely watched 4000 level that we haven’t closed over since Dec 13th. So no matter how you look at it, a positive day technically. And I postulated that if they haven’t already, CTA’s will be jumping on this train soon. I ended Monday with

Now is the test. Do we get the follow through buying that keeps us above for more than a day or two or do we fall back into the chop like every other time since the start of the bear market? Answer is above my pay grade, but we’ll know soon enough. We do get flash PMI’s tomorrow. I’d be surprised if they are market moving (but they might be if they come in significantly different from expectations which are for more weakness). Also a relatively big day for earnings (see below) so that potentially could impact things as well.

But on Tuesday in contrast to my thinking that the flash PMIs would be dismissed, it appears they had a sizeable impact on trading, particularly in the dollar and bond markets as both the dollar and yields fell sharply following the release (see charts in Tuesday’s wrap up) which gave a lift to equities that were in danger of breaking down (the SPX notably had fallen beneath 4000 at that point). From there equities continued to grind higher throughout the day to end little changed near their highs. They might have done better but for relatively weak earnings releases. But the recovery kept the SPX above all of those key levels identified above while the Nasdaq and NDX approach those same key levels currently (see chart in the Bloomberg section of Tuesday’s wrap-up), and the RUT is also below a key level (19,000)). I ended Tuesday with:

As noted Monday, after breaking through those well-watched resistance levels, now is the test. As I said, “do we get the follow through buying that keeps us above for more than a day or two or do we fall back into the chop like every other time since the start of the bear market?” Wednesday is free of any major data, so while earnings will be important (which we will get a lot of), the day’s action might give us some indication of which way the markets seem to want to go (and whether we are getting any of that systematic buying) as we head into the data heavy end of the week.

And earnings were in fact “important” on Wednesday, particularly those from heavyweight Microsoft (easily the second largest stock in the indices) along with Dow component Boeing. Those in addition to other weak reports noted in Wednesday’s report had stocks down early with the SPX at one point -1.5%. But whereas Tuesday the recovery was fueled by a big drop in bond yields on the back of weak PMI’s, Wednesday stocks recovered in the face of modestly rising yields (although yields still finished lower on the day). The recovery was also more impressive than Tuesday’s due to the fact that at the lows the SPX had fallen beneath all of those well watched levels (4000, MOAT, 200-DMA), making today’s action notable to me. Still it left the major indices little changed for a second day, an inconclusive result at best ahead of more earnings and some key economic data tomorrow. I ended Wednesday with

So for a second day stocks recovered from early losses to finish little changed. I’m inclined to take that bullishly (failure to break down), particularly given we broke those noted key levels during the session, breadth outperformed modestly today, and the sideways action has helped to work off some of the overbought condition we started the week with. Tomorrow, though, we get some big data, particularly 4Q GDP. That definitely has the potential to move markets, as do earnings releases once again (particularly the card companies in terms of what they see in consumer spending). So we’ll see how those come out, and if we can make some better headway towards my target of 4100.

And on Thursday we did “make some better headway towards my target of 4100” getting about halfway there on the back of better corporate news (noted in Thursday’s; summary) and no economic data that the market had a major issue with. While most data came in better than expected, each had caveats, as noted in the linked summaries. Also aiding stocks was declines in yields and the dollar during the session (although both ended higher on the day). And I also noted on a technical note that while the SPX was clear of its 200-DMA, the Nasdaq Comp was testing it’s while the RUT was testing that key 1910 level. I ended Thursday with

While we get some earnings and data tomorrow, they are less important than the releases we got today (while the personal income and spending numbers and PCE prices are important, they were incorporated into the 4QGDP number we got today, so we have a very good idea how they’ll come out (weaker consumer spending, weak business investment, in-line prices, solid incomes), and the companies reporting are a lower tier than what we got earlier this week). So there’s really no reason the rally in the SPX can’t continue to that 4100 target area, particularly as I suspect we’re going to see increasing short covering and systematic buying the further we get above the MOAT and 200-DMA. The Nasdaq and RUT are trickier due to the resistance noted at the top, but perhaps this is the time for them as well. We’ll find out soon enough.

And on Friday, that all played out pretty well. The PCE did come in roughly as expected (although it did show sticky services inflation which is something that will almost certainly come up in the Fed press conference next week), and company reports were mixed but didn’t really impede stocks from rallying. A huge day from Tesla and some other tech heavyweights flattered the indexes, but the RUT was also up four tenths of a percent. And neither higher yields nor a higher dollar had much impact, which tells me that there likely was some systematic buying going on (or at least short covering). It was enough to push the SPX up to that 4100 target before it fell back late in the day, but the Nasdaq and RUT kept more of their gains which got them over that resistance (although not by a lot), setting up for an interesting Monday.

Dollar

10-year yield

SPX

. All the major market averages finished higher for the week, with the Nasdaq Composite climbing 4.3% to rack up a fourth straight week of gains, while the S&P 500 gained 2.4%, the Dow Jones average ended up 1.8%, and the Russell 2000 +2.4%.

Flows, Positioning, Etc.

As in the week through Jan 25th, Lipper mostly saw a continuation of what we saw in the previous two weeks with global equity funds seeing continued inflows for the first time in nine weeks with strong flows into European funds again this week and a continued deceleration of outflows from US equities. And after global bond funds saw their first weekly net buying since mid-August three weeks ago week (the most since August 2021) that continued for a fourth week. One difference though was money flowing out of cash globally but into cash in the US (it was the opposite last week). Emerging markets saw a third week of large inflows. RTRS.

Refinitiv Lipper data showed global equity funds obtained $3.23 billion worth of inflows during the week, compared with $5.16 billion worth of net purchases in the previous week.

Fund flows: Global equities, bonds and money market

European and Asian equity funds received $3.15 billion and $1.36 billion worth of inflows, but investors sold about $1.14 billion worth of U.S. equity funds. Global data showed many sectoral funds were out of favor with health care, industrials and financials witnessing disposals of $1.8 billion, $695 million and $687 million, respectively.

Fund flows: Global equity sector funds

As noted, U.S. equity funds witnessed net selling, although outflows during the week stood at just $1.14 billion, the lowest since Nov. 16. It was though a tenth straight week of outflows.

U.S. growth and value funds, both saw withdrawals, worth $3.68 billion and $501 million, respectively.

Fund flows: US growth and value funds

Among sectors, health care, financials and industrials saw $1.35 billion, $857 million and $774 million worth of disposals. Materials led inflows.

Fund flows: US equity sector funds

Meanwhile, global bond funds accumulated a net $11.35 billion worth of inflows in a fourth successive week of net buying. Global short- and medium-term bond funds obtained $1.05 billion, while government bond funds drew $3.53 billion in a 13th straight week of net buying, but investors exited $160 million worth of high yield funds after two weeks of net purchases.

Global bond fund flows in the week ended Jan 25

U.S. bond funds obtained net inflows for a third straight week. U.S. bond funds obtained a net $4.89 billion worth of inflows, although a tad lower than the previous weeks $5.83 billion worth of net purchases. U.S. taxable bond funds attracted $3.75 billion worth of inflows while municipal bond funds drew a net $1.07 billion. Investors purchased U.S. short/intermediate investment-grade, general domestic taxable fixed income, and emerging markets debt funds worth $1.37 billion, $1.09 billion and $822 million, respectively.

Fund flows: US bond funds

Global money market funds suffered $12.25 billion worth of outflows, but U.S. money market funds attracted $10.75 billion worth of inflows after facing two weeks of outflows.

Among global commodity funds, precious metal funds lured $1.19 billion, the biggest weekly inflow in nine months, but energy funds had outflows of $87 million. Data for 24,502 emerging market (EM) funds showed equity funds attracted a net $5.02 billion in a third successive week of net buying, while bond funds obtained a net $3.9 billion worth of inflows.

Fund flows: EM equities and bonds

And Bank of America also strong inflows into European stocks (the fastest pace in nearly a year) as well as EM, while US equity inflows remained muted (but positive unlike the Lipper data). Bonds had a fourth straight week of strong inflows in this data as well. Hartnett noted “capitulation” in technology and health care outflows.

European stock funds had $3.4 billion of inflows in the week through Jan. 25, according to a note from the bank’s strategists led by Michael Hartnett, citing EPFR Global data. This is the largest addition since February, before these funds had 48 straight weeks of outflows. With a growing chorus of investors souring on the US, emerging-market equities outpaced other regions in the week with $7.9 billion coming in, according to the note. US stocks saw just $300 million, the first positive flow in four weeks. Among sectors, Hartnett said flows data show “capitulation” in technology and health care as the outflow trend of the past weeks was the worst since January 2019. By contrast, materials and utilities saw inflows at $700 million and $200 million, respectively. Bonds had a fourth straight week of inflows at $12.2 billion, exceeded by global equity funds with $13.9 billion coming in. Hartnett added that US money market fund assets hit all-time high at $4.8 trillion. There’s “still lots of liquidity sloshing around.”

That data was part of the weekly “Flow Show” report from BofA (FYI, I’m becoming a private client of BoA in part so I start getting this data directly). Interestingly, despite his overall bearishness, Hartnett sees likely further gains before it all falls apart. I do like the disclosure and the lava comment.

Signs point to a US “hard landing” in 2023, Hartnett and his team wrote in the note dated Thursday. Further tightening of financial conditions may be needed this spring to tip the US economy “into the recession the consensus craves,” they said. But the S&P 500 “pain trade” — typically a crowded strategy that tests the resolve of investors — will be around 4,100 to 4,200 points, or as much as 3.4% higher from current levels. “After that we sell,” the strategists wrote, citing a “moment where stock gains start dragging yields higher.”

And Deutsche Bank is even more optimistic. BBG.

A team led by Binky Chadha is maintaining its view that the S&P 500 can rise to 4,500 points by the end of the first quarter, about 12% above current levels, before slumping amid an economic contraction. That’s even as the benchmark is headed for its best January since 2019. “We view the rally as having further to go,” the strategists wrote in a note dated Jan. 25. “While a number of leading indicators have fallen steeply, raising the alarm, there are several reasons for a continued pushing out of the timing of a potential recession.” Among those are strong household and corporate balance sheets, hesitancy to fire employees and excess savings accumulated at the start of the pandemic, they said. “I wouldn’t necessarily describe it as a bullish view on fundamentals. The basic driver of the rally in our view is a positioning squeeze,” Chadha said in a separate interview on Bloomberg TV on Wednesday.

Chadha’s team expects the S&P 500 to fall significantly when the recession begins before rebounding to 4,500 by the end of the year. The strategist said the S&P 500 can slide to as low as 3,250 — down 19% from Wednesday’s close. “A very important aspect of the recession playbook to keep in mind if you’re thinking out 12 months is that equities pretty robustly bottom about halfway through” the year, he said on Bloomberg TV. “They will come all the way back in the fourth quarter.” The Deutsche Bank team called the first-quarter rally back in November, although their 2022 year-end target didn’t pan out, with the benchmark ending the year at 3,839.50 versus their forecast of 4,750 points.

But others aren’t having it. JP Morgan strategists retained their bearish posture. HR.

Eventually, “risk markets will have to reconnect with the late-cycle backdrop.” That’s according to JPMorgan analysts led by Marko Kolanovic, who last week warned that a recession isn’t in the price for equities. The bank pointed at technical flows to explain part of the recent rally, and they’re not wrong [more on that later]. For their part, JPMorgan sees the flow drivers running out of gas, and on their view, the fundamentals aren’t supportive. “We anticipate markets struggle with the Fed, disappointing earnings and/or guidance, weak capex and worsening activity momentum,” the bank cautioned. “With new orders negative, it is difficult to see PMIs in coming months reach a level that would justify the stock performance, and the cyclical and banks rally is at odds with the current PMI trajectory,” they went on to say, adding that “in earlier quarters, we benefited from the relationship between rising PPIs and profitability as corporates could pass on price increases [but] now we face the reverse of that at a time when consumers’ excess savings are exhausted.”

BBG - And earnings are a concern for JPMorgan Chase & Co. strategist Mislav Matejka, who notes that the environment will be particularly challenging this year, with corporate pricing power starting to reverse, just as margins are near record-high in the US and in Europe. “Even if companies do not disappoint for the fourth quarter 2022, we do not believe EPS upgrades will come in the first half of this year,” Matejka wrote in a note.

As did Mike Wilson. BBG.

Morgan Stanley strategist Michael Wilson elaborated on points he made in a note to clients on Monday: Namely, that investors are failing to price in a backdrop of weakening economic data and earnings for 2023. Recent optimism around a less hawkish Federal Reserve, China reopening and a weaker dollar is already priced into share prices, he wrote. “The question is when will equity indices price the current weakness in the leading data and the eventual weakness in the hard data?,” wrote Wilson, who was the top-ranked strategist in last year’s Institutional Investor survey. “We think it’s this calendar quarter.” Wilson’s view serves as a warning sign after the S&P 500 Index rose 12% since mid-October in its recovery from last year’s bear market. The gauge looks expensive compared with average historical levels given that earnings estimates have been falling for months.

Although he’s bullish 2024 - “As bearish as we are on earnings in the near-term, we actually are probably more bullish than most in 2024 because we think we are in this boom-bust-boom environment,” Wilson said in an interview on Bloomberg TV. “If you agree with our earnings call next year then you almost have to agree with our earnings call this year and the market won’t look through that.”

And you can add Blackrock to the bearish near term bullish long term list.

An investor’s time horizon is key when gauging how 2023 developments so far affect investments. These events have upped our confidence in our strategic views on a horizon of five years and more. Economic risks like a closed China and ultra-high inflation have lessened, further underpinning our strategic overweight of stocks, as the chart shows. Equity valuations look reasonable versus our long-term expectations. The stock rally hints at how markets will likely react once inflation eases and rate hikes pause, buoying prospects for long-term corporate earnings. Yet before this outlook becomes reality, we see DM stocks falling when recessions we expect manifest. We think the U.S. economy’s 2023 calendar year growth will then be positive. Investors with a longer-term investment horizon can position for the rebound now but could see more pain to come in the near term.

We may turn more positive on stocks when the damage we see ahead is priced or our assessment of market risk sentiment shifts. For now, the fading risks after this year’s positive developments are key to our strategic views. Case in point: inflation. We have always expected it to fall as pandemic drivers – like consumer spending’s shift from services to goods – reversed. What’s key is our view of U.S. inflation landing closer to 3% than the Federal Reserve’s 2% target. Markets aren’t pricing that in. Plus, longer-term trends like aging demographics, geopolitical fragmentation and the energy transition mean inflationary pressures will be higher than in the past. Treasury yields are falling further away from where we think they’ll climb to in the long term as investors demand more term premium, or compensation for the risk of holding them amid persistent inflation and heavy debt loads. We don’t think nominal sovereign bonds can diversify portfolios anymore, and our preference for inflation-linked bonds is stronger given 2023 events. We see stock returns offering more compensation for risk than bonds.

While Tom Lee is still refreshingly Tom Lee.

And getting back to positioning the WSJ analysis of EPFR data confirms the flight to cash noted by BofA.

Investors have added about $135 billion to global money-market funds over the past four weeks, according to EPFR data through Jan. 18. That is the best stretch since the four-week period ended May 2020, when those funds logged roughly $175 billion in net inflows. The average return on U.S. money-market funds this month is 4.12%, the highest yield since the 2008 financial crisis, Crane Data show. The S&P 500, on the other hand, has a dividend yield of about 1.6%. The index is up 4.6% so far in January. By the end of December, assets sitting in money-market funds hit a record $5.18 trillion, Crane Data going back to 2006 show. That surpassed the previous high of $5.16 trillion from May 2020.

And while hedge funds remained relatively bearishly positioned as of mid-week.

Per my notes during the week, trend followers (CTA’s) are near their highs since the bear market start in US equities (red line) and well above ex-US (blue).

From Charlie McElligott (via HR, these are the flow drivers JPM was talking about “running out”):

According to Nomura’s estimates, CTAs have covered 12 of 13 legacy shorts, and are now net long again, after almost $140 billion in buying since last month. There might be room for more. Even after recent adds, exposure sits in just the 46%ile going back more than a decade. “Systematic strategies continue to increase equities exposure so far in 2023, revers[ing] last year’s FCI tightening-driven shorts and Underweights,” Nomura’s Charlie McElligott said Tuesday.

Meanwhile, the decline in three-month realized vol helped spur more than $25 billion in added equities exposure from the vol-control universe over the past three months, on Nomura’s data. Overall, vol-control’s equity exposure has almost tripled versus three months ago, but remains relatively low. “If the current vol compression holds, there would be further substantial buying from vol-control looking out two weeks to a month” assuming stocks stay a semblance of well-behaved, McElligott remarked. Of course, it’s earnings season and the tech titans will report over that two-week period, starting on Tuesday with Microsoft. If daily swings at the index level average 2% or more, the latent vol-control bid could morph into lurking sell pressure.

And while flows into the SPX have been positive in January, it appears they may be decelerating.

Yet a peek into the trading activity behind the benchmark suggests the bullish run lacks conviction. Flows into the SPDR S&P 500 ETF Trust (ticker SPY) show that, while the fund is on pace to see net inflows in January after two straight months of investors taking assets out, the total amount of money coming in weekly has been steadily declining this month. Flows into two other major funds tracking the S&P 500 — the Vanguard S&P 500 ETF (VOO) and IShares Core S&P 500 ETF (IVV) — tell a similar story.

Earnings

As earnings are a direct input into stock prices, these along with multiples are the two direct determinants into where a stock is priced. So as those go so will the market all else (the multiple) equal (see chart).

And here has been my overall message since the start of 4Q earnings season:

As I have been writing for the last couple of months,

So far there’s been been some degradation in [4Q22 and2023 earnings expectations], but they’ve held up much better than what you’d typically see in a recessionary period as we’re still talking earnings growth at this point (although decelerating).

And as I noted three weeks ago the total deterioration in estimates for 2023 has been around -8.5% from the peak, and 4Q has seen some deterioration as well. But, importantly, earnings are still forecast to be UP in 2023(by 4%, although it’s all back half loaded). That is not anything like what would be expected in a recession (and why many analysts have 2023 earnings expectations forecast to be more around the $200 mark, meaning the “feared number” is certainly lower than the $230 or so that’s estimated, setting us up for the potential for more “better than feared” earnings seasons in coming quarters). This will be one of the key questions of 2023. Do earnings hold up or don’t they. I have been in the more positive camp all year despite those who predicted an “earnings disaster” this year, and I continue to think they’ll come in at least better than feared, especially after 20% of the SPX has already preannounced (a very high rate) as noted last week. I also think there will be some good support from the weaker dollar (it was down 10% in the 4th quarter), that will hopefully offset the the impact of the 2022 tax increases (buyback tax, minimum corporate tax, etc.). Currently, expectations are for a -3.9% y/y drop in 4Q earnings which I think we’ll beat.

And while earnings have come in “better than feared” (as evidenced by the climb in equities since the start of earnings season, it has not been by much, with one of the weaker beat rates we’ve seen, and unusually seeing expectations fall for the current reporting quarter (4Q) after the start of reporting (expectations are now down to -5% y/y drop from -3.2% ahead of the season starting). Still, it’s relatively early with just 29% of companies reporting (although higher in terms of market cap). Factset updates through Thursday’s earnings:

The Q4 earnings season for the S&P 500 continues to be subpar. While the number of S&P 500 companies reporting positive earnings surprises increased over the past week, the magnitude of these earnings surprises decreased during this time. Both metrics are still below their 5-year and 10-year averages. As a result, the earnings decline for the fourth quarter is larger today compared to the end of last week and compared to the end of the quarter. If the index reports an actual decline in earnings for Q4 2022, it will mark the first year-over-year decline in earnings reported by the index since Q3 2020.

Overall, 29% of the companies in the S&P 500 have reported actual results for Q4 2022 to date. Of these companies, 69% have reported actual EPS above estimates, which is above the percentage of 67% at the end of last week, but below the 5-year average of 77% and below the 10-year average of 73%. In aggregate, companies are reporting earnings that are 1.5% above estimates, which is below the percentage of 3.3% at the end of last week, below the 5-year average of 8.6%, and below the 10-year average of 6.4%. If 1.5% is the actual surprise percentage for the quarter, it will mark the second-lowest surprise percentage reported by the index since Q3 2012, trailing only Q1 2020 (1.1%).

As a result, the index is reporting lower earnings for the fourth quarter today relative to the end of last week and relative to the end of the quarter. The blended (combines actual results for companies that have reported and estimated results for companies that have yet to report) earnings decline for the fourth quarter is -5.0% today, compared to the earnings decline of -4.9% last week and the earnings decline of -3.2% at the end of the fourth quarter (December 31).

Negative earnings surprises reported by companies in the Financials and Industrials sectors were mostly offset by positive earnings surprises reported by companies in multiple sectors, resulting in a small increase in the earnings decline for the index during the past week. Negative earnings surprises and downward revisions to earnings estimates for companies in the Financials sector have been the largest contributors to the increase in the overall earnings decline for the index since December 31. If -5.0% is the actual decline for the quarter, it will mark the first time the index has reported a year-over-year decrease in earnings since Q3 2020 (-5.7%). Four of the 11 sectors are reporting year-over-year earnings growth, led by the Energy and Industrials sectors. On the other hand, seven sectors are reporting a year-over-year decline in earnings, led by the Materials, Consumer Discretionary, Communication Services, and Financials sectors.

In terms of revenues, 60% of S&P 500 companies have reported actual revenues above estimates, which is below the 5-year average of 69% and below 10-year average of 63%. In aggregate, companies are reporting revenues that are 1.0% above the estimates, which is below the 5-year average of 1.9% and below the 10-year average of 1.3%. The index is also reporting higher revenues for the fourth quarter today relative to the end of last week, but flat revenues relative to the end of the quarter. The blended revenue growth rate for the fourth quarter is 3.9% today, compared to a revenue growth rate of 3.7% last week and a revenue growth rate of 3.9% at the end of the fourth quarter (December 31).

Positive revenue surprises reported by companies in multiple sectors (led by the Energy sector) were the largest contributors to the slight increase in the revenue growth rate for the index during the past week. Since December 31 positive and negative revenue surprises in multiple sectors have offset each other, resulting in no change in the overall growth rate. If 3.9% is the actual growth rate for the quarter, it will mark the lowest revenue growth rate reported by the index since Q4 2020 (3.2%). Eight sectors are reporting year-over-year growth in revenues, led by the Energy and Industrials sectors. Three sectors are reporting a year-over-year decline in revenues, led by the Utilities sector.

Looking ahead, analysts expect earnings declines for the first half of 2023, but earnings growth for the second half of 2023. For Q1 2023 and Q2 2023, analysts are projecting earnings declines of -3.0% and -2.4%, respectively. For Q3 2023 and Q4 2023, analysts are projecting earnings growth of 3.7% and 10.3%, respectively. For all of CY 2023, analysts predict earnings growth of 3.4%.

The forward 12-month P/E ratio is 17.8, which is below the 5-year average (18.5) but above the 10-year average (17.2). It is also above the forward P/E ratio of 16.7 recorded at the end of the fourth quarter (December 31), as the price of the index has increased while the forward 12-month EPS estimate has decreased since December 31.

During the upcoming week, 107 S&P 500 companies (including six Dow 30 components) are scheduled to report results for the fourth quarter.

Guidance though continues to be weak as “17 S&P 500 companies have issued negative EPS guidance and 2 S&P 500 companies have issued positive EPS guidance.” This has the forward 12-month EPS continuing its decline since peaking last year, although, again, the overall decline has been much less severe than what we would expect to see in a recession scenario.

And some more granular data on forward earnings from Brian Gilmartin consistent with the foregoing. That 18x P/E is starting to seem a little rich to me and while the earnings yield remains above Treasuries for now, the spread is pretty narrow. As I’ve noted many times if earnings hold up, I think we’ve likely put in durable lows at 3500ish in the SPX (which we may revisit) but if earnings continue to crack it will be more problematic. I’m particularly concerned about the expectations for a very strong 4Q23 and 2024.

The forward 4-quarter estimate (FFQE) slid again this week to $225.02 from last week’s $225.23 and the 9/30/22 $230.43;

The PE ratio on the S&P 500 jumped to 18x this week after the weekly 2.5% rally, up from the 17.5x last week, and the 15.5x from 9/30/22;

The 5.53% S&P 500 earnings yield has declined for 4 straight weeks after peaking near 5.86% on January 6th, 2023;

The Q4 ’22 bottom-up estimate slid one single penny this week to $53.26 from $53.27 a week ago. The same estimate was $57.91 on 9/30/22;

Note how 2023’s expected S&P 500 EPS growth rate has slid to just 2.8% as of this week.

….

this table is catching my interest since it a.) looks at the forward S&P 500 EPS estimates, and b.) measures the rate-of-change for said estimates over time. The 12-week rate-of-change shows the negative EPS estimate revisions becoming less severe, but note how sequential and 4-week rates of change the last two weeks have become a little more severe.

And per my comment about not being very comfortable with an 18x forward P/E, Jurrien Timmer provides some support (for not being comfortable). “At a forward P/E of 17.55x (as of last Friday), the market is trading several points above its fair value, as has been the case for a while. During last year’s bear market, the S&P 500 rarely traded below its fair value, depriving contrarians of a bell-ringing buy signal.”

And in line with most analyst expectations, margins have become to come in from record levels, although remain healthy historically, although it is the sixth straight quarter of declines. Factset.

The (blended) net profit margin for the S&P 500 for Q4 2022 is 11.4%, which is below the previous quarter’s net profit margin of 11.9% and below the year-ago net profit margin of 12.4%. However, it is equal to the 5-year average net profit margin (11.4%).If 11.4% is the actual net profit margin for the quarter, it will mark the sixth straight quarter in which the net profit margin for the index has declined quarter-over-quarter. It will also mark the lowest net profit margin reported by the index since Q4 2020 (10.9%).

At the sector level, four sectors are reporting a year-over-year increase in their net profit margins in Q4 2022 compared to Q4 2021, led by the Energy sector (to 13.4% vs. 9.3%). On the other hand, seven sectors are reporting a year-over-year decrease in their net profit margins in Q4 2022 compared to Q4 2021, led by the Materials sector (10.1% vs. 13.2%) and Financials sector (15.5% vs. 18.5%). Four sectors are reporting net profit margins in Q4 2022 that are above their 5-year averages, led by the Energy sector (13.4% vs. 7.4%). On the other hand, seven sectors are reporting net profit margins in Q4 2022 that are below their 5-year averages, led by the Communication Services sector (9.6% vs. 11.7%).

Only two sectors are reporting a quarter-over-quarter increase in their net profit margins in Q4 2022 compared to Q3 2022, led by the Financials sector (to 15.5% vs. 14.2%). On the other hand, seven sectors are reporting a quarter-over-quarter decrease in their net profit margins in Q4 2022 compared to Q3 2022, led by the Real Estate sector (35.1% vs. 37.7%). Two sectors (Communication Services and Information Technology) are reporting no change in net profit margins quarter-over-quarter.

What is driving the continuing decline in net profit margins for the S&P 500? Higher costs are likely having a negative impact on net profit margins. Producer prices increased by 6.2% in December. Again, although the number has been falling over the past several months, the percentage has exceeded 6.0% (year-over-year) for 21 straight months. During the previous earnings season, 402 S&P 500 companies cited “inflation” on earnings calls for the third quarter, which was the third-highest number in more than 10 years. Companies may be having more difficulty raising prices to offset higher costs, as the S&P 500 is reporting its lowest revenue growth for Q4 2022 (3.7%) since Q4 2020 (3.2%).

In addition, companies are facing a difficult year-over-year comparison to unusually high net profit margins in 2021. In Q4 2021, the S&P 500 recorded the fourth-highest net profit margin (12.4%) reported by the index since FactSet began tracking this metric in 2008. It is interesting to note that analysts believe net profit margins for the S&P 500 will be higher going forward. As of today, the estimated net profit margins for Q1 2023, Q2 2023, Q3 2023, and Q4 2023 are 11.9%, 12.1%, 12.3%, and 12.2%, respectively.

And Mike Wilson continues to think it’s just the start for the “profit reckoning”. HR.

“Suffice it to say, we’re not biting on this recent rally because our work and process are so convincingly bearish on earnings,” he wrote, reminding investors that the bank’s conviction doesn’t hinge on the timing of any US economic recession. Indeed, it doesn’t even hang on a recession happening in 2023 at all. Instead, it’s all about margins and negative operating leverage. In that regard, “the evidence is mounting,” Wilson said. Revenue could “fall off quickly and unexpectedly, while costs remain sticky in the short-term,” he warned, pointing to bloated inventories and “less productive headcount” as “the primary culprits.” That deleterious conjuncture is already visible in some industries even before the onset of an economic downturn. “It’s simply a matter of timing and magnitude, and we think the earnings recession is imminent,” he said, encouraging market participants to “stay focused on fundamentals and ignore the false signals and misleading reflections in this bear market hall of mirrors.” Morgan Stanley expects new lows for the S&P, after which the bear market should come to an end “later this quarter or early in Q2.”

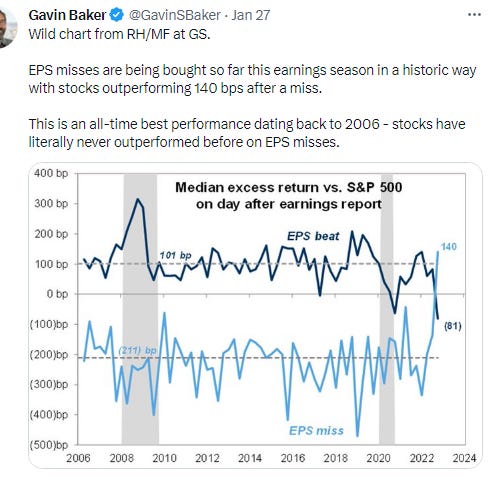

And while again it’s early, we’re seeing a weird divergence between companies that beat and those that miss.

Companies in the S&P 500 that have exceeded projections on both earnings per share and sales have outperformed the benchmark by an average of 1.45% within a day of reporting, exceeding the norm of the past six years, according to data compiled by Bloomberg Intelligence.

And those that fell short underperformed by just 1.7%, the least negative reaction in eight quarters, as many companies report taking steps to adjust to shifting business conditions.

And as a reminder here was Goldman’s estimates, a little below the median (although those have been revised down somewhat as we enter the season with expectations for a -4.6% y/y drop according to Factset as of this week.

And the reports will continue fast and furious next week. SA.

Earnings spotlight: Monday, January 30 - NXP Semiconductors (NXPI) and Whirlpool (NYSE:WHR).

Earnings spotlight: Tuesday, January 31 - Exxon Mobil (XOM), General Motors (GM), UPS (UPS), Pfizer (PFE), Caterpillar (CAT), McDonald's (MCD), Amgen (AMGN), AMD (AMD), Electronic Arts (EA), and UBS (UBS)

Earnings spotlight: Wednesday, February 1 - AmerisourceBergen (ABC), Altria (MO), Peloton Interactive (PTON), and Meta Platforms (META).

Earnings spotlight: Thursday, February 2 - ConocoPhillips (COP), Merck (MRK), Eli Lilly (LLY), Amazon (AMZN), Apple (AAPL), Alphabet (GOOG), Starbucks (SBUX), Ford Motor (F), and Qualcomm (QCOM).

Earnings spotlight: Friday, February 3 - Cigna (NYSE:CI), Regeneron Pharmaceuticals (REGN), and Church & Dwight (NYSE:CHD).

And I’ll keep these charts up for now.

Major Market Technicals

I said last week,

So another chance to move through the MOAT as it’s been described (Mother Of All Trendlines)). The good news is we’re a little less overbought than this time a week ago.

And for the first time since the start of the bear market, the SPX (and Nasdaq it turns out) was able to punch firmly above the MOAT (the RUT was already above its).

Which set it up to run to my target of 4100, which it did during the week. As with crossing the MOAT (pun intended) I don’t have firm feelings on whether the SPX can punch above 4100. That I think is more about the data in this data-heavy week than anything. Daily technicals remain very positive.

And as noted the Nasdaq (and NDX) also pushed through their MOATs as well as their 200-DMAs. Unlike the SPX though they are also above their highs from December giving them considerable room to run. Daily technicals very positive here as well.

And as noted the RUT was already above its MOAT (and 200-DMA), and now is just over its September and November highs appearing to give it a lot of room as well. Daily technicals very positive here as well.

Helene’s take.

Breadth

Breadth continued to be good but not great. But good is still better than poor, and that has been enough to keep the indices moving higher. It also ended in a positive note. Here was Friday’s report:

Breadth was good, maybe the best since Monday taking both indexes together. The numbers softened from Thursday (except Nasdaq volume which improved), but the decline was modest compared with the difference in the index gains. 59% of volume was positive on the NYSE (after 64% yesterday), while the Nasdaq had 66% (after 59% yesterday). Issues were 56 and 55% (after 66 and 57%). Again, considering the index gains were much less today, those are pretty decent numbers, although nothing to write home about.

But interesting overall volumes have been weak on the NYSE while strong on the Nasdaq.

While the McClellan Summation Index (what the average stock has been doing), continues moving higher which is supportive to equities.

As does the volume based version of the Nasdaq.

While the % of stocks above 200-DMAs remains the highest its been since the start of the bear market

And new highs over lows has been strongly positive.

SPX Sectors

Sector performance last week was solidly to the upside for the third week in the last four. Only utilities and healthcare were down for the week. Consumer discretionary led on the back of a huge week for Tesla along with gains for other heavyweights (AMZN, DIS, etc.).

As you know if you read regularly, my sector theme the last few months as been around a dispersion between sectors (strong vs week).

Ten weeks ago I noted:

We’re starting to see a clearer discrepancy growing between some sectors that are below their 200-DMA and trendlines from the beginning of the year (tech, discretionary, communications, real estate), and others that are above those and are showing strong relative strength (industrials, materials, financials, staples, utilities, and energy).

Since that time, as noted last week, outside of a short consolidation by the leading sectors, not much changed except for utilities, which was unable to make headway, and staples and healthcare also started to pull back last week, although they remained above their 200-DMAs. But financials and materials had very good weeks to join industrials, staples, and energy as the clear leaders.

Last week, though, I noted

we’re seeing more glimmers of potential change as those “weakest” sectors (mostly the growth names plus real estate) outperformed. Now most of them are up to around their 200-DMAs and downtrend lines (communications still has some ground to travel). A break above those would be notable. On the flip side, the “strongest” sectors consolidated this week, but those same five sectors remain the leaders for now. Staples and utilities remain below their 200-DMAs, while health care remains above although has been declining steadily for a month.

And with the positive weeks noted above, we did in fact see tech and communications break above their 200-DMAs, while real estate and discretionary touched them on Friday but could not close over. Tech and discretionary also broke above their bear market downtrend lines while the other two are just below. So, in summary, we continue to see the lagging sectors catch up to the previous leaders who outside of utilities remain leaders.

In terms of the MACD which is my favorite technical trigger, as with last week all of the growth sectors (communications, tech, discretionary), most of the cyclicals (financials, materials, energy (industrials are neutral)), but just one defensive (real estate) are in bullish configurations (“go long” and rising). Staples, healthcare, and utilities are all in the weakest configuration (“go short” and falling). Discretionary and communications are overbought though and in need of a consolidation.

And some more charts and tweets on sectors (most from last week, just leaving up):

Economy

This week it was hard to spin reports as positive or negative for the most part. GDP beat expectations but due to a big inventory build, personal income and spending showed incomes holding up but spending weakening with prices in line but services prices accelerating, PMI’s increased but remained in contraction, durable goods were a big beat but due to aircraft with core business spending contracting for a second month, jobless claims fell but continuing claims increased, new home sales increased but only after downward revisions to previous months, pending home sales increased but remain down over 30% y/y, consumer sentiment improved but remains historically very low. The only unambiguous report (negatively) was LEI’s which continued to fall deeper into recession territory.

And the standard boilerplate on why I care about the economic indicators:

And, again, I follow the economic indicators because stock investing for me (as is probably also the case for most of you) is not my main “job” day-to-day, so I want to be apprised of what’s happening on “Main Street” as much as “Wall Street”. But, also, as I’ve noted too many times to mention, the economy has a direct feed through to stock prices via earnings. Given what you’re buying is a stream of earnings discounted at some multiple, that stream of earnings is pretty important. And every recession has seen actual earnings (not just expectations) decline at least low double digits (even the “mild” recessions and deeper recessions see the -30% or more area). So that’s why it’s important for us to pay attention to whether a recession is coming (unless this time is different). What we’ve seen so far does not qualify as a recession to me (or most economists). But if we do enter into a recession, it’s important to note that not only have stocks never bottomed in advance of a recession, but on average they don’t bottom until nine months after one has started. Of course, we’ve never seen a recession forecast so far in advance as this one, so it’s also possible, like most things this cycle, that you can throw the history book out the window in terms of when the bottom will (or has) occur vis-à-vis the recession starting.

As the Atlanta Fed GDPNow model, which did a decent job of tipping a strong 4Q number has turned to 1Q23 with a small increase.

While the Weekly Economic Index (WEI), an index of ten daily and weekly indicators of real economic activity scaled to align with the four-quarter GDP growth rate, which had fallen for the most part since February until Dec 10th when it started moving higher, getting up to 2.05% in GDP growth over the next 12 months three weeks ago but plummeted last week to +0.87%, fell further to +0.71%, the lowest since March 2021. It remains well below the 13-week trendline of 1.46%. It was 2.35% end of October, 6.16% February 19th (the peak in 2022), and 4.94% a year ago.

The decrease in the WEI for the week of January 21 (relative to the final estimate for the week of January 14) is due to falls in retail sales, railroad traffic, electricity output, and fuel sales, which more than offset increases in steel production, tax withholding, and consumer confidence and a decline in initial unemployment insurance claims.

And here’s is Goldman’s latest.

While it looks like some economists might be coming around to my thinking that a recession isn’t a done deal. Argus.

According to Reuters, the latest survey of businesses by the National Association of Business Economics (NABE) indicated a 56% possibility that the economy was in, or will be in, a recession this year versus a nearly two-thirds possibility at the time of the last survey.

The report also showed labor pressures easing and more optimism on profits. BBG.

A new survey of business economists suggests US job market conditions are beginning to soften, with firms indicating an easing of labor shortages and a pullback in hiring expectations. A National Association for Business Economics survey showed about a third of respondents say their firms are not facing any labor shortages, and nearly 20% expect employment at their company to fall in the coming months. “For the first time since 2020, more respondents expect falling rather than increased employment at their firms in the next three months,” NABE President Julia Coronado, founder and president of MacroPolicy Perspectives LLC, said in a statement. “Fewer respondents than in recent years expect their firms’ capital spending to increase in the same period.” Only 12% of those surveyed think headcount will rise in the next three months — less than half the share that said their companies had increased employment over the past three months. The survey of 60 NABE members was conducted Jan. 4-11. That said, respondents are slightly more optimistic about future profits, with over half expecting margins to remain unchanged in the next three months, and a smaller share expecting them to decline.

Up Next

But others agree the risk seems to be falling.

As do markets (also seem to agree the risk of recession has fallen).

Although that’s not atypical heading into a recession (“one final bounce”).

And even the more bearish are acknowledging the strength in pushing out their recession calls.

Morgan Stanley economists are sticking by their call for a “softish” landing in the US and reckon even if there is a recession it will be milder than most. In a Monday report to clients, economists led by Seth Carpenter said “it is far too soon to declare victory” given higher Federal Reserve interest rates take time to bite. But the US labor market has proved stronger than anticipated and “inflation has turned down decisively,” they said. “We continue to think that even if our baseline view is wrong, any recession that might come this year would likely be shallow,” the economists wrote. “A far cry from the 2008 recession to be sure, and probably mild even relative to the 1991 and 2001 recessions.” Among the reasons for that optimism: Businesses are loathe to lay off workers after discovering how hard it is to hire and corporate balance sheets are in strong shape so a credit crunch can be avoided. While a global slowdown is also underway, “it’s not looking like a disaster,” the Morgan Stanley economists said.

And we got some more regional PMI reports.

The Richmond Fed Mfg index fell under expectations with new orders falling sharply. Each of its three component indexes: shipments, new orders, and employment declined, with the index for new orders plummeting from −4 to −24 in January. Employment also turned mildly negative (orange line). More positively, prices continued to decelerate.

Fifth District manufacturing firms reported some deterioration in business conditions in January, according to the most recent survey from the Federal Reserve Bank of Richmond. The composite manufacturing index fell noticeably into negative territory, decreasing from 1 in December to −11 in January. Each of its three component indexes: shipments, new orders, and employment declined, with the index for new orders plummeting from −4 to −24 in January. Alongside a slightly negative employment index, the wage index increased from 37 to 41 in January. The local business conditions index also decreased somewhat, moving further into negative territory with a reading of −13 in January. Although the local business conditions expectations index rose slightly from December, firms generally reported pessimism about conditions over the next six months. January survey results indicated continued easing of supply chain constraints. The index for order backlogs retreated further into negative territory, indicating that businesses continued to see declining backlogs. Meanwhile, the index for vendor lead time also remained well below 0, suggesting a continued decline in lead times. The average growth rates of both prices paid and prices received decreased in January. Expectations for both price growth measures over the next 12 months also decreased to a level much lower than last year.

While the service sector report also remained in contraction territory but in this case improving slightly. Employment was positive here but prices paid also accelerated slightly.

Fifth District service sector activity improved slightly but remained soft in January, according to the most recent survey by the Federal Reserve Bank of Richmond. The revenues and demand indexes both rose to −6 from −12 and −8, respectively, in December. Firms' expectations for revenues and demand over the next six months also improved somewhat in January. Similarly, firms' assessments of current and anticipated local business conditions improved slightly but remained low. Most firms reported continued spending in capital, equipment/ software, and services, but the share of firms increasing capital and equipment/software spending decreased from last month. A larger share of firms reported increased hiring in January, with the employment index rising from −2 to 9. Nonetheless, firms' ability to find workers with the necessary skills saw little improvement as the index remained unchanged at −10 in January. Firms continued to increase wages and expect further wage increases in the near term. Average growth in prices paid increased slightly in January, while growth in prices received decreased somewhat. Firms expect both to moderate over the coming year.

And we also got the Philly Fed services index which also improved to +12.7 from +8 in December. The indexes for general activity at the firm level, sales/revenues, new orders, and full-time employment all rose. Firms continued to report overall increases in both prices paid and received; however, increases in prices paid were less widespread than in recent months. The respondents continue to anticipate growth over the next six months.

And the Chicago Fed does a sort of PMI on economic conditions which improved in January from its most negative since the pandemic but remaining well under the 0 dividing line of increasing versus decreasing economic activity. The outlook though deteriorated with 59% of respondents expecting lower economic activity over the next year.

The Chicago Fed Survey of Economic Conditions (CFSEC) Activity Index increased to –27 in January from –40 in December, suggesting that economic growth was well below trend. The CFSEC Manufacturing Activity Index increased to –16 in January from –44 in December, and the CFSEC Nonmanufacturing Activity Index increased to –31 in January from –38 in the previous month.

• Respondents’ outlooks for the U.S. economy for the next 12 months deteriorated slightly, and remained pessimistic on balance. Fifty-nine percent of respondents expected a decrease in economic activity over the next 12 months.

• The pace of current hiring decreased, as did respondents’ expectations for the pace of hiring over the next 12 months. Both hiring indexes remained negative.

• Respondents’ expectations for the pace of capital spending over the next 12 months increased, but the capital spending expectations index remained negative.

• The labor cost pressures index increased, as did the nonlabor cost pressures index. The labor cost pressures index moved into positive territory, while the nonlabor cost pressures index moved up to a neutral value

But overall according to Goldman forward looking components are “firmly in expansion territory”.

And I like to look at the credit card company reports. Here’s some takeaways. BBG.

Visa Inc. and Mastercard Inc. saw purchase volumes on their cards climb less than expected in the final three months of the year, a sign that historic levels of inflation have begun to put a damper on consumer spending. Spending on Visa’s cards climbed 1.7% to $3.01 trillion in the company’s fiscal first quarter, missing the $3.16 trillion average of analyst estimates compiled by Bloomberg. At Mastercard, volumes jumped 11% to $1.73 trillion, also missing estimates. So far, both companies have said inflation hasn’t weighed on consumers’ overall spending patterns. Instead, card customers have shifted their spending to lower-cost items or generic brands. The two companies have said they continue to get a boost from spending on travel and dining out with pandemic-related restrictions easing globally. “As we look at the broader economy, we see the continued recovery of cross-border travel, with volumes up 59% versus a year ago and we’re encouraged by Asia opening up further,” Mastercard Chief Executive Officer Michael Miebach said in a statement announcing his company’s fourth-quarter results earlier Thursday.

While total volume on AmEx’s network increased less than expected in the final three months of last year, the record number of new cardholders AmEx added in 2022 should help revenue climb as much as 17% in 2023, the company said. That’s higher than the 11% analysts in a Bloomberg survey were expecting. “It’s a premium customer base, and that premium customer base, while not immune to economic downturns, certainly right now is spending on through,” Chief Executive Officer Stephen Squeri said on a call with analysts Friday. “This is a premium card member base that appreciates premium products and is spending.”

And in a sign of the pressures of high interest rates and a cooling economy, more Americans are falling behind on their car payments than during the financial crisis. I think this is being exacerbated by last year’s sky-high prices which resulted in many car owners now underwater on their loans. BBG.

In December, the percentage of subprime auto borrowers who were at least 60 days late on their bills rose to 5.67%, up from a seven-year low of 2.58% in April 2021, according to Fitch Ratings. That compares to 5.04% in January 2009, the peak during the Great Recession. The average new auto loan rate was 8.02% in December, up from 5.15% a year earlier, according tao Cox Automotive. The rate can be much higher for subprime borrowers. While the number of vehicle repossessions is rising, it’s still below pre-pandemic levels. At Manheim, an auto auction company, the number of repossessed cars increased 11% in 2022 compared to the prior year, but that was still down 26% from 2019.

Real Estate

As Mike Simonsen after seeing glimmers of hope in his data last week sees more this week.

And the largest homebuilder is optimistic.

And even John Burns who has been pretty bearish almost sounded constructive.

And building costs are also coming down.

And I also noted in the Economic section the housing reports which had some indications of potential stabilization in the housing market. Redfin also reports signs of recovery.

The housing market has begun to recover after hitting a low point in the second week of November. We’re not out of the woods yet, but homebuyers are coming off the sidelines: The number of Redfin customers requesting first tours has improved 17 percentage points from the November trough, and the number of people contacting Redfin agents to start the homebuying process has improved 13 points. Compared with a year ago, home tours and requests for service are down 23% and 27% respectively, but that’s an improvement from the November trough, when both were down 40%. This is already translating into more home sales. Redfin agents report that bidding wars are back in some markets, including Seattle, central Florida and Richmond, VA. Homebuyer demand remains down from its early 2022 highs, but the market has shifted into a new phase and well-priced listings are selling quickly.

Buyers have acclimated to the 6% mortgage rate, which feels like a relief after watching affordability erode as rates surpassed 7% in the fall. Some buyers are even scoring a rate that starts with a five, an important psychological threshold, while others are opting for an adjustable-rate mortgage or getting a rate buydown as a seller concession. While demand is coming back in some pockets of the country, it’s selective: Homes that are eliciting bidding wars tend to be affordable, suburban, single-family, move-in ready and most importantly, priced competitively. Most everything else is sitting. Even though homebuyer demand is improving, the main factor driving bidding wars is low inventory. It’s not surprising that sellers are slower to embrace the shifting market, as buyers tend to react first to falling mortgage rates, with sellers following suit months later. This effect is likely to be pronounced in 2023: Would-be sellers are more sensitive to elevated rates because 85% of mortgage holders have a rate far below today’s level of roughly 6%. This “lock-in” effect and still-high rental prices are motivating many potential move-up buyers to become landlords instead of home sellers. Redfin agents have also observed in their conversations with homeowners that there’s fear around listing at a time when home-price growth has been shrinking and buyers are regaining power.

Condos and higher-priced homes are still a struggle to sell. Redfin agents report that sellers of expensive homes and condos are offering buyers incentives to close deals.

The factor most likely to slow or reverse the housing market recovery is that there are too few homes for sale, which could hold back total sales volumes and price people out of homebuying. Even though housing costs are declining, they remain significantly higher than they were two years ago. Home prices will likely be sticky this year in many places where there are still plenty of stale listings; once they finally sell they will hold back price growth while overall low inventory keeps prices from going down much.

And after the huge jump (28%) in the prior week, the weekly MBA Mortgage Applications Index saw another fairly large jump in the third week of January (+7%) led by refis (+15%). Purchases though fell -1% w/w. They are down -77% and -39% y/y respectively. This week’s results included an adjustment for the observance of Martin Luther King, Jr. Day.

US MBA Mortgage Applications Jan 20: 7.0% (prev 27.9%) - US 30-Yr MBA Mortgage Rate Jan 20: 6.20% (prev 6.23%)

“Mortgage rates declined for the third straight week, which is good news for potential homebuyers looking ahead to the spring homebuying season. Mortgage rates on most loan types decreased last week and the 30-year fixed rate reached its lowest level since September 2022 at 6.2 percent,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “Overall applications increased with both gains in purchase and refinance activity, but purchase applications remained almost 39 percent lower than a year ago. Homebuying activity remains tepid, but if rates continue to fall and home prices cool further, we expect to see potential buyers come back into the market. Many have been waiting for affordability challenges to subside.” Added Kan, “Despite a 15 percent increase in refinances, they were still 77 percent behind last year’s pace, as rates remained more than two percentage points higher, thus providing very little refinance incentive for most borrowers who are locked into lower rates.” ... The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($726,200 or less) decreased to 6.20 percent from 6.23 percent, with points increasing to 0.69 from 0.67 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

And some charts from Goldman on the housing market.

And more evidence of the convergence of low and high priced sales.

And apartment leasing perhaps has bottomed as well.

As delinquencies remain low.

While over in the commercial area the Architecture Billings Index (ABI) from the American Institute of Architects (AIA) remained in contraction territory in December although improving slightly to 47.5 from 46.6 (any score below 50 indicates a decline in firm billings). Inquiries into new projects posted a positive score of 52.3, however new design contracts remained in negative territory with a score of 49.4.

“Despite strong revenue growth last year, architecture firms have modest expectations regarding business conditions this coming year,” said AIA Chief Economist Kermit Baker, PhD, Hon. AIA. “With ABI scores for the entire fourth quarter of 2022 in negative territory, a slowdown in construction activity is expected later this year, though the depth of the downturn remains unclear.”

Regional averages: Midwest (49.4); South (48.6); Northeast (46.5); West (45.5)

Sector index breakdown: mixed practice (54.8); institutional (47.3); commercial/industrial (45.2); multi-family residential (44.3)

The regional and sector categories are calculated as a three-month moving average, whereas the national index, design contracts and inquiries are monthly numbers.

Subscribe for free to receive new posts and support my work.

Commodities/Currencies/Bonds

Bonds/Rates/Credit

The big events for the bond markets this week were the GDP and PCE reports (and perhaps the inflation expectations) which all came in pretty much as expected (although services prices in the PCE report were a little elevated as discussed in that report). So it’s not a big surprise that yields didn’t do much this week. The 10-yr ended at 3.52%, and the 2-yr 4.21%.

Which saw the 2-10 curve remain inverted but off the most negative levels (but still the lowest since the ‘80’s , while the 3 mos/10 yr curve (generally considered a better recession indicator than 2/10), remained at “since-1981” extremes and will continue to become more inverted as short rates will continue to climb until the market is convinced the Fed is done hiking.

And breakevens continue to remain very subdued.

But not all are so sanguine. BBG.

Some of the world’s largest asset managers such as BlackRock Inc., Fidelity Investments and Carmignac are warning markets are underestimating both inflation and the ultimate peak of US rates, just like a year ago. “Inflation is here to stay,” said Frederic Leroux, a member of the investment committee and head of the cross asset team at €44 billion ($47 billion) French asset manager Carmignac in a phone interview. “After the crisis central bankers thought they could decide the level of interest rates. In the past two years they realized they don’t: inflation does.” He added that one of the biggest mispricings in the market today is the expectation that inflation will come down to 2.5% next year, before adding that the world is entering a macroeconomic cycle comparable to between 1966 and 1980. That period saw energy shocks that drove US inflation into double digits twice.

Analysts at BlackRock’s Investment Institute also see high inflation persisting, with little hope that a recession will spur the Fed to cut rates. Instead, they expect the Fed to taper its outsized hikes into smaller ones as the pain of the economic slowdown becomes clear, even if inflation stays above the bank’s 2% target. “Central banks are unlikely to come to the rescue with rapid rate cuts in recessions they engineered to bring down inflation to policy targets. If anything, policy rates may stay higher for longer than the market is expecting,” a team of analysts including Jean Boivin, the head of the Institute, wrote last week. BlackRock is underweight developed market equities and it prefers investment-grade credit to long term government bonds.

Not all funds agree of course. Dutch asset manager Robeco, with €246 billion under management, takes the view that 2023 will be the peak for rates, the dollar and also inflation. This is mainly because of its expectations for a recession and policy makers’ inability to engineer a soft landing, which it thinks will spark rate cuts.

Personally, I think this (whether inflation continues to head lower and can crack under the 3-4% area) along with earnings are the biggest stories for 2023 outside of the Ukraine war (due to its global implications). I had been saying for much of December that I thought yields were too low if the Fed is going to 5%. I had said I would not be surprised to see the 10-year hit 4% and the 2-year at least 4.75 if not 5%. Remember the 2-year has never peaked below the ultimate terminal rate. The peak in the 2-year so far has been 4.73%. That said, as I noted two weeks ago Bloomberg Intelligence believes if the terminal rate were to be 5.5% their model says fair value on a two-year would be 4.6%. That combined with market expectations that the Fed won’t get over 5% has me starting to think we might have seen the peaks in rates. And as I noted last week more strategists agree with that view. Bloomberg sees 3% in the 10-year by year-end and Morgan Stanley now 3.15%. That would be great, but as of now I remain unconvinced, and I think it’s not unlikely the Fed holds rates at or around 5% through 2023 which I think will at some point pull up those rates. This is why inflation reports will remain a top data point this year.

In terms of expectations regarding the Fed, the expected terminal rate pricing remained around 4.9% this week. Swap traders continue to see a peak in March, although the percentage seeing no hike in March fell slightly to 15% from 20% last week although up from 10% two weeks ago. The first cut though remains in November, something I’m quite sure Jerome Powell will be looking to push out Wednesday. The February meeting is a done deal on a 25bps hike as I noted last week. More interesting will be the press conference and the discussion around “how high” and for “how long” (in particular will Powell commit to another hike at this point or keep it “data dependent”). In terms of how long as noted he’ll try to make it clear the Fed has no intention of cutting anytime soon to try to talk down the markets. For sure he will be looking to avoid anything that will further rally the stock and bond markets further loosening financial conditions (noted later). You’re likely well apprised of the run equities have had in January, but bonds have as well with benchmark 5- and 10-year yields having dropped around 40 basis points in January.

And as we move through the year, here are a couple of Fed cheat sheets that I’ll keep up.

And this is an interesting development. We’ll have to see how it unfolds.

And financial conditions continue to ease.

Something Larry Summers says the Fed should be concerned about. HR.

Summers … flagged the recent easing in financial conditions documented above. “In a way, the monetary impulse that’s coming into the economy is much less contractionary than you would think just looking at Fed funds,” he said, calling that something the Fed may want to be concerned about.

As interest rate volatility continues to move lower which should hopefully help liquidity.

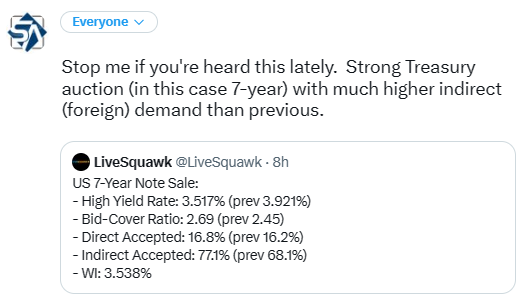

And the strong Treasury auctions continued this week.

And saw this interesting chart this week. I hadn’t realized how much Chinese holdings of Treasuries had dropped in 2022. Would argue that this is likely closer to the end than the beginning of this process (and perhaps them coming back into the market is part of what we’re seeing commensurate with their reopening).

The data on China’s Treasury holdings isn’t complete given the role of custody accounts, but the trend is certainly lower. At $870 billion, the total pile attributed to China by the Treasury department is down by a third over the past decade.

But some of that buying is also from pension funds. This though could be a headwind for equities. BBG.

“Asset managers came into the year with large cash balances and there is a little bit of a ‘get in now before its too late’ sentiment,” said Alexandra Wilson-Elizondo, head of multi-asset retail investing at Goldman Sachs Asset Management. Investors are seeing global disinflation signs, some weaker data and “if history is a guide it shows that turning points can be abrupt.” That bullish mood was underscored this week when investors bought much bigger slices of new Treasury debt sales than is typically seen, locking in yields that remain near the higher end of the range seen over the past 15 years. At current levels, Treasuries are seen as an attractive hedge against a recession That macroeconomic outlook is expected to keep benchmark yields rangebound, supported by the twin forces of moderating price pressures and employment growth.

“The pensions are in good shape. They can now essentially immunize — take out the equities, move into bonds and try to have assets match liabilities,” Mike Schumacher, head of macro strategy at Wells Fargo, said in an interview. “That explains some of the rallying of the bond market over the last three or four weeks.” An irony of pension accounting is that a year like last year, with its twin routs in stocks and bonds, can be a blessing of sorts to some benefit plans, whose future costs are a function of interest rates. When rates climb, their liabilities shrink and their “funded status” actually improves. Even as markets suffered their worst year since the financial crisis, corporate plans reaped a windfall as aggregate liabilities fell by $493 billion, more than enough to offset investment losses of $321 billion. The largest 100 US corporate pension plans now enjoy an average funding ratio of about 110%, the highest level in more than two decades, according to the Milliman 100 Pension Funding index. That’s welcome news for fund managers who suffered years of rock-bottom interest rates and were forced to chase returns in the equity market. Now, they have an opportunity to unwind that imbalance and Wall Street banks pretty much agree on how they’ll use the extra cash to do it: buying bonds, and then selling stocks to buy more bonds.

Pension funds need to keep some exposure to stocks to boost returns, but that equation is changing. Once a corporate plan reaches full funding, their aim is often to derisk by jettisoning stocks and adding fixed income assets that line up with their liabilities. With the largest 100 US corporate defined benefit funds riding a cash pile of $133 billion after average yields on corporate debt more than doubled last year, their path is wide open. JPMorgan’s strategist Marko Kolanovic estimates derisking will lead pension managers to buy as much as $1 trillion of bonds; Bank of America’s Braizinha says a $500 billion buying spree is closer to the mark. If pension fund managers increase their allocation by 3% to 4% it would translate into $1 trillion of bond purchases, according to JPMorgan calculations. Even a 6% increase isn’t out of the question, according to the firm’s strategists.

And PIMCO also likes bonds. BBG.

There’s “a strong case for investing in bonds” as a recession looms this year, fixed-income investing giant Pacific Investment Management Co. says in a new report. The bond manager has a baseline outlook for “a modest recession and moderating inflation,” an environment in which bonds have “the potential for both attractive returns and mitigation against downside risks.” US core bond funds that yield 5.1% or higher “may offer additional downside mitigation versus outer-circle assets in the event of worse outcomes,” Pimco says. Pimco advocated being neutral on interest-rate risk and expects a yield range of about 3.25% to 4.25% for the 10-year US Treasury. The outlook for US mortgage backed securities is solid, and “an expected decline in interest rate volatility would support MBS.”

As the NY Fed’s latest corporate bond indicators continues to see a healthy market.

Corporate bond market functioning appears healthy, with the overall market-level CMDI around its historical 30th percentile.

Market functioning in the investment-grade segment continued to improve in January and is now below its historical 75th percentile.

As Morgan is cautious on junk debt (as am I).

Dollar (DXY)

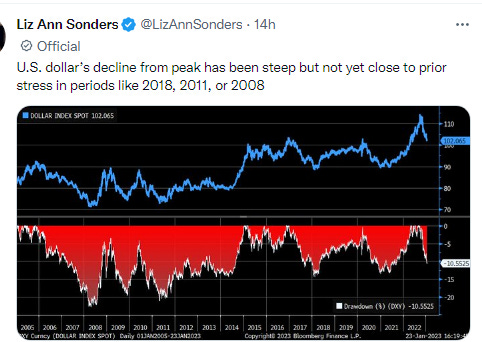

The dollar finished the week just above its 6-month closing low reached earlier in the week remaining at the bottom of its recent range and just above my target. That said, the daily technicals are showing signs of turning more supportive. It’s coming up on a key trendline if it can continue moving sideways. A lot of resistance overhead though, and for now the overall trend is down.

VIX

The VIXfell for most of the week again at one point touching the lowest level in over a year before recovering to close around the 52-week closing lows.

Crude (/CL)

I noted a week ago that WTI had gotten to my $83 area target but had stalled. I said “for now, I think it has a decent chance to move through that resistance. If not it might pull back to the uptrend line.” And so it did neither instead continuing to pound against the 100-DMA but not above to close above it. Daily technicals remain positive, but they’re starting to weaken, so now I’m starting to wonder if it will get through as I had been more confident about earlier in the week. The 100-DMA is proving very difficult to crack.

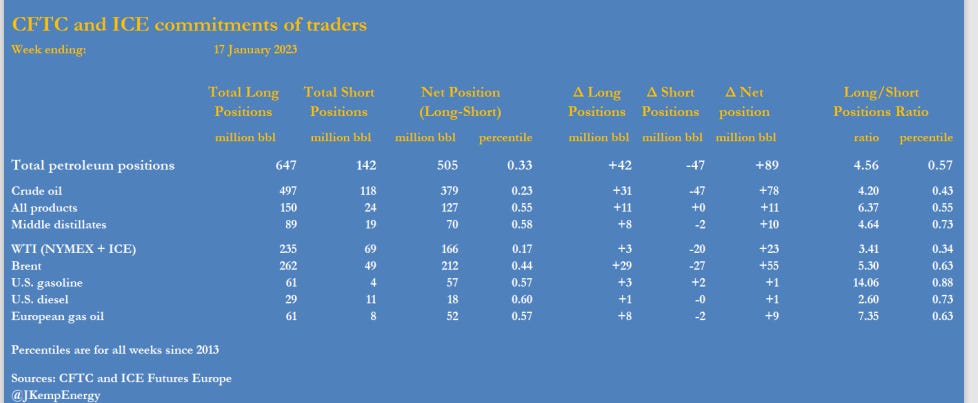

And for a third week money managers were buying although also for a third week it was mostly Brent (which now has the net positioning in Brent well above WTI as discussed below).

Overall positioning still remains historically (last 10 years) low although now definitely off the bottom. Coming into the week net positioning (longs minus shorts) was in the 44th percentile of all years since 2013 for Brent and 17th for WTI. But long/short positioning (my gauge of bullishness) was in the 63rd percentile for Brent and 34th for WTI so a relatively bullish positioning in Brent but no so much WTI.

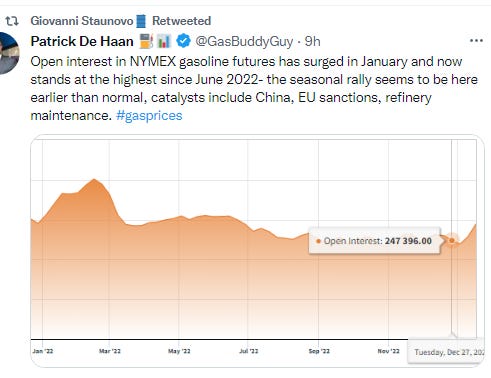

And open interest continues to rebuild which should hopefully dampen volatility (which we saw this week).

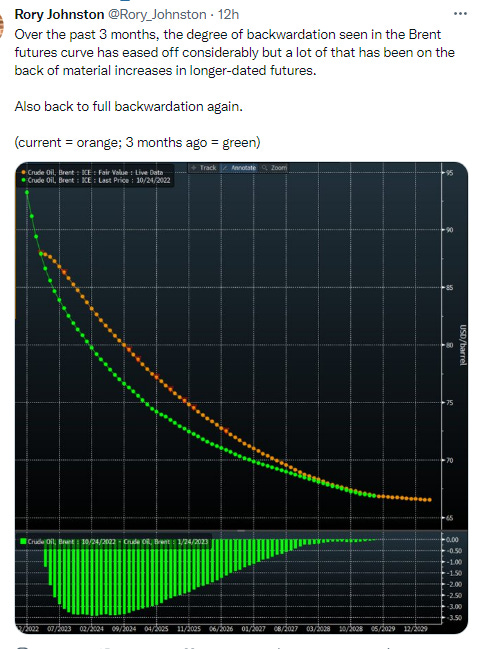

And a more bullish posture was also evidenced by calendar spreads which got back to backwardation across the curve.

But not all are so bullish.

Tuesday - “Crude has been the laggard recently,” while products have been strong, with Europe’s diesel market hit $1,000 yesterday, he said. “Diesel and other products are likely to drag crude up.”

And an interesting catalyst for oil of late.